Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Appendix C

C-1

Appendix C

Activity-Based Costing

QUESTIONS

1. Manufacturing overhead costs cannot be directly traced to units of product like

2. In the first stage, service department costs are assigned to operating departments.

3. Operating departments are directly involved in manufacturing or selling the products

4. Activity-based costing (ABC) is a method for allocating shared costs among

departments or products. It is especially common for overhead allocation. The goal

5. Anything to which costs would be assigned is considered a “cost object.” Common

6. An activity cost driver is the measure of the activity that causes costs to be incurred.

7. Activity-based costing is typically used when a company produces many different

8. Typical activity cost pools include: purchasing, order processing, accounting,

engineering, factory maintenance, and legal services (other answers are possible).

10. While ABC may provide more accurate cost assignments, the additional cost to

implement activity-based costing may not be justified. That is, the value of the

11. Activity-based costing may be used in any type of organization. The premise of ABC

is that activities cause costs. Since all organizations engage in activities, these

QUICK STUDIES

Quick Study C-1 (10 minutes)

Quick Study C-2 (10 minutes)

2. Assign overhead costs to Fast and Standard models

Fast

C-3

Quick Study C-3 (15 minutes)

Expected Activity Activity

Activity Cost Driver Rate

Quick Study C-4 (10 minutes)

2. Assign technical support costs to each model

C-4

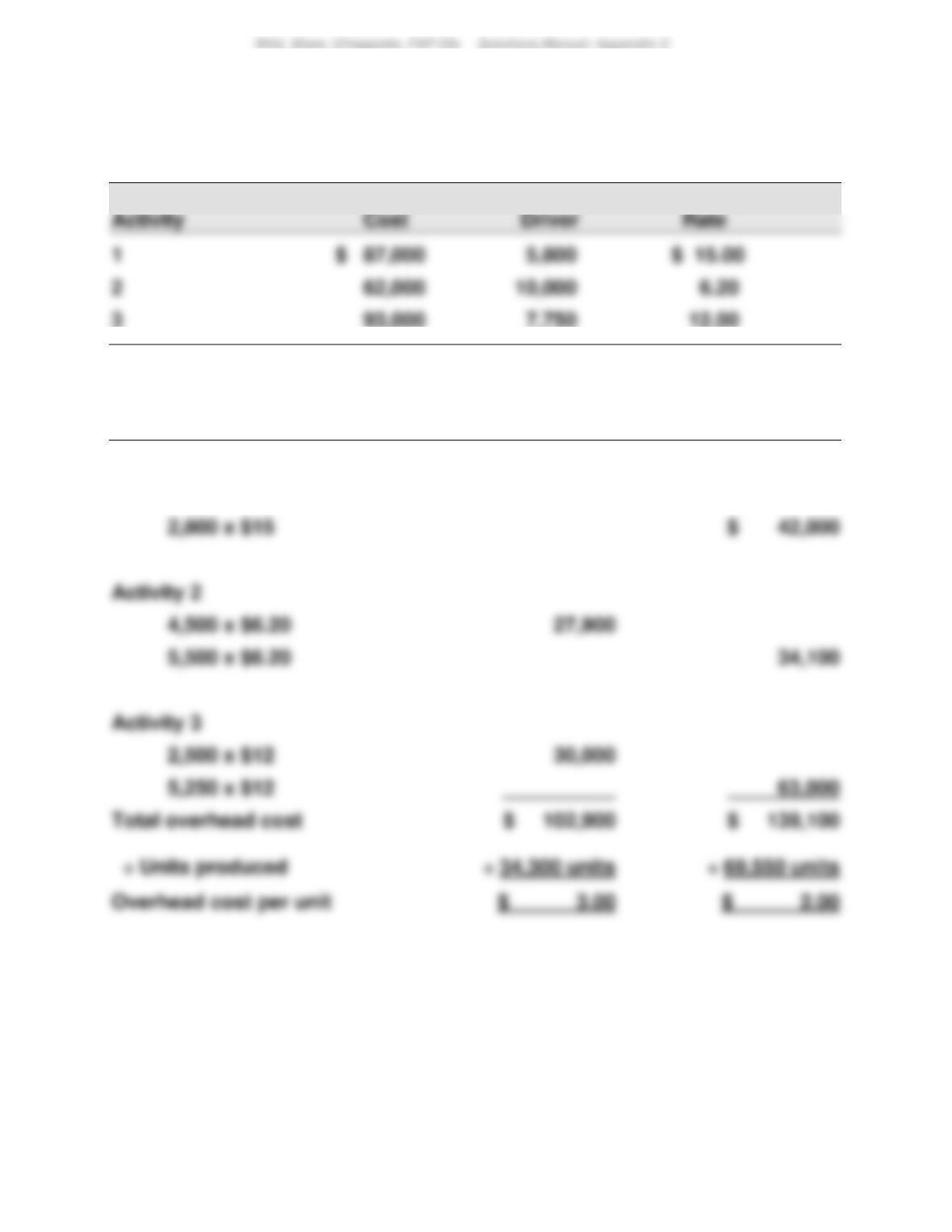

Quick Study C-5 (15 minutes)

1.

Expected Activity Activity

2.

Standard Deluxe

Activity 1

3,000 x $15 $ 45,000

Quick Study C-6 (15 minutes)

Overhead cost allocation of indirect labor and supplies to Department 1:

Rate: ($5,400 + $2,600) / $32,000 = $0.25 / $ of labor cost

Quick Study C-7 (5 minutes)

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Appendix C

EXERCISES

Exercise C-1 (25 minutes)

1. $1,004,000 + $465,300 + $232,000 = $283.55 per machine hour

6,000 machine hours

2. Model 145

Materials and labor $250.00

3. Model 145 Model 212

Price per unit $800.00 $470.00

Exercise C-2 (35 minutes)

1.

Components

Changeover $500,000 / 800 batches $625/batch

Model 145 Model 212

Changeover

400 batches x $625/batch $ 250,000 $ 250,000

Machining

C-8

Exercise C-2 (concluded)

2. Model 145 Model 212

3. Model 145 Model 212

Price per unit $800.00 $470.00

Exercise C-3 (35 minutes)

1. Total direct labor hours:

Product A: 10,000 units x 0.20 DLH/unit = 2,000 DLH

Exercise C-3 (continued)

Product A Product B

Direct materials

A: 10,000 units x $2/unit $ 20,000

2. Product A Product B

Price per unit $20.00 $60.00

Exercise C-3 (concluded)

3. Overhead rates

Machine setup $121,000/(10 + 12) setups $5,500/setup

4. Product A Product B

Price per unit $20.00 $ 60.00

Exercise C-4 (20 minutes)

1.

Client consultation $270,000/1,500 contact hours $180/con.hr.

2.

Client consultation 450 contact hours x $180/con. hr. $ 81,000

Exercise C-5 (25 minutes)

Part 1

Part 2

Determination of cost per driver unit

Cost Center

Cost

Driver

Cost per Driver

C-12

Exercise C-5 (continued)

Part 3

Allocation of costs to the general surgery department using ABC

GENERAL SURGERY

Cost

Driver

Cost per

Driver Unit

Allocated

Cost

Exercise C-6 (30 minutes)

Calculation of predetermined overhead rates to apply ABC

Overhead Cost

Category (Activity

Cost Pool)

Total

Cost

Total Amount

of Cost Driver

Predetermined Overhead Rate

Supervision …………………………

$36,000

of direct labor cost

Depreciation ………………………..

per machine hour

Line preparation ………………….

per setup

1. Assignment of overhead costs to the two products using ABC

Rounded edge

Cost

Driver

Cost per

Driver Unit

Assigned Cost

Supervision ……………………….

Machinery depreciation ……..

$ 28.30

$184.00

Total overhead assigned ……

Driver Unit

Assigned Cost

Supervision ……………………….

Machinery depreciation ……..

$ 28.30

$184.00

Total overhead assigned ……

2. Average cost per foot of the two products

Rounded edge

Squared edge

Direct materials ………………………

$19,000

$ 43,200

Overhead (using ABC) ……………

Total cost ……………………………….

$54,540

$151,660

Average cost per foot (ABC)* …..

3. Using ABC, the average cost of rounded edge shelves declines and the

average cost of squared edge shelves increases. Under the current

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Appendix C

C-14

PROBLEM SET A

Problem C-1A (40 minutes)

1. Grinding & Polishing ($320,000+$135,000)/13,000 MH $35/MH

2.

