B.1 15 Easy

LO

B.2 20 Medium

LO

B-3, B-4

B.3 15 Medium

LO

B.4 15 Medium

LO

B.5 20 Medium

LO

B.6 35 Strong

LO

B.7 25 Strong

LO

B-5, B-6

B-1,

B-2, B-4

B-1,

B-2, B-5

B-3,

B-5, B-6

B-3,

B-5, B-6

B-3,

B-5, B-6

Use of Future Amount Tables

A company sells land in exchange for a long-term note bearing an

unrealistically low interest rate, but the accountant records the transaction at

the face amount of the note. Student is asked to discount the note at a

realistic rate of interest, record the transaction properly, and explain the

effects of the accountant’s error upon the company‘s net income.

Entries to record a capital lease of equipment in the accounting records of

both the lessor and the lessee. Emphasizes allocation of monthly payments

between interest and principal. Also, computation of carrying value of

leased equipment and lease payment obligation.

Determine the present value of an installment note payable that includes an

interest charge in the face amount. Prepare journal entries to record issuance

of the note and the first monthly payment, using the effective interest method

to determine interest expense.

Short exercises in the use of present value tables to determine the present

value of future amounts, annuities, and annuities with a “balloon” payment.

Richland Farms

Custom Truck Builders and Interstate Van Lines

Short exercises in the use of future amount tables to determine the

future amounts of initial investments, annuities, and a combination of

an initial investment and an annuity.

Tilman Company

Use of future value tables to determine the amount of the annual payment for

a sinking fund. The student also is required to prepare a journal entry to

redeem the related bonds.

Use of Present Value Tables

Showcase Interiors

Rural Gas & Electric Co.

Use present value techniques to compute the issuance price of bonds

that sell at a market interest rate above the contract rate. Also, prepare

a journal entry to record issuance of the bonds.

APPENDIX B

Problems

THE TIME VALUE OF MONEY:

FUTURE AMOUNTS AND PRESENT VALUES

Below are brief descriptions of each problem. These descriptions are accompanied by the estimated time

(in minutes) required for completion and by difficulty rating. The time estimates assume use of the

partially filled-in working papers.

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

2.

3.

4.

5. a.

The longer the time until the future cash flow will occur, the smaller its present value. In

6.

8.

Assuming no change in expected cash flows, present values change with changes in (a) current

Financial instruments include cash, equity investments in other businesses, and contracts calling

7.

Short-term accounts receivable and accounts payable are contracts calling for cash receipts or cash

The phrase time value of money recognizes that the value of money varies depending upon when it

The present value of a future amount is the amount that a knowledgeable investor would pay today

The two factors that determine the difference between the present value and the future amount of

The three basic investment applications of the time-value of money include:

15 Minutes, Easy

SOLUTIONS TO PROBLEMS

PROBLEM B.1

USE OF FUTURE AMOUNT TABLES

a. $60,000 x 1.791 (from Table FA-1) = $107,460 future value

$ 132,644

c. 20,000 x 14.487 (from Table FA-2) = $289,740 future value

at future value.)

