CASE 209

Enron: Questionable Not Accounting for the

FutureLeads to Collapse

CASE NOTES FOR INSTRUCTORS

The purpose of this case is to show how it is possible for a well-known and respected company to become

swept up in unethical and illegal business practices, which can result in damage to thousands of

employees, investors, and other stakeholders. Although this case is complex and involves many actors,

one important point that emerges is how a number of individuals, including attorneys, auditors,

executives, and employees, apparently worked together to achieve Enron’s objectives, even though these

objectives were unethical and often not in the best interests of stakeholders.

The Enron case did not end with the collapse of the company. In addition to the complex ethical issues

involved in Enron’s collapse, the company, its partners, and its employees have been caught in several

ongoing legal struggles. In 2004 Enron’s new board of directors sued 11 financial institutions for helping

Lay, Fastow, Skilling, and others to hide Enron’s true financial condition. The proceedings were dubbed

the “megaclaims litigation.” Among the defendants were Royal Bank of Scotland, Deutsche Bank, and

Citigroup. Enron sold its last business, Prisma Energy, in 2006. In early 2007, it changed its name to

Enron Creditors Recovery Corporation. The sole goal of the newly-named organization was to pay off

Enron’s remaining creditors and wrap up Enron’s affairs. By 2008 Enron had settled with all involved

institutions, with Citigroup being the last. Enron was able to obtain nearly $20 million to distribute to its

creditors as a result of the megaclaims litigation.

Since the collapse of Enron, many executives who worked for the company or had business dealings with

it have been swept up in the investigations and prosecutions of the former energy giant. Many of the

people convicted of crimes connected to Enron have already served their sentences, but Jeff Skilling

remains in prison after being convicted of honest services fraud. Former CFO Andy Fastow was released

from prison and now gives lectures on business ethics in different forums. A reduction in former CEO

Jeffrey Skilling’s sentence allowed for his release in 2017. However, in June 2010 the United States

Supreme Court ruled that Skilling should not have been tried under the honest services law because it was

intended for bribes and kickbacks, not for conduct that is ambiguous or vague. However, the court’s

decision did not overturn Skilling’s conviction, but sent the case back to a lower court for evaluation. To

this day, Jeffrey Skilling continues to maintain his innocence. and appeal his case. In April of 2012, the

Supreme Court denied his appeal, claiming any errors made in the trial were negligible. However, the

following year a federal judge reduced Skilling’s sentence to 14 years.

Although this case may not seem so shocking now in the wake of Bernard Madoff and the failure of so

many of Wall Street’s most venerable firms, students should keep in mind that at that time this case sent

shock waves around the world. Instructors may wish to have students compare aspects of this Enron case

with other cases provided in this book, such as the Galleon Group and Wells Fargoand frauds of the

century. These cases share elements, such as the type of misconduct and pervasiveness of unethical

behavior in the companies’ corporate cultures. The Enron case now stands as a precursor for business

misconduct that dominated the early 21st century, and it remains a valuable case.

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

QUESTIONS AND DISCUSSION

1. How did the corporate culture of Enron contribute to its bankruptcy?

Most students will agree that Enron appears to have had a highly unethical corporate culture. However,

this point may be missed by students who are unfamiliar with business ethics and by those who view

Enron’s difficulties as stemming from accounting or auditing problems. In reality, the root of the

company’s downfall lay in its corporate culture that fostered a poor ethical climate and opportunities for

misconduct. The “rank and yank” system created a climate of fear in which performance was prized

2. Did Enron’s bankers, auditors, and attorneys contribute to Enron’s demise? If so, how?

All corporations are supposed to have a number of different gatekeepers in place who ensure that the

business’s dealings are transparent and in compliance with the law. However, in the case of Enron, these

gatekeepers, such as accountants, independent auditors, and government regulators, failed to make sure

that Enron conducted business in a way that was in stakeholders’ interests. For example, the auditors

appeared not to have held Enron to generally accepted accounting standards, which resulted in Enron

Students can also take this opportunity to discuss the roles of individuals and personal responsibility

within the larger corporate structure. Several gatekeepers and employees had opportunities to uncover and

report ethical lapses, but very few people ever questioned Enron’s practices. Highly idealistic students

Instructors may wish to use Table 1 as a supplement to the Enron case. They may want students to analyze

the sentences that were handed down after researching what each key player did and what his/her position

was in the company. Instructors can also discuss the sentencing in white-collar crime versus normal

crimes. Students can look at mandatory minimum prison sentences for a variety of violent and

white-collar crimes at http://www.cga.ct.gov/2008/rpt/2008-R-0619.htm. After students realize that, for

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

3. What role did the company’s chief financial officer play in creating the problems that led to

Enron’s financial problems?

