CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-16

Prob. 9–4A

1.

Depreciation

Expense

Accumulated

Depreciation,

Book Value,

Year

End of Year

End of Year

a.

1 …………………………………………………….. $142,000

$142,000

$658,000

2 …………………………………………………….. 142,000

284,000

516,000

3 …………………………………………………….. 142,000

426,000

374,000

4 …………………………………………………….. 142,000

568,000

232,000

5 …………………………………………………….. 142,000

710,000

90,000

Yearly depreciation = [($800,000 – $90,000) ÷ 5] = $142,000

b.

1

[$800,000 (100% ÷ 5) 2] ……….. $320,000

$320,000

$480,000

2

[$480,000 (100% ÷ 5) 2] ……….. 192,000

512,000

288,000

3

[$288,000 (100% ÷ 5) 2] ……….. 115,200

627,200

172,800

4

[$172,800 (100% ÷ 5) 2] ……….. 69,120

696,320

103,680

5

[$800,000 – $696,320 – $90,000) … 13,680

710,000

90,000

Note: Book value should not be reduced below $90,000, the residual value.

2.

Mar.

4

Cash

135,000

Accumulated Depreciation—Equipment

696,320

Equipment

800,000

Gain on Sale of Equipment

31,320

Gain on sale of equipment = $135,000 – ($800,000 – $696,320) = $31,320

3.

Mar.

4

Cash

88,750

Accumulated Depreciation—Equipment

696,320

Loss on Sale of Equipment

14,930

Equipment

800,000

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-17

Prob. 9–5A

Year 1

Jan.