Job 3175

Job 4286

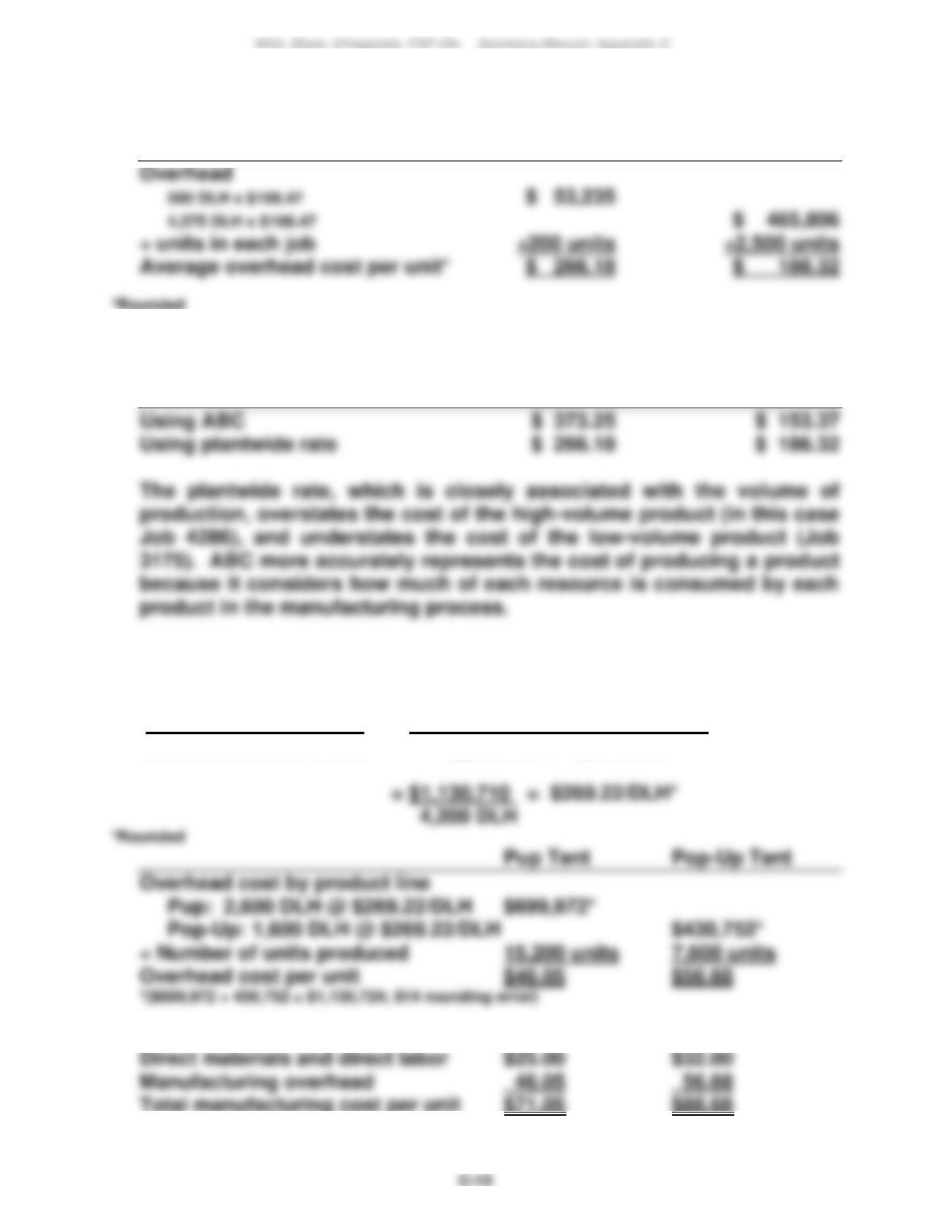

3. Job 3175 Job 4286

4. Plantwide rate

Grinding ……………………………………………………………………. $ 320,000

Problem C-1A (concluded)