This question should help students better understand the role of the chief financial officer (CFO), a role

filled at Enron by Andrew Fastow, who was key in creating Enron’s financial problems. Representing the

final word on a corporation’s finances, the CFO plays a very important role in most firms. At Enron, most

believe that it was Fastow who masterminded many of the unethical/illegal financial transactions that

For much of the past few decades, the role of CFO has been a contentious one. The CFO was associated

with major mergers and acquisitions deals in the early 1990s and was reputed for seeking out loopholes

and accounting tricks in the late 1990s. However, a good CFO should be a highly ethical person because

Even upstanding CFOs often become scapegoats if their companies perform poorly. Because of the

pressure, their average tenure is only about four years. After the Enron bankruptcy and the passage of the

Sarbanes-Oxley Act, CFOs have necessarily been focused on the fundamentals within their companies

(such as financial controls, internal auditing procedures, and accounting practices). In the case of Enron,

ADDITIONAL RESOURCES

Ungagged.net: The Other Side of the Enron Story offers the perspectives of Enron employees

who believe they were the victims of the federal government’s desire to get convictions and place

blame: http://ungagged.net

Interactive graph of Enron’s stock price and the actions of important Enron executives and

partners: http://www.time.com/time/interactive/0,31813,2013797,00.html

Former Enron CFO confronts fraud examiners:

http://www.accountingtoday.com/news/Former-Enron-CFO-Andrew-Fastow-Meets-Fraud-Exami

