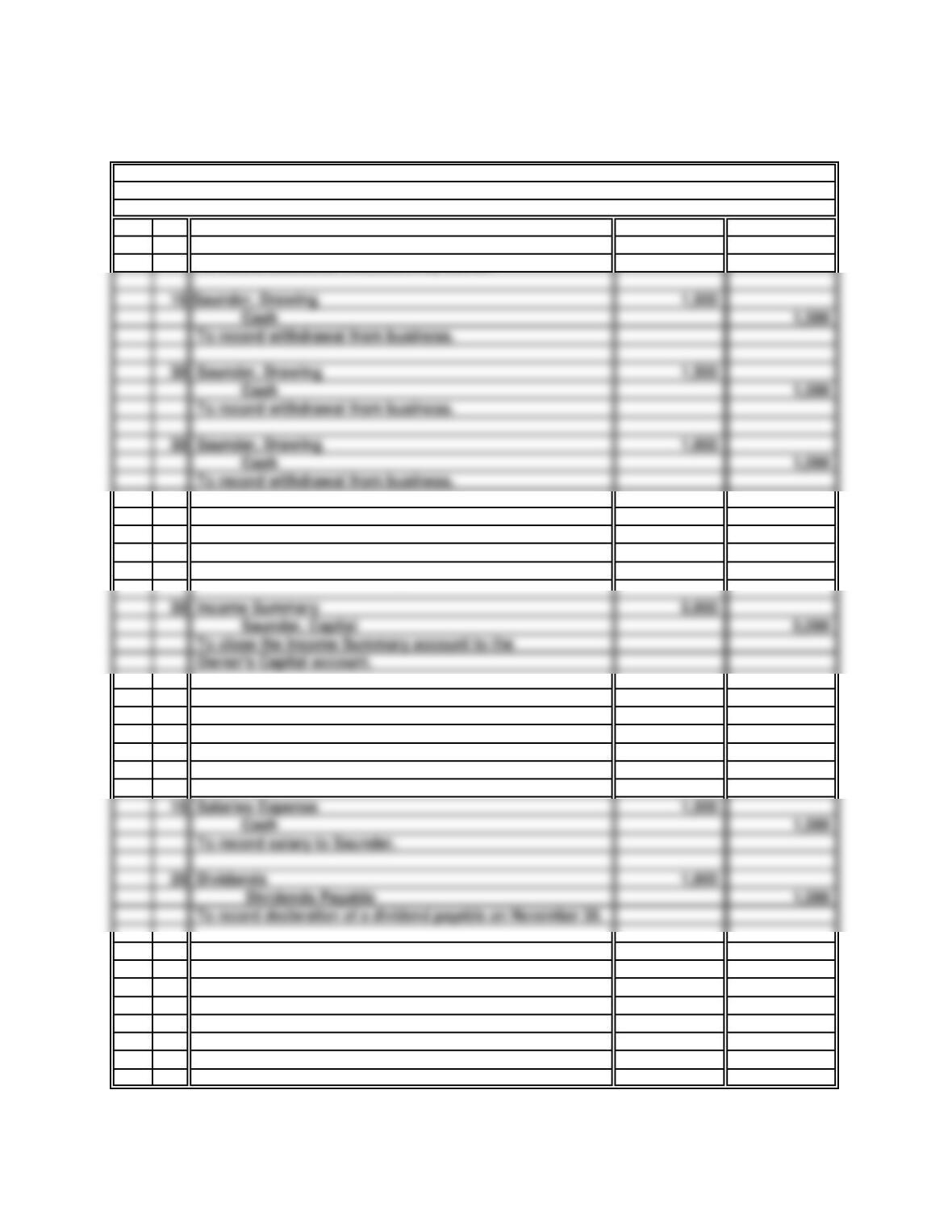

45 Minutes, Strong PROBLEM C.8

S & X CO.

a.

General Journal

(1)

Nov 9 Cash 15,000

Saunder, Capital 15,000

To record additional investment by owner.

(2)

30 Saunder, Capital 4,000

Saunder, Drawing 4,000

To close the owner’s Drawing account.

30 Income Summary 5,000

Saunder, Capital 5,000

Owner’s Capital account.

b.

(1)

Nov 9 Cash 15,000

Capital Stock 15,000

To record additional investment by owner.

15 Salaries Expense 1,500

To record salary to Saunder.

20 Dividends 1,000

Dividends Payable 1,000

15 Saunder, Drawing 1,500

To record withdrawal from business.