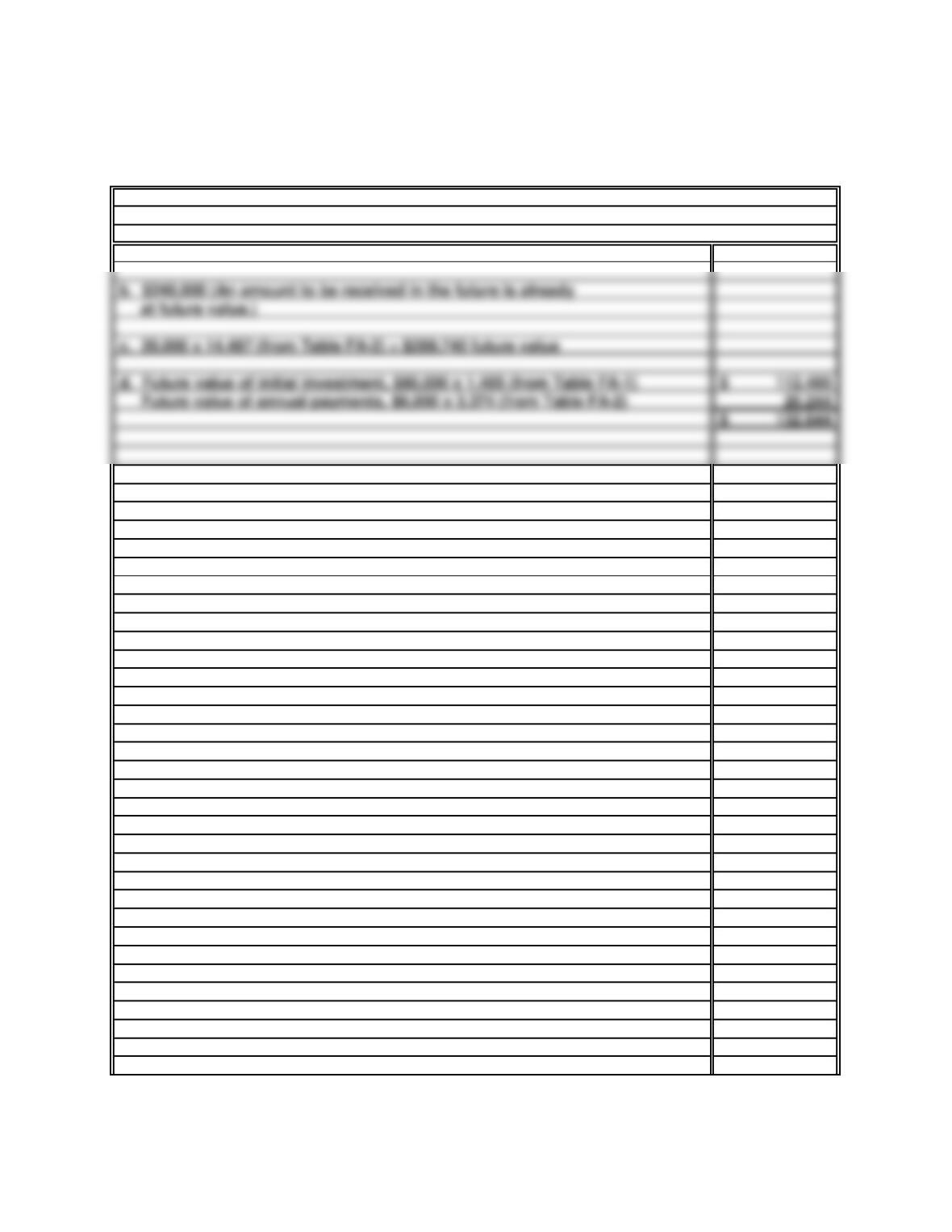

20 Minutes, Medium

a. $ 10,926

c. 500,000

$500,000 ÷ 45.762 (from Table FA-2)

TILMAN COMPANY

PROBLEM B.2

Annual payment:

General Journal

Bond Payable

20 years)

$500,000 – $218,520 ($10,926 annual payment x

Interest earned:

15 Minutes, Medium

a.

d.

Total

Total

Alternative 2:

Add:

Present value of $25,000 received annually for three years, discounted

at 8%: $25,000 x 2.577 (from Table PV-2)

Present value of $15,000 received annually for five years, discounted at

8%: $15,000 x 3.993 (from Table PV-2)

Add: Present value of additional $10,000 received annually during first

three years, discounted at 8%: $10,000 x 2.577 (from Table PV-2)

shown below:

PROBLEM B.3

TABLES

USE OF PRESENT VALUE

$15,000 x 7.360 (from Table PV-2) = $110,400 Present Value

There are several ways to approach this problem. Two alternatives are

Alternative 1:

b.

per month: $300 x 27.661 (from Table PV-2)

Present value of $300 paid monthly for 36 months, discounted at 1 1/2%

present value

Present value of $12,000 due in 36 months, discounted at 1 1/2%

per month: $12,000 x .585 (from Table PV-1)

