Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

9-1

CHAPTER 9

LONG-TERM ASSETS: FIXED AND INTANGIBLE

DISCUSSION QUESTIONS

1. a. O’Neil Office Supplies: Property, plant, and equipment or Fixed assets

depreciation account. Revenue expenditures are recorded as expenses and are costs that benefit only the

current period and are incurred for normal maintenance and repairs of fixed assets.

8. a. An accelerated depreciation method is most appropriate for situations in which the decline in

productivity or earning power of the asset is proportionately greater in the early years of use than in

9. a. No, the accumulated depreciation for an asset cannot exceed the cost of the asset. To do so would

create a negative book value, which is meaningless.

10. a. The cost of a patent should be amortized over the shorter of its legal life or years of usefulness.

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-2

BASIC EXERCISES

BE 9–1

BE 9–2

BE 9–3

BE 9–4

BE 9–5

Feb.

14

Accumulated Depreciation—Delivery Van

2,300

Cash

2,300

14

Delivery Van

450

Cash

450

CHAPTER 9 Long-Term Assets: Fixed and Intangible

BE 9–6

b. $20,625 gain, computed as follows:

c.

Dec.

31

Cash

480,000

Accumulated Depreciation—Equipment

140,625

Equipment

600,000

Gain on Sale of Equipment

20,625

BE 9–7

c.

Dec.

31

Depletion Expense

32,760,000

Accumulated Depletion

32,760,000

Depletion of mineral deposit.

BE 9–8

a.

April

1

Patent

1,500,000

Cash

1,500,000

Acquired patent.

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-5

EXERCISES

Ex. 9–1

Ex. 9–2

Ex. 9–3

Purchase price of land ($90,000 + $50,000) ................................

$ 140,000

Legal fees .....................................................................................

$ 1,750

Delinquent taxes ................................................................

25,000

Demolition of building ................................................................

9,000

35,750

Total costs ........................................................................................

$ 175,750

Salvage of materials ................................................................

(1,000)

Cost of land to be reported .............................................................

$ 174,750

Ex. 9–4

a. No. The $65,500,000 represents the original cost of the equipment. Its

Ex. 9–5

Ex. 9–6

Ex. 9–7

hour per ondepreciati $3.70

hours 28,000

$16,400 – $120,000 =

150 hours at $3.70 = $555 depreciation for April

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-6

Ex. 9–8

a.

Depreciation rate per mile:

Truck No.

Rate per Mile

Miles Operated

Credit to

Accumulated

Depreciation

1

$0.26

21,000

$ 5,460

2

0.16

33,500

5,360

3

0.31

8,000

1,860

4

0.28

22,500

6,300

Total ...................................................................................

$18,980

Note: Mileage depreciation of $2,480 (31 cents 8,000) is limited to $1,860 for Truck 3,

which reduces the book value of the truck to $10,900, its residual value.

b.

Dec.

31

Depreciation Expense—Trucks

18,980

Accumulated Depreciation—Trucks

18,980

Truck depreciation.

Ex. 9–9

a.

$8,500 $85,000 of 10%

Year Second

$8,500 $85,000 of 10%

YearFirst

==

Ex. 9–10

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-7

Ex. 9–11

Ex. 9–12

Ex. 9–13

Ex. 9–14

Ex. 9–15

Mar.

20

Accumulated Depreciation—Delivery Truck

1,890

Cash

1,890

June

11

Delivery Truck

1,350

Cash

1,350

Nov.

30

Repairs and Maintenance Expense

55

Cash

55

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-8

Ex. 9–16

a.

Apr.

30

Carpet

18,000

Cash

18,000

b.

Dec.

