FORMS OF BUSINESS ORGANIZATIONS

Problems

C.1

E-Z Manufacturing Company 15 Easy

LO C-3,

C-10

Students are required to calculate partners’ share of net income, determine

the effects of income taxes for partners, and prepare a statement of

partners’ equity.

C.2

Waffon Corporation 15 Easy

LO C-6,

C-7

Students must analyze the effects of stockholders’ investments, net

income, and dividends on stockholders’ equity.

C.3

Guenther and Firmin 15 Easy

LO C-10

Students are required to distribute net income to partners, including

interest, salaries, and residual amounts.

C.4

Snack Shack 30 Medium

LO C-3

Students are required to demonstrate their understanding of partnership

accounts and the nature of partnership income.

C.5

The Top Hat, Inc. 25 Medium

LO C-6,

C-7

Record typical equity transactions for a corporation and prepare a

statement of retained earnings.

C.6

Frontier Western Wear, Inc. 30 Medium

LO C-4-

C-7

Make entries to record equity transactions for a corporation and close

Income Summary and Dividends accounts. Prepare the stockholders’

equity section of a corporation’s balance sheet.

C.7

Wesson Corporation and Amber Industries 25 Easy

LO C-6,

C-7

Prepare the stockholders’ equity section of the balance sheet of two

different corporations.

C.8

S & X Co. 45 Strong

LO C-1,

C-2, C-4-

C-8

Prepare entries to record owner’s equity transactions in a sole

proprietorship and in a corporation. Contrast the nature of net income for

these two types of business organizations.

Below are brief descriptions of each problem. These descriptions are accompanied by the estimated time (in

minutes) required for completion and by a difficulty rating. The time estimates assume use of the partially

filled-in working papers.

APPENDIX C

Avery and Kirk 20 Easy

Formation of a partnership, journal entries, and a beginning balance

sheet. Entries to close the Income Summary account and drawing

accounts.

Comedy Today 25 Medium

Profit sharing under a variety of agreements. Includes fixed ratio;

interest on beginning capital accounts and fixed ratio for balance;

salaries to partners, interest on capital accounts, and balance in fixed

ratio. Journal entry to close the Income Summary account.

Rothchild Furnishings, Inc. 30 Medium

Sharing of income in a partnership when partnership agreement

provides for salaries to partners, interest on invested capital, and

balance in a fixed ratio. Separate cases handling a loss, a small profit,

and a large profit.

Prime Cuts—a Tax Planning Case 40 Strong

An individual has recently incorporated his business and is now being

“hammered” by the effects of double taxation. Students are to

compute the overall tax burden of the corporation compared to the

former proprietorship and to make tax planning recommendations. A

very practical “eye opener” to the importance of tax planning.

Ramirez and Smith 30 Medium

Given the plans, personal backgrounds, and financial status of two

individuals planning a partnership, draft an income-sharing agreement

that will provide an equitable division of partnership income between

them. Also, prepare a 2-year schedule showing how the recommended

plan will work out under forecasts of earnings. Write a defense of the

profit-sharing plan in the light of the division of earnings over the 2-

year period.

* Supplemental Topic , “Partnership Accounting—A Closer Look.”

*C.9

LO

C-3, C-9,

C-10

*C.10

LO C-10

*C.13

LO C-10

*C.11

LO C-10

C.12

LO

C-1, C-4,

C-5, C-9

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

4.

5.

Salaries of owner-managers are an expense deducted in arriving at the net income of a

Neither the house nor the mortgage should appear in the financial statements of Hansen Sporting

The primary advantages of the partnership form of organization are the opportunity to bring

together sufficient capital to carry on a business and the opportunity to combine the specialized

There are two important reasons why this type of business would probably be organized as a

limited partnership rather than as a general partnership. First, the 50 investors throughout the

7. a.

Owners’ liability for debts of the business. Partners are jointly and individually liable for

b.

Transferability of ownership interest. A partnership interest can be transferred only if the

c.