Job 3175 Job 4286

5. Average overhead cost

Job 3175 Job 4286

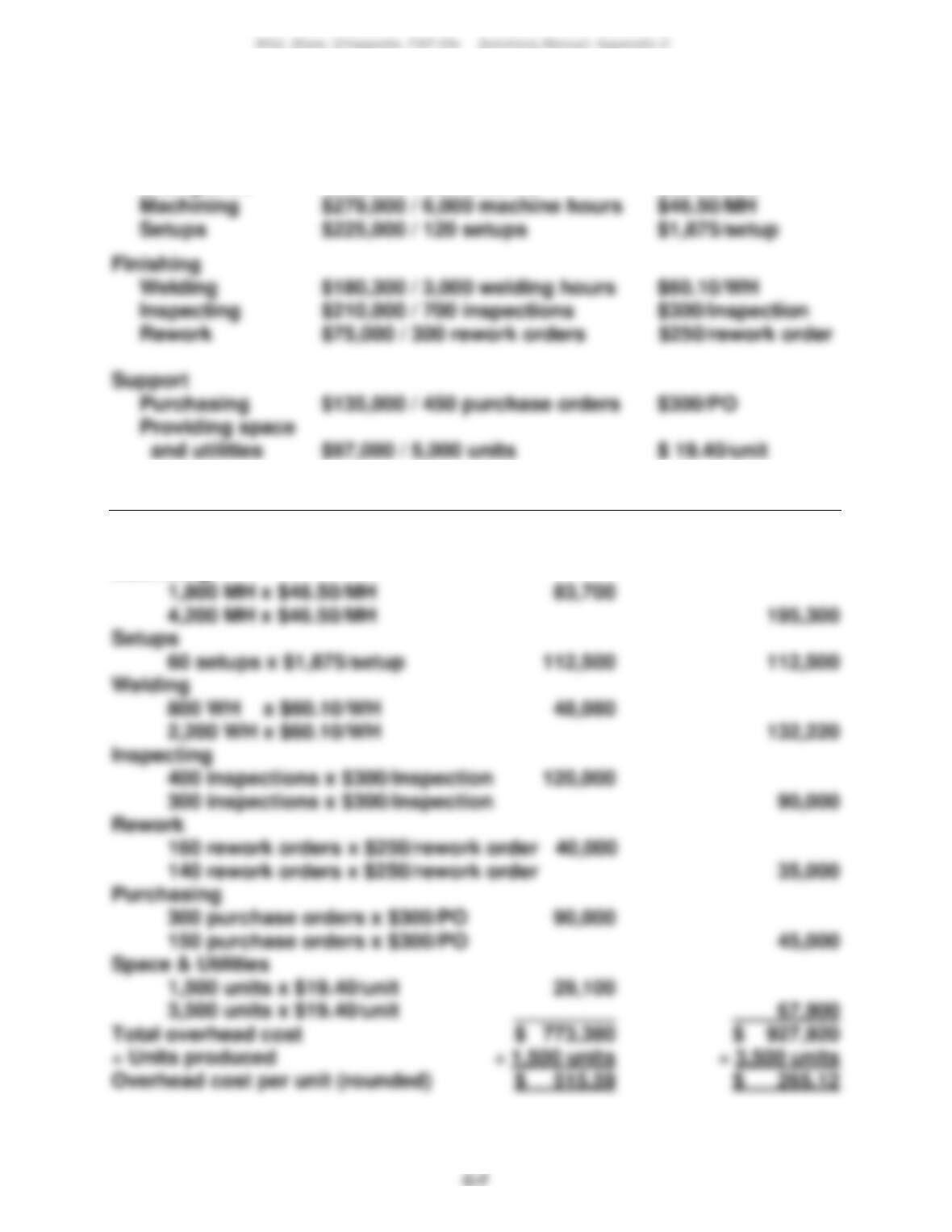

Problem C-2A (50 minutes)

1. Total overhead = $215,630 + $399,480 + $515,600

Total direct labor hours 2,600 DLH + 1,600 DLH

2. Total manufacturing cost per unit:

C-16

Problem C-2A (continued)

3. Gross profit per unit

4. Pattern alignment $64,400/560 batches $115/batch

Pup Tent

Pop-Up Tent

Pattern alignment

140 batches x $115…

$ 16,100

420 batches x $115

$ 48,300

Cutting

7,000 MH x $4.10

28,700

5,300 MH x $4.10

21,730

Moving product

800 moves x $42

1,600 moves x $42

Sewing

2,600 DLH x $78

1,600 DLH x $78

124,800

Inspecting

240 insp. x $40

360 insp. x $40

Folding

15,200 units x $2.10

7,600 units x $2.10

Providing space

4,300 sq. ft. x $6

4,300 sq. ft. x $6

Material handling

Total overhead

$508,520

÷ units

C-17

5.

Pup Tent Pop-Up Tent

Selling price $65.00 $200.00

6. Departmental overhead rates based on direct labor hours and machine

hours are still volume-based measures and would not improve the