CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–4A

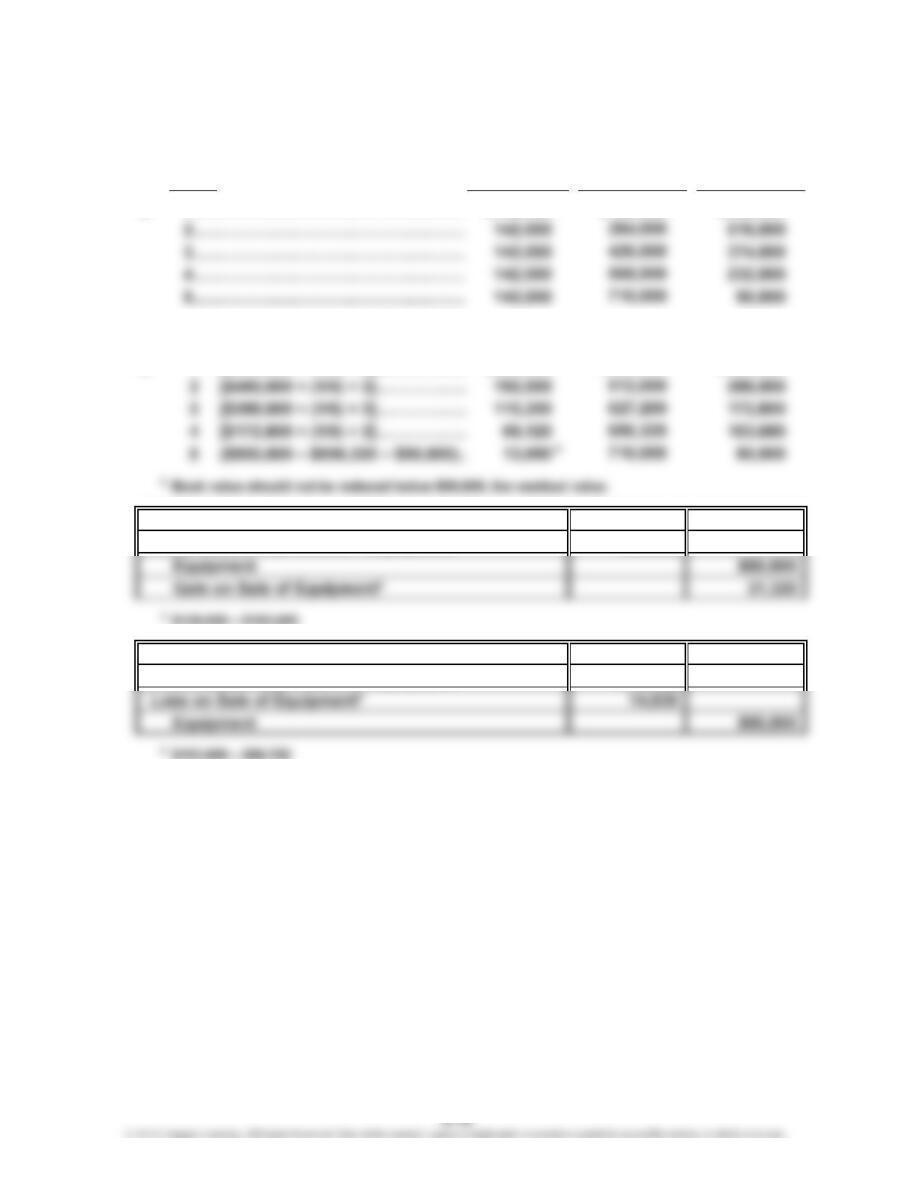

1.

Depreciation Book Value,

Year Expense End of Year

a. 1…………………………………………… $142,000 $658,000

*[($800,000 – $90,000) ÷ 5]

