CHAPTER 8 Receivables

8–20

Prob. 8–3A

1.

Year

Bad Debt Expense

Balance of

Allowance

Account,

End of Year

Expense

Actually

Reported

Expense

Based on

Estimate

Increase

(Decrease)

in Amount

of Expense

1

$ 4,500

$ 9,000

$4,500

$ 4,500

2

9,600

12,500

2,900

7,400

3

12,800

15,000

2,200

9,600

4

16,550

22,000

5,450

15,050

2. Yes. The actual write-offs of accounts originating in the first two years are reasonably

close to the expense that would have been charged to those years on the basis of 1% of

CHAPTER 8 Receivables

8–21

Prob. 8–4A

1. (a) (b)

Note

Due Date

Interest Due at Maturity

1.

May 5

$500

($75,000 60 ÷ 360 4%)

2.

May 22

300

($40,000 45 ÷ 360 6%)

3.

Dec. 10

600

($36,000 120 ÷ 360 5%)

4.

Nov. 21

180

($27,000 30 ÷ 360 8%)

5.

Feb. 17

360

($48,000 90 ÷ 360 3%)

6.

Jan. 29

450

($72,000 45 ÷ 360 5%)

2.

Dec.

10

Accounts Receivable

36,600

Notes Receivable

36,000

Interest Revenue

600

3.

Dec.

31

Interest Receivable

328

Interest Revenue

328

Accrued interest:

$48,000 3% 42 360

= $168

$72,000 5% 16 360

160

Total

$328

4.

Jan.

29

Cash

72,450

Notes Receivable

72,000

Interest Receivable

160

Interest Revenue ($72,000 5% 29 ÷ 360).

290

Feb.

17

Cash

48,360

Notes Receivable

48,000

Interest Receivable

168

Interest Revenue ($48,000 3% 48 ÷ 360).

192

CHAPTER 8 Receivables

8–22

Prob. 8–5A

Apr.

10

Notes Receivable

144,000

Accounts Receivable

144,000

May

15

Notes Receivable

270,000

Accounts Receivable

270,000

June

9

Cash

145,200

Notes Receivable

144,000

Interest Revenue ($144,000 5% 60 ÷ 360)