Continuity of existence. A partnership is terminated upon the resignation or death of any

d.

Federal taxation on income. A corporation is subject to federal income tax on its income,

8.

*9.

*10.

Consideration should be given to differences in the contributions of the partners to the business

One factor to be considered is that the salary allowance has first priority in the division of

income among the partners. A second factor is the difference in the share of the residual

The term double taxation refers to the fact that the income of a corporation is taxed at two

SOLUTIONS TO PROBLEMS

b.

c.

Gonzales Todd Walker Total

$ 50,000 $ 60,000 $ 40,000 $ 150,000

$ 110,000 $ 120,000 $ 100,000 $ 330,000

$ 85,000 $ 97,000 $ 65,000 $ 247,000

Balances, December 31, 20xx

Add: Net income for the year

Subtotals

Less: Drawings

15 Minutes, Easy

Statement of Partners’ Equity

For the Year Ended December 31, 20xx

E-Z MANAUFACTURING COMPANY

PROBLEM C.1

Each partner must report his share of net income of the partnership ($60,000) on his or her

personal income tax return.

E-Z MANUFACTURING COMPANY

Balances, January 1, 20xx

PROBLEM C.2

WASSON CORPORATION

a.

15 Minutes, Easy

Additional investment $20,000 [$50,000 (ending capital stock balance) – $30,000 (beginning

capital stock balance)].

*

Net

Guenther Firmin Income

$ 247,000

$ 80,000 $ 60,000 (140,000)

PROBLEM C.3

15 Minutes, Easy

Net income to be divided

GUENTHER AND FIRMIN

Salary allowances to partners

$ 107,000

$ 80,000

$ 143,000 $ 104,000 $ 0

Total share to each partner

Income after salary allowances

Interest allowances on beginning capital:

Guenther ($100,000 × 15%)

Firmin ($80,000 × 15%)

Remaining income after salaries and interest

Guenther (60%)

Firmin (40%)

b.

Glen Chow Wilkes Total

Beginning capital balance $ 55,000 $ 60,000 $ 5,000 $ 120,000

Add: Net income 30,000 30,000 30,000 90,000

Less: Drawing 15,000 15,000 25,000 55,000

Ending capital balance $ 70,000 $ 75,000 $ 10,000 $ 155,000

c.

d.

PROBLEM C.4

30 Minutes, Medium

Assuming that each partner devoted the same amount of time to the business, Glen and

Partnership net income should compensate partners for their services to the business,

Snack Shack

Statement of Partners’ Equity

For the Year Ended December 31, 20xx

SNACK SHACK

PROBLEM C.5

THE TOP HAT, INC.

a.