31

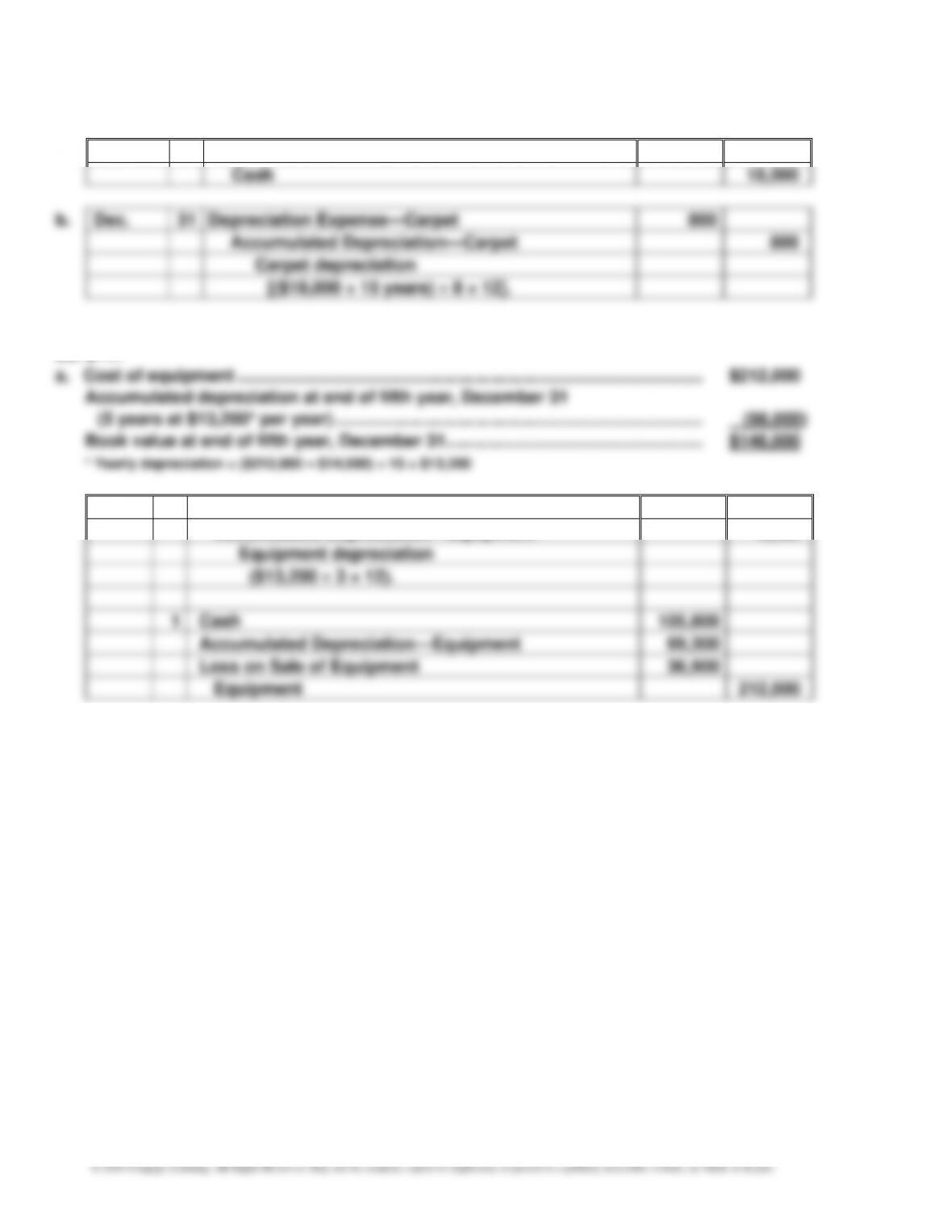

Depreciation Expense—Carpet

800

Accumulated Depreciation—Carpet

800

Carpet depreciation

[($18,000 ÷ 15 years) 8 ÷ 12].

Ex. 9–17

b.

Apr.