1,200

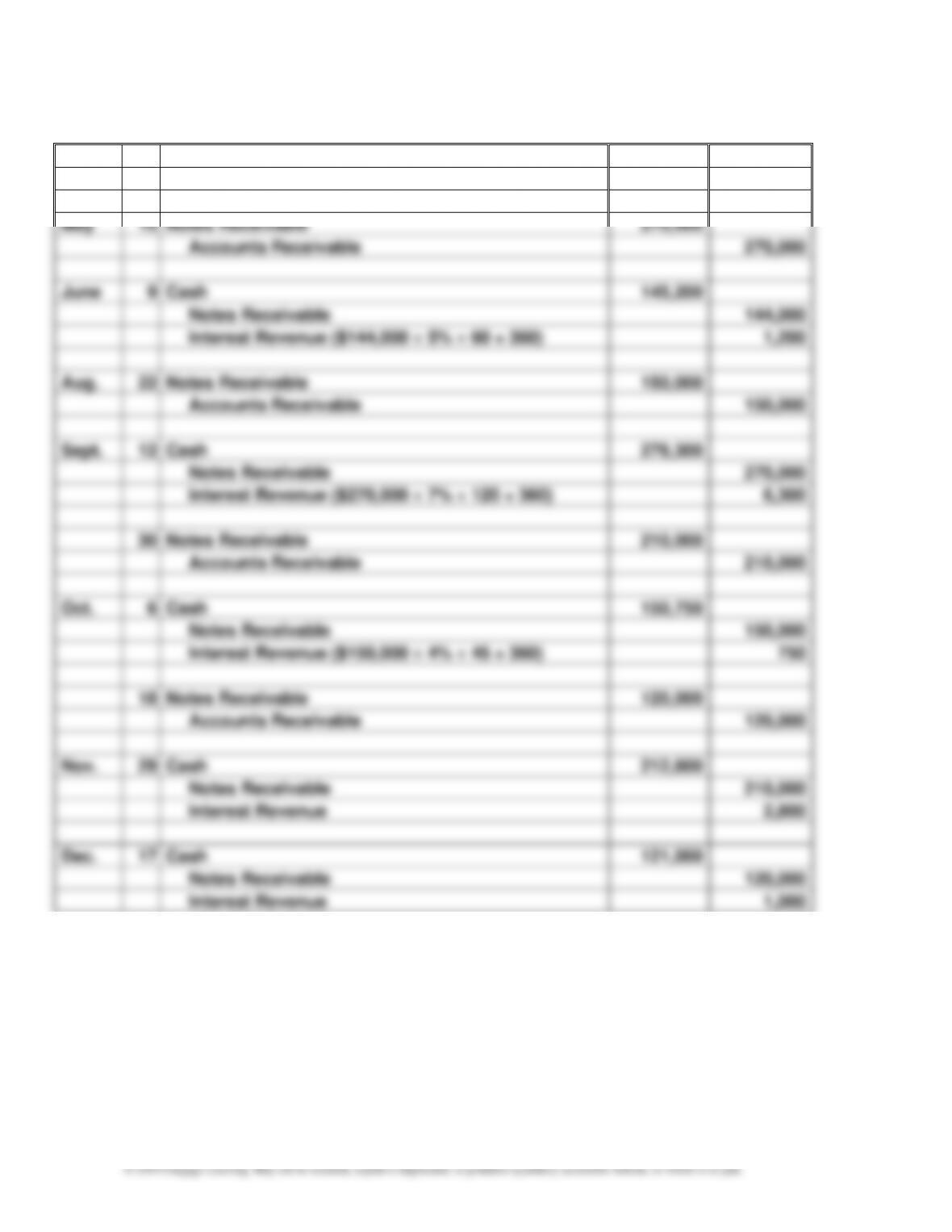

Aug.

22

Notes Receivable

150,000

Accounts Receivable

150,000

Sept.

12

Cash

276,300

Notes Receivable

270,000

Interest Revenue ($270,000 7% 120 ÷ 360)

6,300

30

Notes Receivable

210,000

Accounts Receivable

210,000

Oct.

6

Cash

150,750

Notes Receivable

150,000

Interest Revenue ($150,000 4% 45 ÷ 360)

750

18

Notes Receivable

120,000

Accounts Receivable

120,000

Nov.

29

Cash

212,800

Notes Receivable

210,000

Interest Revenue

2,800

Dec.

17

Cash

121,000

Notes Receivable

120,000

Interest Revenue

1,000

CHAPTER 8 Receivables

8–23

Prob. 8–6A

Jan.

3

Notes Receivable

18,000

Cash

18,000

Feb.

10

Accounts Receivable—Bradford & Co.