General Journal

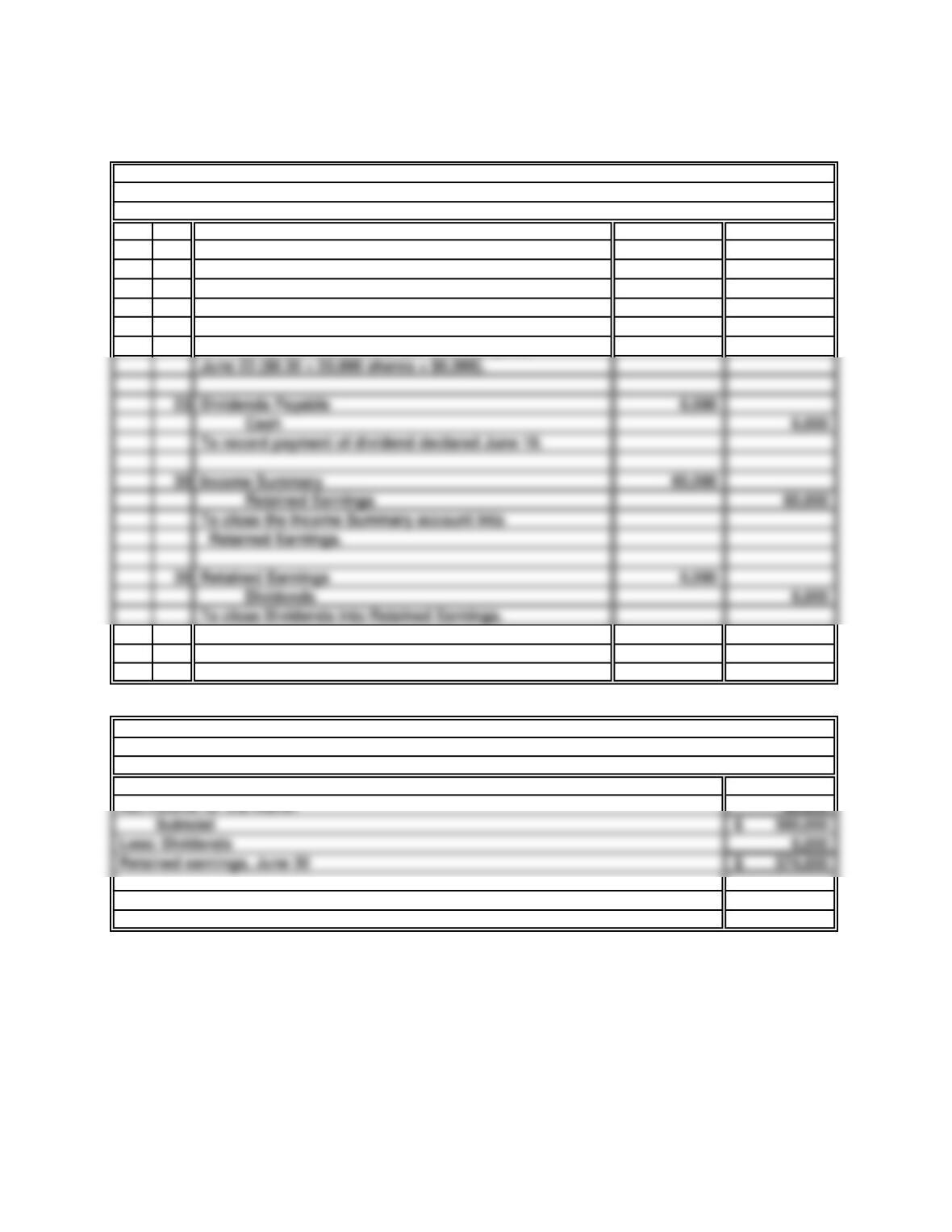

Jun 3 Cash 20,000

Capital Stock 20,000

Issued 1,000 shares of capital stock at $20 per share.

10 Dividends 6,000

Dividends Payable 6,000

Declared a dividend of $0.30 per share, payable

b.

Retained earnings, May 31 520,000$

25 Minutes, Medium

THE TOP HAT, INC.

