CHAPTER 1 Introduction to Accounting and Business

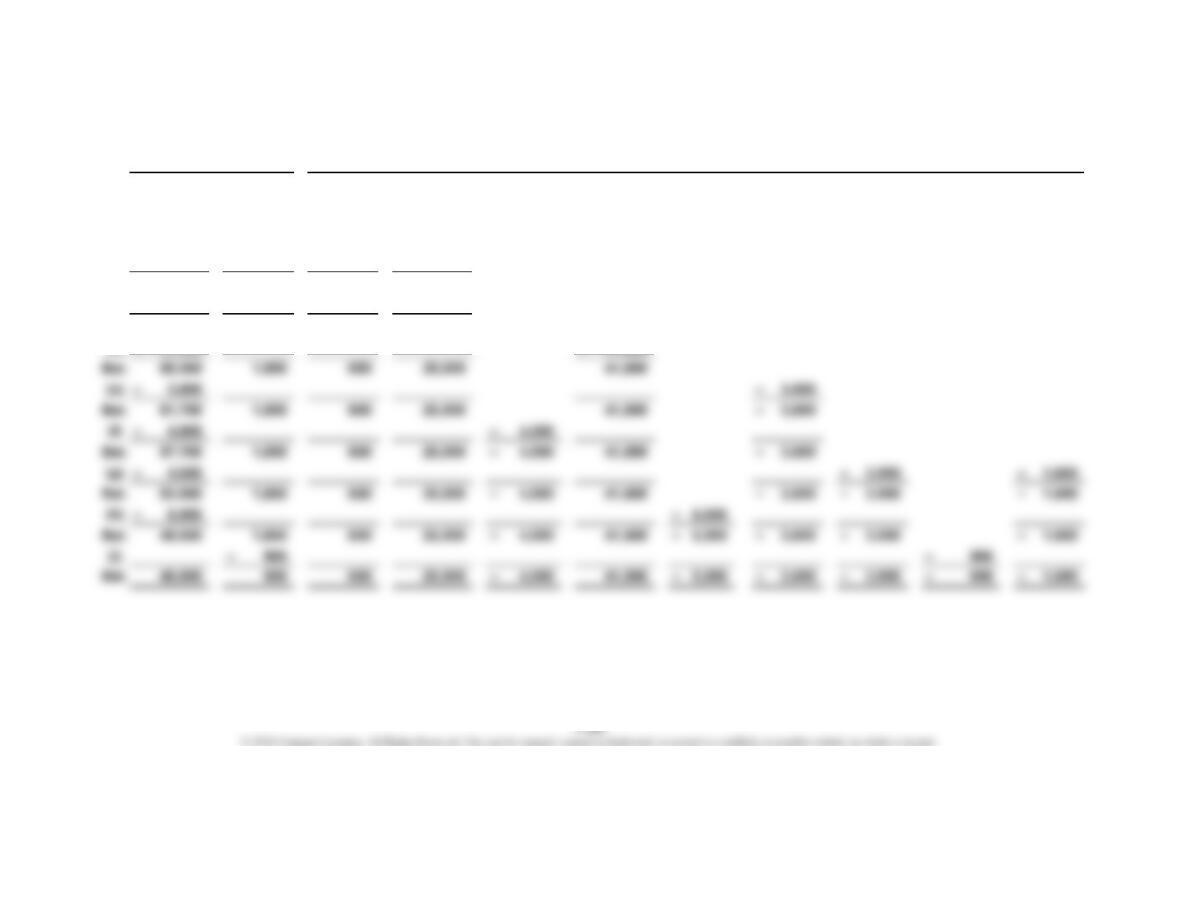

Prob. 1–3A (Concluded)

4. (Optional)

Cash flows from operating activities:

Cash received from customers $110,000

Deduct cash payments for expenses

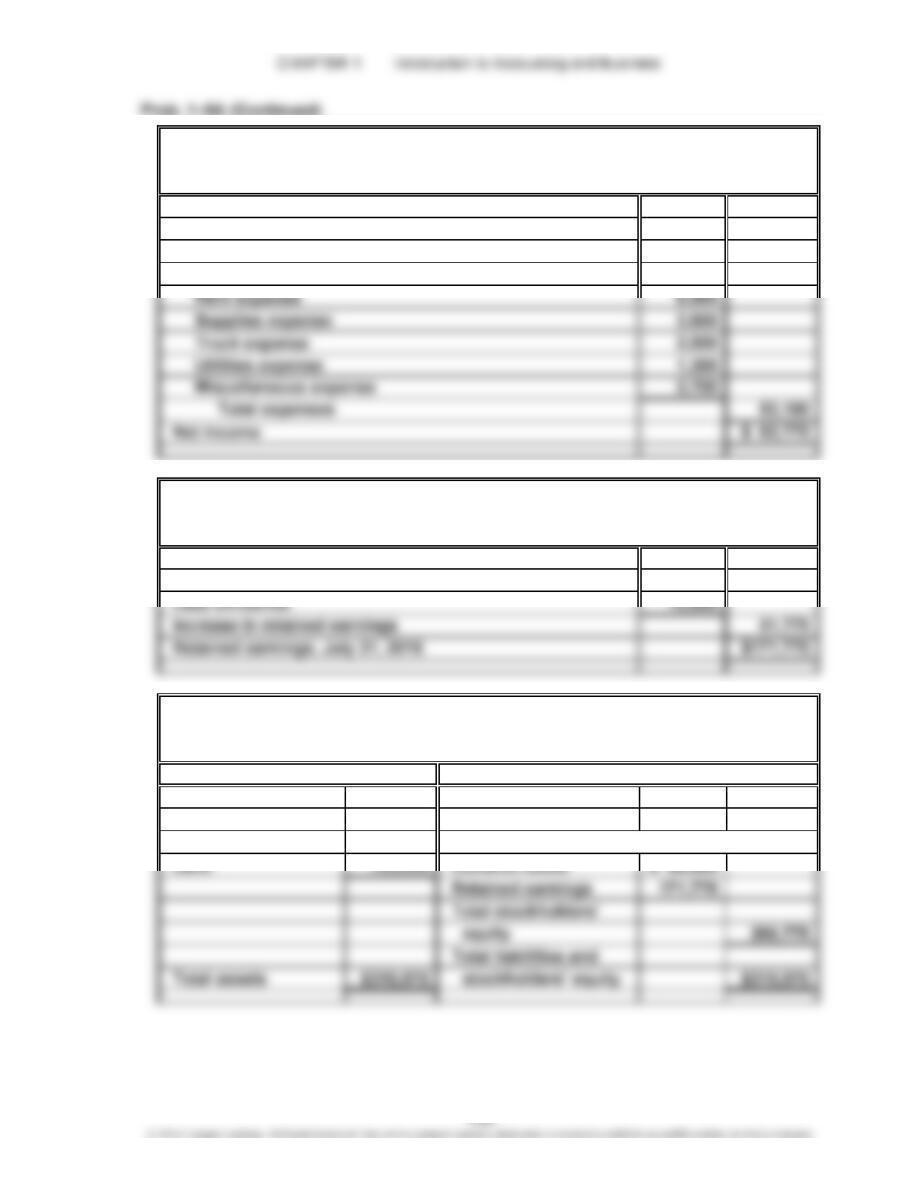

RELIANCE FINANCIAL SERVICES

Statement of Cash Flows

For the Month Ended July 31, 2016

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–4A

1.

=+

+=+ – + –– –– –

(a) + 25,000 + 25,000

(b) + 1,850 + 1,850

Bal. 25,000 1,850 1,850 25,000

(c) – 1,200 – 1,200

Bal. 23,800 1,850 650 25,000

(d) + 41,500 + 41,500

Cash Dividends

Auto

Exp.

Assets Stockholders’ Equity

Supplies

Accts.

Payable

Liabilities

Common

Stock

Sales

Comm.

Salaries

Exp.

Supplies

Exp.

Misc.

Exp.

Rent

Exp.