30 Saunder, Drawing 1,500

To record withdrawal from business.

30 Saunder, Drawing 1,000

To record withdrawal from business.

PROBLEM C.8

S & X CO. (concluded)

General Journal

Nov 30 Salaries Expense 1,500

Cash 1,500

To record salary to Saunder.

(2)

30 Income Tax Expense 600

Income Tax Payable 600

To accrue income taxes expense for November.

($2,000 × 30% = $600)

30 Income Summary 600

Income Tax Expense 600

To close the Income Tax Expense account

into the Income Summary account.

30 Income Summary 1,400

Retained Earnings 1,400

To close the Income Summary account.

30 Retained Earnings 1,000

To close the Dividends account.

c.

d.

The net income differs for two reasons. First, the corporation is subject to income taxes, and

If the business is organized as a sole proprietorship, Saunder will pay taxes on the net

30 Dividends Payable 1,000

Cash 1,000

To record the payment of the dividend declared

on November 20.

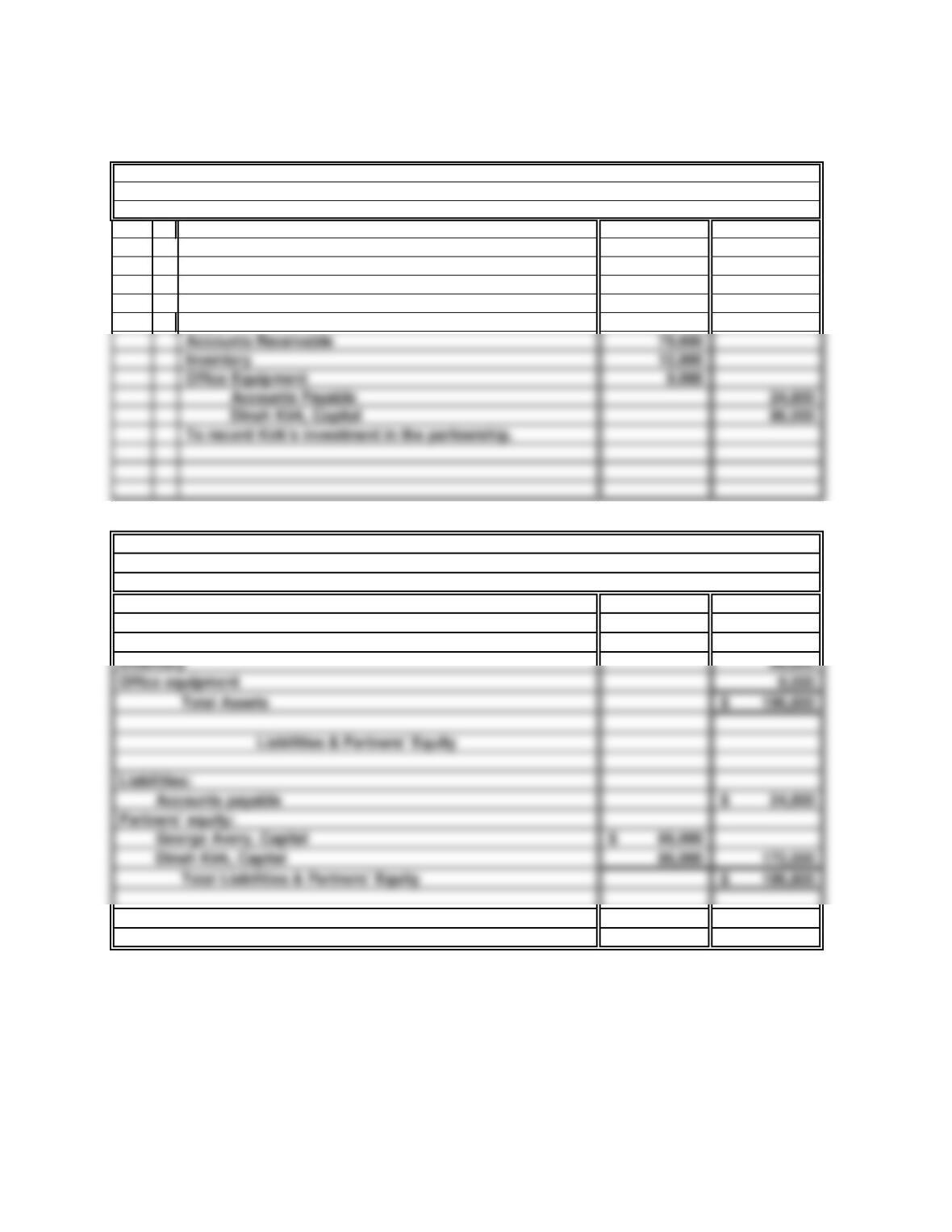

PROBLEM C.9

AVERY AND KIRK

a.

