7-1

CHAPTER 7

FINANCING ACTIVITIES

Solutions to Questions, Exercises, Problems, and Teaching Notes to Cases

7.1 Common Equity Transactions.

Item

Common

Stock

Additional

Paid-in

Capital

Deferred

Compensation

Retained

Earnings

Treasury

Stock at

Cost

Total

Common

Shareholders’

Equity

(1) The direct effect of the property dividend is to reduce retained earnings by the fair

Chapter 7

Financing Activities

7-2

7.2 Common Equity Issue.

a.

CC AOCI RE

1

Cash +1,000,000 Common Stock +100,000

APIC +900,000

Journal Entry

CC AOCI RE

2

Land +150,000 Common Stock +10,000

APIC +140,000

Journal Entry

2. Land ………………………………………………………………………… 150,000

b. In each transaction, the company uses the attribute “fair value” as the measure-

ment basis for the transaction. The net increase in shareholders’ equity always

7.3 Dividends.

a.

Shareholders’ Equity

+LiabilitiesAssets =

Investments …………………………………………………………… 10,000

Chapter 7

Financing Activities

7-3

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

CC AOCI RE

4

Common Stock +80,000 Retained Earnings (80,000)

5. Memorandum entry only to note that number of shares outstanding triples to

b. The book value of common equity (that is, total shareholders’ equity) decreases

only when assets are disbursed (Transactions 1 and 2). The remainder of the

Chapter 7

Financing Activities

7-4

7.4 Cash Flow Effects of Equity and Debt Financing.

a. Financing; increase in cash

b. No effect; shown in an accompanying schedule of significant investing and

financing activities

j. Financing; increase in cash from receipt of the exercise price (The tax savings

also will be reported as an increase in cash in the financing section after being

removed from the operating section.)

o. Operating; decrease in cash (Under the indirect method and U.S. GAAP, the

p. Financing; decrease in cash

Chapter 7

Financing Activities

7-5

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

q. Financing; decrease in cash (The gain on retirement would be reported as a

subtraction in the operating section because, under the indirect method, all of

net income is initially reported as an operating cash inflow and non-operating

gains and losses must be removed from the section.)

r. Financing; decrease in cash (The loss on retirement would be reported as an

addition in the operating section because, under the indirect method, all of net

income is initially reported as an operating cash inflow and non-operating gains

and losses must be removed from the section.)

7.5 Accounting for a Note Payable.

a.

12/31/17 Signing

Shareholders’ Equity

+LiabilitiesAssets =

12/31/18 Year-End Interest Payment

Shareholders’ Equity

+LiabilitiesAssets =

12/31/19 Year-End Interest Payment

Shareholders’ Equity

+LiabilitiesAssets =

Effective Interest Amortization Table

3% Cash 4% Effective Book Value

Date Interest Interest Expense Amortization of Note

Chapter 7

Financing Activities

7-6

b. (1) On the face of its December 31, 2019, balance sheet, The Cola-Cola Com–

pany reports long-term debt equal to the book value of the note using the

c. (1) If The Coca-Cola Company chooses the fair value option, it will report

long-term debt on the face of its December 31, 2019, balance sheet at fair

7.6 Accounting for Troubled Debt: Settlement.

Record Increase in Investment’s Fair Value:

CC AOCI RE

Investments +15,000 Gain +15,000

Shareholders’ Equity

+LiabilitiesAssets =

Journal Entry

Settle Debt:

Shareholders’ Equity

7-7

7.7 Accounting for Troubled Debt: Modification of Terms.

a. (1) U.S. GAAP

Undiscounted Future Cash Flows of

Restructured Debt:

exist (that is, the effective rate is set equal to zero) because the future cash

flows are now equal to the new (reduced) book value.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

Journal Entry

(2) IFRS

Under IFRS, Great Beef Co. would compare the present value of future

cash flows under the restructured debt (instead of the undiscounted or gross

cash flows as is done under U.S. GAAP) to the book value of the debt. The

present value calculation uses the historical effective interest rate of 9%:

Present Value of Future Cash Flows (Using a

Financial Calculator):

Chapter 7

Financing Activities

7-8

which the fair value of the debt is below the current book value. Computing

fair value requires the use of a current market rate of interest (15%) instead

of the historical rate of 8% to compute the present value of the restructured

debt’s cash flows.