24,000

Sales

24,000

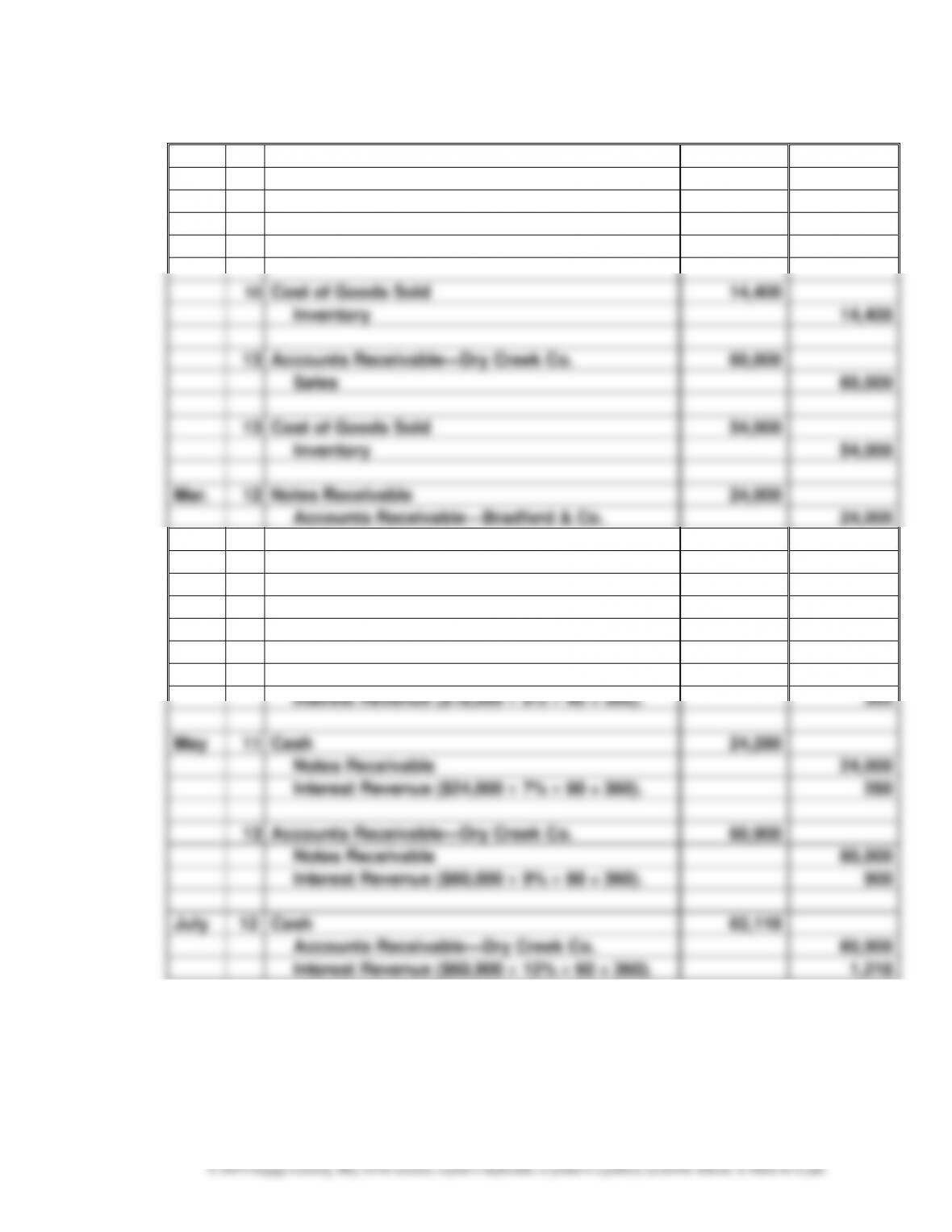

10

Cost of Goods Sold

14,400

Inventory

14,400

13

Accounts Receivable—Dry Creek Co.

60,000

Sales

60,000

13

Cost of Goods Sold

54,000

Inventory

54,000

Mar.

12

Notes Receivable

24,000

Accounts Receivable—Bradford & Co.

24,000

14

Notes Receivable

60,000

Accounts Receivable—Dry Creek Co.

60,000

Apr.

3

Notes Receivable

18,000

Cash

360

Notes Receivable

18,000

Interest Revenue ($18,000 8% 90 ÷ 360).

360

May

11

Cash

24,280

Notes Receivable

24,000

Interest Revenue ($24,000 7% 60 ÷ 360).

280

13

Accounts Receivable—Dry Creek Co.

60,900

Notes Receivable

60,000

Interest Revenue ($60,000 9% 60 ÷ 360).

900

July

12

Cash

62,118

Accounts Receivable—Dry Creek Co.

60,900

Interest Revenue ($60,900 12% 60 ÷ 360).

1,218

CHAPTER 8 Receivables

8–24

Prob. 8–6A (Concluded)

Aug.

1

Cash

18,540

Notes Receivable

18,000

Interest Revenue ($18,000 9% 120 ÷ 360).

540

Oct.

5

Accounts Receivable—Halloran Co.

13,230

Sales

13,230

5

Cost of Goods Sold

8,100

Inventory

8,100

15

Cash

13,230

Accounts Receivable—Halloran Co.

13,230

CHAPTER 8 Receivables

8–25

Prob. 8–1B

2.

Jan.

19

Accounts Receivable—Arlene Gurley

2,660

Allowance for Doubtful Accounts

2,660

19

Cash

2,660

Accounts Receivable—Arlene Gurley

2,660

Apr.

3

Allowance for Doubtful Accounts

12,750

Accounts Receivable—Premier GS Co.

12,750

July

16

Cash

5,500

Allowance for Doubtful Accounts

16,500

Accounts Receivable—Hayden Co.

22,000

Nov.

23

Accounts Receivable—Harry Carr

4,000

Allowance for Doubtful Accounts

4,000

23

Cash

4,000

Accounts Receivable—Harry Carr

4,000

Dec.

31

Allowance for Doubtful Accounts

24,000

Accounts Receivable—Cavey Co.

3,300

Accounts Receivable—Fogle Co.

8,100

Accounts Receivable—Lake Furniture

11,400

Accounts Receivable—Melinda Shryer

1,200

31

Bad Debt Expense

56,590

Allowance for Doubtful Accounts

56,590

Uncollectible accounts estimate

($60,000 – $3,410).

CHAPTER 8 Receivables

8–26

Prob. 8–1B (Concluded)

1. and 2.

Allowance for Doubtful Accounts

Apr.

3

12,750

Jan.

1

Balance

50,000

July

16

16,500

Jan.

19

2,660

Dec.

31

24,000

Nov.

23

4,000

Dec.

31

Unadjusted Balance

3,410

Dec.

31

Adjusting Entry

56,590

Dec.

31

Adjusted Balance

60,000

Dec.

31

Adjusting Entry 56,590

3. $2,290,000 ($2,350,000 – $60,000)

4. a. $79,000 [$15,800,000 (1/2 1%)]

b. $82,410 ($79,000 + $3,410)

c. $2,267,590 ($2,350,000 – $82,410)

CHAPTER 8 Receivables

8–27

Prob. 8–2B

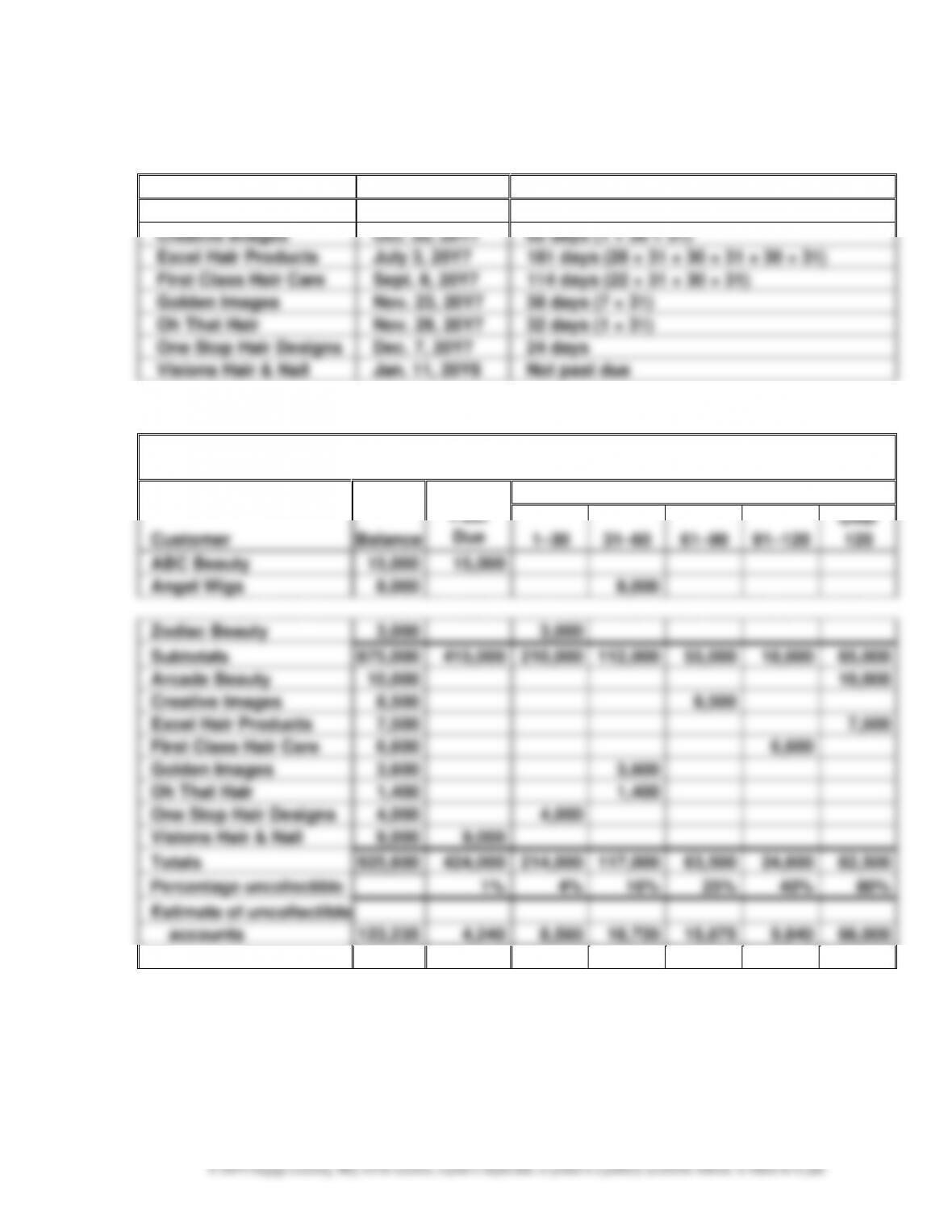

1.

Customer

Due Date

Number of Days Past Due

Arcade Beauty

Aug. 17, 20Y7

136 days (14 + 30 + 31 + 30 + 31)

Creative Images

Oct. 30, 20Y7

62 days (1 + 30 + 31)

Excel Hair Products

July 3, 20Y7

181 days (28 + 31 + 30 + 31 + 30 + 31)

First Class Hair Care

Sept. 8, 20Y7

114 days (22 + 31 + 30 + 31)

Golden Images

Nov. 23, 20Y7

38 days (7 + 31)

Oh That Hair

Nov. 29, 20Y7

32 days (1 + 31)

One Stop Hair Designs

Dec. 7, 20Y7

24 days

Visions Hair & Nail

Jan. 11, 20Y8

Not past due

2. and 3.

