APPENDIX A

Time Value of Money

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE A-1

(a) Interest = p X i X n

I = $6,000 X .05 X 12 years

(b) Future value factor for 12 periods at 5% is 1.79586 (from Table 1)

BRIEF EXERCISE A-2

(1) Case A 5% 3 periods (2) Case A 3% 8 periods

BRIEF EXERCISE A-3

FV = p X FV of 1 factor

BRIEF EXERCISE A-4

FV of an annuity of 1 = p X FV of an annuity factor

BRIEF EXERCISE A-5

FV = p X FV of 1 factor + (p X FV of an annuity factor)

BRIEF EXERCISE A-6

FV = p X FV of 1 factor

BRIEF EXERCISE A-7

(a) (b)

(1) 12% 7 periods

(2) 10% 20 periods

BRIEF EXERCISE A-8

(a) i = 10%

?

$25,000

0 1 2 3 4 5 6 7 8 9

Discount rate from Table 3 is .42410 (9 periods at 10%). Present value

BRIEF EXERCISE A-8 (Continued)

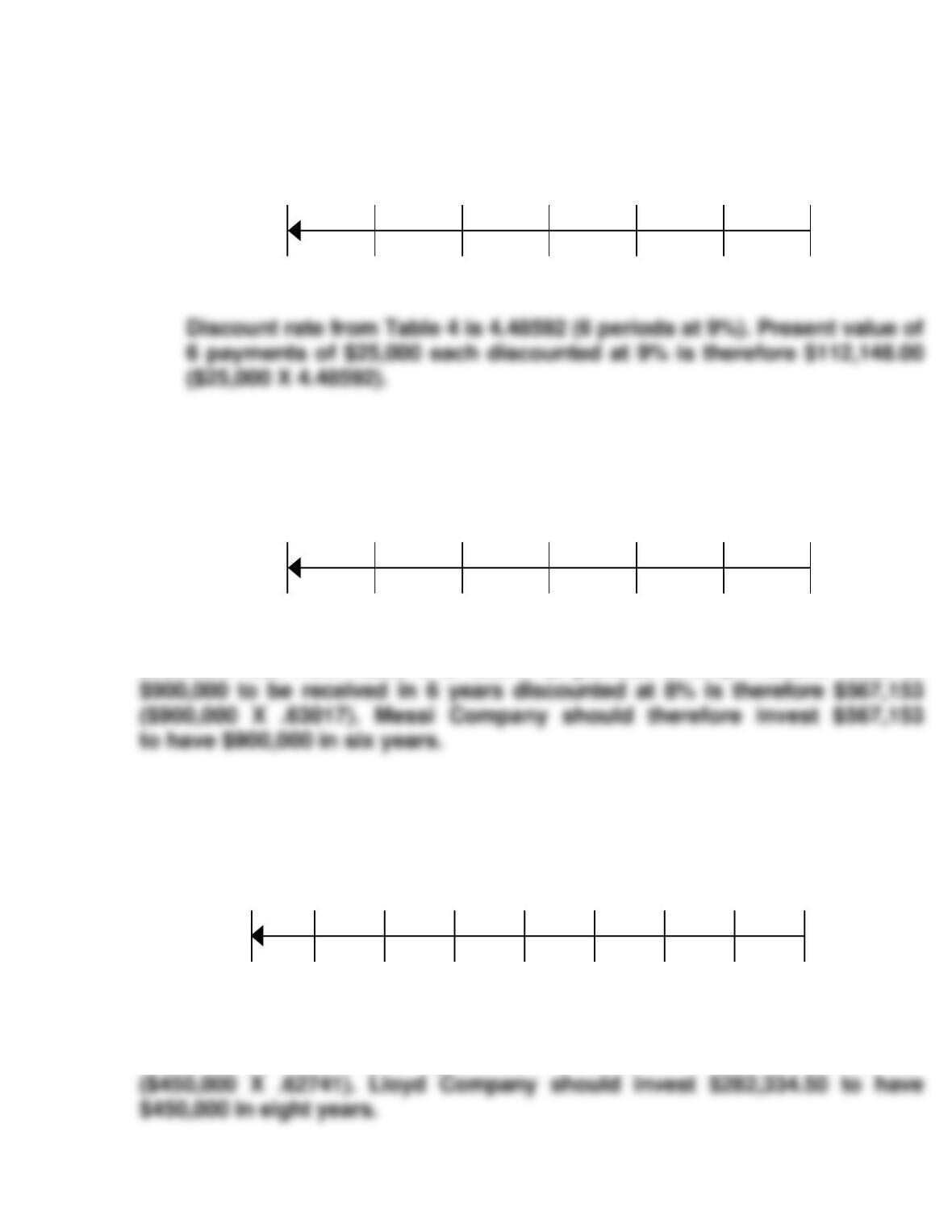

(b) i = 9%

? $25,000 $25,000 $25,000 $25,000 $25,000 $25,000

0 1 2 3 4 5 6

BRIEF EXERCISE A-9

i = 8%

? $900,000

0 1 2 3 4 5 6

Discount rate from Table 3 is .63017 (6 periods at 8%). Present value of

BRIEF EXERCISE A-10

i = 6%

?

$450,000

0 1 2 3 4 5 6 7 8

Discount rate from Table 3 is .62741 (8 periods at 6%). Present value of

$450,000 to be received in 8 years discounted at 6% is therefore $282,334.50

BRIEF EXERCISE A-11

i = 8%

? $40,000 $40,000 $40,000 $40,000 $40,000 $40,000

0 1 2 3 4 14 15

BRIEF EXERCISE A-12

i = 5%

? $80,000 $80,000 $80,000 $80,000 $80,000 $80,000

0 1 2 3 4 5 6

Discount rate from Table 4 is 5.07569. Present value of 6 payments of $80,000

BRIEF EXERCISE A-13

i = 5%

? $400,000

Diagram

for

Principal

0 1 2 3 4 19 20

i = 5%

Present value of principal to be received at maturity:

$400,000 X 0.37689 (PV of $1 due in 20 periods

at 5% from Table 3) …………………………………………………….. $150,756*

Present value of interest to be received periodically

BRIEF EXERCISE A-14

The bonds will sell at a discount (for less than $400,000). This may be proven

as follows:

Present value of principal to be received at maturity:

$400,000 X .31180 (PV of $1 due in 20 periods

at 6% from Table 3) …………………………………………………….. $124,720*

Present value of interest to be received periodically

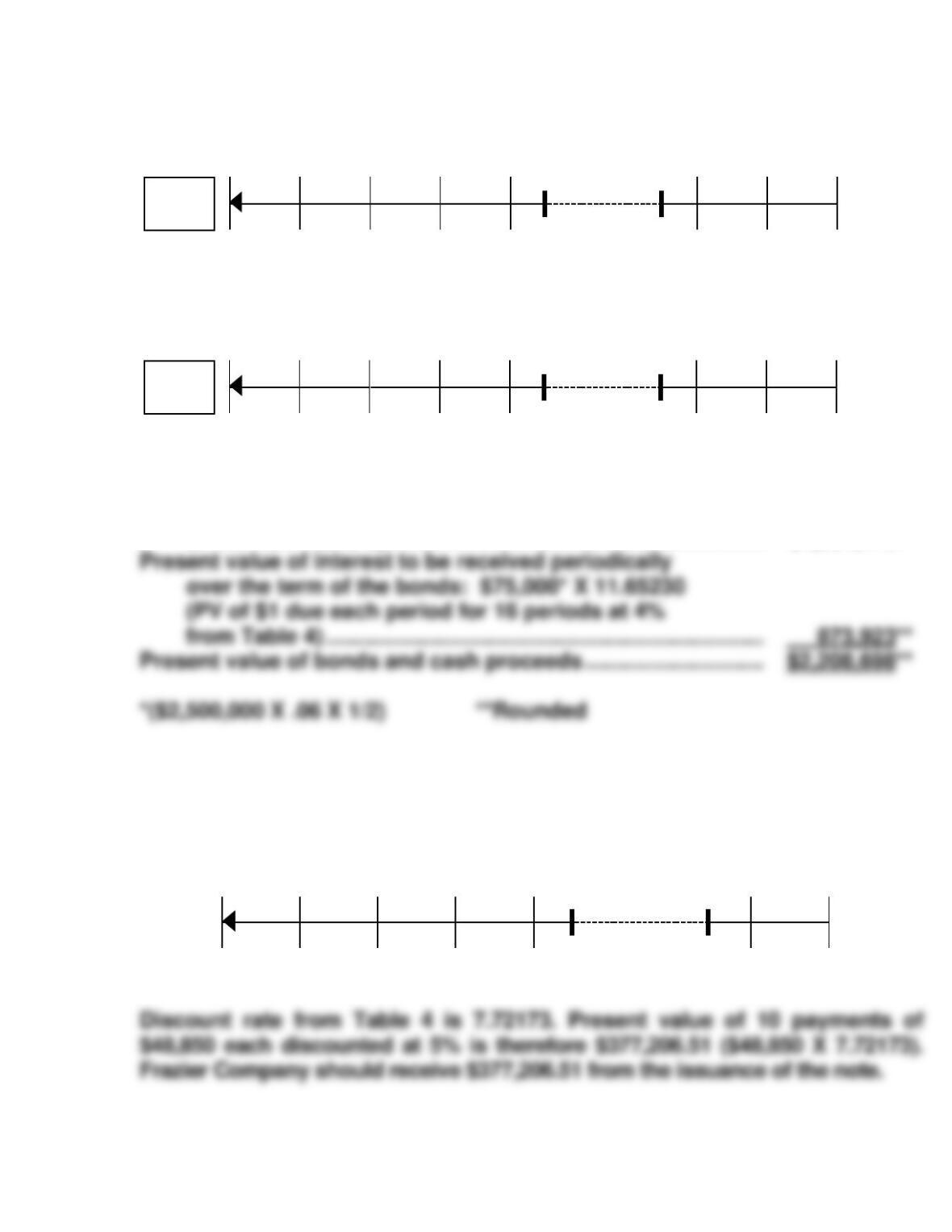

BRIEF EXERCISE A-15

i = 6%

? $75,000

Diagram

for

Principal

0 1 2 3 4 5 6

Present value of principal to be received at maturity:

$75,000 X .70496 (PV of $1 due in 6 periods

at 6% from Table 3) ……………………………………………………. $52,872.00

Present value of interest to be received annually

over the term of the note: $3,000* X 4.91732

BRIEF EXERCISE A-16

i = 4%

? $2,500,000

Diagram

for

Principal

0 1 2 3 4 14 15 16

i = 4%

? $75,000 $75,000 $75,000 $75,000 $75,000 $75,000 $75,000

Diagram

for

Interest

0 1 2 3 4 14 15 16

Present value of principal to be received at maturity:

$2,500,000 X 0.53391 (PV of $1 due in 16 periods

at 4% from Table 3) ……………………………………………………. $1,334,775

BRIEF EXERCISE A-17

i = 5%

? $48,850 $48,850 $48,850 $48,850 $48,850 $48,850

0 1 2 3 4 9 10

BRIEF EXERCISE A-18

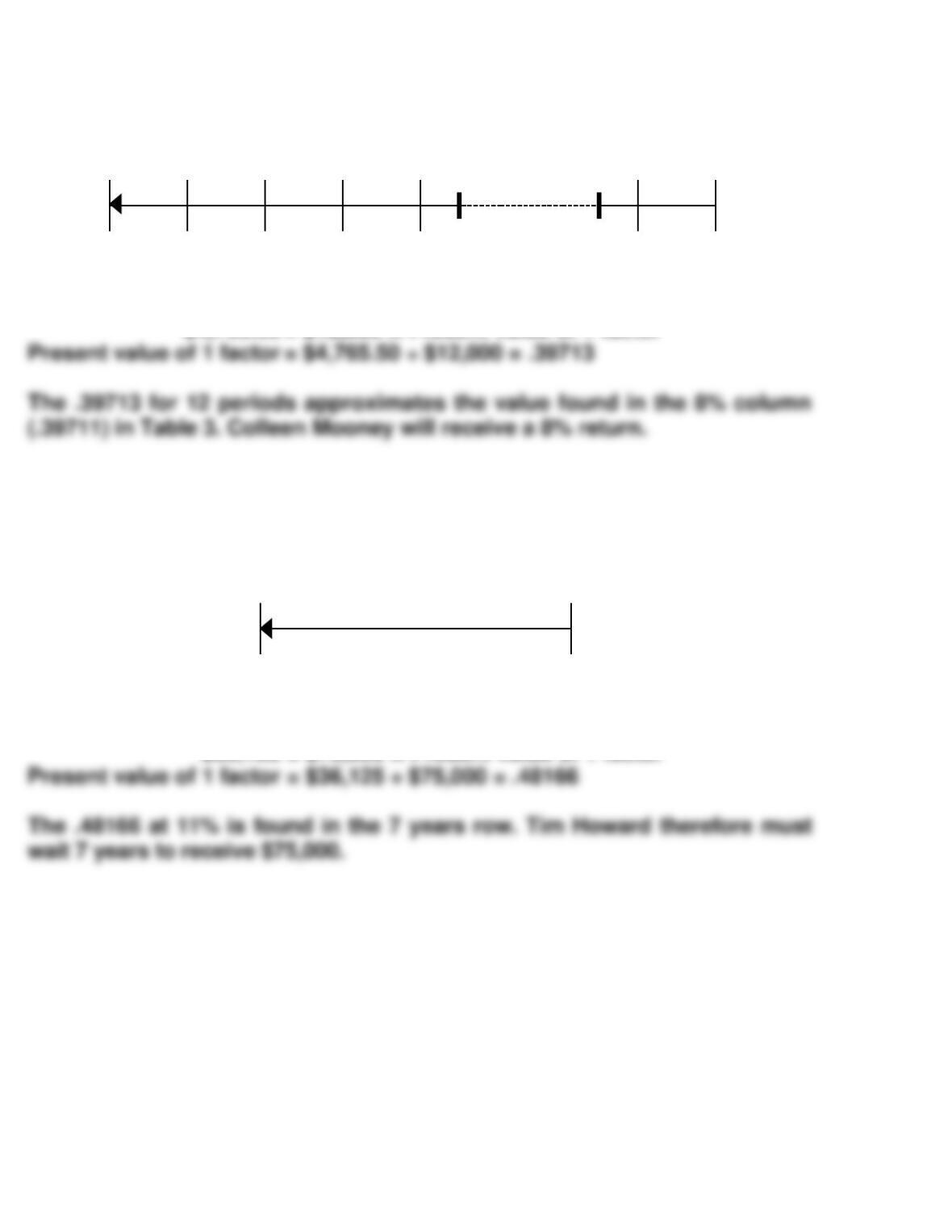

i = ?

$4,765.50 $12,000

0 1 2 3 4 11 12

Present value = Future value X Present value of 1 factor

$4,765.50 = $12,000 X Present value of 1 factor

BRIEF EXERCISE A-19

i = 11%

$36,125 $75,000

n = ?

Present value = Future value X Present value of 1 factor

$36,125 = $75,000 X Present value of 1 factor

BRIEF EXERCISE A-20

i = ?

? $1,200 $1,200 $1,200 $1,200 $1,200 $1,200 $1,200 $1,200

0 1 2 3 4 5 6 14 15

$10,271.38

The 8.55948 for 15 periods is found in the 8% column in Table 4. Joanne

Quick will therefore earn a rate of return of 8%.

BRIEF EXERCISE A-21

i = 9%

$1,300 $1,300 $1,300 $1,300 $1,300 $1,300

$7,793.83 n = ?

Present value = Future amount X Present value of an annuity factor

BRIEF EXERCISE A-22

i = 9%

?

$2,700

$2,700

$2,700

$2,700

$2,700

$2,700

$2,700

0

1

2

3

4

5

6

7

Discount rate from Table 4 is 5.03295. Present value of 7 payments of

$2,700 each discounted at 9% is therefore $13,588.97 ($2,700 X 5.03295).

