SPECIAL APPENDIX 2

UNDERSTANDING THE ISSUES

1. (a) No equity investment would be shown in this case. The Primary Beneficiary could own

various debt or equity securities, but it is not required in order to consolidate.

2. It is based on a contractual agreement that could include interest on intercompany debt or

management fees.

Special Appendix 2—Exercises SA2–2

EXERCISES

EXERCISES SA2-1

Determination and distribution of excess schedule:

Fair value of equity …………………………….. $600,000

Less book value of equity ……………………. (80,000)

Excess of fair value over book value …….. 520,000

EXERCISES SA2-2

Income Distribution Schedule:

VIE Company Income Distribution

(A1) Depreciation adjustment …….. $20,000 Internally generated net

income ……………………………. $70,000

Adjusted income ……………………. $50,000

SA2–3 Special Appendix 2—Problems

PROBLEMS

PROBLEM SA2-1

Determination and distribution of excess schedule:

Fair value of equity …………………………….. $170,000

Less book value of equity ……………………. (80,000)

Excess of fair value over book value …….. 90,000

Special Appendix 2—Problems SA2–4

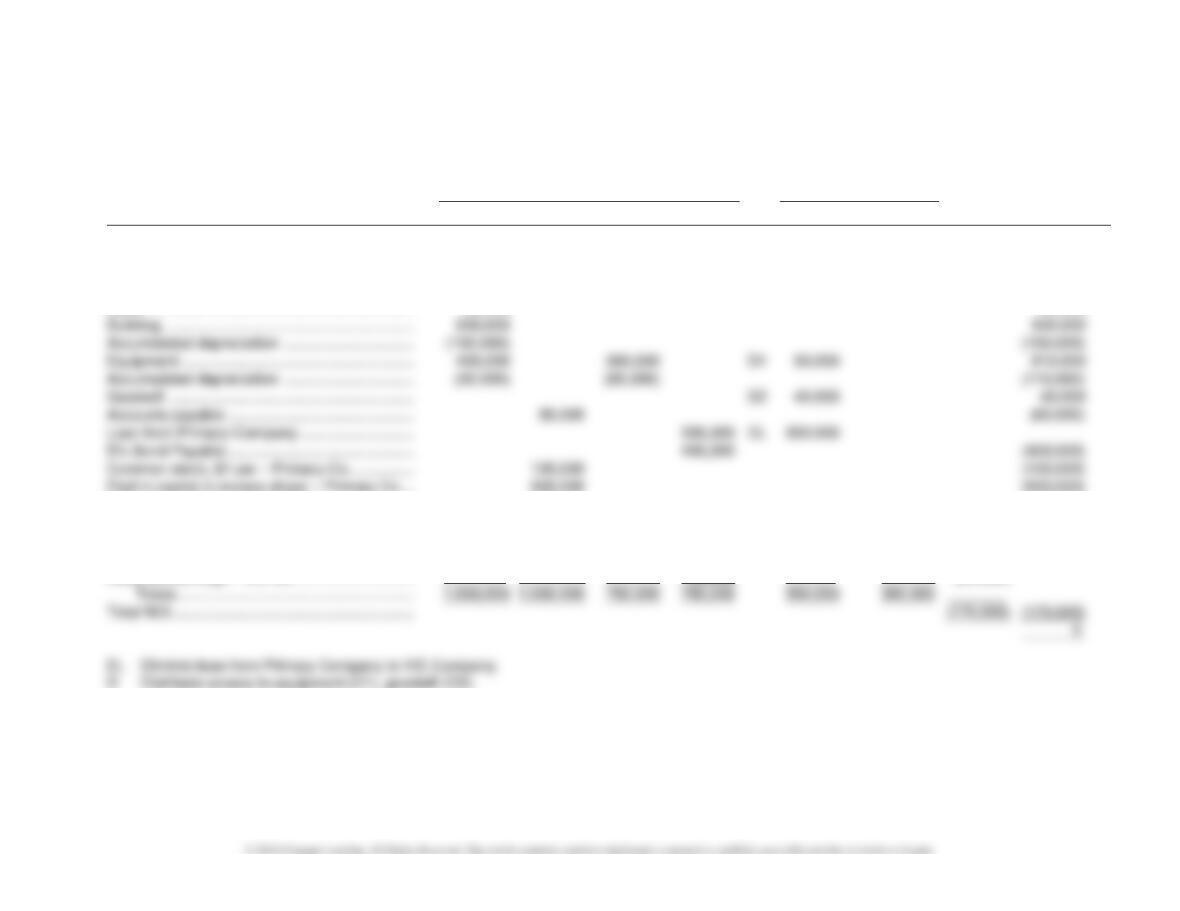

Primary Company and VIE Company

Consolidated Balance Sheet

December 31, 2015

Balance Sheets, Dec. 31, 2015 Eliminations Consolidated

Balance

Sheet Primary Company VIE Company Dr Cr NCI

Cash ………………………………………………….. 200,000 80,000 280,000

Accounts receivable ……………………………….. 400,000 400,000

Inventory ……………………………………………… 400,000 400,000

Loan receivable from VIE Co. …………………… 300,000 EL 300,000

Land …………………………………………………… 50,000 50,000

Retained earnings – Primary Co. ……………….. 570,000 (570,000)

Common stock, $1 par – VIE Co. ………………. 10,000 (10,000)