Total

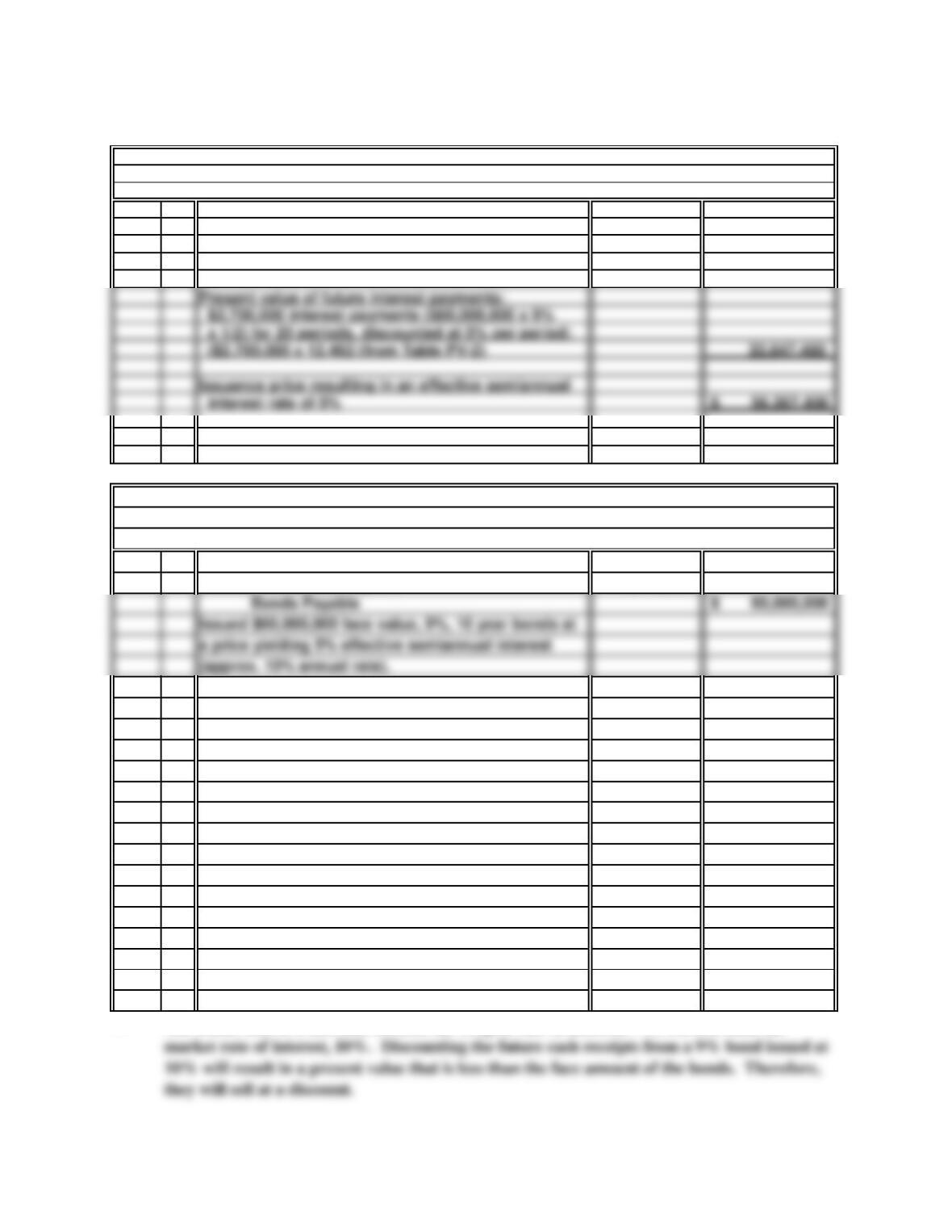

15 Minutes, Medium

a.

22,620,000$

June 30 $ 56,267,400

3,732,600

Bonds Payable 60,000,000$

Issued $60,000,000 face value, 9%, 10 year bonds at

(approx. 10% annual rate).

c.

The bonds sold at a discount because the coupon rate of interest, 9%, was less than the

General Journal

Discount on Bonds Payable

Cash

b.

PROBLEM B.4

(from Table PV-1)

discounted at 5% per period: $60,000,000 x .377

Present value of future principal payment:

RURAL GAS & ELECTRIC CO.