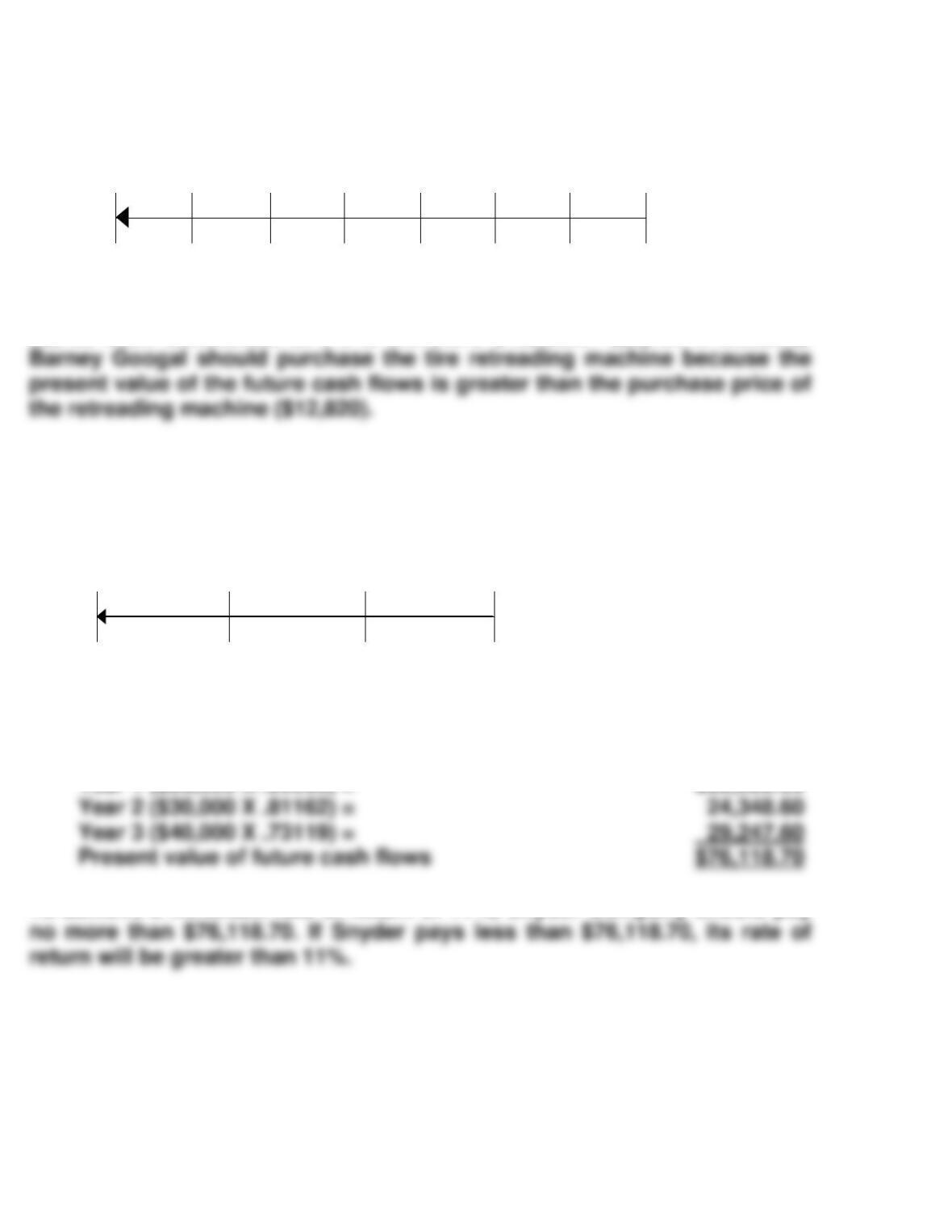

BRIEF EXERCISE A-23

i = 11%

?

$25,000

$30,000

$40,000

0

1

2

3

To determine the present value of the future cash flows, discount the future

cash flows at 11%, using Table 3.

Year 1 ($25,000 X .90090) =

$22,522.50

Year 2 ($30,000 X .81162) =

Year 3 ($40,000 X .73119) =

Present value of future cash flows

$76,118.70

To achieve a minimum rate of return of 11%, Snyder Company should pay

BRIEF EXERCISE A-24

10*

?

–18,000

0

50,000

N

I/YR.

PV

PMT

FV

BRIEF EXERCISE A-25

10

?

42,000

–6,500

0

N

I/YR.

PV

PMT

FV

BRIEF EXERCISE A-26

40

?

178,000*

–8,400

0

N

I/YR.

PV

PMT

FV

(semiannual)

10.76%

BRIEF EXERCISE A-27

(a)

Inputs:

7

7.35

?

16,000

0

N

I

PV

PMT

FV

(b)

Inputs:

10

10.65

?

16,000**

200,000*

N

I

PV

PMT

FV

Answer:

Answer:

BRIEF EXERCISE A-28

(a)

Note—set payments at 12 per year.

Inputs:

96

7.8

42,000

?

0

N

I

PV

PMT

FV

(b)

Note—set payments to 1 per year.

Inputs:

5

7.25

8,000

?

0

N

I

PV

PMT

FV

Answer:

Answer: