1. Merchandising businesses acquire merchandise for resale to customers. It is the selling of

2. Yes. Gross profit is the excess of (net) sales over cost of merchandise sold. A net loss arises

4. a. 1% discount allowed if paid within 15 days of date of invoice; entire amount of invoice

6. a. A credit memo issued by the seller of merchandise indicates the amount for which the

r

8. Examples of such accounts include the following: Sales, Sales Discounts, Sales Returns and

CHAPTER 5

ACCOUNTING FOR MERCHANDISING BUSINESSES

DISCUSSION QUESTIONS

5-1

CHAPTER 5 Accounting for Merchandising Businesses

PE 5–1A

PE 5–1B

PE 5–2A

PE 5–2B

PE 5–3A

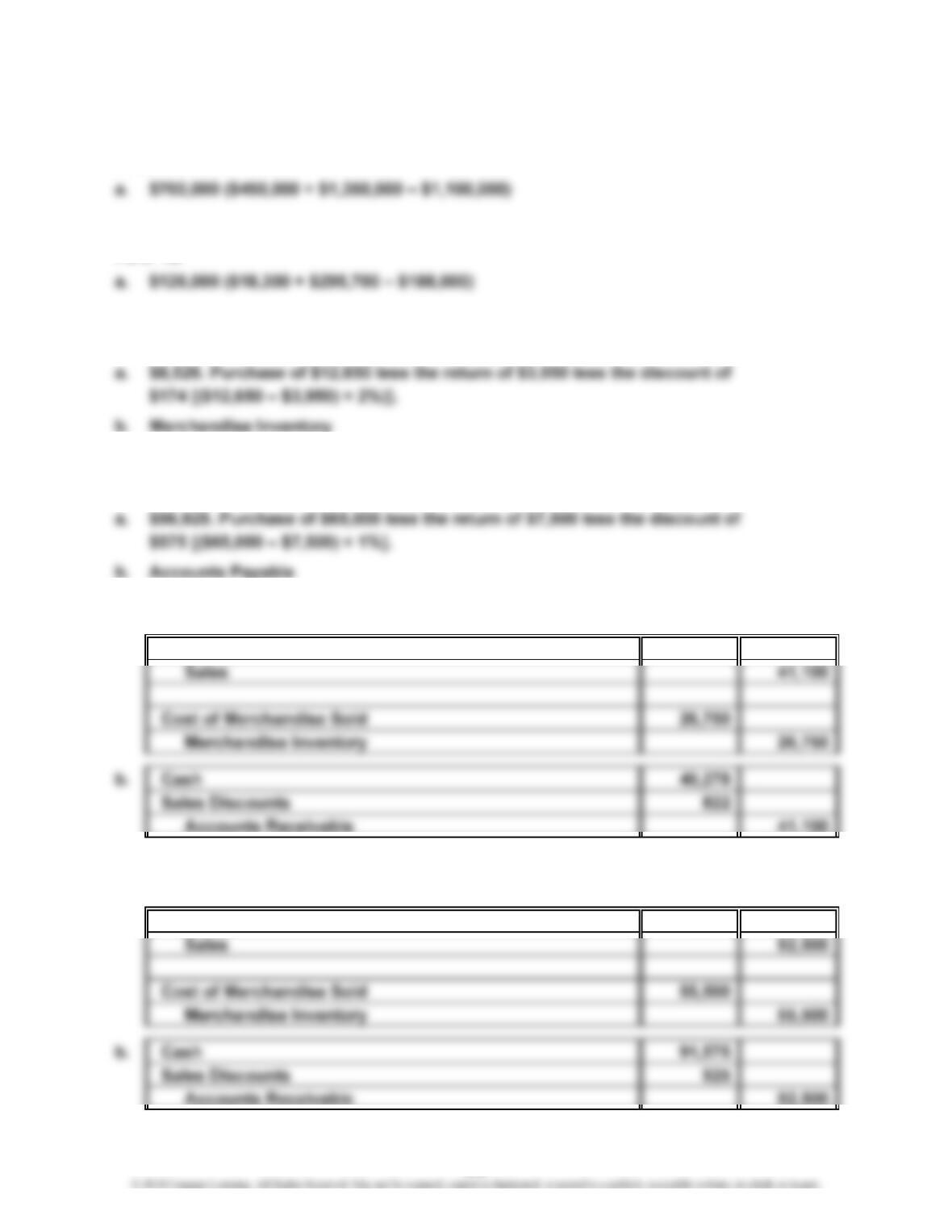

a. Accounts Receivable 41,100

PE 5–3B

a. Accounts Receivable 92,500

PRACTICE EXERCISES

5-2

CHAPTER 5 Accounting for Merchandising Businesses

PE 5–4A

a. $161,400. Purchase of $180,000 less return of $20,000 less the discount of

PE 5–4B

a. $31,680. Purchase of $36,000 less return of $4,000 less the discount of

PE 5–5A

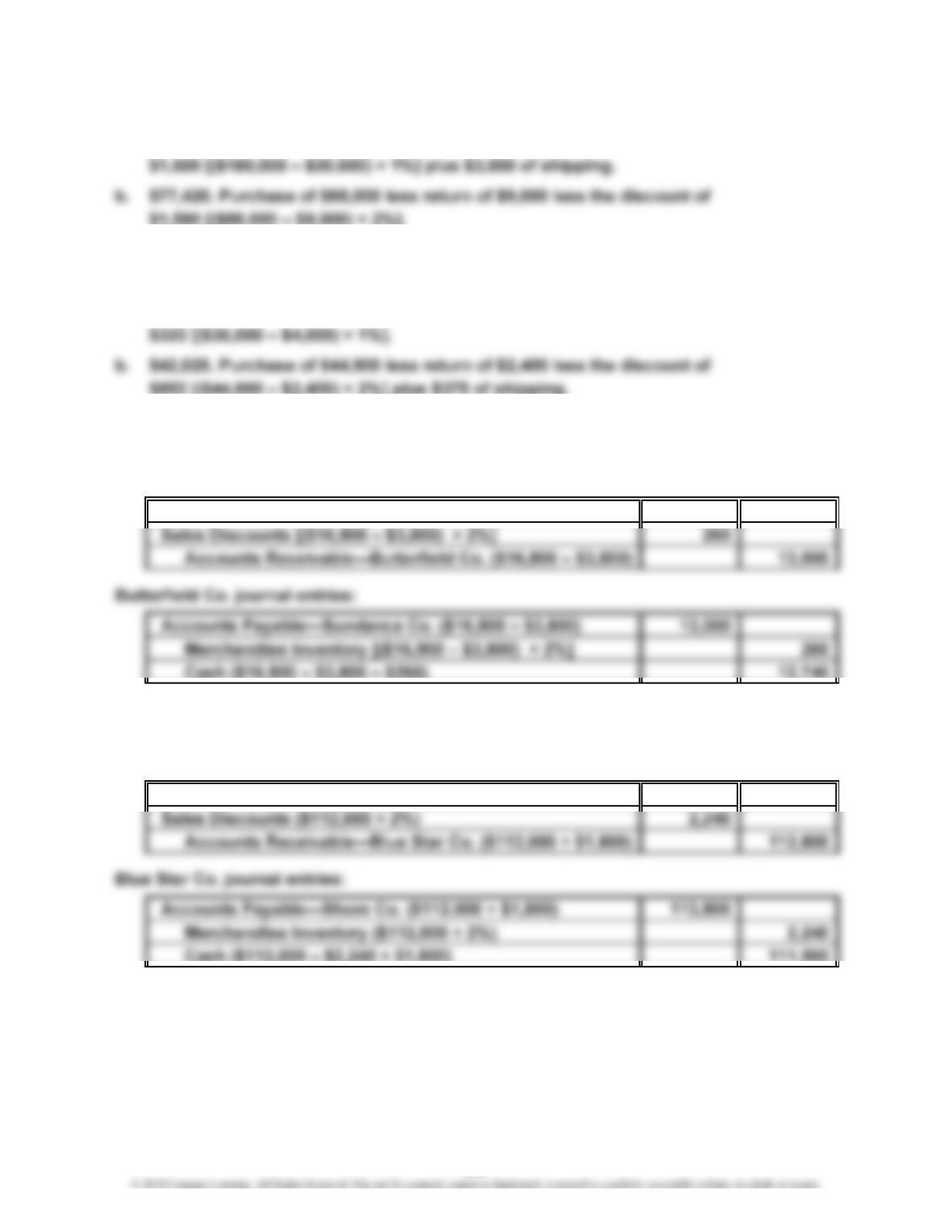

Sundance Co. journal entries:

Cash ($16,800 – $3,800 – $260) 12,740

PE 5–5B

Shore Co. journal entries:

Cash ($112,000 – $2,240 + $1,800) 111,560

5-3

CHAPTER 5 Accounting for Merchandising Businesses

PE 5–6A

Apr. 30 Cost of Merchandise Sold

PE 5–6B

Dec. 31 Cost of Merchandise Sold

PE 5–7A

a. 2014 2013

PE 5–7B

a. 2014 2013

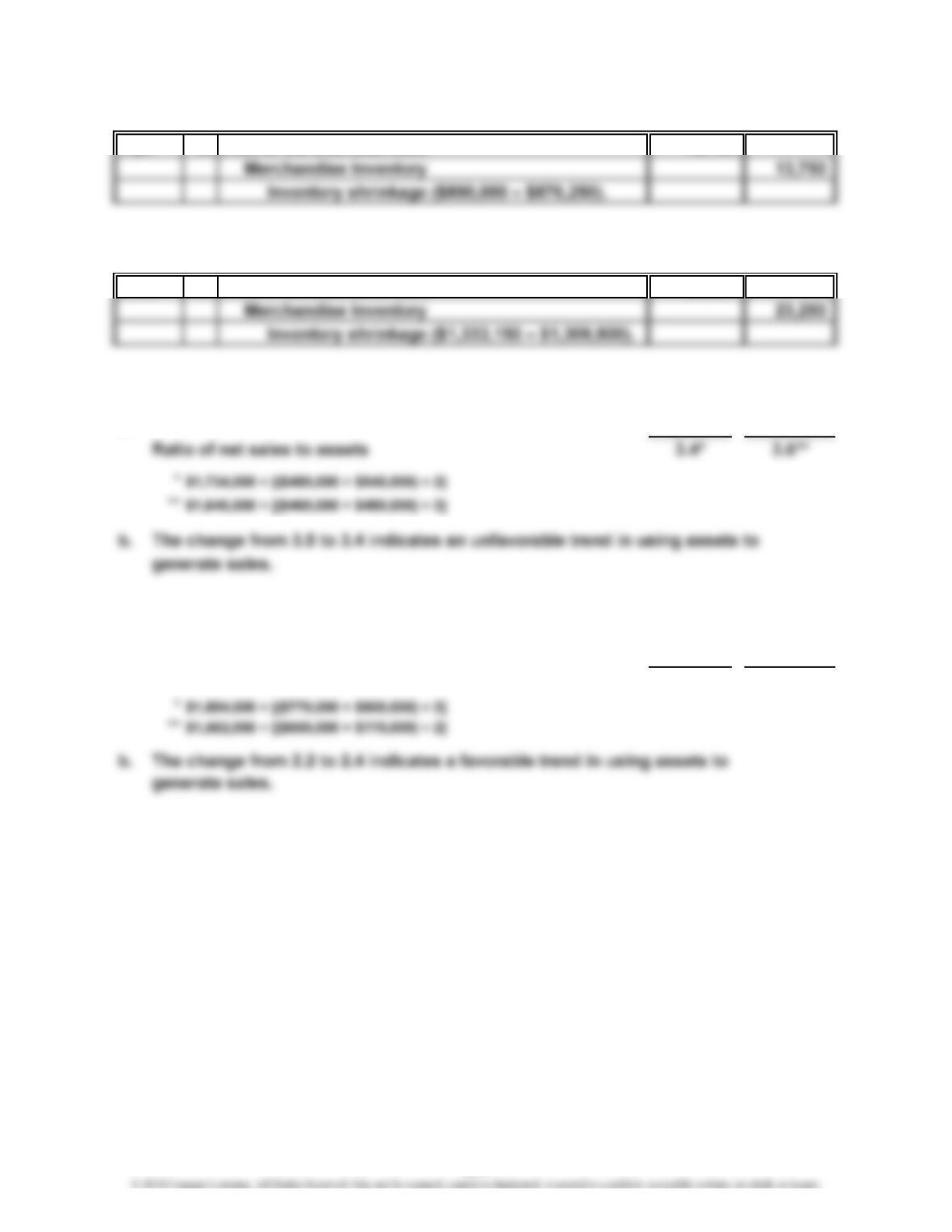

Ratio of net sales to assets 2.4* 2.2**

23,250

13,750

5-4

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–1

a. $931,000 ($2,450,000 – $1,519,000)

Ex. 5–2

Ex. 5–4

The offer of Supplier Two is lower than the offer of Supplier One. Details are as follows:

Supplier One Supplier Two

List price $100,000 $99,750

Ex. 5–5

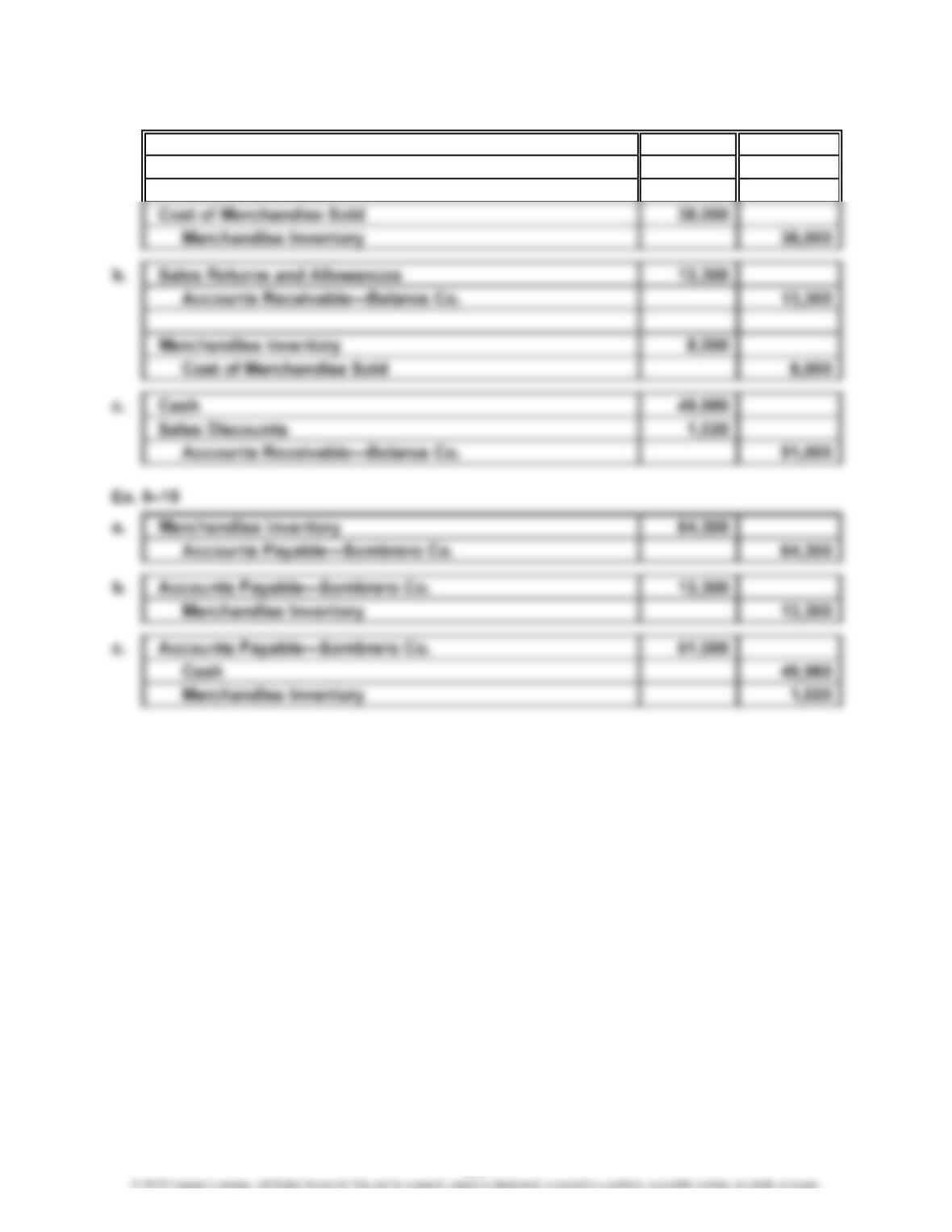

(1) Purchased merchandise on account at a cost of $21,000.

