APPENDIX B

PROCESS COST SYSTEMS

EXERCISES

E–1

a. Work in Process—Blending Department Increase

Materials—Cocoa Beans Decrease

Materials—Sugar Decrease

Materials—Dehydrated Milk Decrease

E–2

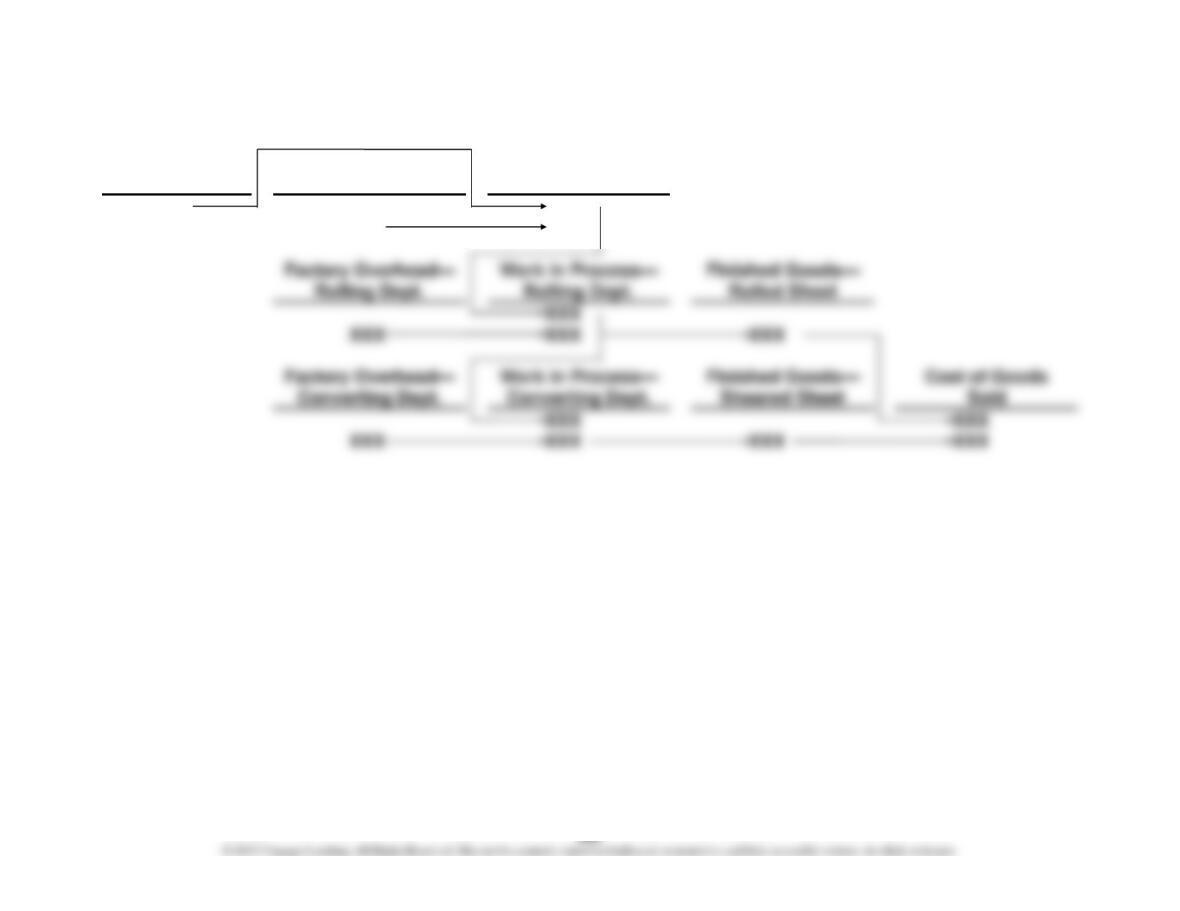

Materials

Factory Overhead—

Smelting Dept.

Work in Process—

Smelting Dept.

XXX

XXX

XXX

XXX

Rolling Dept.

Rolled Sheet

XXX

XXX

XXX

XXX

Sheared Sheet

XXX

XXX

XXX

XXX

XXX

XXX

E–3

a. and b.

A

B

C

1

a. Units

b. Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

3,500

4

Units started during period

24,900

5

Total

28,400

6

Units to be assigned costs:

7

Transferred to Packing Department

8

Inventory in process, ending (30% completed)

9

Total

*30% × 3,200

E–4

a. Drawing Department

A

B

C

1

Units

Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

3,000

4

Units started during period

91,000

5

Total

94,000

6

Units to be assigned costs:

7

Transferred to Winding Department in May

90,000

9

Total

94,000

*55% × 4,000

b. Winding Department

A

B

C

1

Units

Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

2,000

4

Units started during the period

90,000

5

Total

92,000

6

Units to be assigned costs:

7

Transferred to Finished Goods in May

89,200

9

Total

92,000

*25% × 2,800

E–5

a. Units in process, July 1 ……………………………………… 20,000

Units placed into production for July ………………….. 144,000

b.

A

B

C

1

Units

Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

20,000

4

Units started during the period

144,000

5

Total

164,000

6

Units to be assigned costs:

7

Transferred to Finished Goods in July

8

Inventory in process, July 31 (60% completed)

9

Total

164,000

*60% × 21,500

E–6

a. and b.

A

B

C

1

a. Units

b. Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

10,000

4

Units started during the period

82,300

5

Total

6

Units to be assigned costs:

7

Transferred to Finished Goods

81,300

8

Inventory in process, ending (30% completed)

11,000

9

Total units

*30% × 11,000

c. Cost per Equivalent Unit =

Units Equivalent Total

Costs Production Total

Cost per Equivalent Unit =

units 84,600

*$346,860

= $4.10

E–7

a.

A

B

C

1

Units

Equivalent Units

of Production

2

Units to be accounted for:

3

Beginning work in process

2,000

4

Units started during the period

46,200

5

Total

48,200

6

Units to be assigned costs:

7

Transferred to Finished Goods in April

45,900

8

Inventory in process, April 30 (70% completed)

9

Total units

48,200

*70% × 2,300

Cost per Equivalent Unit =

Units Equivalent Total

Costs Production Total

Cost per Equivalent Unit =

units 47,510

*$546,365

= $11.50

*$9,120 + $324,800 + $137,045 + $75,400

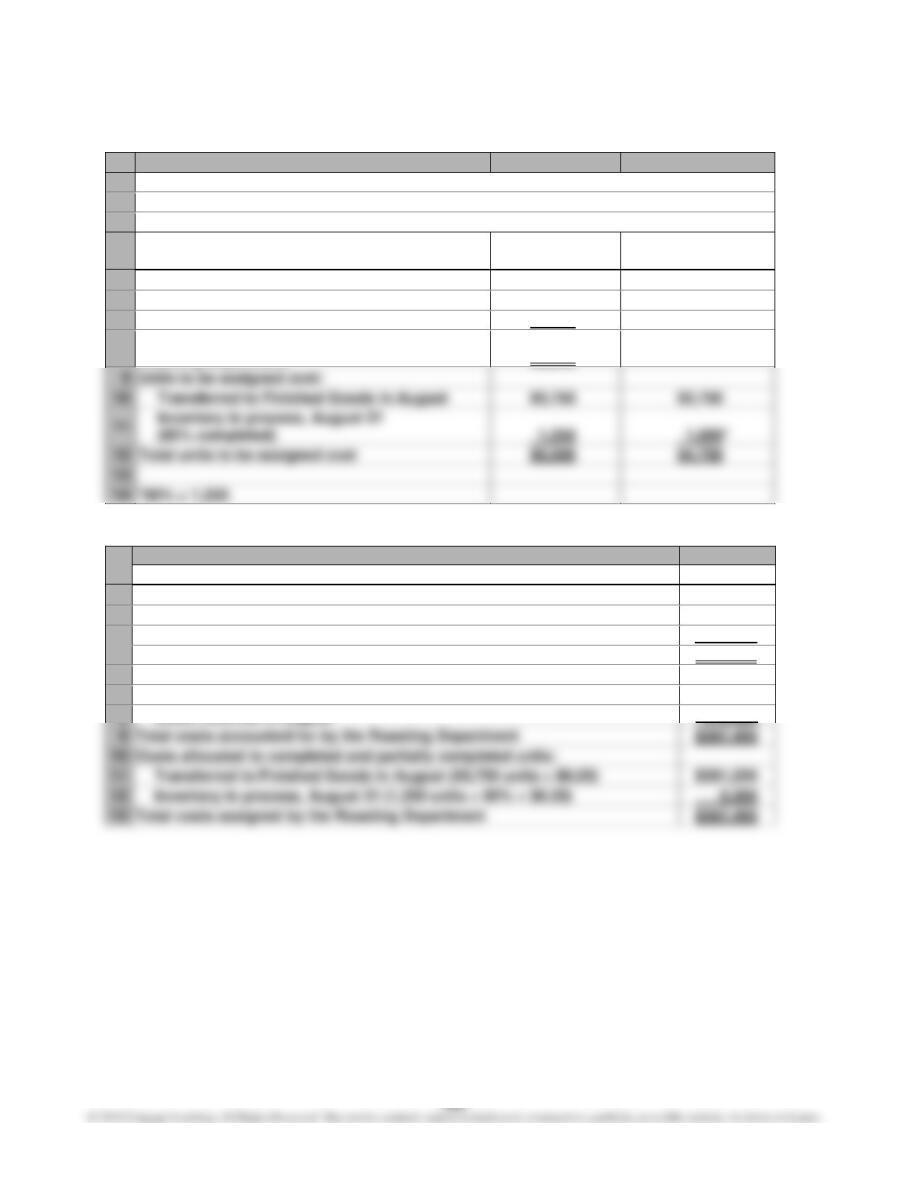

E–8

A

B

C

1

COLONEL DIRKS COFFEE COMPANY

2

Cost of Production Report—Roasting Department

3

For the Month Ended August 31

4

Units

Units

Equivalent Units

of Production

5

Units charged to production:

6

Inventory in process, August 1

2,000

7

Received from materials storeroom

93,000

8

Total units accounted for by the

Roasting Department

95,000

9

Units to be assigned cost:

Transferred to Finished Goods in August

93,750

Inventory in process, August 31

Total units to be assigned cost

95,000

*80% × 1,250

A

B

1

Costs

2

Unit costs:

3

Total costs for August in Roasting Department

$ 587,450

4

Total equivalent units

÷ 94,750

5

Cost per equivalent unit

$ 6.20

6

Costs assigned to production:

7

Inventory in process, August 1

$ 8,130

8

Costs incurred in August

579,320

9

Total costs accounted for by the Roasting Department

$ 587,450

Costs allocated to completed and partially completed units:

Transferred to Finished Goods in August (93,750 units × $6.20)

$ 581,250

Inventory in process, August 31 (1,250 units × 80% × $6.20)