Aging of Receivables Schedule

December 31, 20Y7

Customer

Balance

Not

Past

Due

Days Past Due

1–30

31–60

61–90

91–120

Over

120

ABC Beauty

15,000

15,000

Angel Wigs

8,000

8,000

Zodiac Beauty

3,000

3,000

Subtotals

875,000

415,000

210,000

112,000

55,000

18,000

65,000

Arcade Beauty

10,000

10,000

Creative Images

8,500

8,500

Excel Hair Products

7,500

7,500

First Class Hair Care

6,600

6,600

Golden Images

3,600

3,600

Oh That Hair

1,400

1,400

One Stop Hair Designs

4,000

4,000

Visions Hair & Nail

9,000

9,000

Totals

925,600

424,000

214,000

117,000

63,500

24,600

82,500

Percentage uncollectible

1%

4%

16%

25%

40%

80%

Estimate of uncollectible

accounts

123,235

4,240

8,560

18,720

15,875

9,840

66,000

CHAPTER 8 Receivables

8–28

Prob. 8–2B (Concluded)

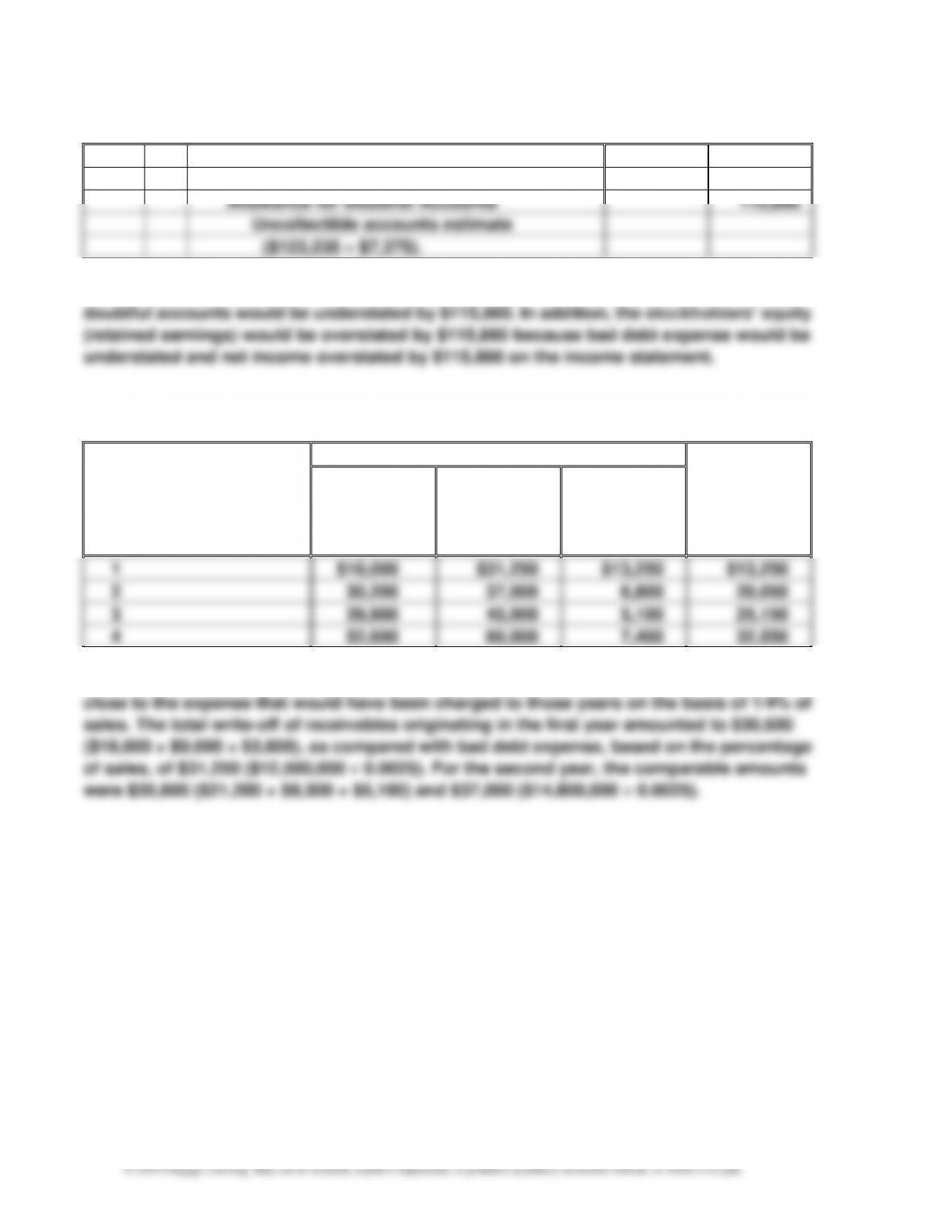

4.