General Journal

July 1 Cash 30,000

Inventory 56,000

George Avery, Capital 86,000

To record Avery’s investment in the partnership.

1 Cash 9,400

b.

Assets

Cash 39,400$

Accounts receivable 79,600

20 Minutes, Easy

AVERY AND KIRK

Balance Sheet

July 1, 20xx

Accounts Receivable 79,600

Inventory 12,800

Office Equipment 9,000

Accounts Payable 24,800

Dinah Kirk, Capital 86,000

To record Kirk’s investment in the partnership.

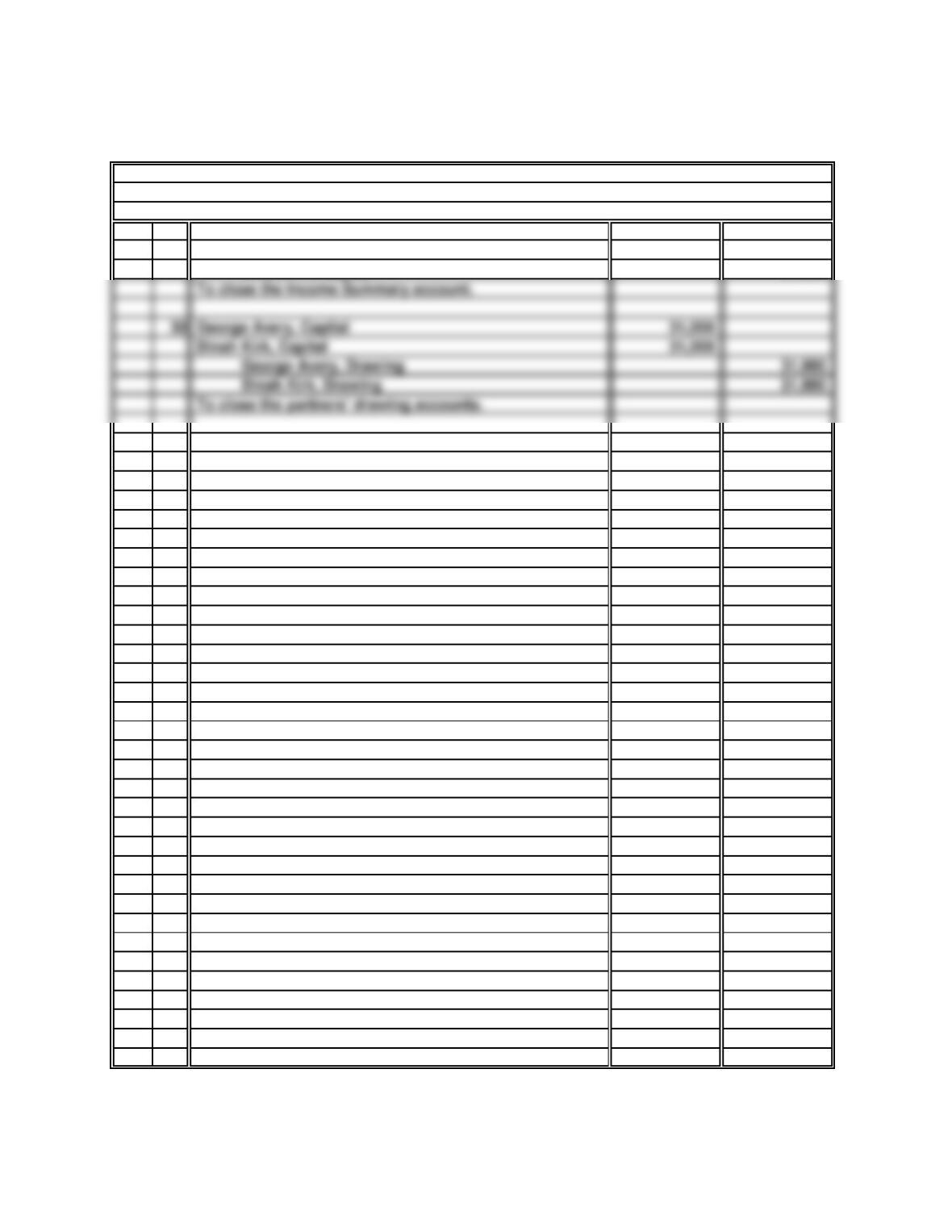

PROBLEM C.9

AVERY AND KIRK (concluded)

c.