b. 1 [$800,000 × (1/5) × 2]……………

…

$320,000 $480,000

…

…

…

2. Cash

Accumulated Depreciation—Equipment

3. Cash

Accumulated Depreciation—Equipment

Depreciation,

End of Year

88,750

696,320

696,320

135,000

$320,000

$142,000

Accumulated

*

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–5A

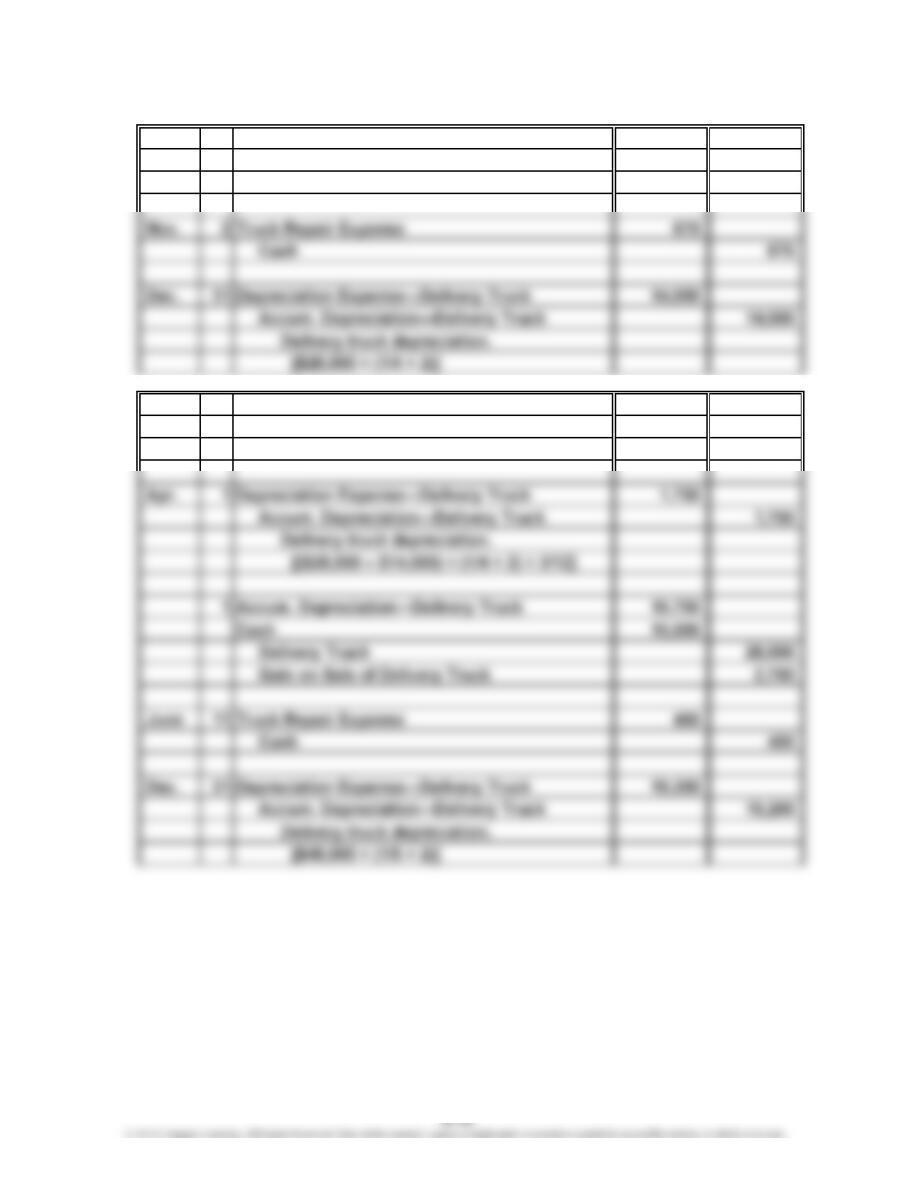

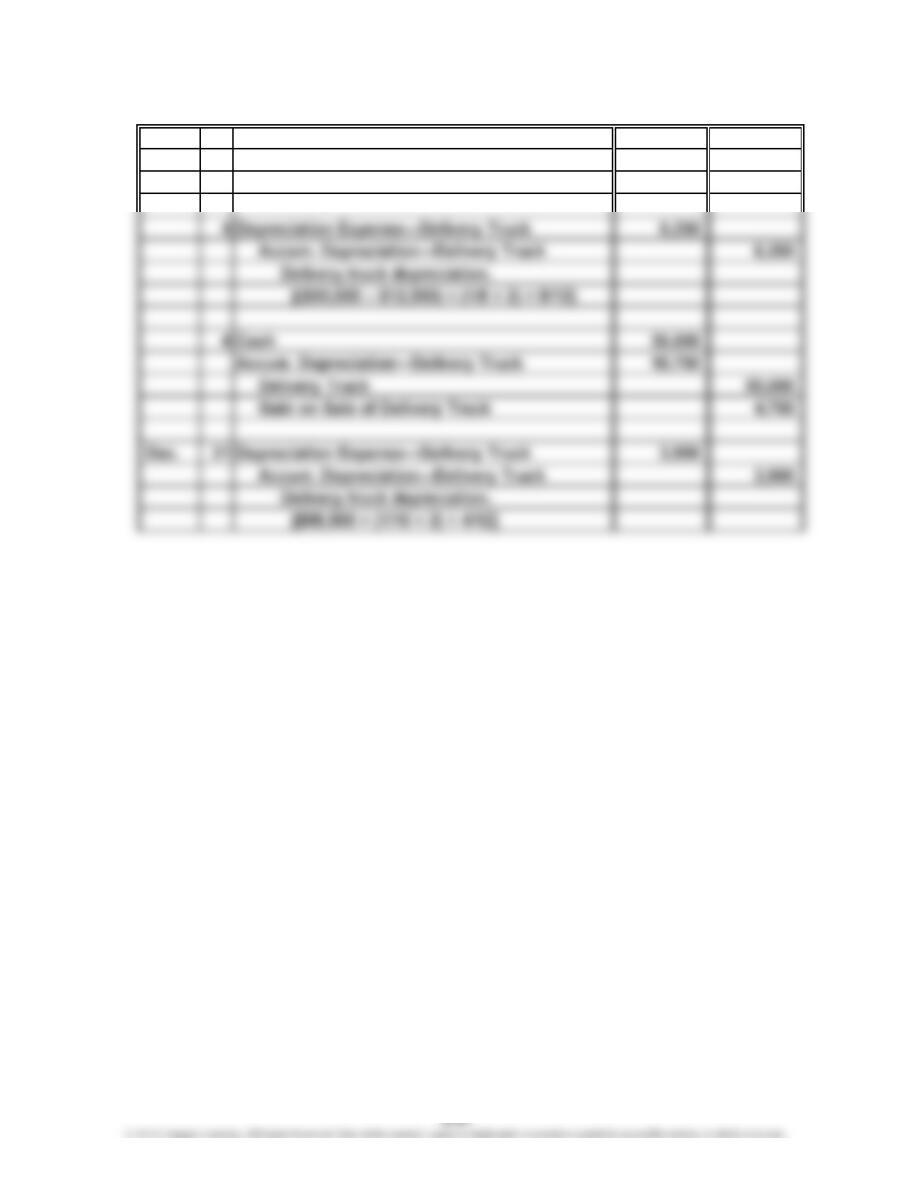

2012

Jan. 4 Delivery Truck 28,000

Cash 28,000

2013

Jan. 6 Delivery Truck 48,000

Cash 48,000

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–5A (Concluded)

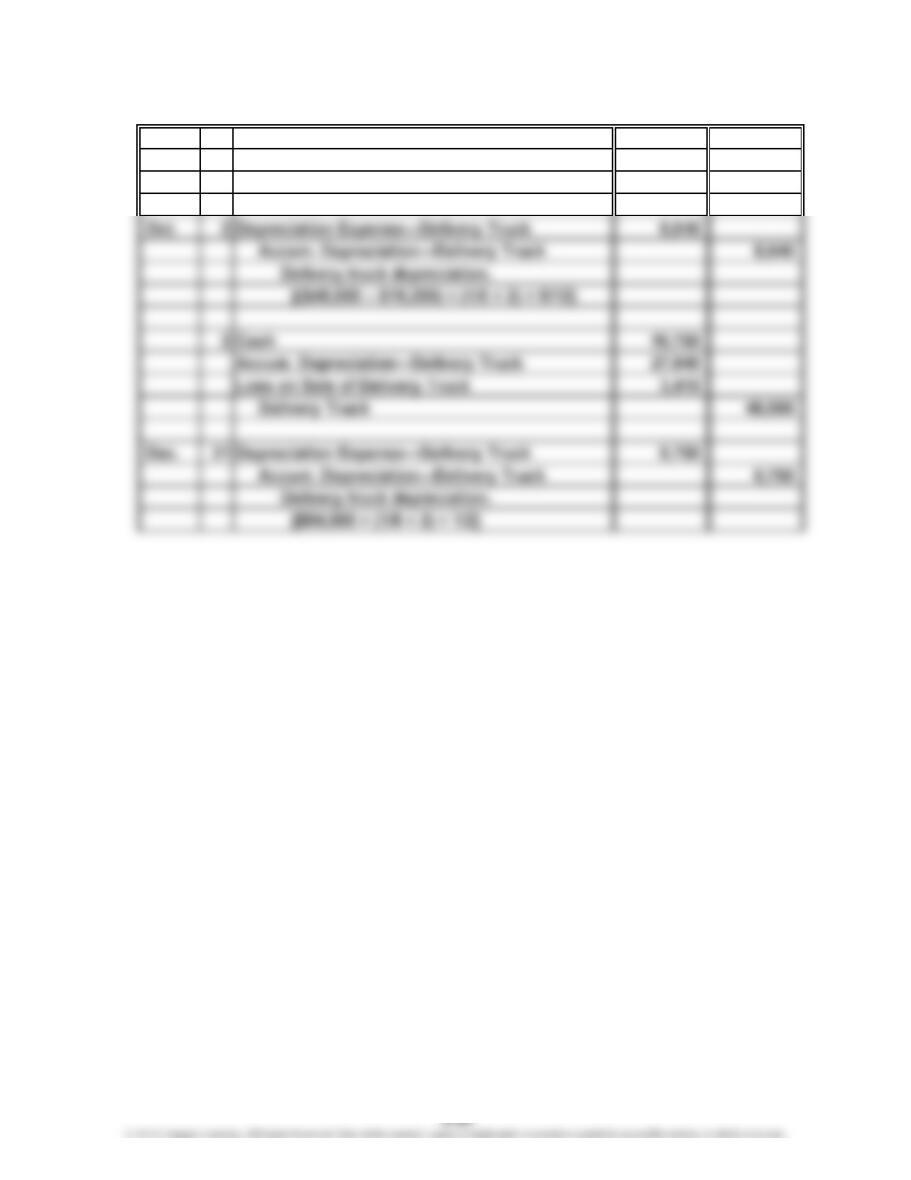

2014

July 1 Delivery Truck 54,000

Cash 54,000

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–6A

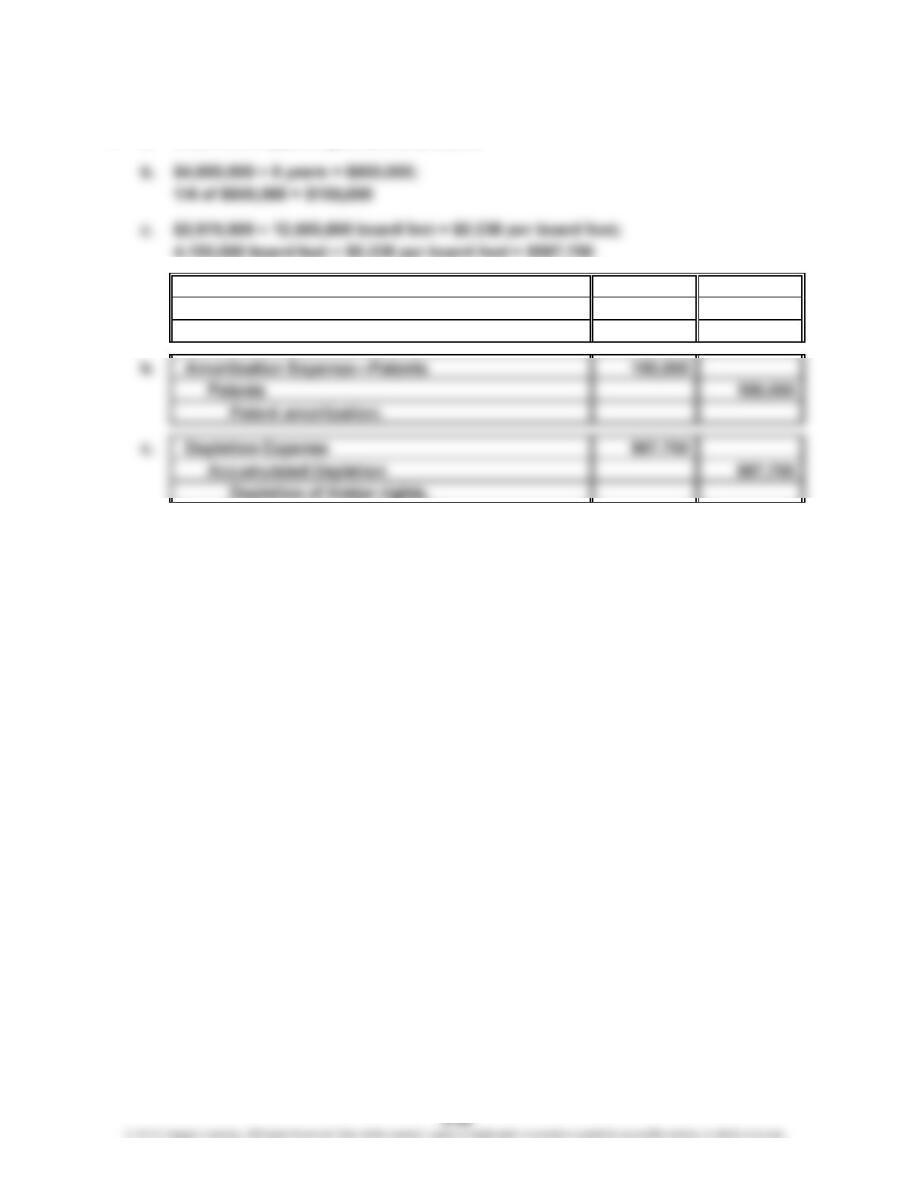

1. a. $1,600,000 ÷ 5,000,000 board feet = $0.32 per board foot;

2. a. Depletion Expense 352,000

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–1B

1. Land Other

Item Land Improvements Building Accounts

a. $ 3,600

b. 780,000

c. 23,400

3. Since land used as a plant site does not lose its ability to provide services, it is

4. Since Land Improvements are depreciated, depreciation expense of $4,320

($21,600 × 1/10 × 2) would be understated and net income would be overstated

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–2B

1.

a. Straight- b. Units-of- c. Double-

Line Output Declining-Balance

Year Method Method Method

2013 $ 71,250 $102,600 $160,000

3. Over the four-year life of the equipment, all three depreciation methods yield

Depreciation Expense

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–3B

a. Straight-line method:

2012: [($108,000 – $7,200) ÷ 3] × 3/12…………………………………………

…

$ 8,400

2013: [($108,000 – $7,200) ÷ 3]…………………………………………………

…

33,600

…

…

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–4B

1.

