A-1

APPENDIX C

FACTORY OVERHEAD VARIANCES

E-1

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred …… $101,750

Budgeted variable factory overhead for 8,000 hrs.

[8,000 × ($31 – $18)] ……………………………………… (104,000)

Variance—favorable ……………………………………… $ (2,250)

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs ($101,750 + $180,000) $281,750

Applied costs (8,000 hrs. × $31) (248,000)

Balance, underapplied factory overhead $ 33,750

Actual Factory Budgeted Factory Applied Factory

Overhead Overhead for Amount Overhead

E-2

a. Controllable variance:

Actual variable factory overhead

($1,428,000 – $300,000) …………………….. $1,128,000

Standard variable factory overhead at

actual production:

Standard hours for actual production ……. 52,000

Variable factory overhead rate1 ……………… × $22

Standard variable factory overhead .. (1,144,000)

Controllable variance—favorable ……………….. $(16,000)

2

Fixed factory overhead rate: hrs. 60,000

$300,000 = $5 per hr.

3

or $1,428,000 – [($22 + $5) × 52,000 hrs.] = $24,000

A-3

E-2, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs $ 1,428,000

Applied costs ($27 × 52,000 hrs.) (1,404,000)

Balance, underapplied factory overhead $ 24,000

Actual Factory Budgeted Factory Applied Factory

Overhead Overhead for Amount Overhead

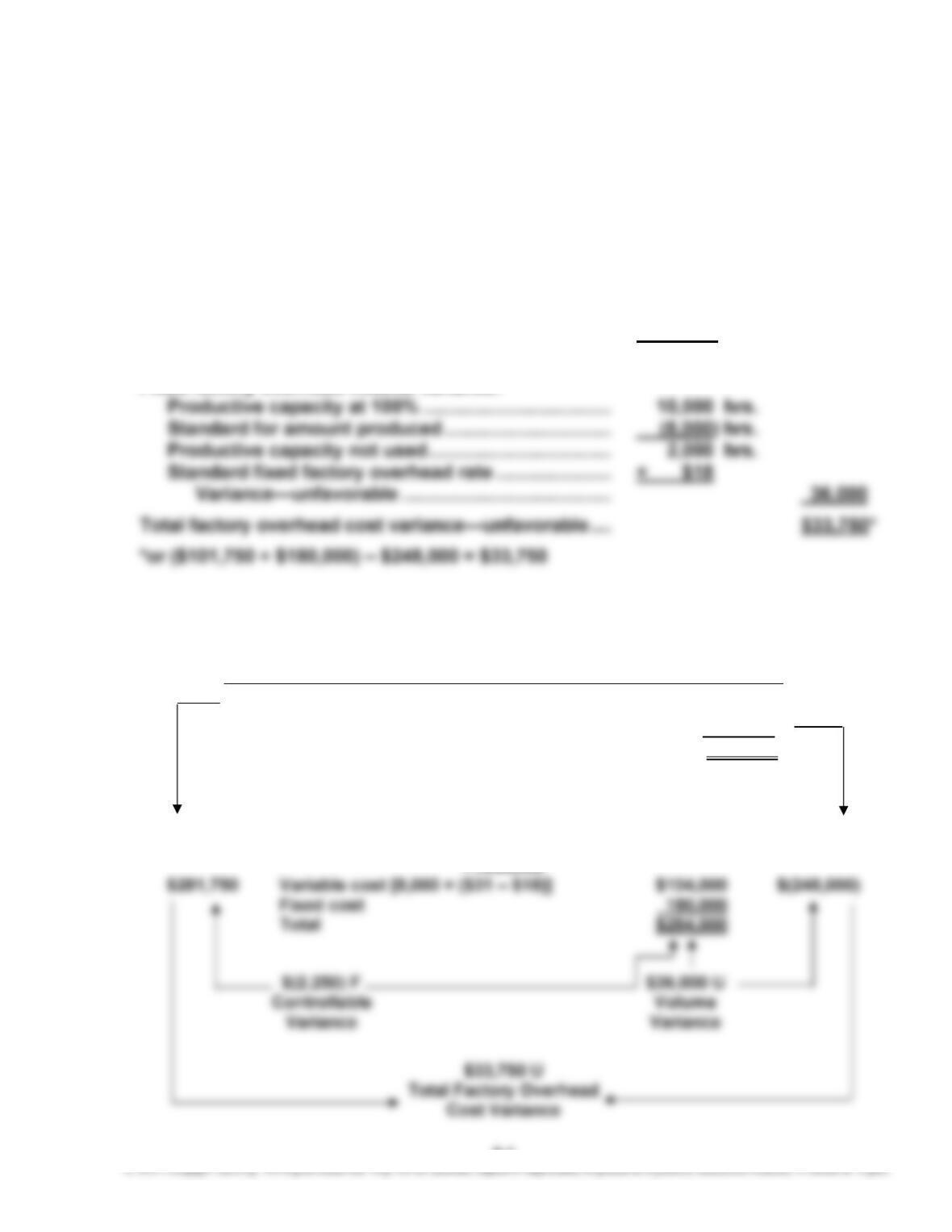

E-3

In determining the volume variance, the productive capacity overemployed (5,000

hours) should be multiplied by the standard fixed factory overhead rate of $3.25

($9.00 – $5.75) to yield a favorable variance of $16,250. The variance analysis pro-

vided by the chief cost accountant incorrectly multiplied the 5,000 hours by the

total factory overhead rate of $9.00 per hour and reported it as unfavorable.

A correct determination of the factory overhead cost variances is as follows:

Total factory overhead cost variance—favorable ……… $(20,000)

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs ($600,000 + $325,000) $925,000

Applied costs (105,000 hrs. × $9.00) (945,000)

Balance, overapplied factory overhead $ (20,000)