General Journal

June

30 Income Summary 74,000

George Avery, Capital 37,000

Dinah Kirk, Capital 37,000

25 Minutes, Medium PROBLEM C.10

COMEDY TODAY

a.

Distribution of Net Income Abbott Martin Net Income

(1) Fixed ratio

(2) Interest on capitals, and fixed ratio

(3) Salaries, interest, and fixed ratio

Net income to be divided 110,000$

Salary allowances to partners 36,000$ 56,000$ (92,000)

Total share to each partner 42,000$ 68,000$ 0$

Income after salary allowances 18,000$

Interest allowances on beginning capital:

Total share to each partner 38,500$ 71,500$ 0$

PROBLEM C.10

COMEDY TODAY (concluded)

b.

General Journal

Journal entry to close Income Summary account

(Case 3 from part a above)

30 Minutes, Medium PROBLEM C.11

ROTHCHILD FURNISHING’S, INC.

Partner Partner Partner Net

Axle Brandt Conrad Income

a. Net income to be divided 526,000$

Salary allowances to partners 10,000$ 50,000$ 28,000$ (88,000)

Income after salary allowances 438,000$

Total share to each partner 226,600$ 196,800$ 102,600$ 0$

b. Net income to be divided 95,000$

Salary allowances to partners 10,000$ 50,000$ 28,000$ (88,000)

Income after salary allowances 7,000$

Interest allowances on capital:

Remaining loss after salary and interest allowances (41,000)$

Allocated in a fixed ratio:

Total share to each partner 11,100$ 53,133$ 30,767$ 0$

Division of Net Income

Interest allowances on capital:

Remaining income after salary and interest allowances 390,000$

Allocated in a fixed ratio:

PROBLEM C.11

ROTHCHILD FURNISHING’S, INC. (concluded)

Partner Partner Partner Net

Axle Brandt Conrad Income (loss)

c. Loss to be divided (32,000)$

Salary allowances to partners 10,000$ 50,000$ 28,000$ (88,000)

Losses after salary allowances (120,000)$

Interest allowances on capital:

Division of Net Income

Remaining loss after salary and interest allowances (168,000)$

Allocated in a fixed ratio:

Total share to each partner (52,400)$ 10,800$ 9,600$ 0$

a.

b.

c.

$ 1,000,000

$ 600,000

Less: Corporate income taxes (40%) ……………………………………

Net income of the business (and dividends received by Weber) ……..

PROBLEM C.12

PRIME CUTS

Several reasons why it might be advantageous for Weber to have incorporated his business

include:

40 Minutes, Strong

Income before taxes ……………………………………………………….

Computation of income that Weber would have retained after income taxes if the business

were still organized as a sole proprietorship:

d.

The term double taxation refers to the concept that corporate income is taxed at two

The corporate form could enable Weber to gradually transfer ownership interests in

the business to his children or other heirs.

Limiting personal liability. For example, in the event that some customers are made ill

Computation of income retained by Weber after income taxes with the

company organized as a corporation:

$ 1,000,000

Income before taxes (also net income) …………………………………..

PROBLEM C.12

PRIME CUTS (concluded)

e.

Drawing as much salary as possible. His salary is a deductible expense to the

corporation in its computation of taxable income. While his salary will still be subject to

Weber might organize the business as an S Corporation. This would eliminate the

There are many ways in which Weber could reduce this “tax bite.” In fact, his current

strategies are maximizing the adverse effects of “double taxation.” Weber should consider:

PROBLEM C.13

RAMIREZ AND SMITH

a.

c.

The preceding schedule shows that Partner Ramirez will have a $14,000 advantage over

Partner Smith in both years. In the first year Ramirez will be credited with income of

$2,000 while Smith will be charged with a loss of $12,000. (The difference between a

30 Minutes, Medium

Income-sharing proposal:

Assuming that the present earning capacity of the two partners reflects the relative value

of their services to the new partnership, the difference in the value of their services should

be recognized by agreeing to a salary allowance of $48,000 per year for Ramirez and

(Part b is on next page.)