$60,000,000 due after 20 semiannual periods,

33,647,400

Issuance price resulting in an effective semiannual

interest rate of 5%

($2,700,000 x 12.462 (from Table PV-2)

x 1/2) for 20 periods, discounted at 5% per period:

Present value of future interest payments:

$2,700,000 interest payments ($60,000,000 x 9%

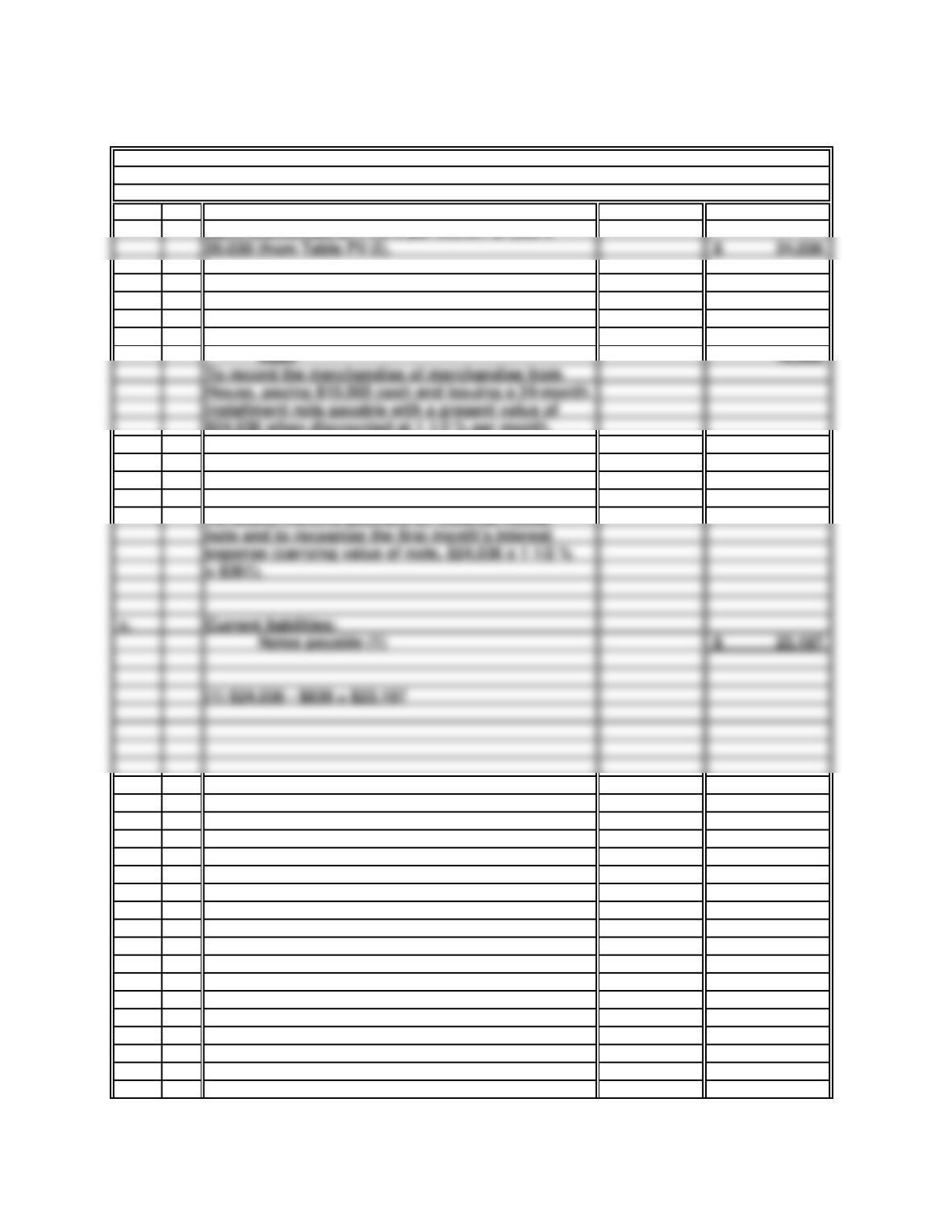

20 Minutes, Medium

a.

b.