EXERCISES

5-5

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–6

a. Merchandise Inventory 60,000

Accounts Payable 60,000

Ex. 5–7

a. Merchandise Inventory 71,500

Accounts Payable—Sitwell Co. 71,500

5-6

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–8

a. Cash 45,000

Sales 45,000

Ex. 5–9

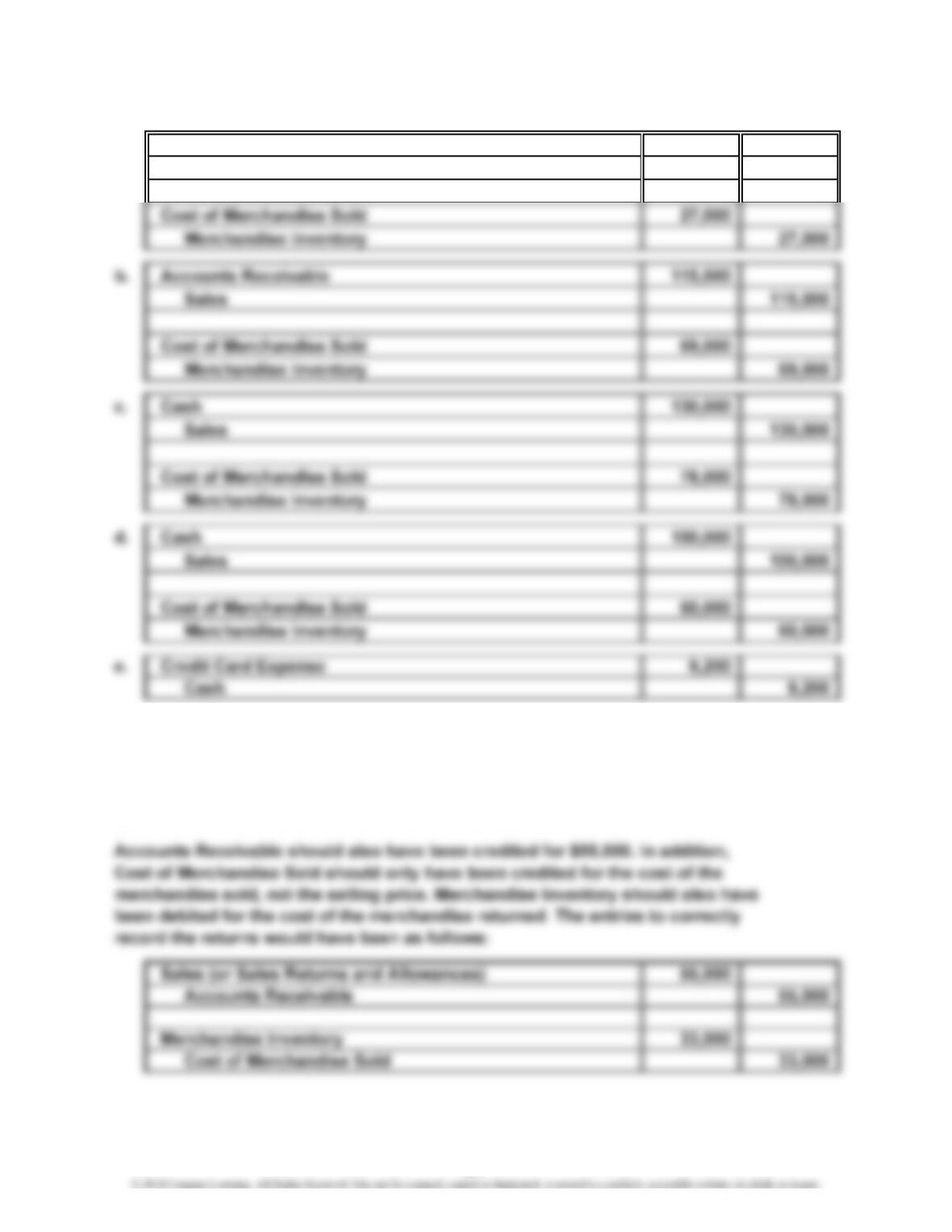

It was acceptable to debit Sales for the $55,000. However, using Sales Returns

and Allowances assists management in monitoring the amount of returns so that

quick action can be taken if returns become excessive.

5-7

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–11

(1) Sold merchandise on account, $42,000.