A-5

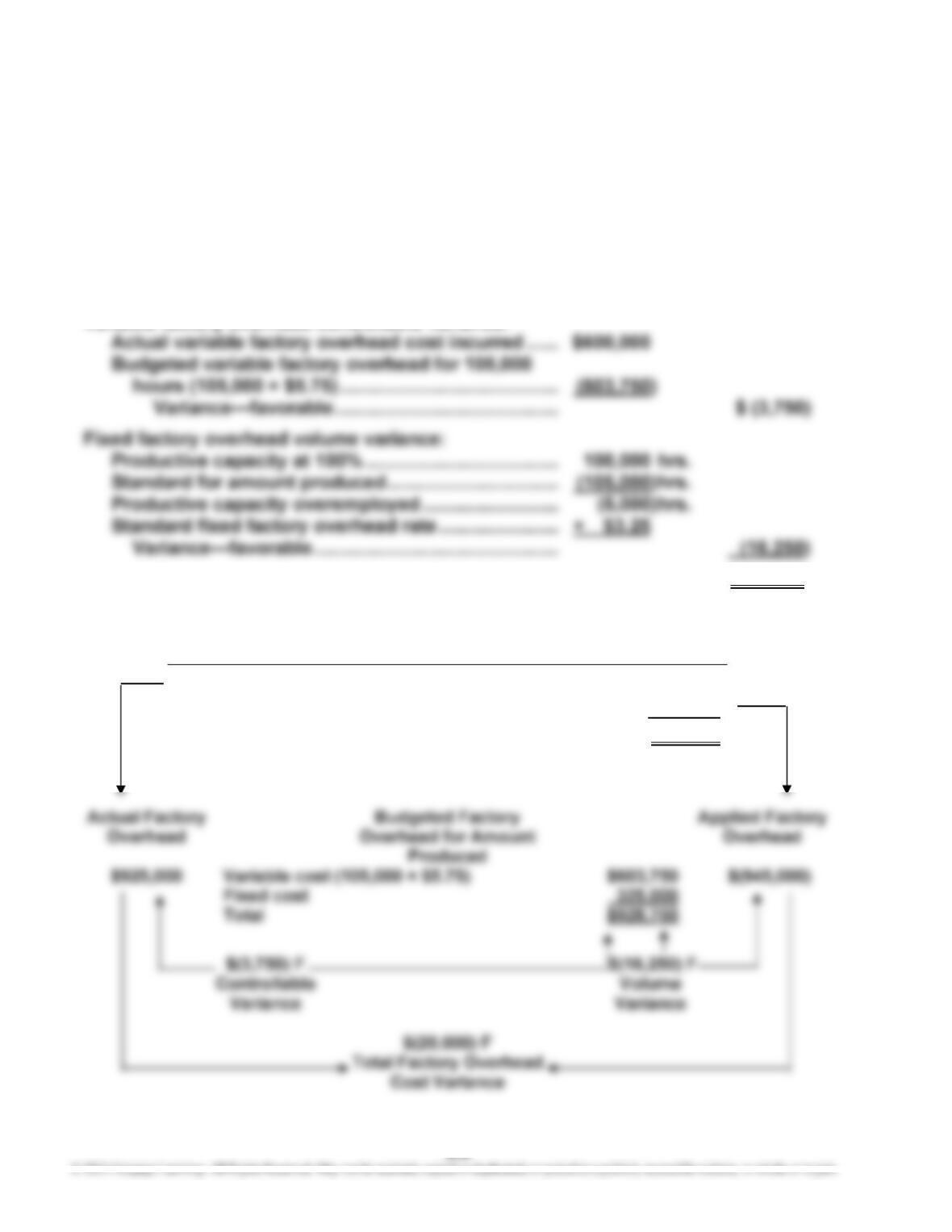

E-4

A B C D E

1 TOPEKA PLASTICS INC.

2 Factory Overhead Cost Variance Report—Trim Department

3 For the Month Ended July 31

6

7 Budget

(at Actual

Production)

8 Variances

9 Actual Unfavorable Favorable

10 Variable factory overhead cost:*

11 Indirect factory labor $ 23,250 $ 22,400 $ 850

12 Power and light 20,000 20,160 $ (160)

13 Indirect materials 11,100 10,080 1,020

14 Total variable factory overhead

cost $ 54,350 $ 52,640

15 Fixed factory overhead cost:

16 Supervisory salaries $ 50,000 $ 50,000

17 Depreciation of plant and

*The budgeted variable factory overhead costs are determined by multiplying

28,000 hours by the variable factory overhead cost rate for each variable cost

category. These rates are determined by dividing each budgeted amount (esti-

mated at the beginning of the month) by the planned (budgeted) volume of

25,000 hours as shown below.

E-4, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs $148,850

Applied costs [28,000 × ($1.88* + $3.15)] (140,840)