Present Value of Future Cash Flows (Using a 15%

Current Market Rate):

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

Journal Entry

b. (1) U.S. GAAP

Gross Future Cash Flows of Restructured Debt:

Because gross future cash flows are greater than the current book value of

Chapter 7

Financing Activities

7-9

(2) IFRS

Under IFRS, Great Beef Co. would compare the present value of future

cash flows under the restructured debt to the book value of the debt using

the historical effective interest rate of 9%.

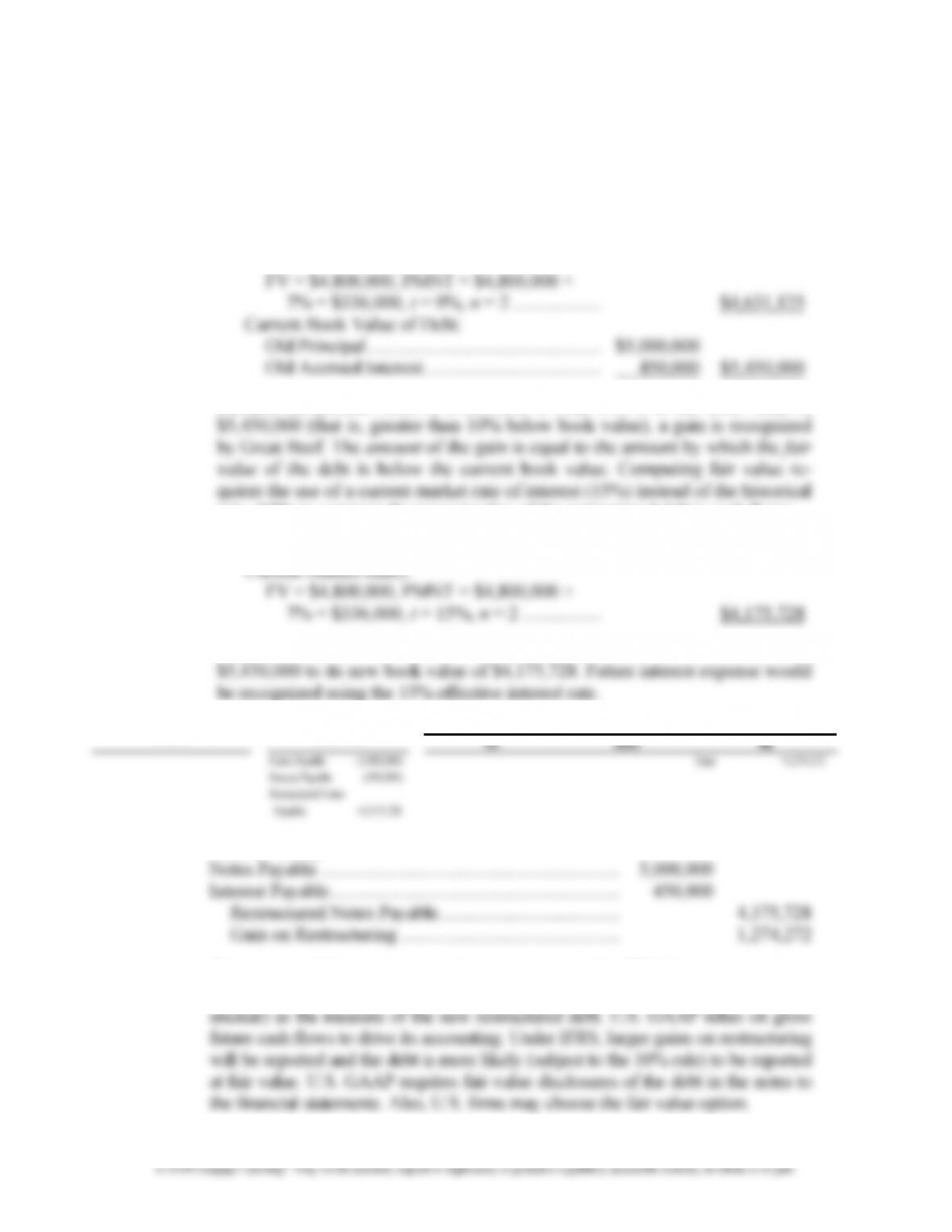

Present Value of Future Cash Flows (Using a

Financial Calculator):

Because the present value of $4,631,125 is only 84.9% of the book value of

rate of 8% to compute the present value of the restructured debt’s cash flows:

Present Value of Future Cash Flows (Using a 15%

A gain is recorded for the decrease in the liability from its book value of

Journal Entry

c. The primary difference between the two systems is that IFRS bases computations

on the more economically relevant fair value (although the need for the 10% rule is