4

Delivery Truck

26,000

Cash

26,000

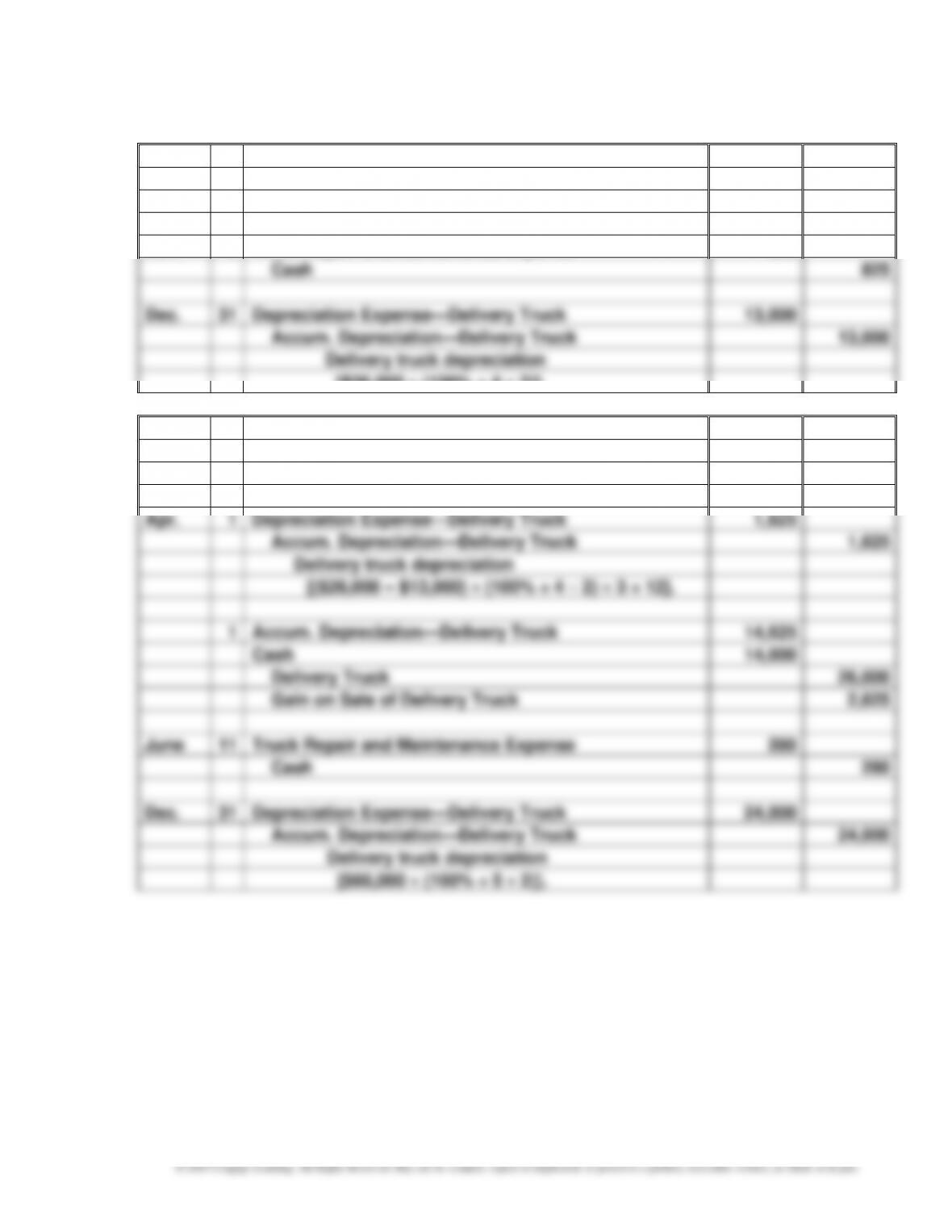

Nov.

2

Truck Repair and Maintenance Expense

825

Cash

825

Dec.

31

Depreciation Expense—Delivery Truck

13,000

Accum. Depreciation—Delivery Truck

13,000

Delivery truck depreciation

[$26,000 (100% ÷ 4 2)].

Year 2

Jan.

6

Delivery Truck

60,000

Cash

60,000

Apr.

1

Depreciation Expense—Delivery Truck

1,625

Accum. Depreciation—Delivery Truck

1,625

Delivery truck depreciation

[($26,000 – $13,000) (100% ÷ 4 2) 3 ÷ 12].

1

Accum. Depreciation—Delivery Truck

14,625

Cash

14,000

Delivery Truck

26,000

Gain on Sale of Delivery Truck

2,625

June

11

Truck Repair and Maintenance Expense

280

Cash

280

Dec.

31

Depreciation Expense—Delivery Truck

24,000

Accum. Depreciation—Delivery Truck

24,000

Delivery truck depreciation

[$60,000 (100% ÷ 5 2)].

CHAPTER 9 Long-Term Assets: Fixed and Intangible

Prob. 9–5A (Concluded)