20Y7

Dec.

31

Bad Debt Expense

115,860

Allowance for Doubtful Accounts

115,860

Uncollectible accounts estimate

($123,235 – $7,375).

5. On the balance sheet, assets would be overstated by $115,860 because the allowance for

Prob. 8–3B

1.

Year

Bad Debt Expense

Balance of

Allowance

Account,

End of Year

Expense

Actually

Reported

Expense

Based on

Estimate

Increase

(Decrease)

in Amount

of Expense

1

$18,000

$31,250

$13,250

$13,250

2

30,200

37,000

6,800

20,050

3

39,900

45,000

5,100

25,150

4

52,600

60,000

7,400

32,550

2. Yes. The actual write-offs of accounts originating in the first two years are reasonably

CHAPTER 8 Receivables

8–29

Prob. 8–4B

1. (a) (b)

Note

Due Date

Interest Due at Maturity

1.

Feb. 13

$110

($33,000 30 ÷ 360 4%)

2.

Apr. 23

525

($60,000 45 ÷ 360 7%)

3.

Oct. 10

600

($48,000 90 ÷ 360 5%)

4.

Nov. 6

200

($16,000 75 ÷ 360 6%)

5.

Jan. 14

480

($36,000 60 ÷ 360 8%)

6.

Feb. 8

240

($24,000 60 ÷ 360 6%)

2.

Oct.

10

Accounts Receivable

48,600

Notes Receivable

48,000

Interest Revenue

600

3.

Dec.

31

Interest Receivable

452

Interest Revenue

452

Accrued interest:

$36,000 8% 46 ÷ 360

= $368

$24,000 6% 21 ÷ 360

84

Total

$452

4.

Jan.

14

Cash

36,480

Notes Receivable

36,000

Interest Receivable

368

Interest Revenue ($36,000 8% 14 ÷ 360)

112

Feb.

8

Cash

24,240

Notes Receivable

24,000

Interest Receivable

84

Interest Revenue ($24,000 6% 39 ÷ 360)

156

CHAPTER 8 Receivables

8–30

Prob. 8–5B

Mar.

8

Notes Receivable

33,000

Accounts Receivable

33,000

31

Notes Receivable

80,000

Accounts Receivable

80,000

May

7

Cash

33,275

Notes Receivable

33,000

Interest Revenue ($33,000 5% 60 ÷ 360)

275

16

Notes Receivable

72,000

Accounts Receivable

72,000

June

11

Notes Receivable

36,000

Accounts Receivable

36,000

29

Cash

81,400

Notes Receivable

80,000

Interest Revenue ($80,000 7% 90 ÷ 360)

1,400

July

26

Cash

36,270

Notes Receivable

36,000

Interest Revenue ($36,000 6% 45 ÷ 360)

270

Aug.

4

Notes Receivable

48,000

Accounts Receivable

48,000

14

Cash

73,260

Notes Receivable

72,000

Interest Revenue ($72,000 7% 90 ÷ 360)

1,260

Dec.

2

Cash

49,440

Notes Receivable

48,000

Interest Revenue

1,440

CHAPTER 8 Receivables

8–31

Prob. 8–6B

Jan.

21

Accounts Receivable—Black Tie Co.

28,000

Sales

28,000

21

Cost of Goods Sold

16,800

Inventory

16,800

Mar.

18

Notes Receivable

28,000

Accounts Receivable—Black Tie Co.

28,000

May

17

Cash

28,280

Notes Receivable

28,000

Interest Revenue ($28,000 6% 60 ÷ 360)

280

June

15

Accounts Receivable—Pioneer Co.

17,523

Sales

17,523

15

Cost of Goods Sold

10,600

Inventory

10,600

21

Notes Receivable

18,000

Cash

18,000

25

Cash

17,523

Accounts Receivable—Pioneer Co.

17,523

July

21

Notes Receivable

18,000

Cash

120

Notes Receivable

18,000

Interest Revenue ($18,000 8% 30 ÷ 360)

120

Sept.

19

Cash

18,270

Notes Receivable

18,000

Interest Revenue ($18,000 9% 60 ÷ 360)

270

22

Accounts Receivable—Wycoff Co.

20,000

Sales

20,000

CHAPTER 8 Receivables

8–32

Prob. 8–6B (Concluded)

Sept.

22

Cost of Goods Sold

12,000

Inventory

12,000

Oct.

14

Notes Receivable

20,000

Accounts Receivable—Wycoff Co.