PROBLEM C.13

RAMIREZ AND SMITH (concluded)

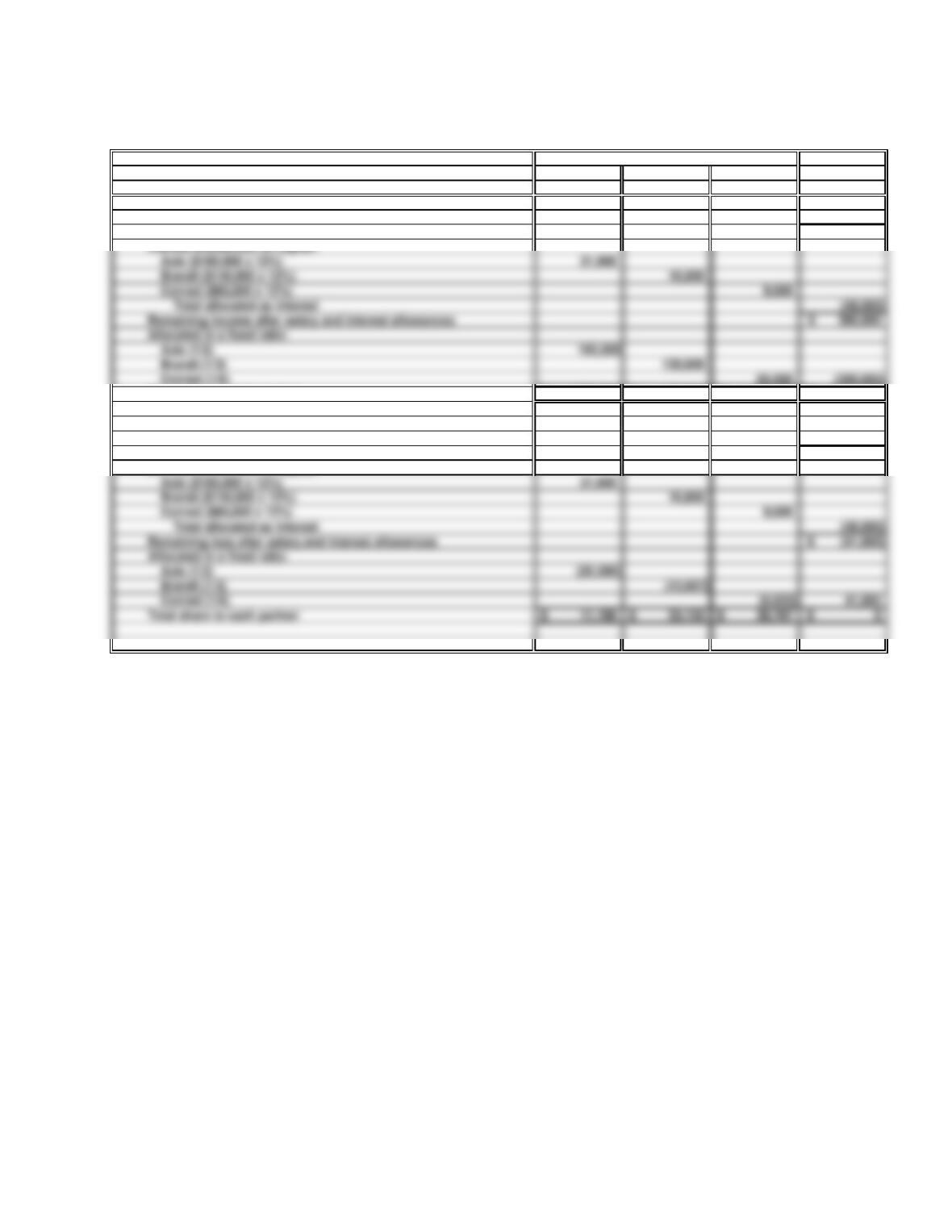

b. RAMIREZ AND SMITH

Division of Partnership Net Income

Net

Income (Loss)

Ramirez Smith Allocated

First year:

Net income (loss) to be divided (10,000)$

Salary allowances to partners 48,000$ 30,000$ (78,000)

Second year:

Net income (loss) to be divided 80,000$

Salary allowances to partners 48,000$ 30,000$ (78,000)

Remaining income (loss) after salary allowances 2,000$

Interest allowances on beginning capital balances:

Remaining income (loss) after salary and interest allowances (22,000)$

Allocated in a fixed ratio:

Total share to each partner 47,000$ 33,000$ 0$

Remaining income (loss) after salary allowances (88,000)$

Interest allowances on beginning capital balances:

Remaining income (loss) after salary and interest allowances (112,000)$

Allocated in a fixed ratio:

Total share to each partner 2,000$ (12,000)$ 0$