1

Depreciation Expense—Equipment

3,300

Accumulated Depreciation—Equipment

3,300

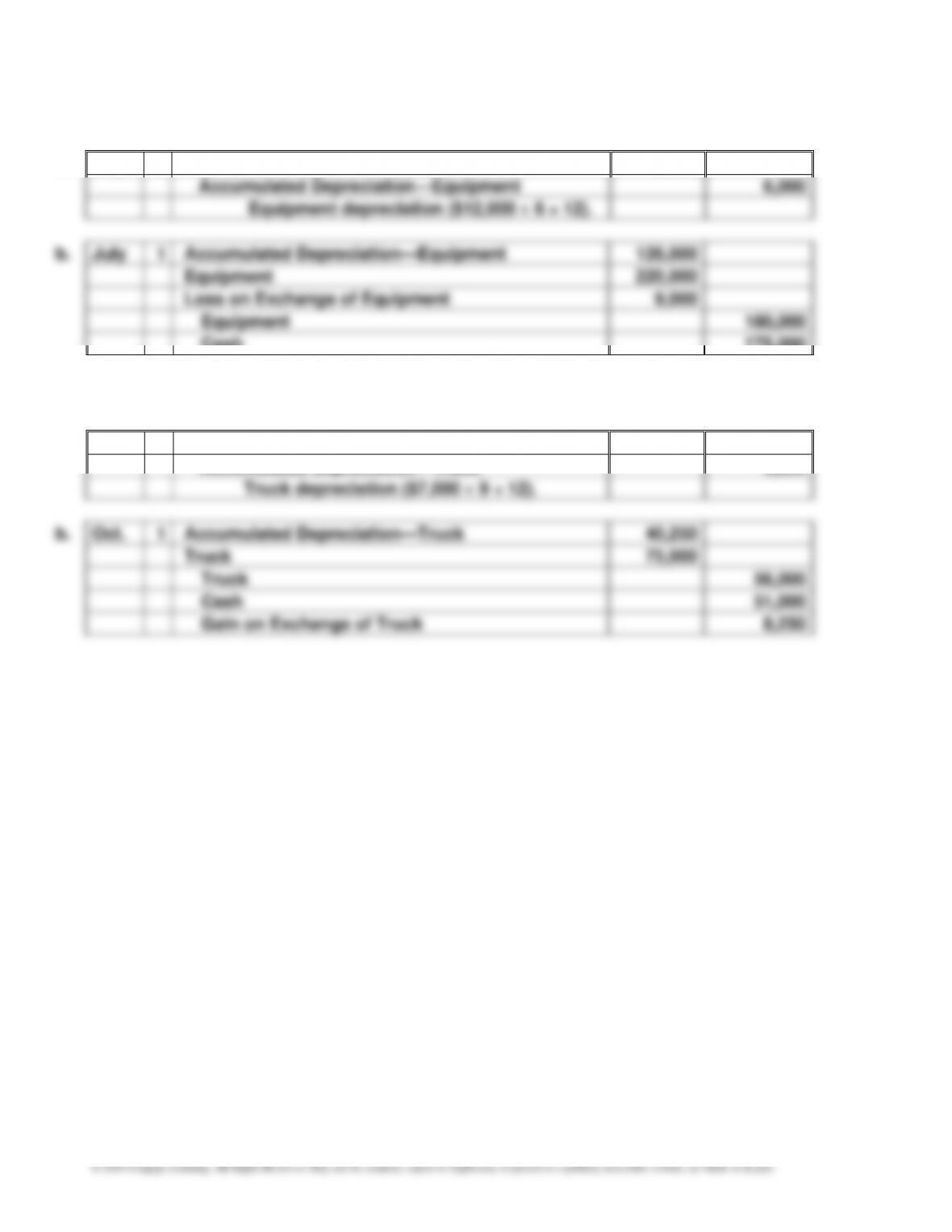

Equipment depreciation

($13,200 3 ÷ 12).

1

Cash

105,800

Accumulated Depreciation—Equipment

69,300

Loss on Sale of Equipment

36,900

Equipment

212,000

Loss on sale of equipment = [($212,000 – $69,300) – $105,800] = $(36,900)

CHAPTER 9 Long-Term Assets: Fixed and Intangible

Ex. 9–18

c.

Year 4

Jan.

3

Cash

300,000

Accumulated Depreciation—Equipment

52,500

Loss on Sale of Equipment

22,500

Equipment

375,000

Loss on sale of equipment = $322,500 – $300,000 = $(22,500)

d.

Year 4

Jan.