6,200

Total costs assigned by the Roasting Department

$ 587,450

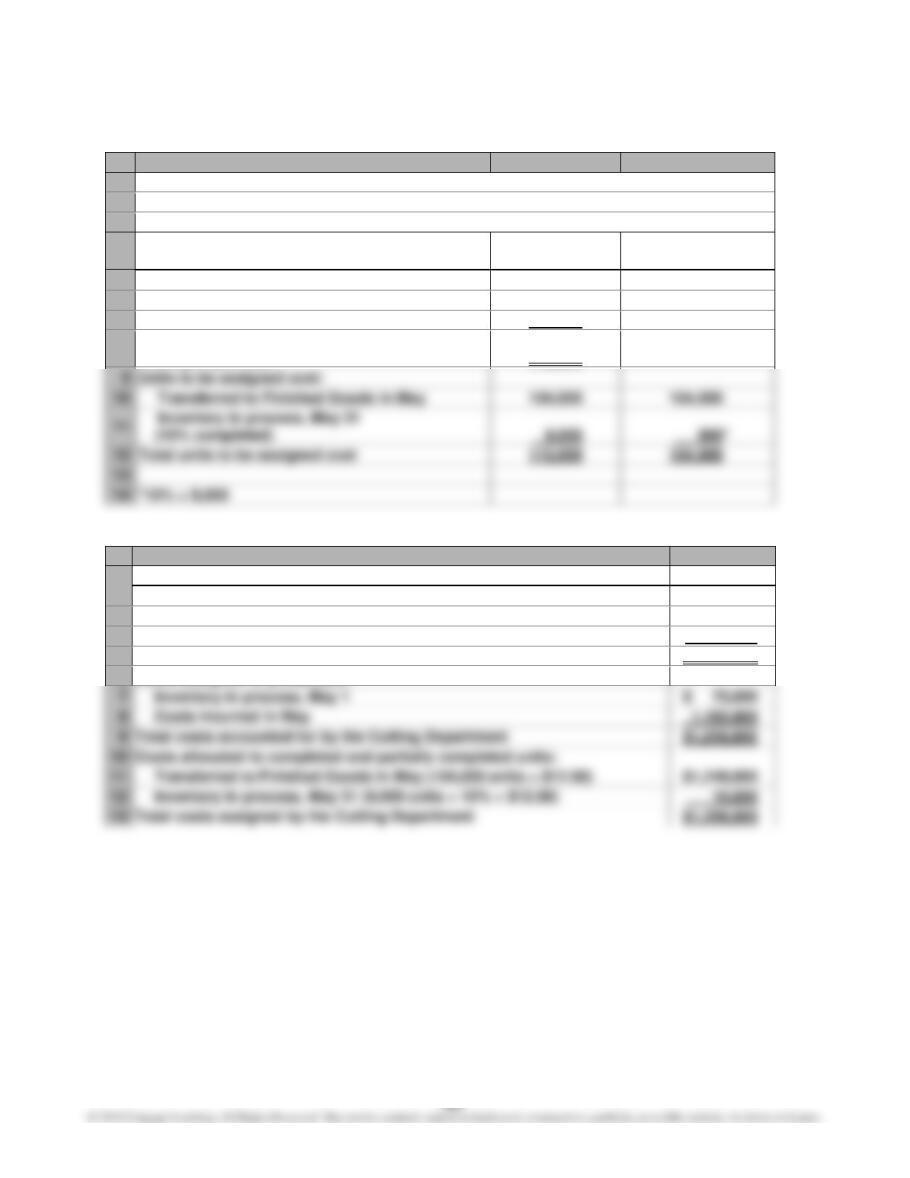

E–9

A

B

C

1

ORIENTAL CARPET COMPANY

2

Cost of Production Report—Cutting Department

3

For the Month Ended May 31

4

Units

Units

Equivalent Units

of Production

5

Units charged to production:

6

Inventory in process, May 1

8,000

7

Received from Weaving Department

105,000

8

Total units accounted for by the

Cutting Department

113,000

9

Units to be assigned cost:

Transferred to Finished Goods in May

104,000

Inventory in process, May 31

Total units to be assigned cost

113,000

*10% × 9,000

A

B

1

Costs

2

Unit costs:

3

Total costs for May in Cutting Department

$1,258,800

4

Total equivalent units

÷ 104,900

5

Cost per equivalent unit

$ 12.00

6

Costs assigned to production:

7

Inventory in process, May 1

$ 75,000

8

Costs incurred in May

1,183,800

9

Total costs accounted for by the Cutting Department

$1,258,800

Costs allocated to completed and partially completed units:

Transferred to Finished Goods in May (104,000 units × $12.00)

$ 1,248,000

Inventory in process, May 31 (9,000 units × 10% × $12.00)

10,800

Total costs assigned by the Cutting Department

$ 1,258,800

E–10

Memo

To: Production Manager

The cost of production report was used to identify the cost per case for each of

the four flavors as shown below.