ners-67263-1.html

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

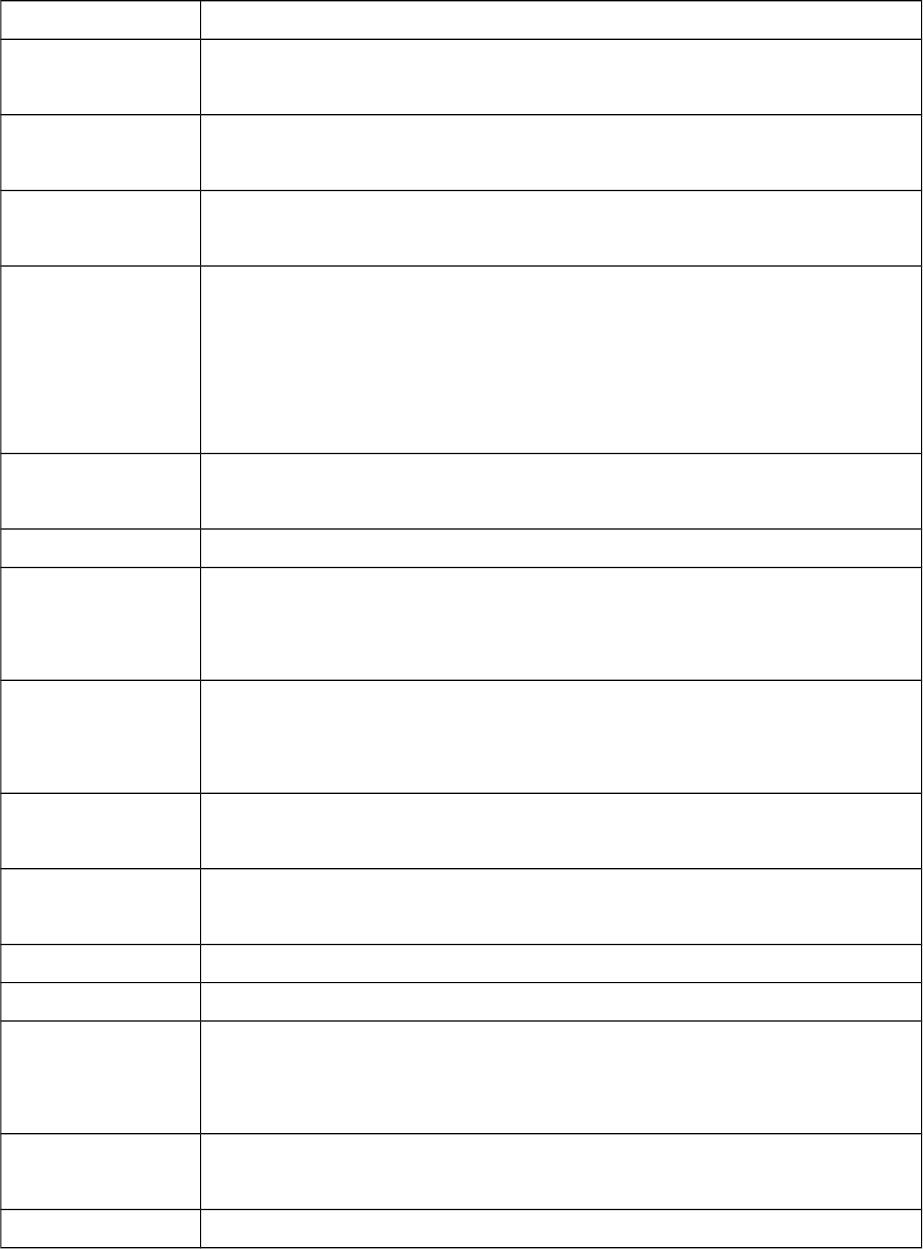

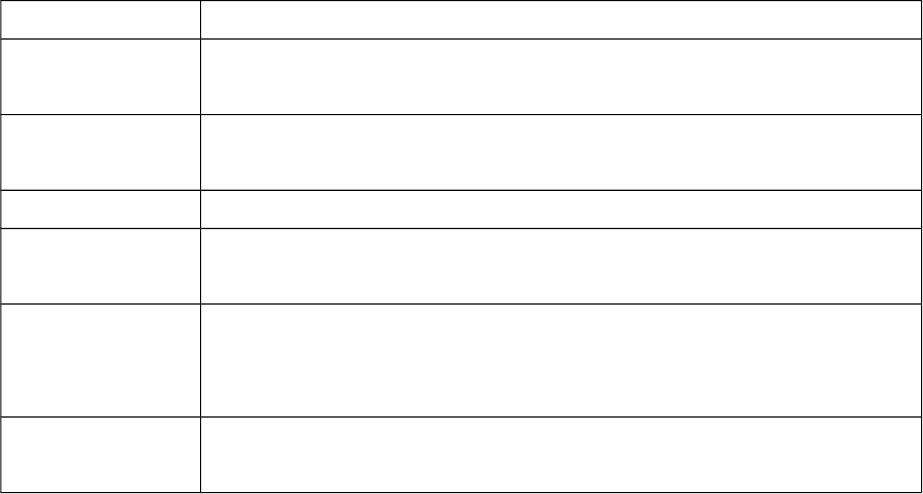

Key Enron Figures and Their Sentences

Name Sentence

Jeffrey Skilling 24 years and 4 months in prison; sentence reduced to 14 years

$45 million in fines

Andrew Fastow 6 years in prison

$23.8 million in cash and property

Lea Fastow 1 year in prison

1 year of supervised release.

Richard Causey 5 years and 6 months in prison

2 years of probation

$25,000 fine

Agreed to pay another $1.25 million to the victims’ funds

Forfeited a claim to about $250,000 in deferred compensation

Ben Glisan Jr. 5 years in prison

Michael Kopper 37 months in prison, served 23 months

Jordan Mintz $25,000 in civil fines

$1 in disgorgement

2 year ban from practicing before the SEC

David Duncan $25,000 in civil fines

$1 in disgorgement

2 year ban from practicing before the SEC

Timothy Belden $2.1 million in fines

2 year ban from practicing before the SEC

Larry Lawyer 2 years of probation

Jeffrey Richter 2 years of probation

Kevin Howard 1 year of probation

Rex Shelby 3 months in a halfway house

3 months of house arrest

$3.6 million in fines

Dan Boyle 3 years and 10 months in prison

$320,000 in fines

David Delainey 2 years and 6 months in prison

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

$8 million in fines

Paula Rieker 2 years of probation

Kenneth Rice 27 months in prison

$15 million in fines

John Forney 2 years of probation

Mark Koenig 18 months in prison

$50,000 in fines.

Kevin Hannon 2 years in prison

2 years of probation

$125,000 fine

Timothy Despain 4 years of probation

$10,000 in fines

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.