8–1

CHAPTER 8

RECEIVABLES

DISCUSSION QUESTIONS

2. Dan’s Hardware should use the direct write-off method because it is a small business that has a relatively

small number and volume of accounts receivable.

4. The accounts receivable and allowance for doubtful accounts may be reported at a net amount of $661,500

($673,400 – $11,900) in the “Current assets” section of the balance sheet. In this case, the amount of the

5. (1) The percentage rate used is excessive in relationship to the accounts written off as uncollectible;

hence, the balance in the allowance is excessive.

6. An estimate based on analysis of receivables provides the most accurate estimate of the current net

realizable value.

8. The interest will amount to $5,100 ($85,000 6%) only if the note is payable one year from the date it was

9. Debit Accounts Receivable for $243,600

10.

Cash

245,427

Accounts Receivable [$240,000 + ($240,000 × 6% × 90 ÷ 360)]

243,600

Interest Revenue ($243,600 × 30 ÷ 360 × 9%)

1,827

CHAPTER 8 Receivables

8–2

BASIC EXERCISES

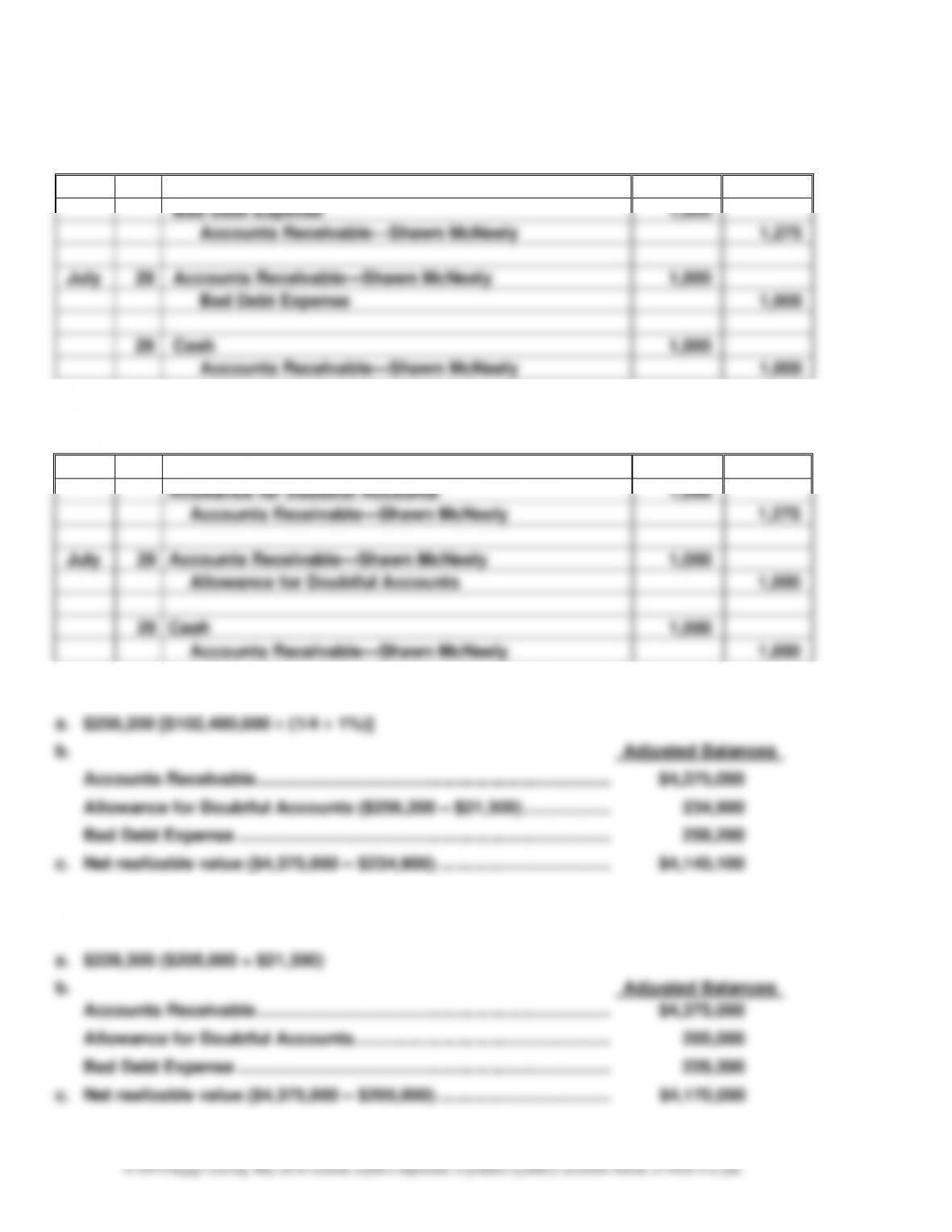

BE 8–1

Mar.

17

Cash

275

Bad Debt Expense

1,000

Accounts Receivable—Shawn McNeely

1,275

July

29

Accounts Receivable—Shawn McNeely

1,000

Bad Debt Expense

1,000

29

Cash

1,000

Accounts Receivable—Shawn McNeely

1,000

BE 8–2

Mar.

17

Cash

275

Allowance for Doubtful Accounts

1,000

Accounts Receivable—Shawn McNeely

1,275

July

29

Accounts Receivable—Shawn McNeely

1,000

Allowance for Doubtful Accounts

1,000

29

Cash

1,000

Accounts Receivable—Shawn McNeely

1,000

BE 8–3

BE 8–4

CHAPTER 8 Receivables

8–3

BE 8–5

a. The due date for the note is August 7, determined as follows:

April ………………………………………………….. 21 days (30 – 9)

BE 8–6

a. Accounts Receivable Turnover =

Receivable AccountsAverage

Sales

13.4

$590,000

$7,906,000

2 $580,000) ($600,000

$7,906,000

:20Y9

11.8

$570,000

$6,726,000

2 $600,000) ($540,000

$6,726,000

:20Y8

==

+

==

+

b. Number of Days’ sales in Receivables =

Sales Daily Average

Receivable AccountsAverage

days 27.2

$21,660.3

$590,000

365 $7,906,000

2 $580,000) ($600,000

:20Y9

days 30.9

$18,427.4

$570,000

365$6,726,000

2 600,000)($540,000

:20Y8

==

+

==

+

c. The increase in the accounts receivable turnover from 11.8 to 13.4 and the

decrease in the days’ sales in receivables from 30.9 days to 27.2 days indicate

favorable changes in the efficiency of collecting receivables.

CHAPTER 8 Receivables

8–4

EXERCISES

Ex. 8–1

Accounts receivable from the U.S. government are significantly different from

Ex. 8–2

a. MGM Resorts International: 15.7% ($89,789,000 ÷ $570,348,000)

Ex. 8–3

Jan.

19

Accounts Receivable—Dr. Kyle Norby

6,400

Sales

6,400

19

Cost of Goods Sold

3,000

Inventory

3,000

June

2

Cash

500

Bad Debt Expense

5,900

Accounts Receivable—Dr. Kyle Norby

6,400

Oct.

23

Accounts Receivable—Dr. Kyle Norby

5,900

Bad Debt Expense

5,900

23

Cash

5,900

Accounts Receivable—Dr. Kyle Norby

5,900

CHAPTER 8 Receivables

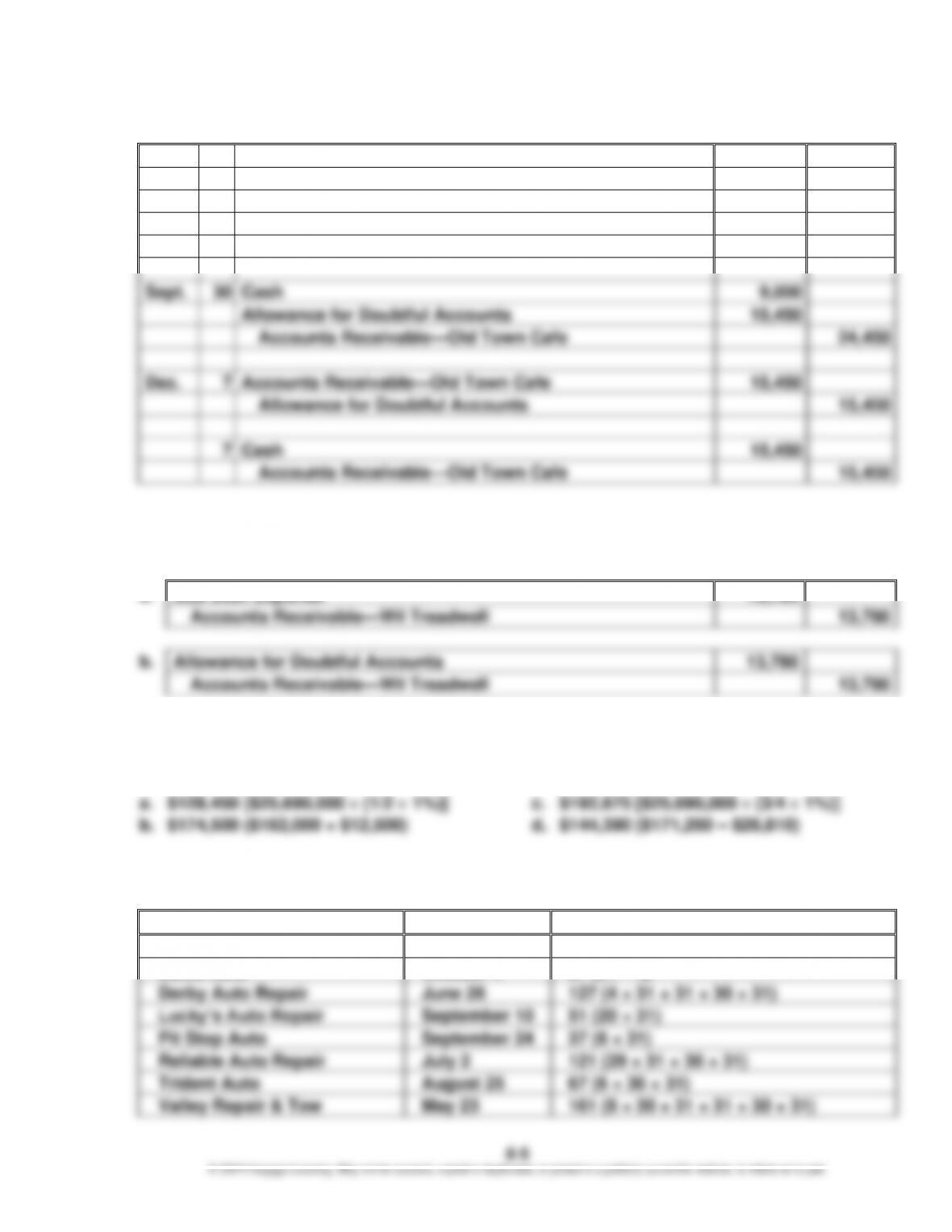

Ex. 8–4

May

24

Accounts Receivable—Old Town Cafe

24,450

Sales

24,450

24

Cost of Goods Sold

14,500

Inventory

14,500

Sept.

30

Cash

9,000

Allowance for Doubtful Accounts

15,450

Accounts Receivable—Old Town Cafe

24,450

Dec.

7

Accounts Receivable—Old Town Cafe

15,450

Allowance for Doubtful Accounts

15,450

7

Cash

15,450

Accounts Receivable—Old Town Cafe

15,450

Ex. 8–5

a.

Bad Debt Expense

13,780

Accounts Receivable—Wil Treadwell

13,780

b.

Allowance for Doubtful Accounts

13,780

Accounts Receivable—Wil Treadwell

13,780

Ex. 8–6

Ex. 8–7

Account

Due Date

Number of Days Past Due

Avalanche Auto

August 15

77 (16 + 30 + 31)

Bales Auto

October 4

27 (31 – 4)

Derby Auto Repair

June 26

127 (4 + 31 + 31 + 30 + 31)

Lucky’s Auto Repair

September 10

51 (20 + 31)

Pit Stop Auto

September 24

37 (6 + 31)

Reliable Auto Repair

July 2

121 (29 + 31 + 30 + 31)

Trident Auto

August 25

67 (6 + 30 + 31)

Valley Repair & Tow

May 23

161 (8 + 30 + 31 + 31 + 30 + 31)

CHAPTER 8 Receivables

8–6

Ex. 8–8

a.

Customer

Due Date

Number of Days Past Due

Boyd Industries

April 7

115 days (23 + 31 + 30 + 31)

Hodges Company

May 29

63 days (2 + 30 + 31)

Kent Creek Inc.

June 8

53 days (22 + 31)

Lockwood Company

August 10

Not past due

Van Epps Company

July 2

29 days (31 – 2)

b.

Aging of Receivables Schedule

July 31

Customer

Balance

Not Past

Due

Days Past Due

1–30

31–60

61–90

Over

90

Acme Industries Inc.

3,000

3,000

Alliance Company

4,500

4,500

Zollinger Company

5,000

5,000

Subtotals

1,050,000

600,000

220,000

115,000

85,000

30,000

Boyd Industries

36,000

36,000

Hodges Company

11,500

11,500

Kent Creek Inc.

6,600

6,600

Lockwood Company

7,400

7,400

Van Epps Company

13,000

13,000

Totals

1,124,500

607,400

233,000

121,600

96,500

66,000

Ex. 8–9

Balance

Not Past

Due

Days Past Due

1–30

31–60

61–90

Over

90

Total receivables

1,124,500

607,400

233,000

121,600

96,500

66,000

Percentage

uncollectible

1%

3%

12%

30%

75%

Allowance for doubtful

accounts

106,106

6,074

6,990

14,592

28,950

49,500

CHAPTER 8 Receivables

8–7

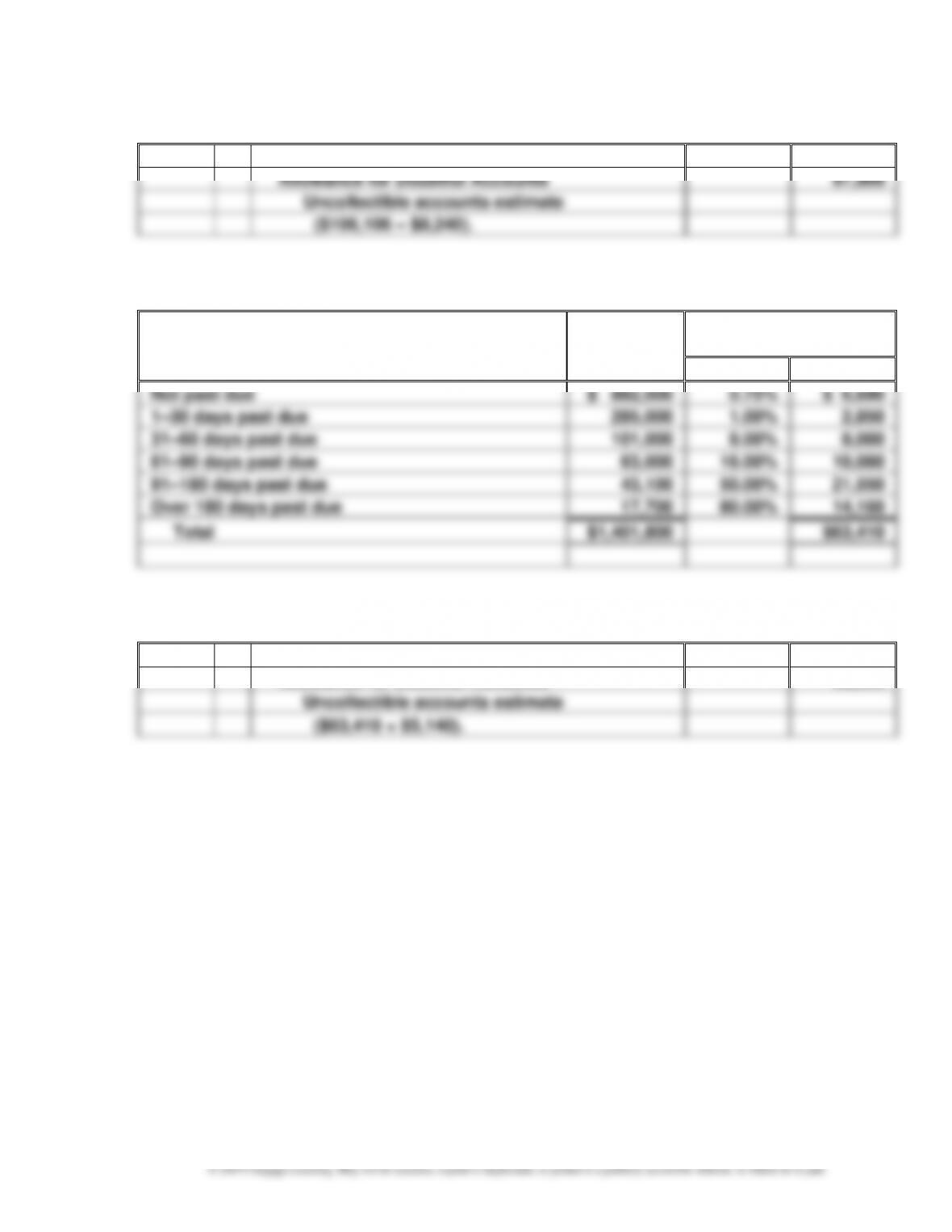

Ex. 8–10

July

31

Bad Debt Expense

97,866

Allowance for Doubtful Accounts

97,866

Uncollectible accounts estimate

($106,106 – $8,240).

Ex. 8–11

Age Interval

Balance

Estimated

Uncollectible Accounts

Percent

Amount

Not past due

$ 892,000

0.75%

$ 6,690

1–30 days past due

285,000

1.00%

2,850

31–60 days past due

101,000

8.00%

8,080

61–90 days past due

63,000

16.00%

10,080

91–180 days past due

43,100

50.00%

21,550

Over 180 days past due

17,700

80.00%

14,160

Total

$1,401,800

$63,410

Ex. 8–12

Dec.

31

Bad Debt Expense

68,550

Allowance for Doubtful Accounts

68,550

Uncollectible accounts estimate

($63,410 + $5,140).

CHAPTER 8 Receivables

8–8

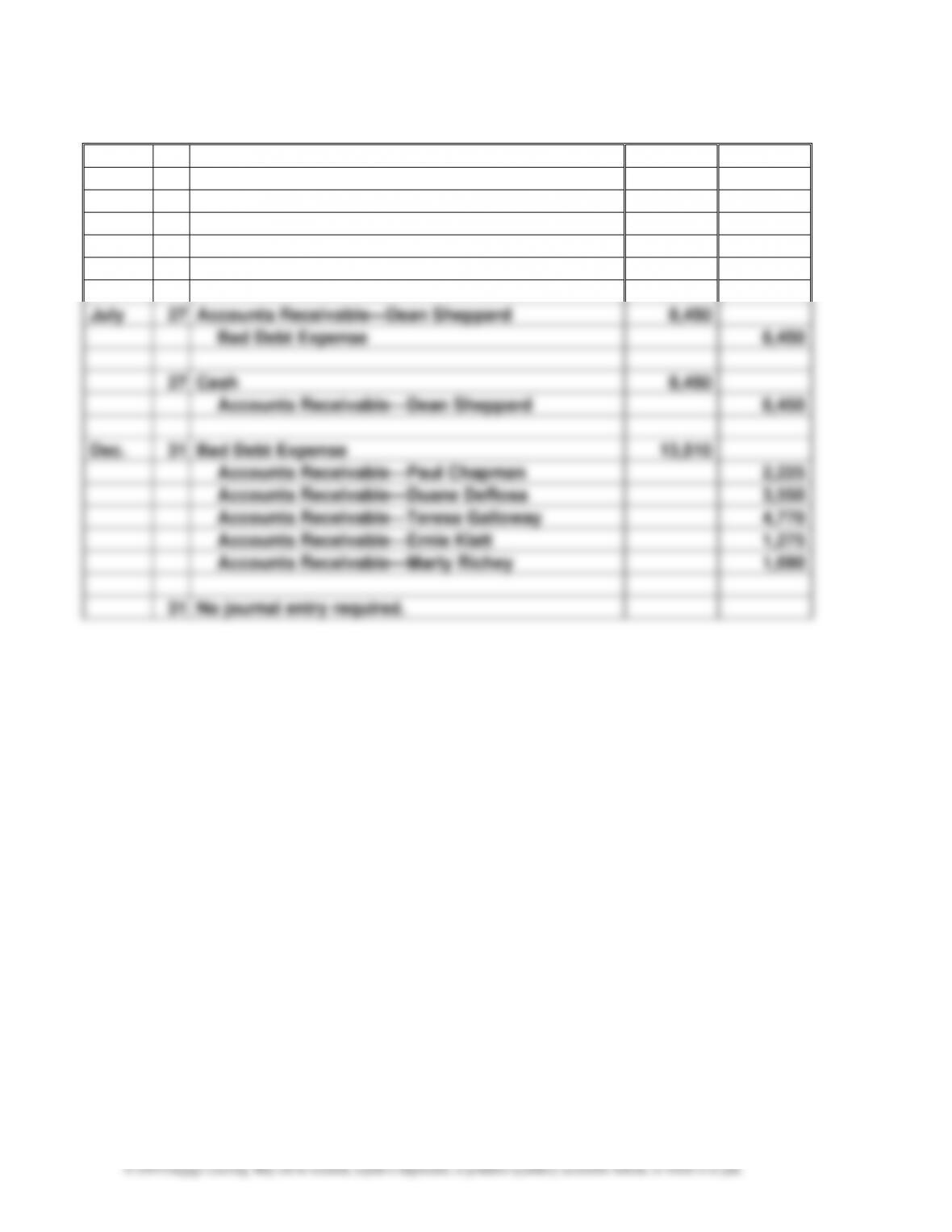

Ex. 8–13

a.

Apr.

13

Bad Debt Expense

8,450

Accounts Receivable—Dean Sheppard

8,450

May

15

Cash

500

Bad Debt Expense

6,600

Accounts Receivable—Dan Pyle

7,100

July

27

Accounts Receivable—Dean Sheppard

8,450

Bad Debt Expense

8,450

27

Cash

8,450

Accounts Receivable—Dean Sheppard

8,450

Dec.

31

Bad Debt Expense

13,510

Accounts Receivable—Paul Chapman

2,225

Accounts Receivable—Duane DeRosa

3,550

Accounts Receivable—Teresa Galloway

4,770

Accounts Receivable—Ernie Klatt

1,275

Accounts Receivable—Marty Richey

1,690

31

No journal entry required.

CHAPTER 8 Receivables

8–9

Ex. 8–13 (Concluded)

b.

Apr.

13

Allowance for Doubtful Accounts

8,450

Accounts Receivable—Dean Sheppard

8,450

May

15

Cash

500

Allowance for Doubtful Accounts

6,600

Accounts Receivable—Dan Pyle

7,100

July

27

Accounts Receivable—Dean Sheppard

8,450

Allowance for Doubtful Accounts

8,450

27

Cash

8,450

Accounts Receivable—Dean Sheppard

8,450

Dec.

31

Allowance for Doubtful Accounts

13,510

Accounts Receivable—Paul Chapman

2,225

Accounts Receivable—Duane DeRosa

3,550

Accounts Receivable—Teresa Galloway

4,770

Accounts Receivable—Ernie Klatt

1,275

Accounts Receivable—Marty Richey

1,690

31

Bad Debt Expense

28,335

Allowance for Doubtful Accounts

28,335

Uncollectible accounts estimate

($3,778,000 0.75% = $28,335).

c. Bad debt expense under:

CHAPTER 8 Receivables

8–10

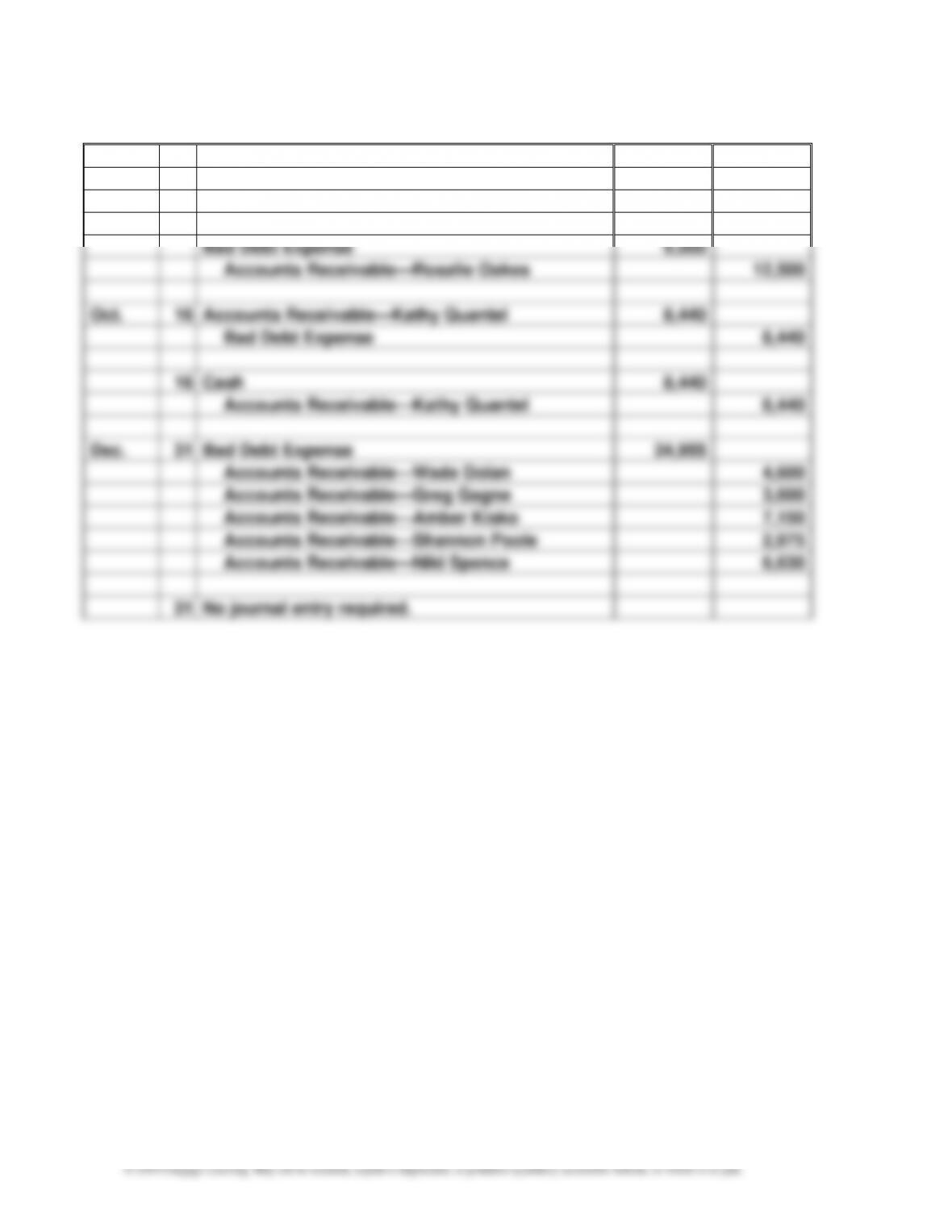

Ex. 8–14

a.

June

8

Bad Debt Expense

8,440

Accounts Receivable—Kathy Quantel

8,440

Aug.

14

Cash

3,000

Bad Debt Expense

9,500

Accounts Receivable—Rosalie Oakes

12,500

Oct.

16

Accounts Receivable—Kathy Quantel

8,440

Bad Debt Expense

8,440

16

Cash

8,440

Accounts Receivable—Kathy Quantel

8,440

Dec.

31

Bad Debt Expense

24,955

Accounts Receivable—Wade Dolan

4,600

Accounts Receivable—Greg Gagne

3,600

Accounts Receivable—Amber Kisko

7,150

Accounts Receivable—Shannon Poole

2,975

Accounts Receivable—Niki Spence

6,630

31

No journal entry required.