Statement of Retained Earnings

For the Month Ended June 30, 20xx

PROBLEM C.6

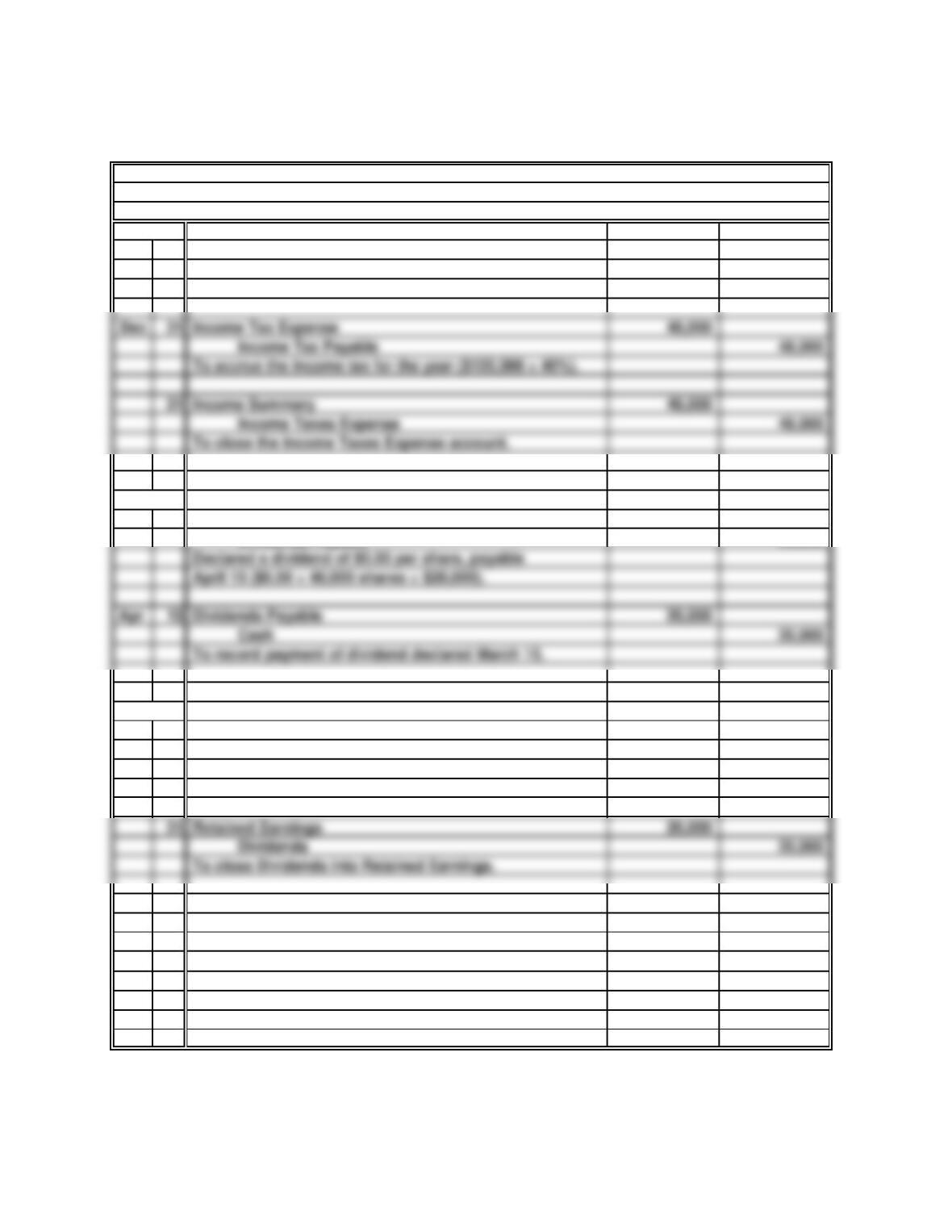

FRONTIER WESTERN WEAR, INC.

a.

General Journal

2017

Jan 15 Cash 800,000

Capital Stock 800,000

Issued 40,000 shares of capital stock at $20 per share.

b.

2018

Mar 15 Dividends 20,000

Dividends Payable 20,000

c.

2018

Dec 31 Retained Earnings 18,000

Income Summary 18,000

To close the Income Summary account for a period

with a net loss.

30 Minutes, Medium

PROBLEM C.6

FRONTIER WESTERN WEAR, INC. (concluded)

d. FRONTIER WESTERN WEAR, INC.

Partial Balance Sheet

December 31, 2018

Stockholders’ equity:

Computation of retained earnings at December 31, 2018:

Income before income tax—2017 120,000$

Less: Income tax expense 48,000

Less: Net loss for 2018 18,000 38,000

Retained earnings, December 31, 2018 34,000$

25 Minutes, Easy PROBLEM C.7

WESSON CORPORATION AND AMBER INDUSTRIES

a. WESSON CORPORATION

Partial Balance Sheet

December 31, 2018

Stockholders’ equity:

Capital stock 250,000$

Retained earnings 21,000*

b.

AMBER INDUSTRIES

Partial Balance Sheet

December 31, 2018

Stockholders’ equity:

Capital stock 1,000,000$