A

B

C

D

E

1

Grape

Cola

Orange

Root Beer

2

Total cost

$26,075

$17,700

3

Number of cases

÷ 3,500

4

Cost per case

$ 7.45

As can be seen, the cost per case of Root Beer is significantly above the cost per

case of the other three flavors. A more detailed analysis is necessary to under-

stand the causes of this difference. The individual cost elements that determine

the total cost can be divided by the number of cases. This analysis is provided

below.

A

B

C

D

E

1

Cost per Case by Cost Element

2

Grape

Cola

Orange

Root Beer

3

Concentrate

$1.90

$2.25

$2.20

$1.80

4

Water

0.60

0.60

0.60

0.60

5

Sugar

1.00

1.00

1.00

1.00

6

Bottles

2.20

2.20

2.20

7

Flavor changeover

1.00

0.10

2.50

8

Conversion cost

The table above indicates that the concentrate per case is actually less for

Grape and Root Beer than for Cola and Orange. This is because the concentrate

supplier charges a higher price for the more popular flavors. The costs per case

for water, sugar, and bottles are the same for each flavor. However, the costs per

case for changeover are much greater for Grape and Root Beer than for the other

two flavors. In addition, the conversion costs per unit for Grape and Root Beer

are $0.35 higher than for Cola and Orange. These last two cost elements are suf-

ficient to cause the cost per case of Grape and Root Beer to be greater than Cola

and Orange.

E–11

The solution to this exercise is to determine if cost per pound trends in paper

stock, conversion, and coating costs are remaining stable over time. The follow-

ing table can be developed from the data:

a.

A

B

C

D

E

F

G

1

April

May

June

July

August

Sept.

2

$0.80

$0.80

$0.80

$0.80

$0.18

$0.22

$0.25

$0.26

$0.40

$0.40

$0.40

$0.40

Paper stock

The cost per pound information is determined by dividing the costs by the

pounds transferred out. The yield is determined by dividing the pounds trans–

ferred out by the pounds input.

b. Operator 1 believes that energy consumption is becoming less efficient. The

energy cost is part of the conversion cost. The conversion cost per output

pound has remained constant for the six months. If the energy efficiency were

declining, it would take more energy per pound of output over time. Thus, we

would expect to see the conversion rate per pound increasing if Operator 1

were correct.

PROBLEMS

P–1

A

B

C

1

JOSHUA FLOUR COMPANY

2

Cost of Production Report—Sifting Department

3

For the Month Ended March 31

4

Units

Units

Equivalent Units

of Production

5

Units charged to production:

6

Inventory in process, March 1

3,200

7

Received from Milling Department

14,500

8

Total units accounted for by the

Sifting Department

17,700

9

Units to be assigned cost:

Transferred to Packaging Department in

Inventory in process, March 31

Total units to be assigned cost

17,700

A

B

1

Costs

2

Unit costs:

3

Total costs for March in Sifting Department

$73,350*

4

Total equivalent units

÷16,300

5

Cost per equivalent unit

$ 4.50

6

Costs charged to production:

7

Inventory in process, March 1

$ 3,500

8

Costs incurred in March

69,850**

9

Total costs accounted for by the Sifting Department

$73,350

Costs allocated to completed and partially completed units:

Transferred to Packaging Department in March (14,900 units × $4.50)

$67,050

Inventory in process, March 31 (2,800 × 50% × $4.50)