Dec 1 34,536

Notes Payable 24,036

installment note payable with a present value of

To record the merchandise of merchandise from

House, paying $10,500 cash and issuing a 24-month

Dec 31 839

361

Cash 1,200

c.

Notes payable (1) 23,197$

(1) $24,036 – $839 = $23,197

note and to recognize the first month’s interest

expense (carrying value of note, $24,036 x 1 1/2 %

= $361).

Current liabilities:

PROBLEM B.5

each, discounted at 1 1/2% per month: $1,200 x

SHOWCASE INTERIORS

Inventory

Present value of 24 monthly payments of $1,200

$24,036 when discounted at 1 1/2 % per month.

Notes Payable

Interest Payable

To record monthly payment on Colonial House

24,036$

20.030 (from Table PV-2).

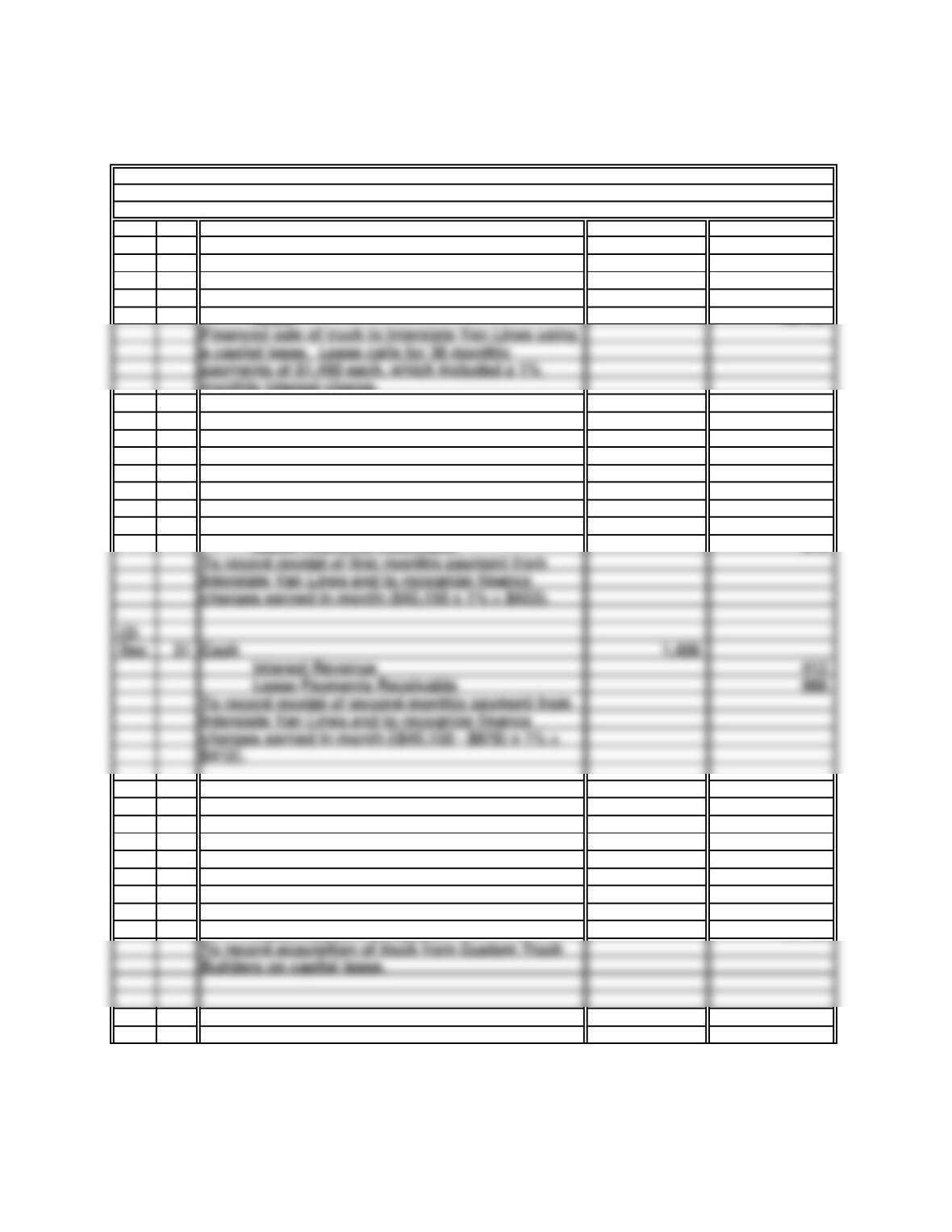

35 Minutes, Strong

a.