Ex. 5–12

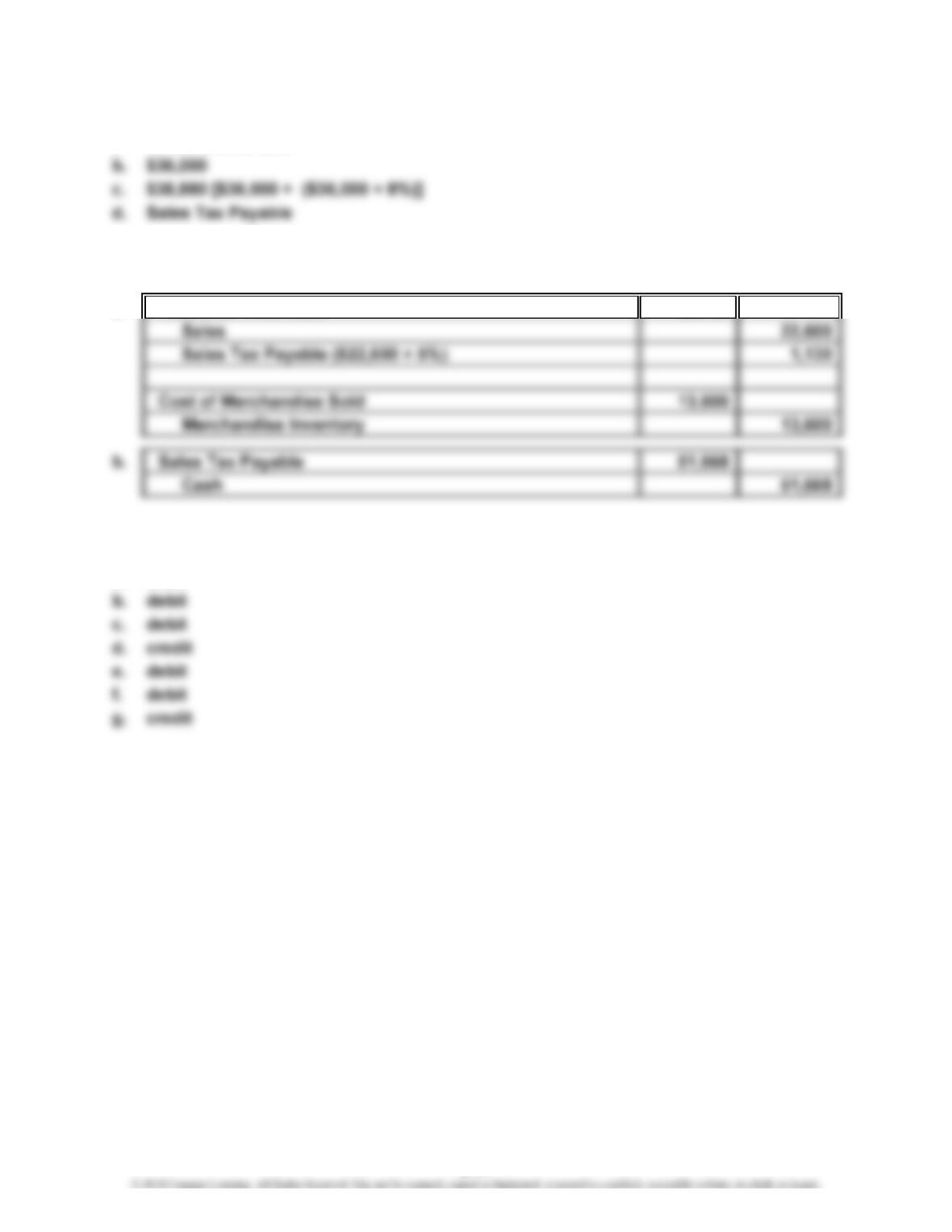

a. $24,000

Ex. 5–13

a. $49,600 ($52,300 – $2,700)

5-8

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–14

a. Accounts Receivable—Belarus Co. 64,300

Sales 64,300

5-9

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–16

Balance Sheet Accounts Income Statement Accounts

100 Assets 400 Revenues

110 Cash 410 Sales

112 Accounts Receivable 411 Sales Returns and

114 Merchandise Inventory Allowances

115 Store Supplies 412 Sales Discounts

116 Office Supplies 500 Expenses

117 Prepaid Insurance 510 Cost of Merchandise Sold

120 Land 520 Sales Salaries Expense

123 Store Equipment 521 Advertising Expense

124 Accumulated Depreciation— 522 Depreciation Expense—

Store Equipment Store Equipment

125 Office Equipment 523 Store Supplies Expense

126 Accumulated Depreciation— 524 Delivery Expense

Office Equipment 529 Miscellaneous Selling

200 Liabilities Expense

210 Accounts Payable 530 Office Salaries Expense

211 Salaries Payable 531 Rent Expense

212 Notes Payable 532 Depreciation Expense—

300 Stockholders’ Equity Office Equipment

310 Capital Stock 533 Insurance Expense

311 Retained Earnings 534 Office Supplies Expense

312 Dividends 539 Miscellaneous

313 Income Summary Administrative Expense

600 Other Expense

610 Interest Expense

Note: The order and number of some of the accounts within subclassifications is

somewhat arbitrary, as in accounts 115–117, accounts 520–524, and accounts

530–534. For example, in a new business, the order of magnitude expense

account balances often cannot be determined in advance. The magnitude may

also vary from period to period.

5-10

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–17

a. At the time of sale

Ex. 5–18

a. Accounts Receivable 23,730

Ex. 5–19

a. debit

5-11

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–20

Ex. 5–21

Ex. 5–22

5-12

CHAPTER 5 Accounting for Merchandising Businesses

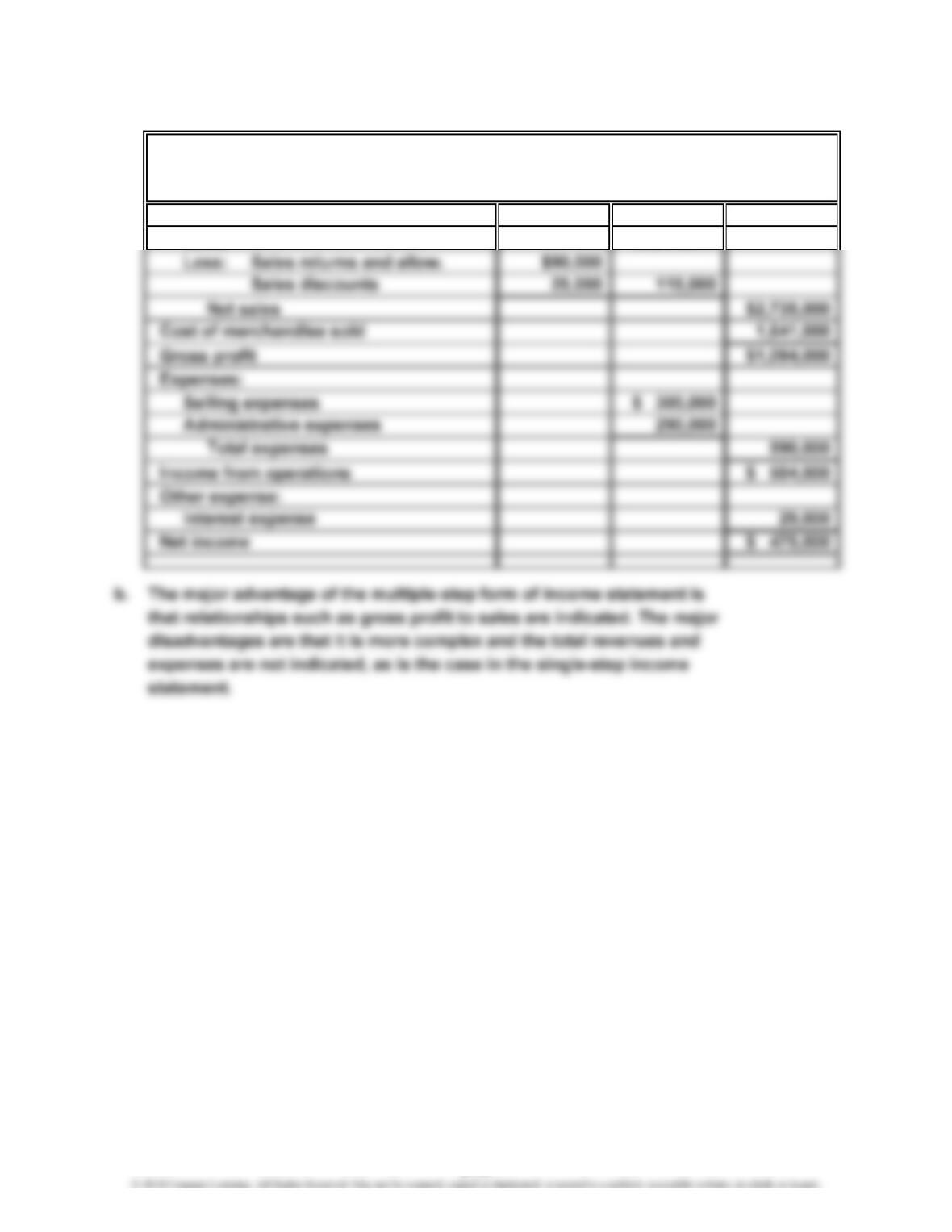

Ex. 5–23

a.

Revenue from sales:

Sales $2,850,000

FOLDAWAY FURNISHINGS COMPANY

Income Statement

For the Year Ended February 28, 2014

5-13

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–24

1. Sales returns and allowances and sales discounts should be deducted from

A correct income statement would be as follows:

Revenue from sales:

Sales $9,132,000

CURBSTONE COMPANY

Income Statement

For the Year Ended August 31, 2014

5-14

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–25

Revenues:

Net sales $3,750,000

Ex. 5–26

Cost of Merchandise Sold 14,450

CUMMERBUND COMPANY

Income Statement

For the Year Ended June 30, 2014

5-15

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–28

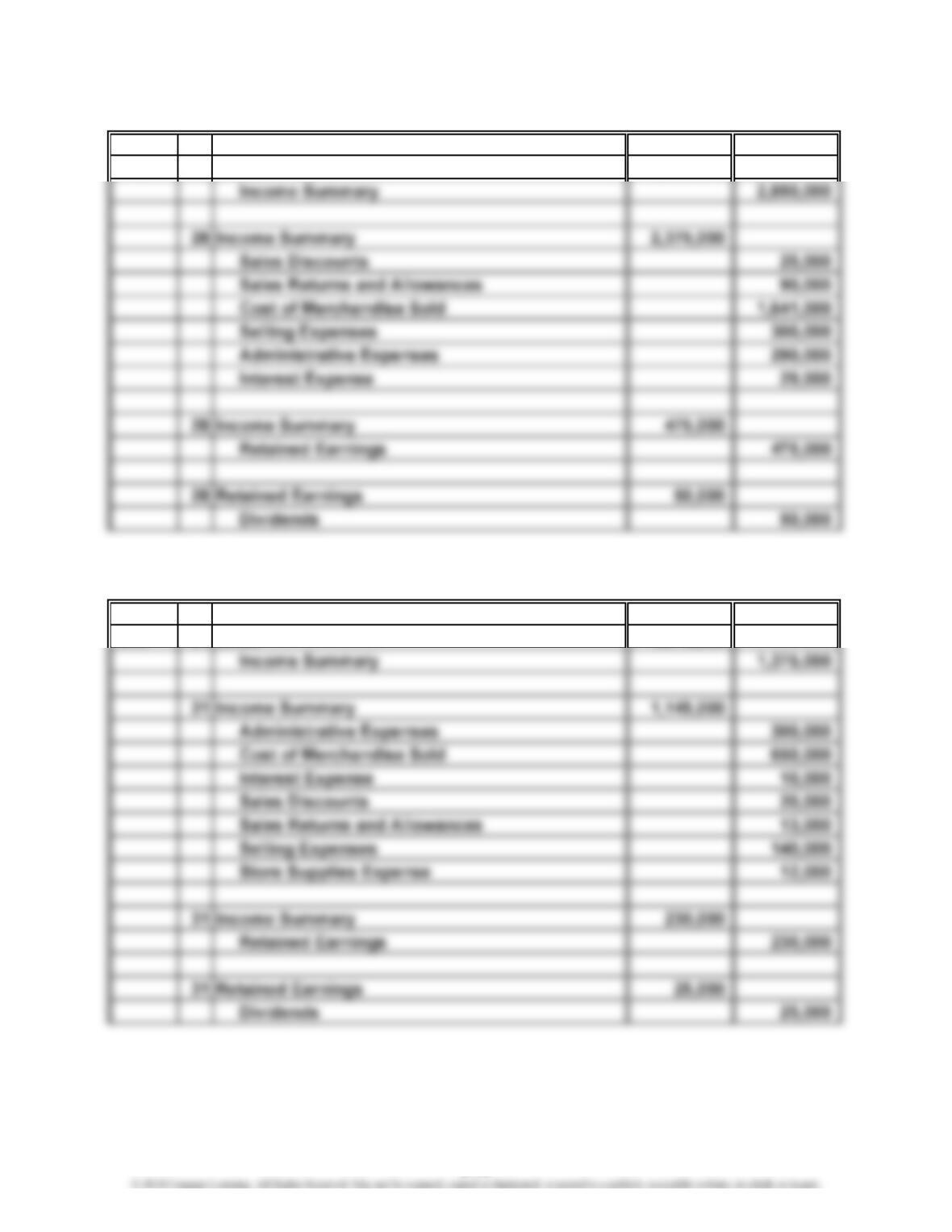

2014

Feb. 28 Sales 2,850,000

Ex. 5–29

2014

Oct. 31 Sales 1,375,000

Closing Entries

Closing Entries

5-16

CHAPTER 5 Accounting for Merchandising Businesses

Ex. 5–30

a. Year 2: 1.68 {$67,997 ÷ [($40,125 + $40,877) ÷ 2]}

Ex. 5–31

Appendix Ex. 5–32

5-17

CHAPTER 5 Accounting for Merchandising Businesses

Appendix Ex. 5–33

a. Cost of merchandise sold:

Merchandise inventory, May 1, 2013 $ 380,000

Appendix Ex. 5–34

Cost of merchandise sold:

Merchandise inventory, November 1 $ 28,000

5-18

CHAPTER 5 Accounting for Merchandising Businesses

Appendix Ex. 5–35

Cost of merchandise sold:

Merchandise inventory, July 1 $ 190,850

Appendix Ex. 5–36

A correct cost of merchandise sold section is as follows:

Cost of merchandise sold:

Merchandise inventory, June 1, 2013 $ 91,300

5-19

CHAPTER 5 Accounting for Merchandising Businesses

Appendix Ex. 5–37

(a) credit

Appendix Ex. 5–38

Jan. 2 Purchases 18,200

Accounts Payable 18,200

5-20