6,300

Total costs assigned by the Sifting Department

$73,350

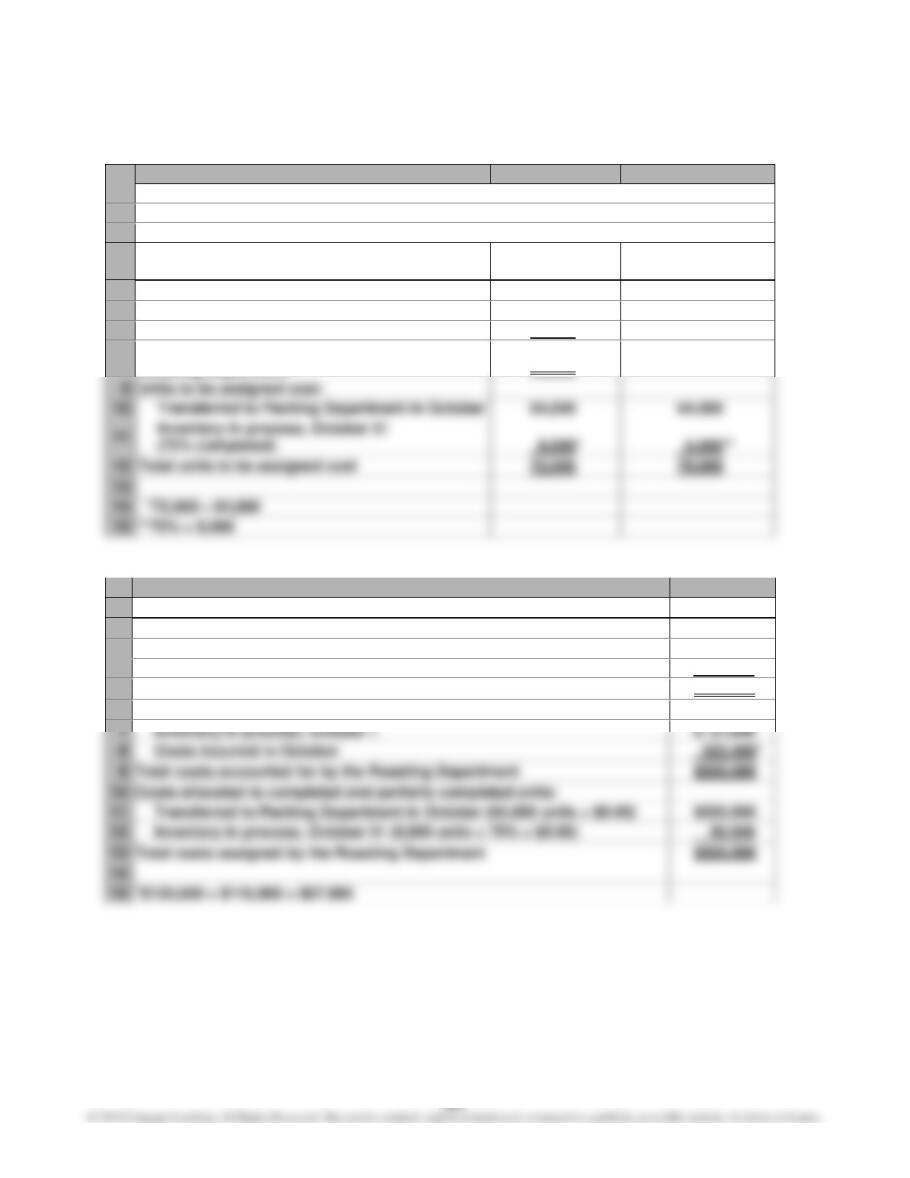

P–2

A

B

C

1

SERGEANT WILKES COFFEE COMPANY

2

Cost of Production Report—Roasting Department

3

For the Month Ended October 31

4

Units

Units

Equivalent Units

of Production

5

Units charged to production:

6

Inventory in process, October 1

7,500

7

Received from materials storeroom

64,500

8

Total units accounted for by the

Roasting Department

72,000

9

Units to be assigned cost:

Transferred to Packing Department in October

64,000

Inventory in process, October 31

Total units to be assigned cost

A

B

1

Costs

2

Unit costs:

3

Total costs for October in Roasting Department

$350,000

4

Total equivalent units

÷ 70,000

5

Cost per equivalent unit

$ 5.00

6

Costs charged to production:

7

Inventory in process, October 1

$ 27,600

8

Costs incurred in October

9

Total costs accounted for by the Roasting Department

Costs allocated to completed and partially completed units:

Transferred to Packing Department in October (64,000 units × $5.00)

$320,000

Inventory in process, October 31 (8,000 units × 75% × $5.00)

30,000

Total costs assigned by the Roasting Department

*$135,600 + $118,900 + $67,900