APPENDIX D

Time Value of Money

Learning Objectives

1. Distinguish between simple and compound interest.

2. Solve for future value of a single amount.

3. Solve for future value of an annuity.

4. Identify the variables fundamental to solving present value problems.

5. Solve for present value of a single amount.

6. Solve for present value of an annuity.

7. Compute the present value of notes and bonds.

8. Use a financial calculator to solve time value of money problems.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT

Brief Exercises

1. 2 AP 8. 5, 6 AP 14. 5, 6,

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE D-1

(a) Interest = p X i X n

(b) Future value factor for 12 periods at 5% is 1.79586 (from Table 1)

BRIEF EXERCISE D-2

(a) (b) (a) (b)

(1) A 6% 3 periods (2) A 5% 8 periods

BRIEF EXERCISE D-3

FV = p X FV of 1 factor

BRIEF EXERCISE D-4

FV of an annuity of 1 = p X FV of an annuity factor

BRIEF EXERCISE D-5

FV = p X FV of 1 factor + (p X FV of an annuity factor)

= ($6,000 X 2.02582) + ($1,000 X 25.64541)

BRIEF EXERCISE D-6

FV = p X FV of 1 factor

BRIEF EXERCISE D-7

(a) (b)

(1) A 12% 6 periods

BRIEF EXERCISE D-8

(a) i = 10%

? $28,000

0 1 2 3 4 5 6 7 8 9

BRIEF EXERCISE D-8 (Continued)

(b) i = 9%

? $28,000 $28,000 $28,000 $28,000 $28,000 $28,000

0 1 2 3 4 5 6

BRIEF EXERCISE D-9

i = 9%

? $750,000

Discount rate from Table 3 is .64993 (5 periods at 9%). Present value of

BRIEF EXERCISE D-10

i = 10%

Discount rate from Table 3 is .46651 (8 periods at 10%). Present value of

BRIEF EXERCISE D-11

i = 5%

Discount rate from Table 4 is 10.37966. Present value of 15 payments of

BRIEF EXERCISE D-12

i = 8%

? $90,000 $90,000 $90,000 $90,000 $90,000 $90,000

0 1 2 3 4 5 6

BRIEF EXERCISE D-13

i = 4%

? $300,000

Diagram

for

Principal

0 1 2 3 4 19 20

Present value of principal to be received at maturity:

$300,000 X 0.45639 (PV of $1 due in 20 periods

at 4% from Table 3) ……………………………………………………… $136,917.00

BRIEF EXERCISE D-14

The bonds will sell at a discount (for less than $300,000). This may be proven

as follows:

Present value of principal to be received at maturity:

$300,000 X .37689 (PV of $1 due in 20 periods

BRIEF EXERCISE D-15

i = 8%

? $64,000

Diagram

for

Principal

0 1 2 3 4 5 6

Present value of principal to be received at maturity:

$64,000 X .63017 (PV of $1 due in 6 periods

at 8% from Table 3) …………………………………………………….. $40,330.88

BRIEF EXERCISE D-16

i = 5%

? $2,600,000

Diagram

for

Principal

0 1 2 3 4 14 15 16

Present value of principal to be received at maturity:

$2,600,000 X 0.45811 (PV of $1 due in 16 periods

at 5% from Table 3) ……………………………………………………. $1,191,086*

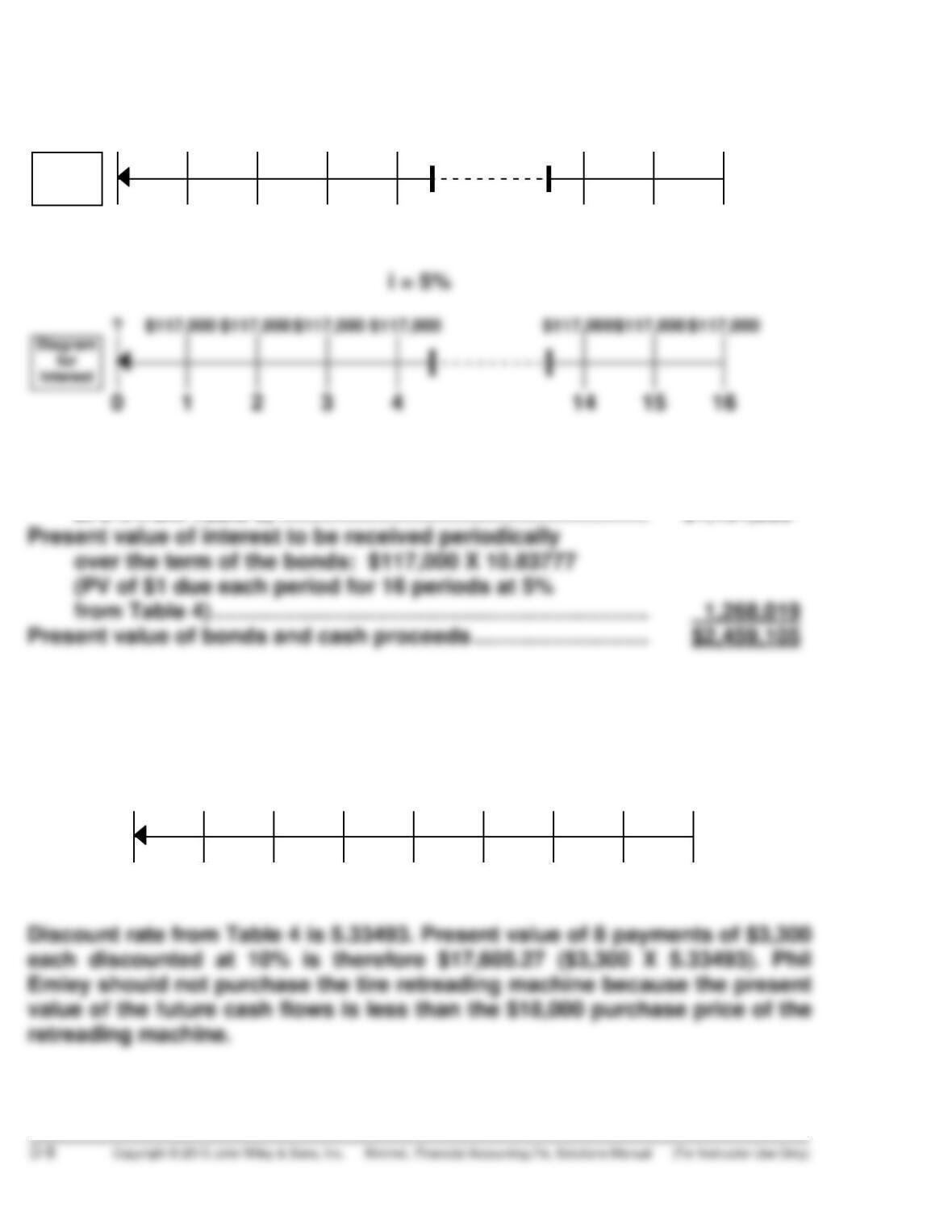

BRIEF EXERCISE D-17

i = 10%

? $3,300 $3,300 $3,300 $3,300 $3,300 $3,300 $3,300 $3,300

0 1 2 3 4 5 6 7 8

BRIEF EXERCISE D-18

i = 4%

? $46,850 $46,850 $46,850 $46,850 $46,850 $46,850

0 1 2 3 4 9 10

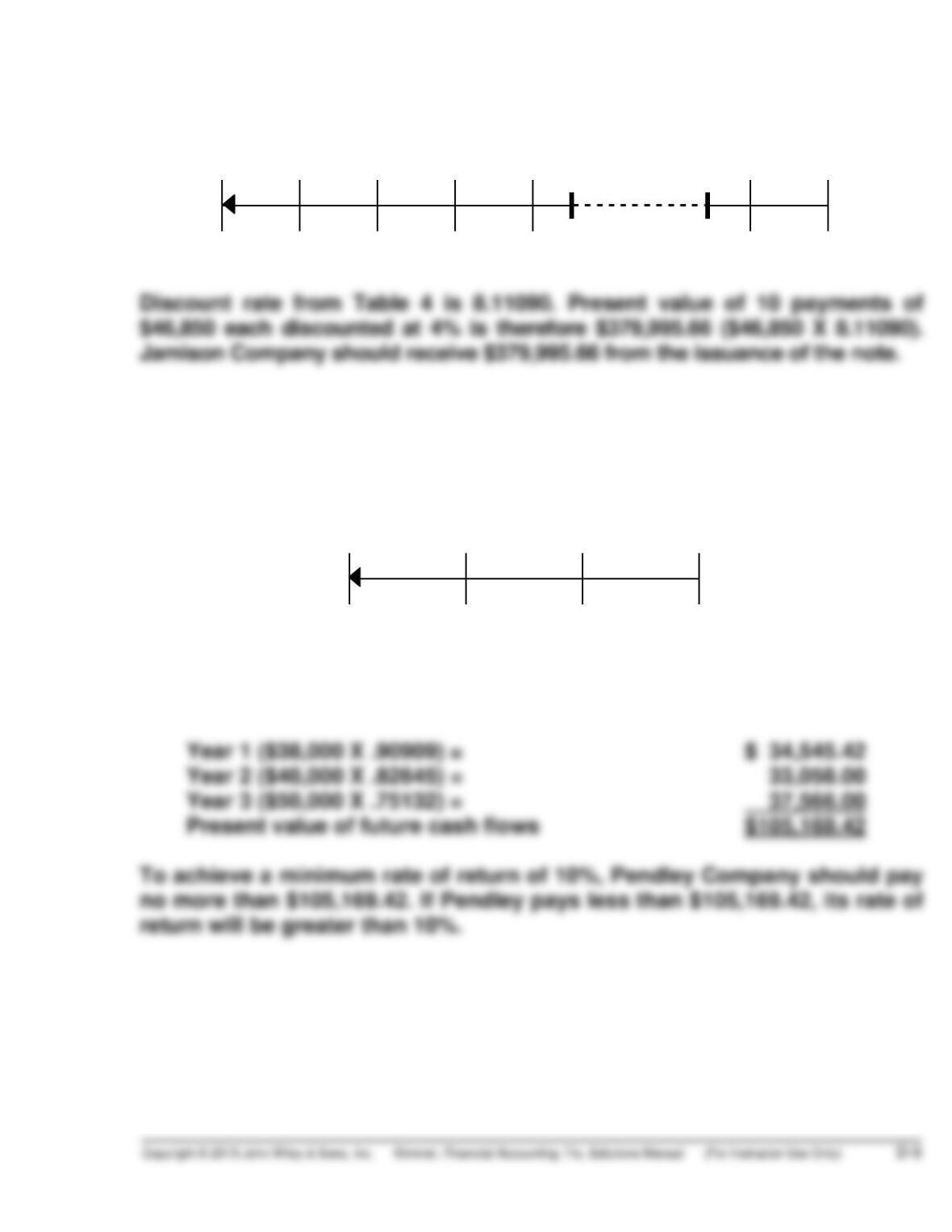

BRIEF EXERCISE D-19

i = 10%

? $38,000 $40,000 $50,000

0 1 2 3

To determine the present value of the future cash flows, discount the future

cash flows at 10%, using Table 3.

BRIEF EXERCISE D-20

i = ?

$4,172.65 $10,000

0 1 2 3 4 14 15

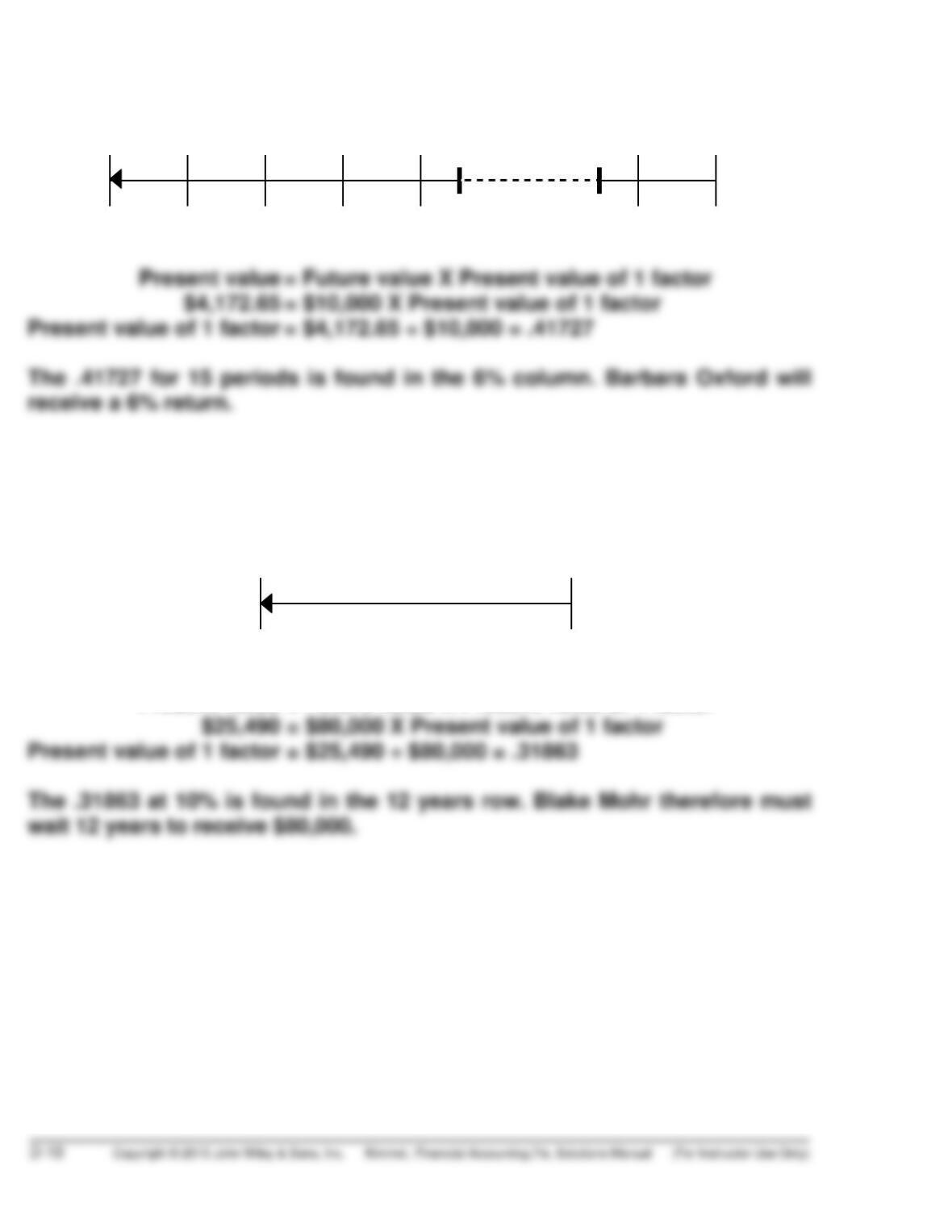

BRIEF EXERCISE D-21

i = 10%

$25,490 $80,000

n = ?

Present value = Future value X Present value of 1 factor

BRIEF EXERCISE D-22

i = ?

? $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000

0 1 2 3 4 5 6 19 20

$9,128.55

BRIEF EXERCISE D-23

i = 11%

$1,000 $1,000 $1,000 $1,000 $1,000 $1,000

$5,146.12 n = ?

BRIEF EXERCISE D-24

10 ? –18,000 0 50,000

N I/YR. PV PMT FV

10.76%

BRIEF EXERCISE D-25

BRIEF EXERCISE D-26

BRIEF EXERCISE D-27

(a)

Inputs: 7 6.9 ? –16,000 0

N I PV PMT FV

(b)

Inputs: 10 8.65 ? 14,000 200,000

N I PV PMT FV

BRIEF EXERCISE D-28

(

a)

Note—set payments at 12 per year.

Inputs: 96 7.8 42,000 ? 0

N I PV PMT FV

A

(

b)

Note—set payments to 1 per year

.

Inputs: 5 7.25 8,000 ? 0

N I PV PMT FV

A