Chapter 7

Financing Activities

7-10

7.8 Redeemable Preferred Stock.

a. If redemption will occur at a specific time or at the time at which a specific

b. If the redemption is at the option of the issuing firm (the preferred stock is

c. If redemption is at the holder’s discretion (that is, the preferred stock is

7.9 Convertible Preferred Stock.

a.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

b.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

c.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

Chapter 7

7-11

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

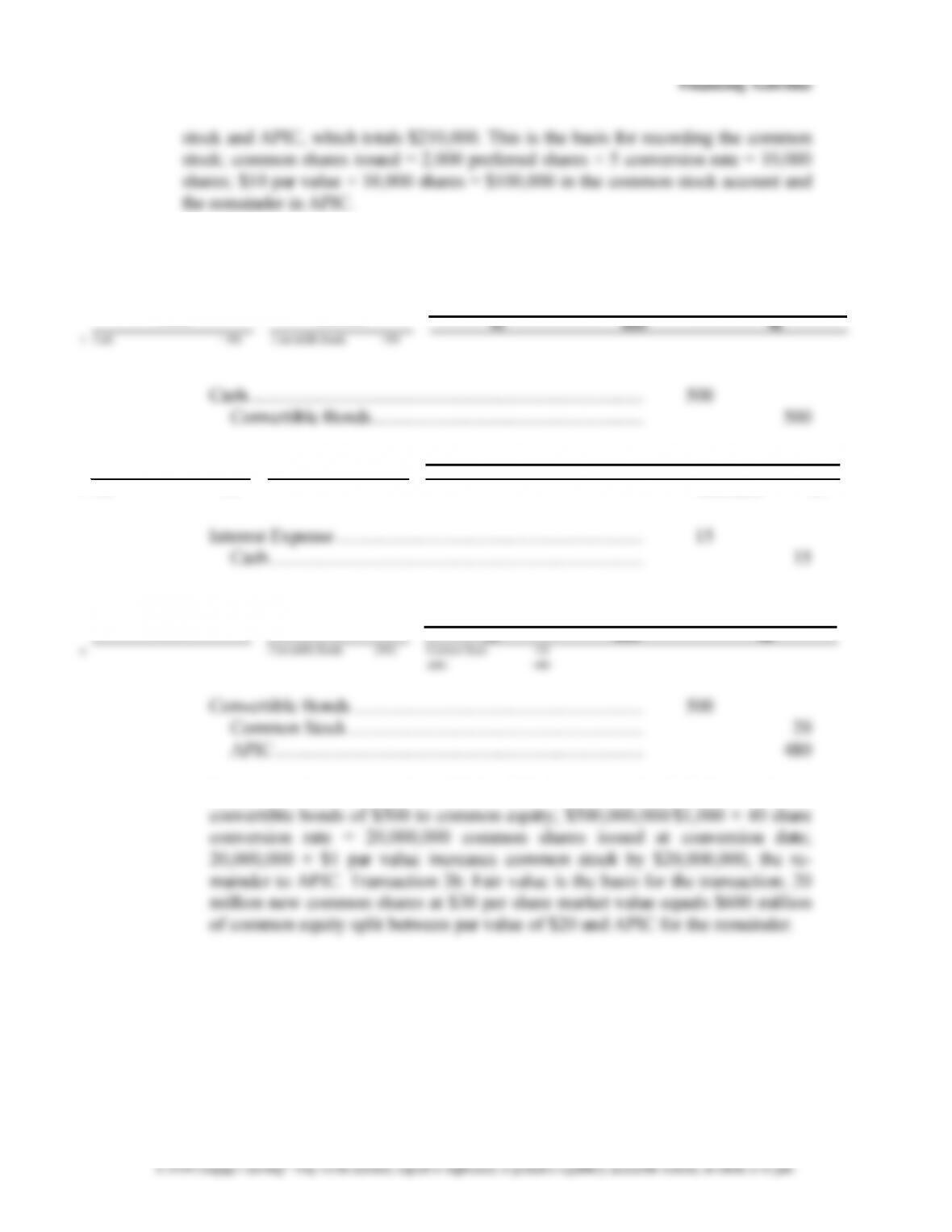

stock and APIC, which totals $210,000. This is the basis for recording the common

stock; common shares issued = 2,000 preferred shares × 5 conversion rate = 10,000

shares; $10 par value × 10,000 shares = $100,000 in the common stock account and

the remainder in APIC.