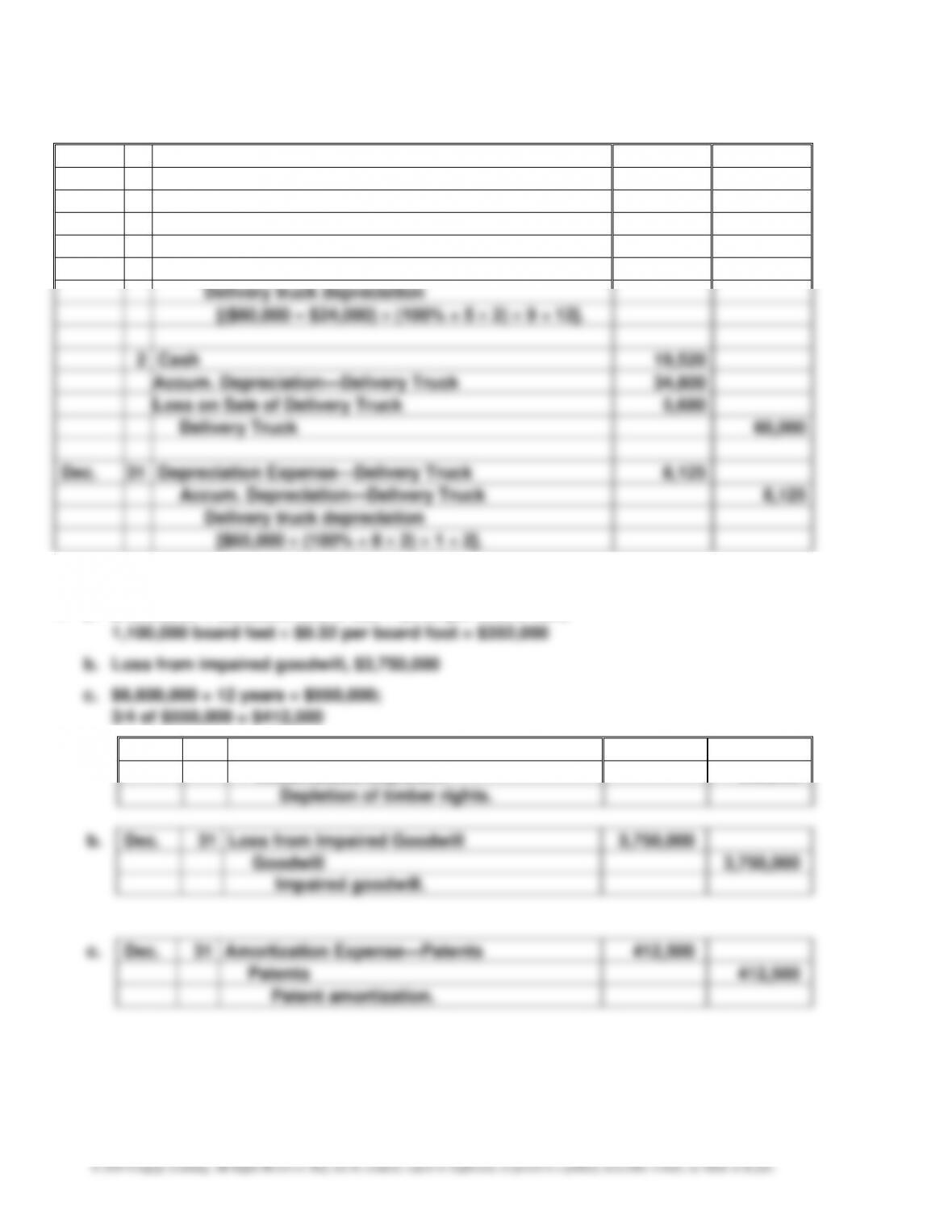

Year 3

July

1

Delivery Truck

65,000

Cash

65,000

Oct.

2

Depreciation Expense—Delivery Truck

10,800

Accum. Depreciation—Delivery Truck

10,800

Delivery truck depreciation

[($60,000 – $24,000) (100% ÷ 5 2) 9 ÷ 12].

2

Cash

19,520

Accum. Depreciation—Delivery Truck

34,800

Loss on Sale of Delivery Truck

5,680

Delivery Truck

60,000

Dec.

31

Depreciation Expense—Delivery Truck

8,125

Accum. Depreciation—Delivery Truck

8,125

Delivery truck depreciation

[$65,000 (100% ÷ 8 2) 1 ÷ 2].

Prob. 9–6A

1. a. $1,600,000 ÷ 5,000,000 board feet = $0.32 per board foot;

2.

a.

Dec.

31

Depletion Expense

352,000

Accumulated Depletion

352,000

Depletion of timber rights.

Dec.

Amortization Expense—Patents

412,500

Patents

412,500

Patent amortization.

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-19

Prob. 9–1B

1.

Item

Land

Land

Improvements

Building

Other

Accounts

a.

$ 3,600

b.

780,000

c.

23,400

d.

15,000

e.

$ 75,000

f.

10,000

g.

(3,400)*

h.

18,000

i.

8,400

j.

$(800,000)*

k.

13,400

l.

3,000

m.

2,000

n.

$14,000

o.

21,600

p.

40,000

q.