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–4A (Concluded)

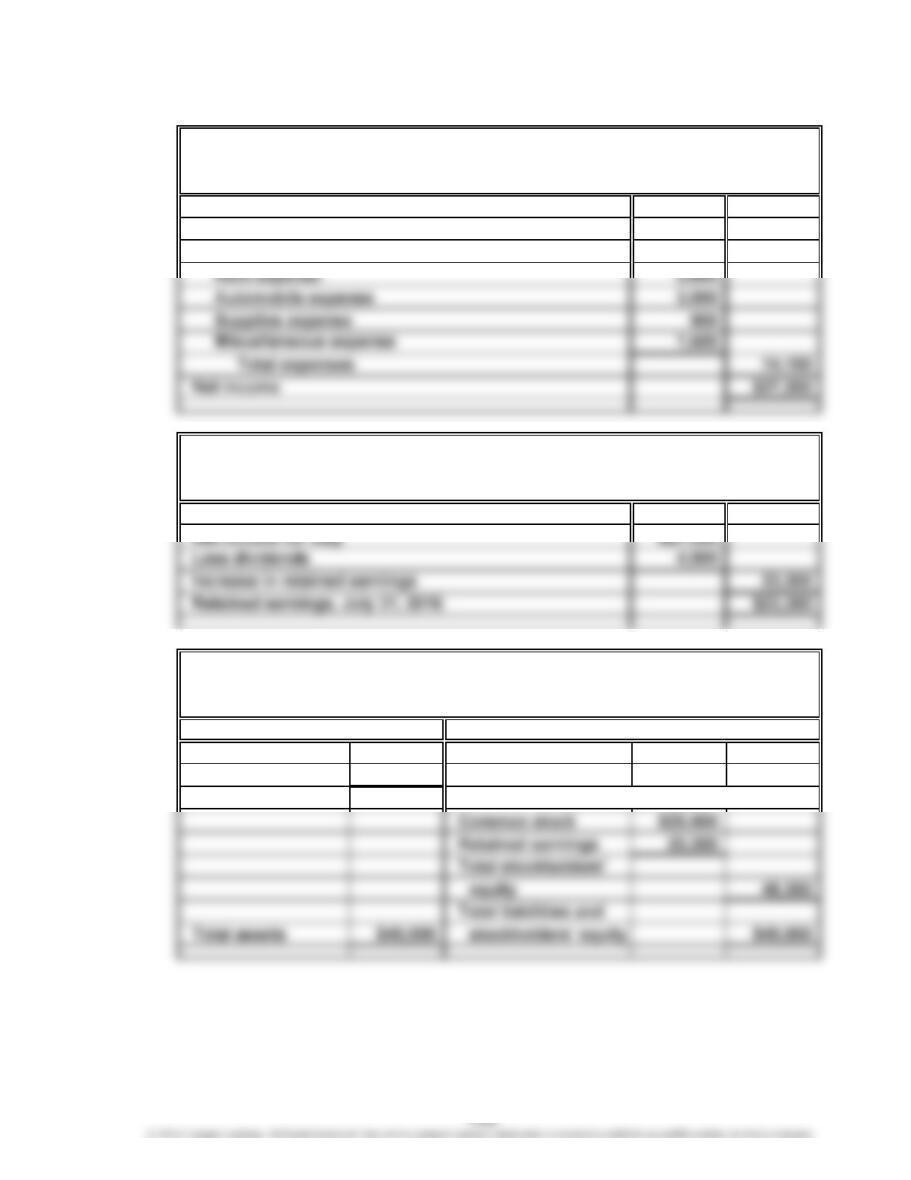

2.

Sales commissions $41,500

Expenses:

Salaries expense $5,000

Retained earnings, July 1, 2016 $0

Cash $48,050 Accounts payable $ 650

Supplies 950

Stockholders’ Equity

HALF MOON REALTY

Income Statement

For the Month Ended July 31, 2016

HALF MOON REALTY

Retained Earnings Statement

For the Month Ended July 31, 2016

HALF MOON REALTY

Balance Sheet

July 31, 2016

Assets Liabilities

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–5A

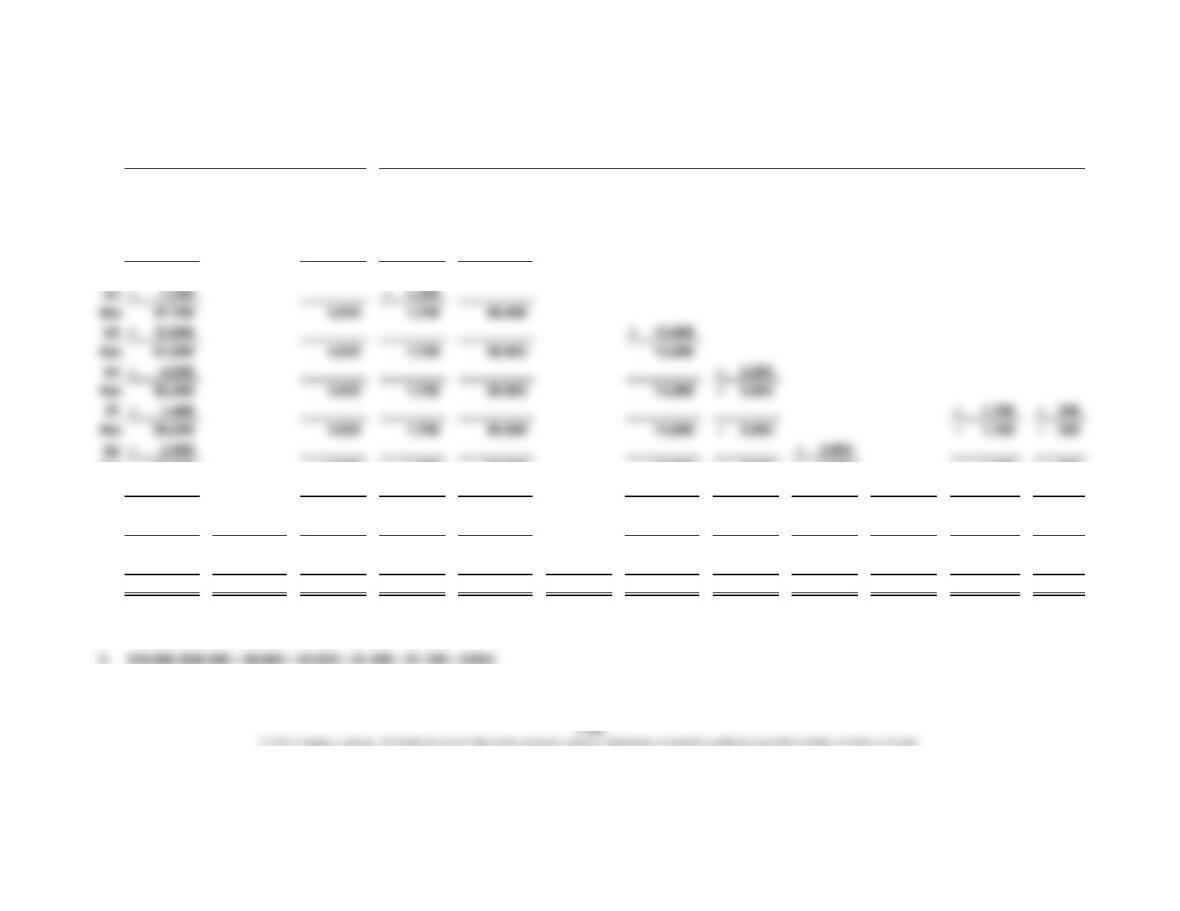

1. = + Stockholders’ Equity

Cash +++

=+

Common

Stock +

Retained

Earnings

Supplies Land

Accounts

Payable

Assets

Accounts

Receivable

Liabilities

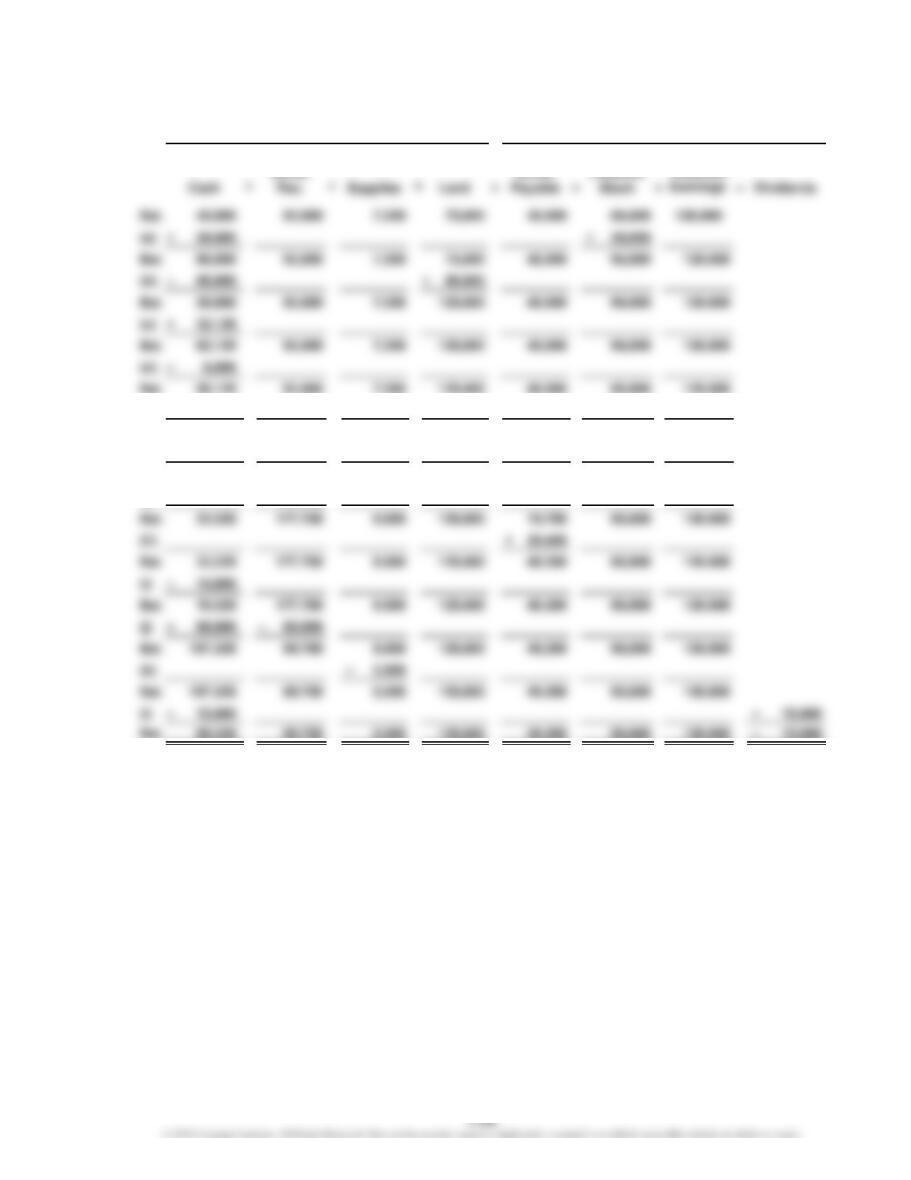

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–5A (Continued)

2. =+

Retained

(e) + 2,500 + 2,500

Bal. 56,125 93,000 9,500 125,000 42,500 95,000 120,000

(f) – 22,800 – 22,800

Bal. 33,325 93,000 9,500 125,000 19,700 95,000 120,000

(g) + 84,750

Stockholders’ Equity

Accts.

Assets

Accts.

Liabilities

Common

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–5A (Continued)

+–

–

–– – – –

Bal.

(a)

Bal.

(b)

Bal.

(c) + 32,125

Bal. 32,125

(d) – 6,000

Bal. 32,125 – 6,000

Stockholders’ Equity (Continued)

Utilities

Exp.

Supplies

Exp.

Dry

Cleaning

Revenue

Dry

Cleaning

Exp.

Wages

Exp.

Rent

Exp.

Truck

Exp.

Misc.

Exp.