3

Cash

325,000

Accumulated Depreciation—Equipment

52,500

Equipment

375,000

Gain on Sale of Equipment

2,500

Gain on sale of equipment = $325,000 – $322,500 = $2,500

Ex. 9–19

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-10

Ex. 9–21

a. Property, plant, and equipment (in millions):

Current

Year

Preceding

Year

Land and buildings ..........................................................

$10,185

$6,956

Machinery, equipment, and internal-use software ........

44,543

37,038

Other fixed assets ............................................................

6,517

5,263

Total cost ..........................................................................

$ 61,245

$ 49,257

Accumulated depreciation and amortization .................

(34,235)

(26,786)

Book value .......................................................................

$ 27,010

$ 22,471

A comparison of the book values of the current and preceding years indicates that they

increased. A comparison of the total cost and accumulated depreciation reveals that

Apple purchased $11,988 million ($61,245 – $49,257) of additional fixed assets, which was

offset by the additional depreciation expense of $7,449 million ($34,235 – $26,786) taken

during the current year.

b. We would expect Apple’s book value of fixed assets to increase during the year as its

sales increase. Although additional depreciation expense for the current year will reduce

Ex. 9–22

1. Fixed assets should be reported at cost and not replacement cost.

CHAPTER 9 Long-Term Assets: Fixed and Intangible

Appendix Ex. 9–23

a.

Price (fair market value) of new equipment .........................

$ 275,000

Trade-in allowance of old equipment ...................................

(90,000)

Cash paid on the date of exchange ......................................

$ 185,000

b.

Fair market value (trade-in allowance) of old equipment ....

$ 90,000

Book value of old equipment ................................................

(68,000)

Gain on exchange of equipment ...........................................

$ 22,000

or

Price (fair market value) of new equipment ..........................

$ 275,000

Assets given up in exchange:

Book value of old equipment ...........................................

$ 68,000

Cash paid on the exchange .............................................

185,000

(253,000)

Gain on exchange of equipment ...........................................

$ 22,000

Appendix Ex. 9–24

a.

Price (fair market value) of new equipment .........................

$ 275,000

Trade-in allowance of old equipment ...................................

(90,000)

Cash paid on the date of exchange ......................................

$ 185,000

b.

Fair market value (trade-in allowance) of old equipment ....

$ 90,000

Book value of old equipment ................................................

(108,000)

Gain on exchange of equipment ...........................................

$ (18,500)

CHAPTER 9 Long-Term Assets: Fixed and Intangible

Appendix Ex. 9–25

a.

July

1

Depreciation Expense—Equipment

6,000

Accumulated Depreciation—Equipment

6,000

Equipment depreciation ($12,000 6 ÷ 12).

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-13

PROBLEMS

Prob. 9–1A

1.

Item

Land

Land

Improvements

Building

Other

Accounts

a.

$ 2,500

b.

340,000

c.

15,500

d.

5,000

e.

(4,000)*

f.

29,000

g.

$ 60,000

h.

6,000

i.

12,000

j.

$(900,000)*

k.

5,500

l.

$32,000

m.

11,000

n.

2,000

o.

2,500

p.

(7,500)*

q.

800,000

r.

34,500

s.

(500)*

2.

$400,000

$45,000

$ 900,000

3. Land used as a plant site does not lose its ability to provide services; thus, it is not

4. Because land improvements are depreciated, depreciation expense of $1,200

CHAPTER 9 Long-Term Assets: Fixed and Intangible

9-14

Prob. 9–2A

1.

Depreciation Expense

Year

a. Straight-

Line

Method

b. Units-of-

Activity

Method

c. Double-

Declining-Balance

Method

Year 1

$22,500

$28,500

$48,000

Year 2

22,500

22,500

16,000

Year 3

22,500

16,500

3,500

Total

$67,500

$67,500

$67,500

Units-of-activity method:

($72,000 – $4,500) ÷ 18,000 hours = $3.75 per hour

3. Over the three-year life of the equipment, all three depreciation methods yield

CHAPTER 9 Long-Term Assets: Fixed and Intangible

Prob. 9–3A

a. Straight-line method:

Year 1: [($270,000 – $9,000) ÷ 3] 9 ÷ 12 ...................................... $65,250