Paid in capital in excess of par – VIE Co.…….. 50,000 (50,000)

Paid-in Capital on Revaluation – VIE Co. …….. D 90,000 (90,000)

Retained earnings – VIE Co. …………………….. 20,000 (20,000)

SA2–5 Special Appendix 2—Problems

PROBLEM SA2-2

Determination and distribution of excess schedule:

Fair value of equity …………………………….. $170,000

Less book value of equity ……………………. (80,000)

Excess of fair value over book value …….. 90,000

Special Appendix 2—Problems SA2–6

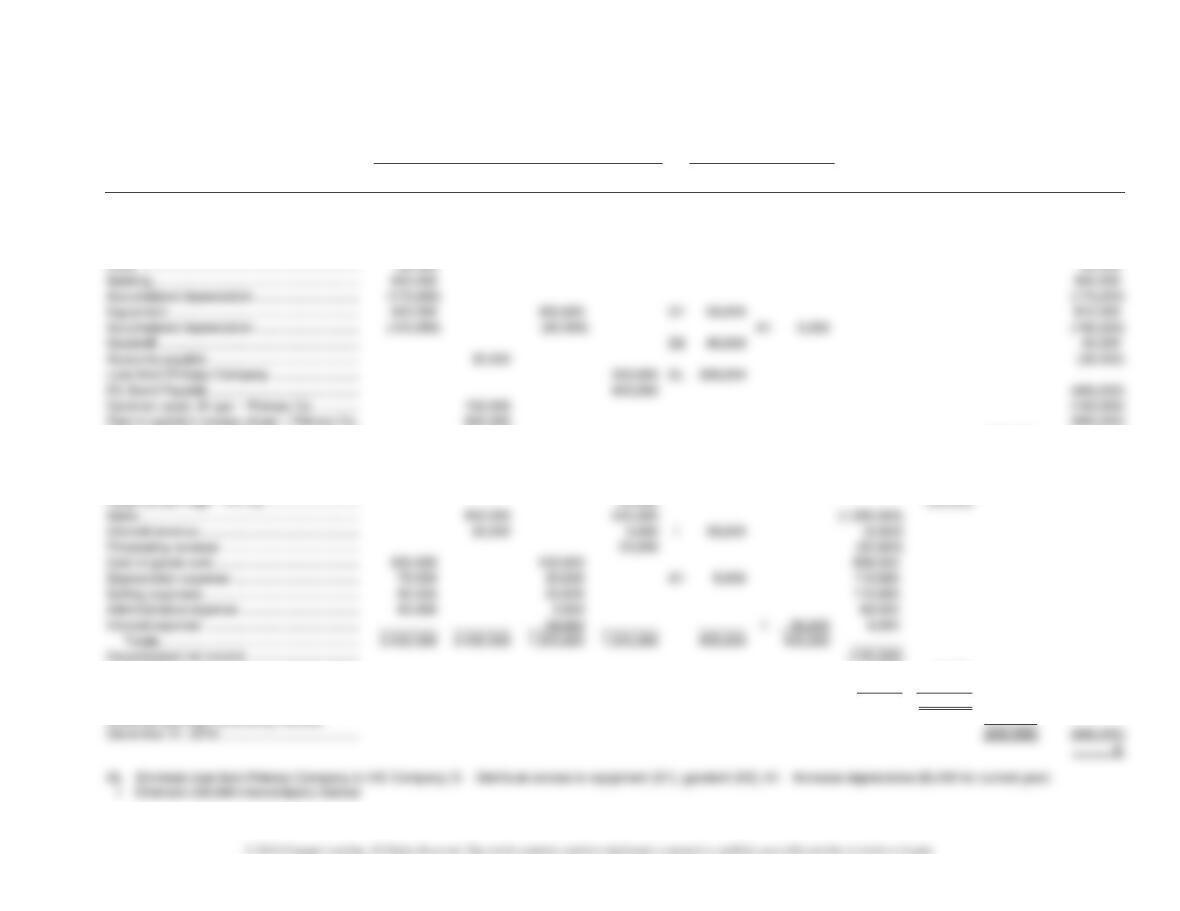

Primary Company and VIE Company

Consolidated Trial Balance

December 31, 2016

Trial Balances, Dec. 31, 2016 Eliminations Income

Statement NCI

Controlling

Retained

Earnings

Consolidated

Balance

Sheet Primary Company VIE Company Dr Cr

Cash ………………………………………… 305,000 110,000 415,000

Accounts receivable ………………………… 425,000 425,000

Inventory …………………………………….. 425,000 425,000

Loan receivable from VIE Co. ……………… 300,000 EL 300,000

Retained earnings – Primary Co. …………… 570,000 (570,000)

Common stock, $1 par – VIE Co. ………….. 10,000 (10,000)

Paid in capital in excess of par – VIE Co. ….. 50,000 (50,000)

Paid-in capital on revaluation – VIE Co. ……. D 90,000 (90,000)

To NCI …………………………………… 9,000 (9,000)

To controlling interest ……………………. 116,000 (116,000)

NCI ………………………………………….. (179,000) (179,000)

Retained earnings, controlling interest,

SA2–7 Special Appendix 2—Problems

Income Distribution Schedule:

VIE Company Income Distribution

(A1) Depreciation adjustment …….. $5,000 Internally generated net

income ……………………………. $25,000

Adjusted income ……………………. $20,000