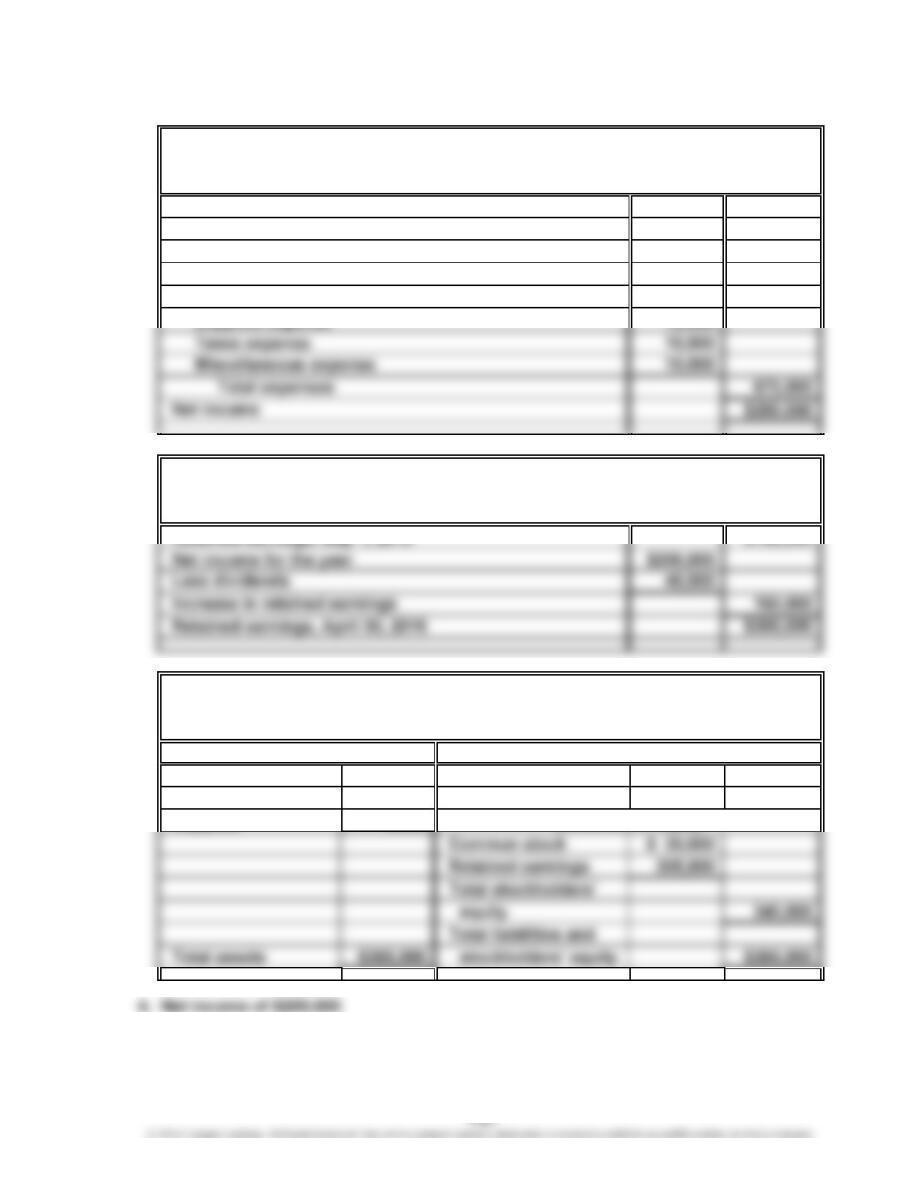

3.

Dry cleaning revenue $116,875

Expenses:

Dry cleaning expense $29,500

Wages expense 7,500

Retained earnings, July 1, 2016 $120,000

Net income for July $63,775

Cash $ 95,325 Accounts payable $ 49,200

Accounts receivable 89,750

Supplies 5,900

Assets Liabilities

Stockholders’ Equity

D’LITE DRY CLEANERS

Income Statement

For the Month Ended July 31, 2016

D’LITE DRY CLEANERS

Retained Earnings Statement

For the Month Ended July 31, 2016

D’LITE DRY CLEANERS

Balance Sheet

July 31, 2016

4. (Optional)

Cash flows from operating activities:

Cash received from customers* $120,125

Deduct cash payments for expenses

and payments to creditors** (42,800)

Net cash flows from operating activities $ 77,325

Cash flows used for investing activities:

D’LITE DRY CLEANERS

Statement of Cash Flows

For the Month Ended July 31, 2016

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–6A

a. Fees earned, $750,000 ($275,000 + $475,000)

b. Supplies expense, $30,000 ($475,000 – $300,000 – $100,000 – $20,000 – $25,000)

c. Retained earnings, April 1, 2016, $0; Wolverine Realty was organized on

April 1, 2016.

d. Net income for April, $275,000 from income statement

e. $150,000 ($275,000

–

$125,000)

f. Retained earnings, April 30, 2016, $150,000

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–1B

1.

Assets = +

+ +=+ –+ –––– –

(a) + 50,000 + 50,000

(b) + 4,000 + 4,000

Bal. 50,000 4,000 4,000 50,000

Bal. 52,550 4,000 1,700 50,000 13,800 – 5,000 – 2,500 – 1,150 – 300

(h) – 1,300 – 1,300

Bal. 52,550 2,700 1,700 50,000 13,800 – 5,000 – 2,500 – 1,300 – 1,150 – 300

(i) + 12,500 + 12,500

Bal. 52,550 12,500 2,700 1,700 50,000 26,300 – 5,000 – 2,500 – 1,300 – 1,150 – 300

(j) – 3,900 – 3,900

Bal. 48,650 12,500 2,700 1,700 50,000 – 3,900 26,300 – 5,000 – 2,500 – 1,300 – 1,150 – 300

2. Stockholders’ equity is the right of stockholders (owners) to the assets of the business. These rights are increased by issuing common stock and

revenues and decreased by dividends and expenses.

4. March’s transactions increased retained earnings by $12,150 ($16,050 – $3,900), which is the excess of March’s net income of $16,050

over dividends of $3,900.

Cash Dividends

Supplies

Expense

Stockholders’ Equity

Accts.

Rec. Supplies

Accts.

Payable

Liabilities

Common

Stock

Fees

Earned

Salaries

Expense

Auto

Exp.

Misc.

Exp.

Rent

Expense

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–2B

1.

Fees earned $875,000

Expenses:

Wages expense $525,000

Rent expense 75,000

Utilities expense 38,000

Supplies expense 12,000

2.

Retained earnings, May 1, 2015 $145,000

3.

Cash $146,000 Accounts payable $ 25,000

Accounts receivable 210,000

Supplies 9,000

For the Year Ended April 30, 2016

WILDERNESS TRAVEL SERVICE

WILDERNESS TRAVEL SERVICE

Income Statement

For the Year Ended April 30, 2016

WILDERNESS TRAVEL SERVICE

Retained Earnings Statement

Balance Sheet

April 30, 2016

Assets Liabilities

Stockholders’ Equity

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–3B

1.

Fees earned $125,000

Expenses:

Salaries expense $58,000

Rent expense 27,000

Auto expense 15,500

Supplies expense 6,100

Miscellaneous expense 7,500

Total expenses 114,100

Net income $ 10,900

2.

3.

BRONCO CONSULTING

Income Statement

For the Month Ended August 31, 2016

BRONCO CONSULTING

Retained Earnings Statement

BRONCO CONSULTING

Balance Sheet

August 31, 2016

Assets Liabilities

4. (Optional)

Cash flows from operating activities:

Cash received from customers $ 92,000

BRONCO CONSULTING

Statement of Cash Flows

For the Month Ended August 31, 2016

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–4B

1.

=+

+=+ –+ –––– –

(a) + 24,000 + 24,000

(b) – 3,600 – 3,600

Bal. 20,400 24,000 – 3,600

(c) – 1,950 – 1,350 – 600

Bal. 18,450 24,000 – 3,600 – 1,350 – 600

(d) + 1,200 + 1,200

Bal. 18,450 1,200 1,200 24,000 – 3,600 – 1,350 – 600

Cash Dividends

Auto

Exp.

Assets Stockholders’ Equity

Supplies

Accts.

Payable

Liabilities

Common

Stock

Sales

Comm.

Salaries

Exp.

Supplies

Exp.

Misc.

Exp.

Rent

Exp.

2.

Sales commissions $19,800

Expenses:

Rent expense $3,600

Salaries expense 2,500

Retained earnings, April 1, 2016 $0

Cash $31,500 Accounts payable $ 450

Supplies 300

Assets Liabilities

Stockholders’ Equity

CUSTOM REALTY

Income Statement

For the Month Ended April 30, 2016

CUSTOM REALTY

Retained Earnings Statement

For the Month Ended April 30, 2016

CUSTOM REALTY

Balance Sheet

April 30, 2016

CHAPTER 1 Introduction to Accounting and Business

Prob. 1–5B

1. Liabilities +

Accounts

Accounts

Common

Retained

Assets

=

Stockholders’ Equity