Depreciation Book Value,

Year Expense End of Year

a. 1……………………………………………

…

$25,625 $84,375

2. Cash

Accumulated Depreciation—Equipment

3. Cash

Accumulated Depreciation—Equipment

Depreciation,

End of Year

10,500

96,250

96,250

18,000

$ 25,625

Accumulated

*

…

…

…

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–5B

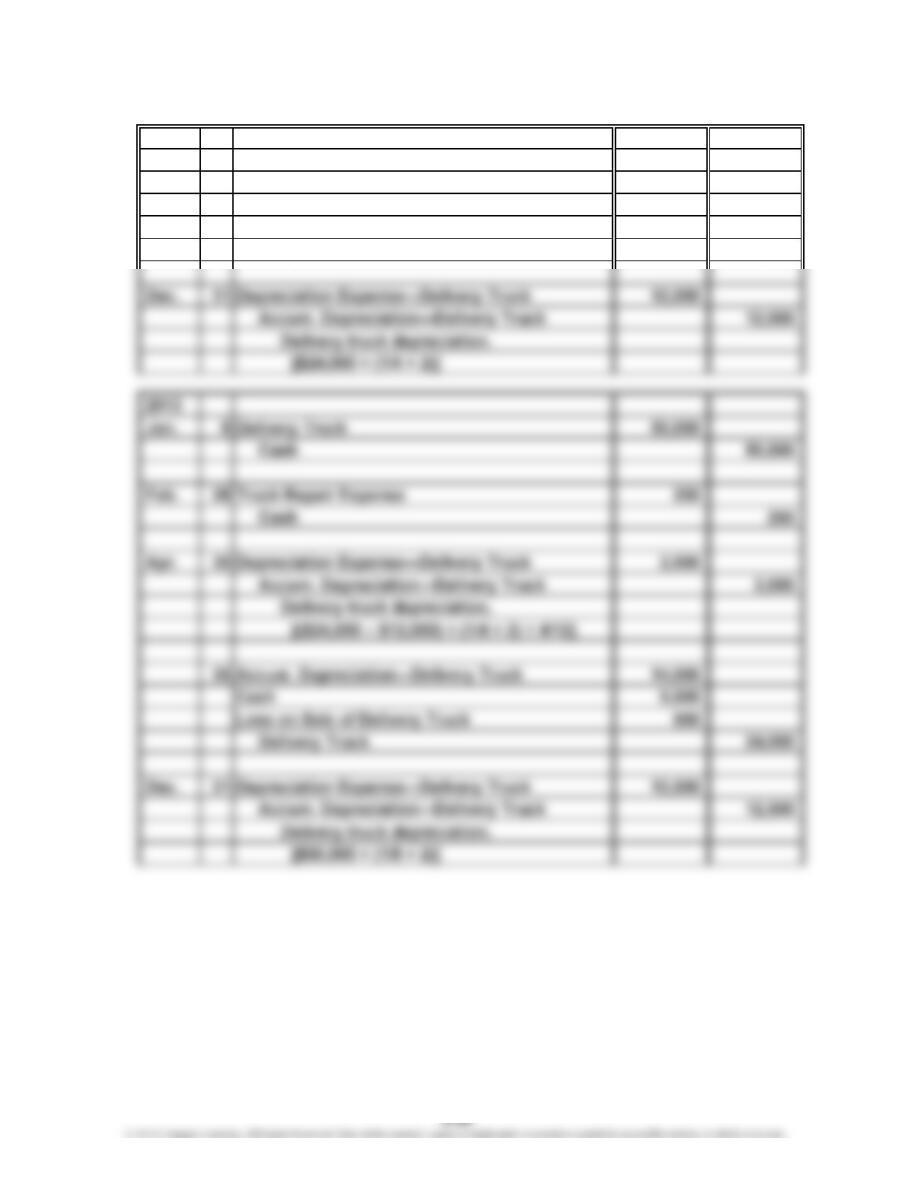

2012

Jan. 8 Delivery Truck 24,000

Cash 24,000

Mar. 7 Truck Repair Expense 900

Cash 900

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–5B (Concluded)

2014

Sept. 1 Delivery Truck 58,500

Cash 58,500

CHAPTER 9 Fixed Assets and Intangible Assets

Prob. 9–6B

1. a. Loss from impaired goodwill, $3,400,000

4,150,000 board feet × $0.238 per board foot = $987,700

2. a. Loss from Impaired Goodwill 3,400,000

Goodwill 3,400,000

Impaired goodwill.

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–1

It is considered unprofessional for employees to use company assets for personal

CP 9–2

You should explain to Nolan and Stacy that it is acceptable to maintain two sets

of records for tax and financial reporting purposes. This can happen when a

company uses one method for financial statement purposes, such as straight-line

depreciation, and another method for tax purposes, such as MACRS depreciation.

CASES & PROJECTS

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–3

1. a. Straight-line method:

2012: ($400,000 ÷ 5) × 1/2…………………………………………………

…

$40,000

2013: ($400,000 ÷ 5)………………………………………………………

…

80,000

…

…

…

…

…

…

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–3 (Continued)