(4,500)*

r.

800,000

s.

(1,400)*

2.

$860,000

$35,600

$922,000

* Receipt.

3. Land used as a plant site does not lose its ability to provide services; thus, it is not

4. Because land improvements are depreciated, depreciation expense of $4,320 ($21,600

1 ÷ 10 2) would be understated, and net income would be overstated by $4,320 on

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-20

Prob. 9–2B

1.

Depreciation Expense

Year

a. Straight-

Line

Method

b. Units-of–

Activity

Method

c. Double-

Declining-Balance

Method

Year 1

$ 71,250

$102,600

$160,000

Year 2

71,250

91,200

80,000

Year 3

71,250

62,700

40,000

Year 4

71,250

28,500

5,000

Total

$285,000

$285,000

$285,000

Units-of–activity method:

($320,000 – $35,000) ÷ 20,000 hours = $14.25 per hour

3. Over the four-year life of the equipment, all three depreciation methods yield the same

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-21

Prob. 9–3B

a. Straight-line method:

Year 1: [($108,000 – $7,200) ÷ 3] 3 ÷ 12 …………………………………… $ 8,400

b. Units-of-activity method:

Activity rate = ($108,000 – $7,200) ÷ 12,000 hours = $8.40 per hour

c. Double-declining-balance method:

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-22

Prob. 9–4B

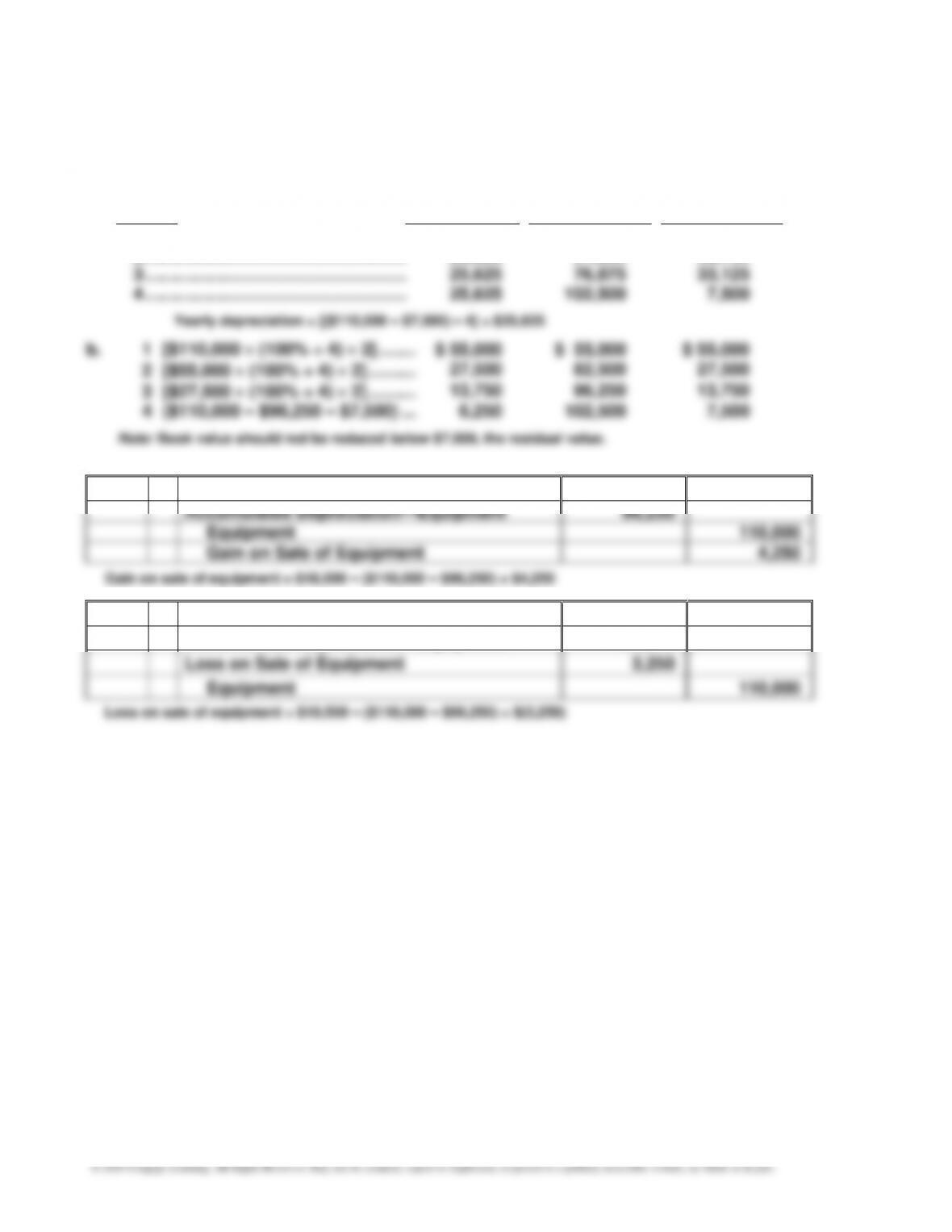

1.

Year

Depreciation

Expense

Accumulated

Depreciation,

End of Year

Book Value,

End of Year

a.

1 ………………………………………………………

$ 25,625

$ 25,625

$ 84,375

2 ………………………………………………………

25,625

51,250

58,750

3 ………………………………………………………

25,625

76,875

33,125

4 ………………………………………………………

25,625

102,500

7,500

Yearly depreciation = [($110,000 – $7,500) – 4] = $25,625

b.

1 [$110,000 (100% ÷ 4) 2] ……………

$ 55,000

$ 55,000

$ 55,000

2 [$55,000 (100% ÷ 4) 2] ……………..

27,500

82,500

27,500

3 [$27,500 (100% ÷ 4) 2] ……………..

13,750

96,250

13,750

4 ($110,000 – $96,250 – $7,500) ……….

6,250

102,500

7,500

Note: Book value should not be reduced below $7,500, the residual value.

2.

Sept.

6

Cash

18,000

Accumulated Depreciation—Equipment

96,250

Equipment

110,000

Gain on Sale of Equipment

4,250

Gain on sale of equipment = $18,000 – ($110,000 – $96,250) = $4,250

3.

Sept.

6

Cash

10,500

Accumulated Depreciation—Equipment

96,250

Loss on Sale of Equipment

3,250

Equipment

110,000

Loss on sale of equipment = $10,500 – ($110,000 – $96,250) = $(3,250)