7.10 Convertible Debt under IFRS and U.S. GAAP.

a. U.S. GAAP (all amounts in millions)

Shareholders’ Equity

+LiabilitiesAssets =

CC AOCI RE

2 Cash (15) Interest Expense (15)

Shareholders’ Equity

+LiabilitiesAssets =

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

Transaction 2: Interest = 3% × $500 = $15. Transaction 3a: Shift book value of

Chapter 7

Financing Activities

7-12

b. IFRS (all amounts in millions)

Bonds +167.75

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

c.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

Under IFRS, the proceeds are allocated between the fair values of the notes and

the conversion options on the notes. If ARTL would have paid 8% interest on the

Chapter 7

7-13

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

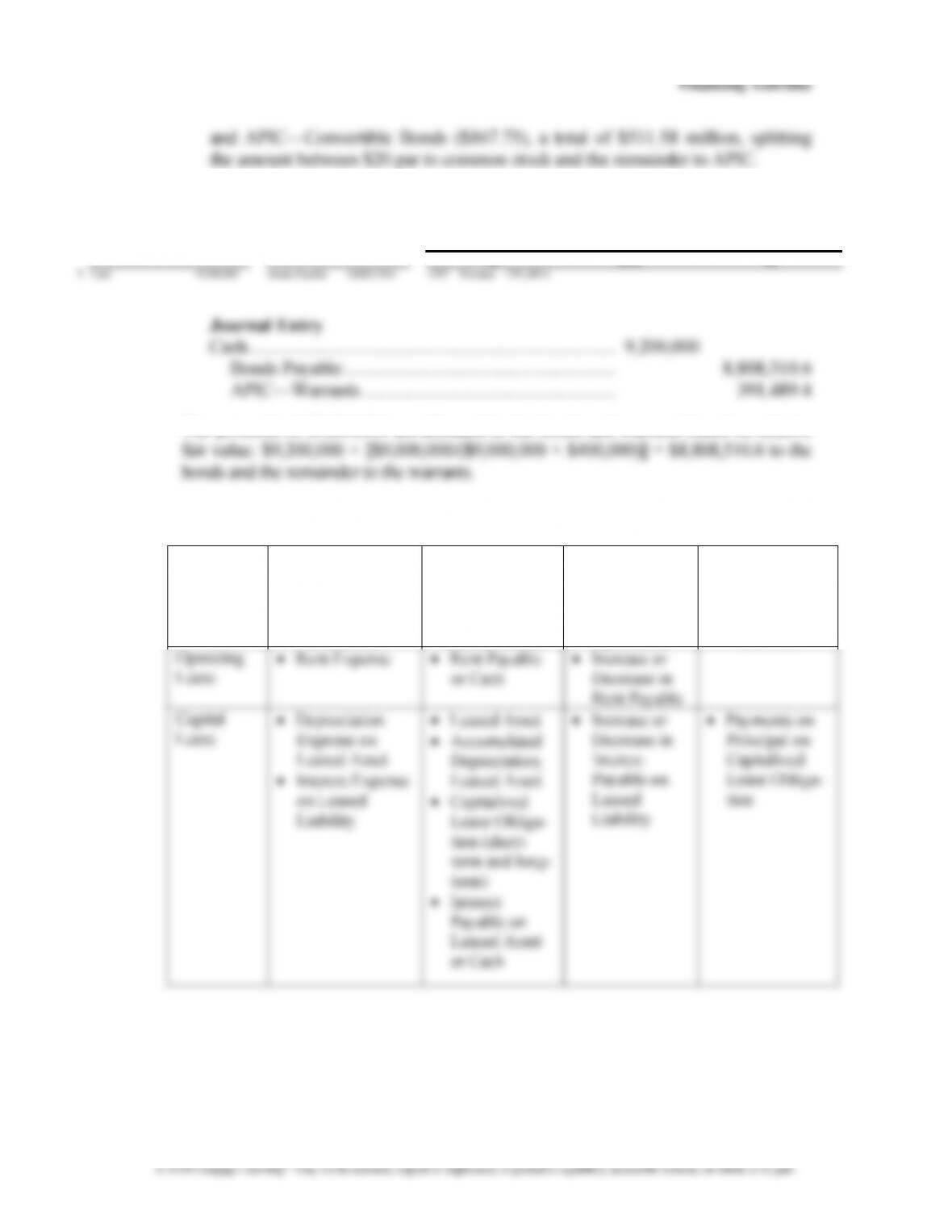

and APIC—Convertible Bonds ($167.75), a total of $511.58 million, splitting

the amount between $20 par to common stock and the remainder to APIC.