2018

(1)

Nov 1 42,150

Sales 42,150

1 33,520

Inventory 33,520

(2)

30 1,400

Interest Revenue 422

978

(3)

Dec 31 1,400

Interest Revenue 412

988

Interstate Van Lines and to recognize finance

charges earned in month [($42,150 – $978) x 1% =

Lease Payments Receivable

Cash

To record receipt of first monthly payment from

To record receipt of second monthly payment from

Interstate Van Lines and to recognize finance

charges earned in month ($42,150 x 1% = $422).

b.

2018

(1)

Nov

1 42,150

42,150

To record acquisition of truck from Custom Truck

Builders on capital lease.

monthly interest charge.

Cost of Goods Sold

To record cost of truck sold under capital lease.

General Journal

Entries to record capital lease transactions in

Cash

Lease Payments Receivable

Lease Payments Receivable

Leased Equipment

Lease Payment Obligation

Entries to record capital lease transactions in

lessee’s accounting records:

PROBLEM B.6

lessor’s accounting records:

CUSTOM TRUCK BUILDERS

AND INTERSTATE VAN LINES

a capital lease. Lease calls for 36 monthly

payments of $1,400 each, which included a 1%

Financed sale of truck to Interstate Van Lines using

35 Minutes, Strong

2018

(2)

Nov 30 422

978

(3)

Dec 31 412

988

Cash 1,400

(4)

31 600

Accumulated Depreciation: Leased Equip.

To record two months’ depreciation on leased

Depreciation Expense: Leased Equipment

equipment [($42,150 – $6,150) x 2/120 = $600

c.

42,150$

600

41,550$

d.

42,150$

40,184$

principal:

December payment

November payment

Computation of lease payment obligation of

Van Lines at Dec. 31, 2018:

Less: Portions of monthly payments applied to

Lease payment obligation, Nov. 1, 2018

PROBLEM B.6

CUSTOM TRUCK BUILDERS AND

INTERSTATE VAN LINES (CONCLUDED)

General Journal

Computation of net carrying value of leased

by Interstate Van Lines at Dec. 31, 2018:

Leased equipment

Less: Accumulated depreciation: leased equipment

Net carrying value, Dec. 31, 2018

Interest Expense

lease payment obligation ($42,150 x 1% = $422)

Lease Payment Obligation

To record second monthly payment to

Custom Truck Builders and to recognize one

Interest Expense

Lease Payment Obligation

month’s interest charge on unpaid balance of

lease payment obligation ($42,150 – $978) x 1% =

$412.

Cash 1,400

month’s interest charge on unpaid balance of

To record first monthly payment to

Custom Truck Builders and to recognize one

25 Minutes, Strong

a.

b.

Dec. 31 139,920

150,000

640,080

640,080

exchange for a $150,000 cash and a five-year, 4%

note receivable with a present value of $640,080

To record sale of land to Skyline Developers in

when discounted at a realistic interest rate (12%).

c. Effects of the accountant’s error upon net income:

PROBLEM B.7

Present value of Skyline note:

RICHLAND FARMS

Loss on Sale of Land (1)

Cash

Notes Receivable

At the date this note is received, its present value is only $640,080; $259,920 of the face

amount of the note represents interest revenue applicable to future periods. By recording

Present value of $900,000 due in five years,

discounted at 12%: $900,000 x .567 (from Table

*$900,000 x 4% = $36,000

years, discounted at 12%: $36,000 x 3.605 (from

Table PV-2).

Present value of note

Present value of $36,000* received annually for five

PV-1 )