CHAPTER 9 Long-Term Assets: Fixed and Intangible

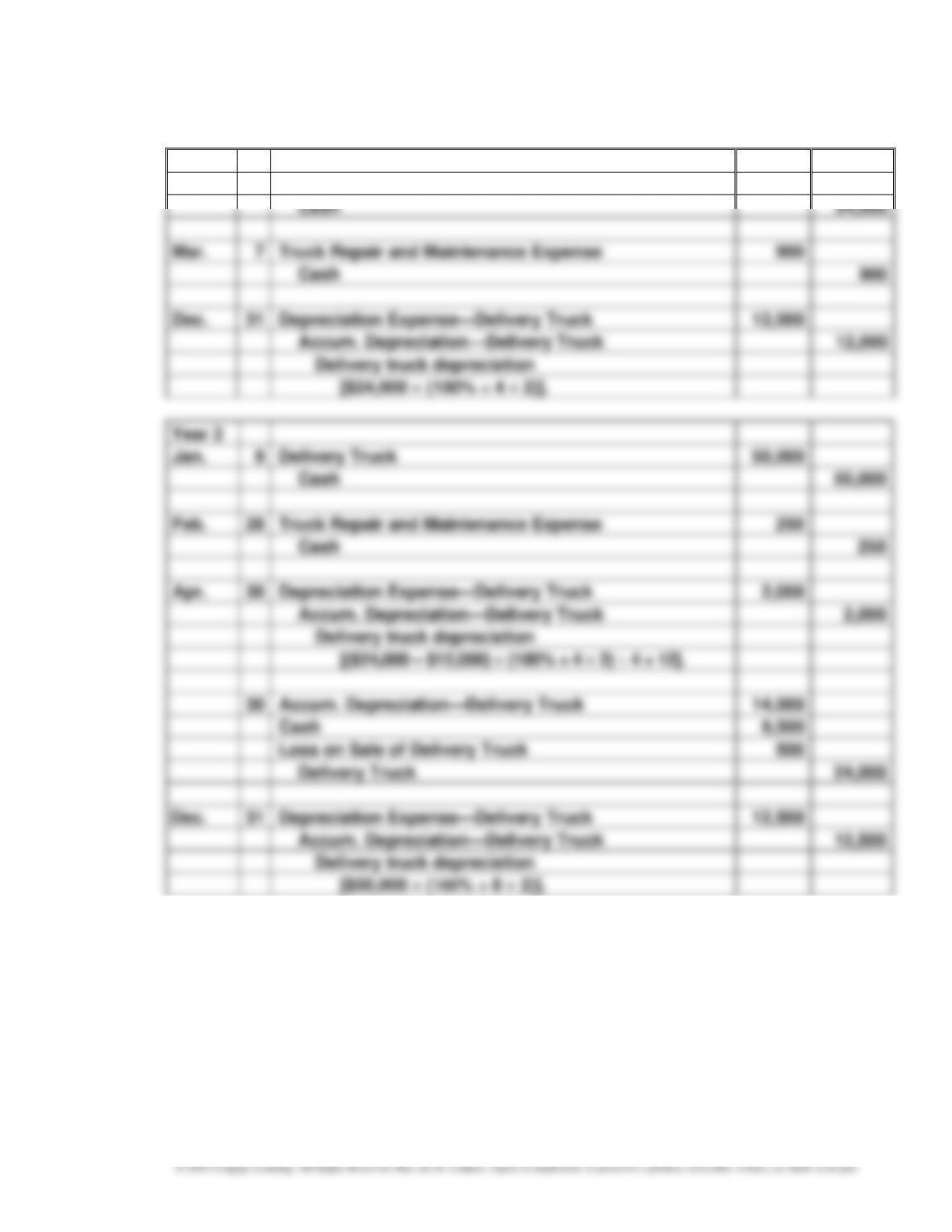

Prob. 9–5B

Year 1

Jan.

8

Delivery Truck

24,000

Cash

24,000

Mar.

7

Truck Repair and Maintenance Expense

900

Cash

900

Dec.

31

Depreciation Expense—Delivery Truck

12,000

Accum. Depreciation—Delivery Truck

12,000

Delivery truck depreciation

[$24,000 (100% ÷ 4 2)].

Jan.

9

Delivery Truck

50,000

Cash

Truck Repair and Maintenance Expense

250

Cash

Apr.

Depreciation Expense—Delivery Truck

Accum. Depreciation—Delivery Truck

Delivery truck depreciation

[($24,000 – $12,000) (100% ÷ 4 2) 4 ÷ 12].

Accum. Depreciation—Delivery Truck

14,000

Cash

Loss on Sale of Delivery Truck

500

Delivery Truck

Depreciation Expense—Delivery Truck

12,500

Accum. Depreciation—Delivery Truck

Delivery truck depreciation

[$50,000 (100% ÷ 8 2)].

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-24

Prob. 9–5B (Concluded)

Year 3

Sept.

1

Delivery Truck

58,500

Cash

58,500

4

Depreciation Expense—Delivery Truck

6,250

Accum. Depreciation—Delivery Truck

6,250

Delivery truck depreciation

[($50,000 – $12,500) (100% ÷ 8 2) 8 ÷ 12].