7.11 Bonds Issued with Detachable Warrants.

CC AOCI RE

Shareholders’ Equity

+LiabilitiesAssets =

The proceeds of $9,200,000 are allocated to the bonds and warrants based on relative

7.12 Effect of Capital and Operating Lease on the Financial Statements.

Income

Statement

Balance Sheet

Statement of

Cash Flows:

Cash Flows

Provided by

Operations

Statement of

Cash Flows:

Cash Used for

Financing

Activities

7-14

7.13 The following amortization table is necessary to answer the questions:

*Present value of an annuity of five payments of $16,275, discounted at 10%.

** Difference due to rounding. It should be $0 liability at the end of the lease.

Rules until January 1, 2019 New Lease Standards

7.14 Accounting for Stock-Based Compensation. Firms adopt stock option plans to

motivate employees to take actions that will increase the market value of a firm’s

7.15 Valuation of Derivatives. Firms must revalue derivatives held as speculative

investments to market value each period and recognize the resulting gain or loss in

Date Payment 10% Interest Amortization Book value

Chapter 7

Financing Activities

7-15

• Show the hedged asset and liability and its related derivative separately on the

balance sheet.

7.16 Accounting for Securitization of Receivables.

a. To record a sale, three criteria must be met:

1. The transferred assets have been isolated from the transferor. The transfer of

the receivables to a legally separate SPE and the absence of evidence that

2. The transferee has the right to pledge or exchange the assets it received, and

3. The transferor does not maintain effective control over the transferred assets

Chapter 7

Financing Activities

7-16

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

cause the holder to return specific assets. It appears that Ford Motor Credit

had relinquished control of the receivables once it transferred them to the

trust.

b. Cash ($46,900 – $12,569) ……………………………………… 34,331

d. Firms prefer to report the securitization of receivables as a sale instead of a collat-

Firms want to avoid recording the debt because it affects their future borrowing

7.17 Accounting for Off-Balance-Sheet Financing.

The analyst should consider separately the receivables for which the airline

Chapter 7

Financing Activities

7-17

varying costs of issuing a like amount of commercial paper, in addition to certain

7.18 Effect of Capitalizing Operating Leases on Balance Sheet Ratios.

a. Gap Inc. (amounts in millions)

Lease Present Value Present

Lease Payment in: Payment Factor at 8% Value

*Present value of an annuity of $360 million for three periods, then discounted

back five periods.

Limited Brands (amounts in millions)

Lease Present Value Present

Lease Payment in: Payment Factor at 8% Value

Chapter 7

Financing Activities

7-18

b. Liabilities to Assets Ratio (as reported)

Long-Term Debt Ratio (as reported)

c. Liabilities to Assets Ratio (as restated)

Long-Term Debt Ratio (as restated)

d. The debt ratios both with and without capitalization of operating leases suggest

7.19 Stock-Based Compensation.

a. Coca-Cola generated tax savings of $98 million ($365 – $267) for 2002, $114

million ($422 – $308) for 2003, and $91 million ($345 – $254) for 2004. Coca-

Cola’s tax savings from stock-based compensation is reported as part of income

b. Firms structure stock option plans so that a period of time elapses between the

Chapter 7

Financing Activities

7-19

c. The fair value of the options granted increased between 2002 and 2003 in part

because the market price of Coca-Cola’s common stock increased between

d. Firms such as Coca-Cola have concluded that the forgone cash flows from sell-

e. The value of an option at any time is:

7.20 Stock-Based Compensation.

a. Stock-based compensation does not require an outflow of cash by Eli Lilly. Be-

cause stock-based compensation is reported as an expense on Lilly’s income

Chapter 7

Financing Activities

7-20

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

equal to the market price at the date of the grant establishes the motivation for

the grantee (in most cases, employees) to take actions that will increase the

market price of the stock over time. In addition, options offered to employees

below the market price of the stock at the date of the grant must be reported as

compensation on the date of the grant by both employees and employers.

d. Eli Lilly states that the nonvested stock option expense of $397.5 million will be

amortized over the remaining service period of two years. Thus, $49.7 million

e. Analysts differ in their views on the more relevant earnings per share number.

Some believe that stock-based compensation should be reported on the income

7.21 Stock-Based Compensation—Vesting and Valuation Models.

a. Vesting refers to stock options offered to employees that can be exercised only

b. Coca-Cola reports vesting periods of one to four years for options granted in