20,000

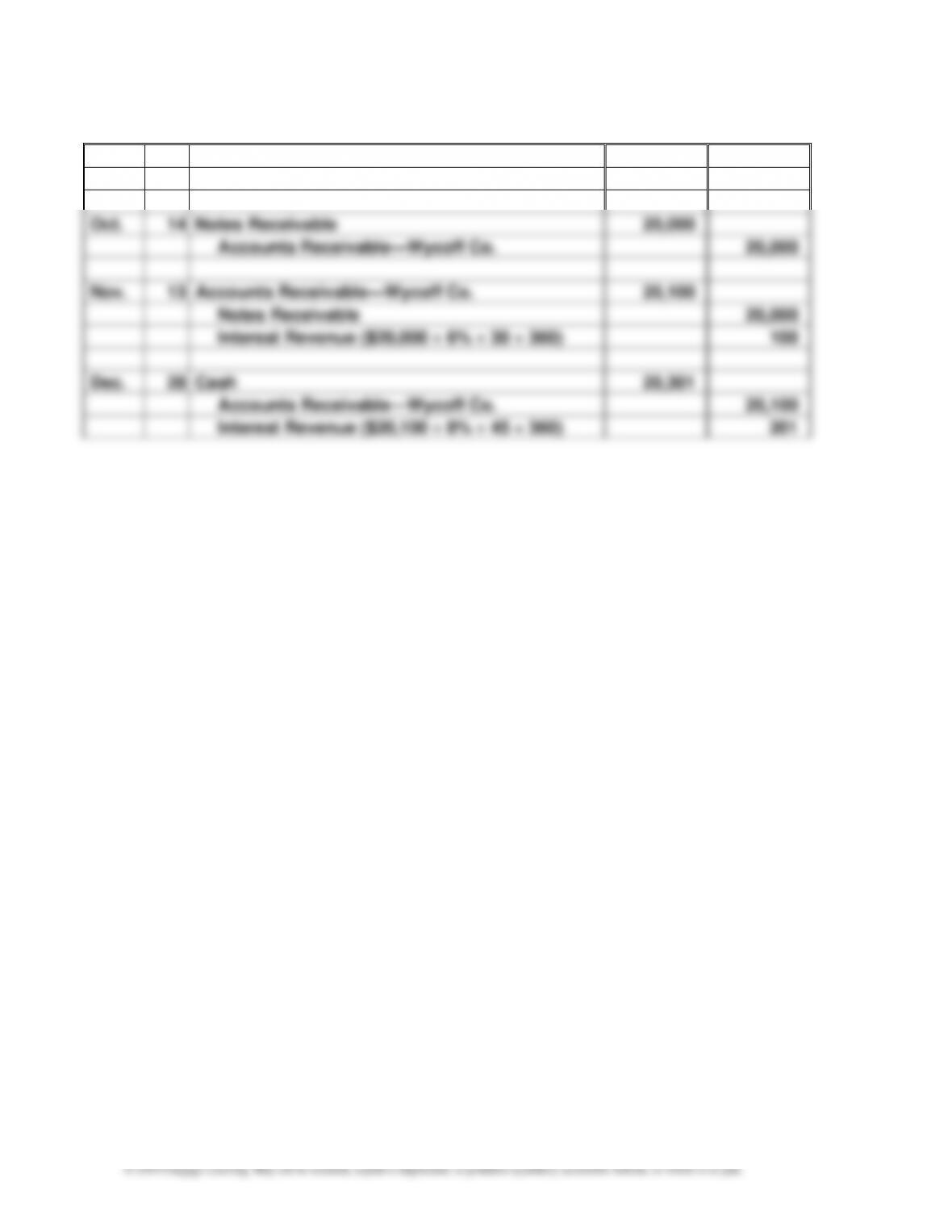

Nov.

13

Accounts Receivable—Wycoff Co.

20,100

Notes Receivable

20,000

Interest Revenue ($20,000 6% 30 360)

100

Dec.

28

Cash

20,301

Accounts Receivable—Wycoff Co.

20,100

Interest Revenue ($20,100 8% 45 360)

201

CHAPTER 8 Receivables

8–33

MAKE A DECISION

MAD 8–1

a.

Receivable AccountsAverage

Sales

Turnover Receivable Accounts =

32.4

$1,221.0

$39,528

2 $1,162) ($1,280

$39,528

:BuyBest

19.4

$6,996.5

$135,987

2 $8,339) ($5,654

$135,987

:Amazon

==

+

==

+

b.

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number =

days 11.3

$108.3

$1,221.0

365 $39,528

2 $1,162) ($1,280

:BuyBest

days 18.8

$372.6

$6,996.5

365 $135,987

2 $8,339) ($5,654

:Amazon

==

+

==

+

c. Best Buy turns accounts receivable into cash 32.4 times per year, while Amazon

d. The large difference in the ratios between these two companies suggests that there

MAD 8–2

a.

Receivable AccountsAverage

Sales

Turnover Receivable Accounts =

12.3

$586.0

$7,230

2 $517) ($655

$7,230

:2 Year

12.0

$621.5

$7,451

2$655)($588

$7,451

:1 Year

==

+

==

CHAPTER 8 Receivables

MAD 8–2 (Concluded)

b.

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number =

days 29.6

$19.8

$586.0

365 $7,230

2 $517) ($655

:2 Year

days 30.5

$20.4

$621.5

365 $7,451

2 $655) ($588

:1 Year

==

+

==

+

c. The accounts receivable turnover has increased from 12.0 to 12.3 between the two

MAD 8–3

a.

Receivable AccountsAverage

Sales

Turnover Receivable Accounts =

47.4

$256.5

$12,154

2 $261) ($252

$12,154

:2 Year

46.2

$248.0

$11,454

2 $252) ($244

$11,454

:1 Year

==

+

==

+

b.

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number =

days 7.7

$33.3

$256.5

365 $12,154

2 $261) ($252

:2 Year

days 7.9

$31.4

$248.0

365 $11,454

2 $252) ($244

:1 Year

==

+

==

+

c. The accounts receivable turnover increased from 46.2 to 47.4, indicating an

8–35

MAD 8–4

a. The average accounts receivable turnover for each company follows:

8–2 and MAD 8–3.

b. L Brands has the higher average accounts receivable turnover.

c. L Brands operates a specialty retail chain of stores that sell directly to individual

consumers. Many of these consumers (retail customers) pay with credit cards or

with cash. In contrast, Ralph Lauren sells its products to retailers, which are then

MAD 8–5

a.

Receivable AccountsAverage

Sales

Turnover Receivable Accounts =

18.6

$808.5

$15,034

2 $753) ($864

$15,034

:2 Year

16.6

$907.5

$15,069

2 $864) ($951

$15,069

:1 Year

==

+

==

+

b.

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number =

days 19.6

$41.2

$808.5

365 $15,034

2 $753) ($864

:2 Year

days 22.0

$41.3

$907.5

365 $15,069

2 $864) ($951

:1 Year

==

+

==

+

c. The accounts receivable turnover increased from 16.6 to 18.6, indicating an

CHAPTER 8 Receivables

TAKE IT FURTHER

TIF 8–1

Estimates of uncollectible accounts receivable create a unique financial reporting

challenge. Because the company does not know with certainty the amount of accounts

receivable that will be uncollectible, there is no “correct” estimate. The company must

TIF 8–2

By computing interest using a 365-day year for depository accounts (liabilities), Bev is

TIF 8–3

A sample solution based on Under Armour’s Form 10-K for the fiscal year ended

December 31, 2016, follows:

d. Under Armour did not disclose the amount of bad debt expense.

2. The company’s accounts receivable turnover has decreased between 2015 and 2016, as

shown below.

Amount in thousands

Receivable AccountsAverage

Sales

Turnover Receivable Accounts =

9.1

$528.162

$4,825.335

2 $622.685) ($433.638

$4,825.335

:2016

11.1

$356.737

$3,963.313

2 $433.638) ($279.835

$3,963.313

:2015

==

+

==

+

8–37

TIF 8–4

To: Todd Hurley, CEO

From: A+ Student

Re: Allowance Method for Uncollectible Accounts

Accounts receivable result from the sale of goods to customers on account. Because

Bad Debt Expense

XXX

Allowance for Doubtful Accounts

XXX

This adjusting entry affects both the income statement and balance sheet. On the

income statement, bad debt expense is matched against the revenues generated by

the accounts receivable. On the balance sheet, the accounts receivable balance is

CHAPTER 8 Receivables

8–38

© 2019 Cengage Learning. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TIF 8–5

1. a. b.

Year

Addition to Allowance

for Doubtful Accounts

Accounts Written

Off During Year

20Y4

$20,000

$15,000 ($20,000 – $5,000)

20Y5

22,000

18,750 ($5,000 + $22,000 – $8,250)

20Y6

24,000

22,050 ($8,250 + $24,000 – $10,200)

20Y7

25,500

21,300 ($10,200 + $25,500 – $14,400)

2. a. The estimate of 1/2 of 1% of credit sales may be too large because the

allowance for doubtful accounts has steadily increased each year. The

b. The balance of Allowance for Doubtful Accounts that should exist at December

31, 20Y7, can only be determined after all attempts have been made to collect