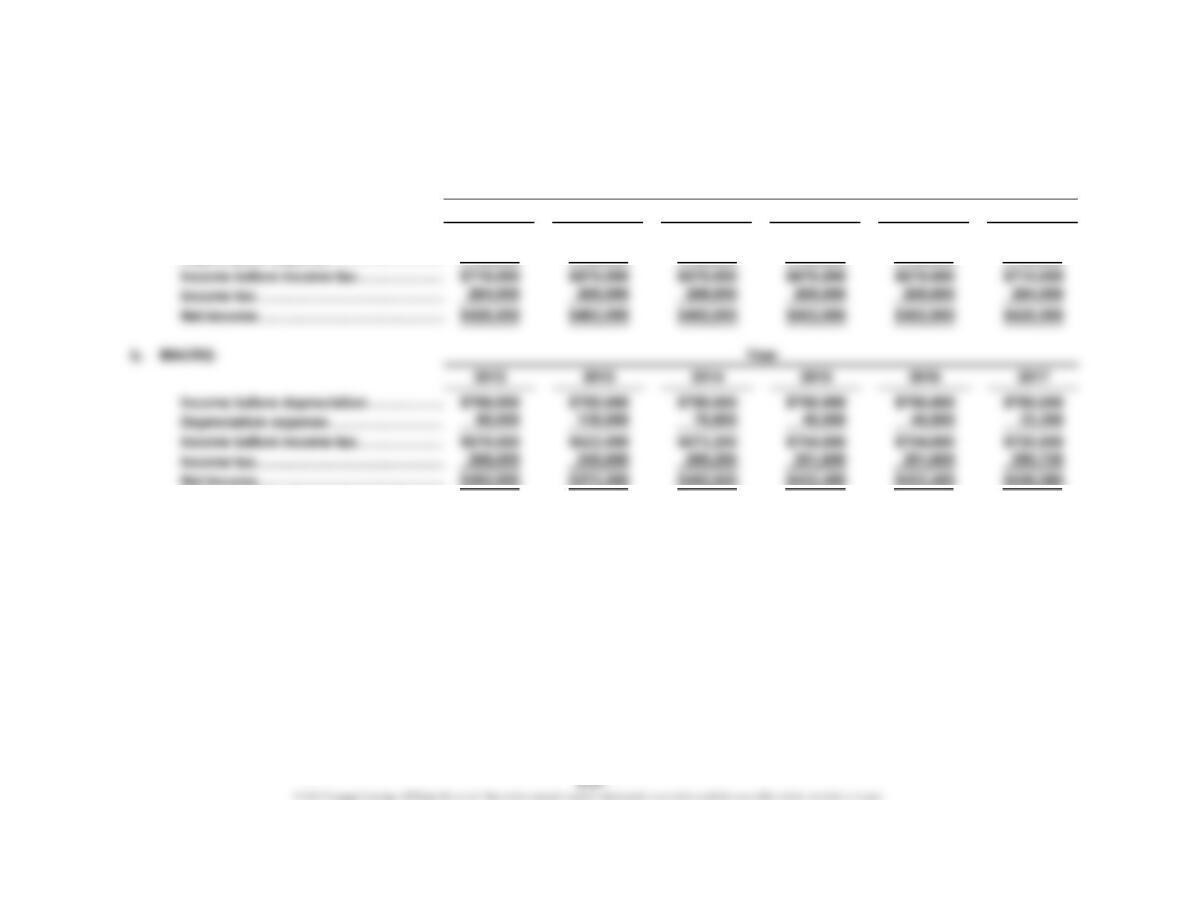

2. a. Straight-line method:

2012 2013 2014 2015 2016 2017

Income before depreciation……………

…

$750,000 $750,000 $750,000 $750,000 $750,000 $750,000

Depreciation expense…………………… 40,000 80,000 80,000 80,000 80,000 40,000

Year

…

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–3 (Concluded)

3. For financial reporting purposes, Tim should select the method that provides

the net income figure that best represents the results of operations.

Note to Instructors: The concept of matching revenues and expenses is discussed

in Chapter 3. However, for income tax purposes, Tim should consider selecting

CP 9–4

Note to Instructors: The purpose of this activity is to familiarize students with the

procedures involved in acquiring a patent, a copyright, and a trademark. You may

wish to divide the class into three groups to report back on patents, copyrights,

and trademarks separately.

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–4 (Concluded)

The application also includes one or more claims, although it is not always a

requirement to submit these when first filing the application. The claims set out

what the applicant is seeking to protect in that they define what the patent owner

Copyright

While copyright in the United States automatically attaches upon the creation of an

original work of authorship, registration with the Copyright Office puts a copyright

holder in a better position if litigation arises over the copyright. A copyright holder

desiring to register his or her copyright should do the following:

CHAPTER 9 Fixed Assets and Intangible Assets

CP 9–5

b. The fixed asset turnover measures the amount of revenue earned per dollar

of fixed assets. Walmart earns $4.01 of revenue for every dollar of fixed assets,

while Occidental earns $0.56 and Comcast Corporation earns $1.60 in revenue

for every dollar of fixed assets. Occidental and Comcast require more fixed

assets to operate their businesses than does Walmart, for a given level of

revenue volume.

Does this mean that Walmart is a better company? Not necessarily. Revenue is

Revenue

Average Book Value of Fixed Assets

=Fixed Asset Turnover Ratioa.