4

Cash

36,000

Accum. Depreciation—Delivery Truck

18,750

Delivery Truck

50,000

Gain on Sale of Delivery Truck

4,750

Dec.

31

Depreciation Expense—Delivery Truck

3,900

Accum. Depreciation—Delivery Truck

3,900

Delivery truck depreciation

[$58,500 (100% ÷ 10 2) 4 ÷ 12].

Prob. 9–6B

1. a. Loss from impaired goodwill, $3,400,000

2.

a.

Dec.

31

Loss from Impaired Goodwill

3,400,000

Goodwill

3,400,000

Impaired goodwill.

b.

Dec.

31

Amortization Expense—Patents

150,000

Patents

150,000

Patent amortization.

c.

Dec.

31

Depletion Expense

987,700

Accumulated Depletion

987,700

Depletion of timber rights.

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-25

MAKE A DECISION

MAD 9–1

a.

AssetsFixed of ValueBook Average

Sales

Ratio Turnover Asset Fixed =

41.7

$212

$8,830

:Netflix

5.3

$25,476

$135,987

:Amazon

=

=

b. Netflix is more efficient than Amazon in generating revenue from fixed assets. Netflix’s

c. The difference in their fixed asset turnover ratios reflects the difference in their core

businesses. Netflix is mostly an Internet streaming and DVD rental company. These

MAD 9–2

a.

AssetsFixed of ValueBook Average

Sales

Ratio Turnover Asset Fixed =

$5,931 =

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-26

MAD 9–2 (Concluded)

b. Delta Air Lines has the largest fixed asset turnover ratio and, thus, is more efficient in

improved scheduling, maintenance, and operating procedures.

MAD 9–3

a.

AssetsFixed of ValueBook Average

Sales

Ratio Turnover Asset Fixed =

2 $83,541) ($84,751

$125,980 =

+

b. Verizon earns $1.50 revenue for every dollar of fixed assets. Telecommunications requires

MAD 9–4

a.

AssetsFixed of ValueBook Average

Sales

Ratio Turnover Asset Fixed =

3.3

$18,576

$60,906

:UPS

2.2

$22,580

$50,365

:FedEx

=

=

b. The ratios show that UPS is 50% more efficient at using its fixed assets than FedEx

CHAPTER 9 Long-Term Assets: Fixed and Intangible

MAD 9–4 (Concluded)

c. The fixed asset turnover is a measure of how efficiently revenue is generated from

underlying fixed assets. In the case of UPS, the fixed assets represent all fixed assets

MAD 9–5

a.

AssetsFixed of ValueBook Average

Sales

Ratio Turnover Asset Fixed =

$80,403 =

CHAPTER 9 Long-Term Assets: Fixed and Intangible

TAKE IT FURTHER

TIF 9–1

1. Estimates of the factors determining depreciation expense create a unique financial

reporting challenge. Because the useful life and residual value are estimates, there

is no “correct” amount. The company must use judgment along with historical data to

2. In this case, both Mike and James appear to be acting unethically. The original useful life

and residual value estimates were based on good faith estimates. By changing these

TIF 9–2

A sample solution based on McDonald’s Form 10-K for the fiscal year ended December 31,

2016, follows:

1. a. Depreciation is determined on a straight-line basis. The following estimated useful

lives are used: buildings—up to 40 years; leasehold improvements—the lesser of

useful lives or lease terms; equipment—3 to 12 years.

2. No. Book value is the difference between the fixed asset account and its related

accumulated depreciation account.

9-29

TIF 9–3

To: Chief Financial Officer, Godwin Co.

From: IMA Student

Re: Financial Statement Effects of Modifications to Trucks 1 and 2

TIF 9-4

You should explain to Nolan and Stacy that it is acceptable to maintain two sets of records for

tax and financial reporting purposes. This can happen when a company uses one method for

financial statement purposes, such as straight-line depreciation, and another method for tax

purposes, such as MACRS depreciation. This should not be surprising because the methods