Balance, underapplied factory overhead $ 8,010

Actual Factory Budgeted Factory Applied Factory

*$47,000 ÷ 25,000 hours budgeted at the beginning of the month

A-7

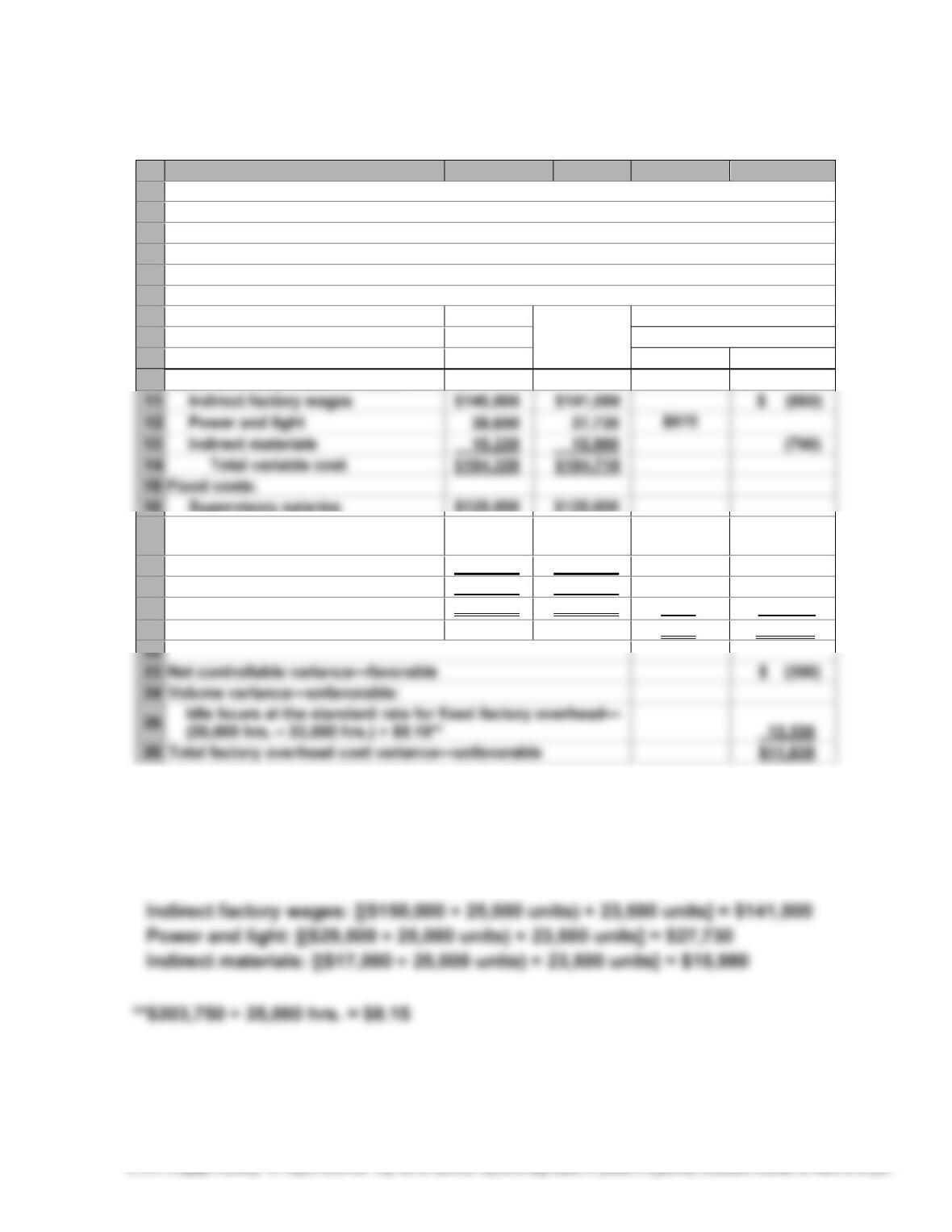

P-1

A B C D E

1 SEABURY, INC.

2 Factory Overhead Cost Variance Report—Assembly Department

3 For the Month Ended October 31

4 Normal capacity for the month 25,000 hrs.

5 Actual production for the month 23,500 hrs.

6

7 Budget

8 (at Actual Variances

9 Actual Production) Unfavorable Favorable

10 Variable factory overhead costs:*

16 Supervisory salaries $125,000 $125,000

17 Depreciation of plant and

equipment 49,000 49,000

18 Insurance and property taxes 29,750 29,750

19 Total fixed cost $203,750 $203,750

20 Total factory overhead cost $388,070 $388,460

21 Total controllable variances $870 $ (1260)

*The budgeted variable costs are determined by multiplying the budgeted variable

costs per unit at planned production times the actual production for October. The

budgeted variable costs per unit are determined by dividing the budgeted variable

cost for October by the planned production for October. Thus, the budgeted

variable costs are determined as follows:

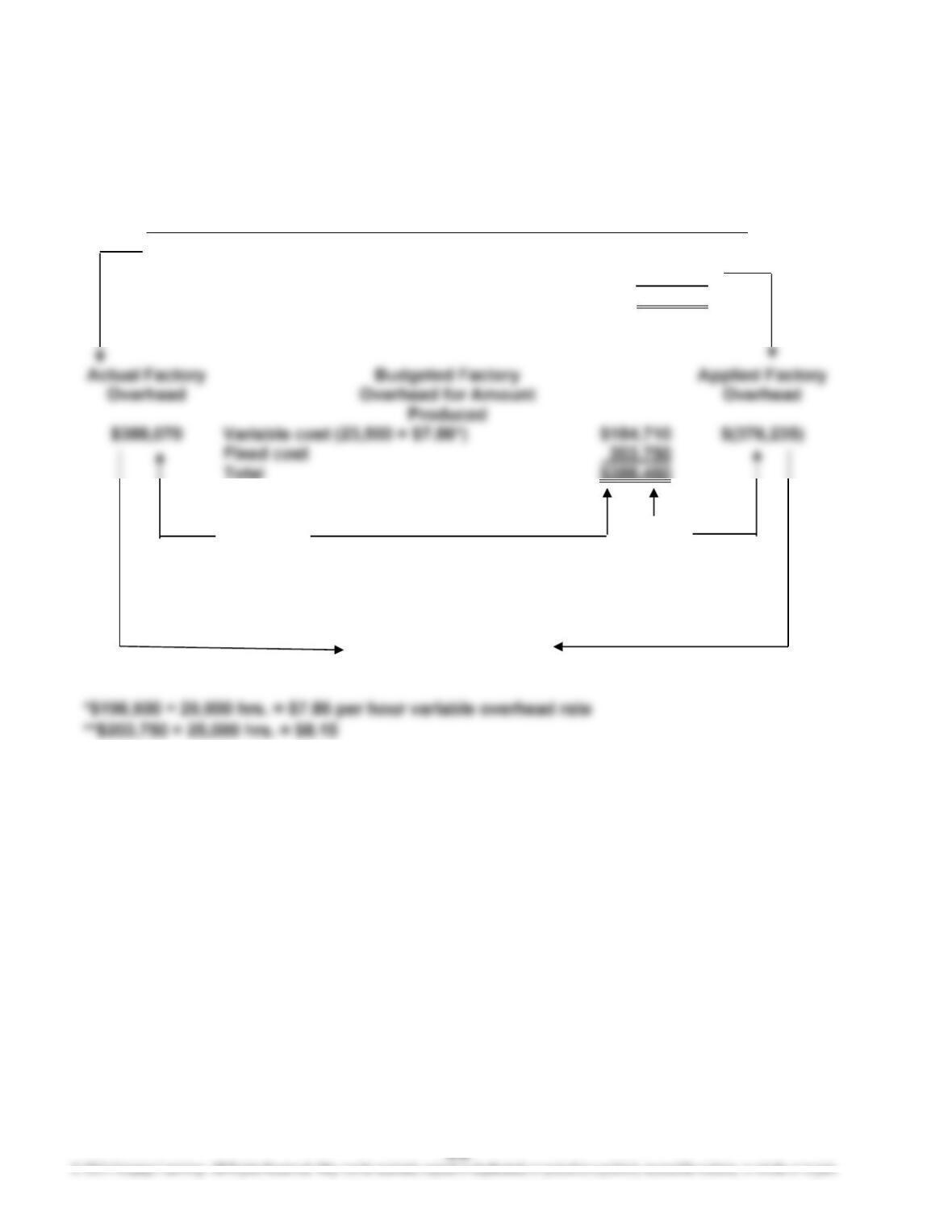

P-1, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs $388,070

Applied costs [23,500 hrs. × ($7.86* + $8.15**)] (376,235)

Balance, underapplied factory overhead $ 11,835

Total $388,460

$(390) F $12,225 U

Controllable Volume

Variance Variance

$11,835 U

Total Factory Overhead

Cost Variance

A-9

P-2

The plant manager is placing pressure on the controller because the controllable

variance is unfavorable. The claim is that these costs are not variable at all. This

claim is difficult to accept. This small company purchases its power from the out-

side. The power and light bill is variable to the amount of energy used in the

plant. Energy usage is likely a function of the number of units produced. Like-

wise, the supplies are likely variable to machine usage, which is also related to

the number of units produced. However, these two costs are not where the prob-

lem lies. The problem is with the indirect factory wages.