CHAPTER 8 Receivables

8–11

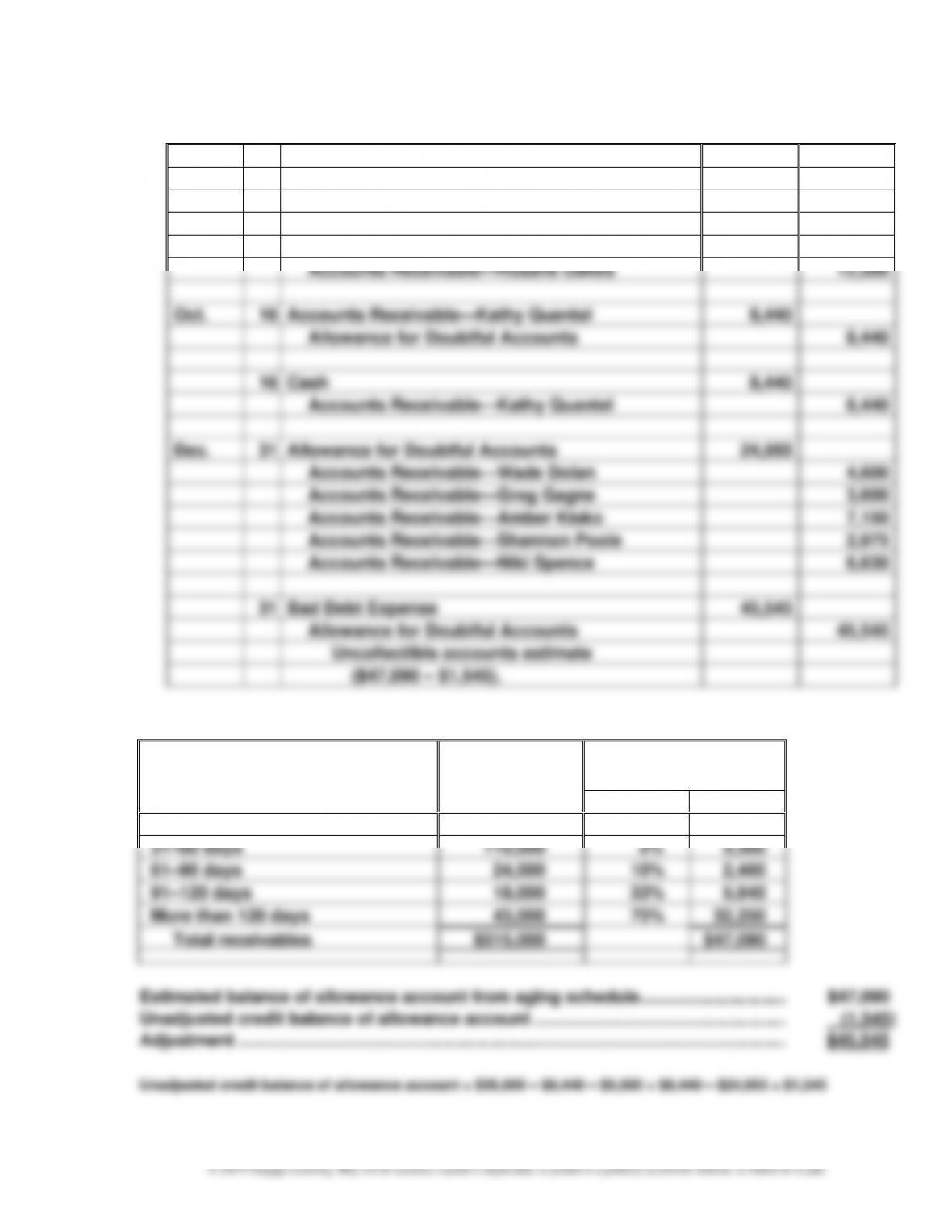

Ex. 8–14 (Continued)

b.

June

8

Allowance for Doubtful Accounts

8,440

Accounts Receivable—Kathy Quantel

8,440

Aug.

14

Cash

3,000

Allowance for Doubtful Accounts

9,500

Accounts Receivable—Rosalie Oakes

12,500

Oct.

16

Accounts Receivable—Kathy Quantel

8,440

Allowance for Doubtful Accounts

8,440

16

Cash

8,440

Accounts Receivable—Kathy Quantel

8,440

Dec.

31

Allowance for Doubtful Accounts

24,955

Accounts Receivable—Wade Dolan

4,600

Accounts Receivable—Greg Gagne

3,600

Accounts Receivable—Amber Kisko

7,150

Accounts Receivable—Shannon Poole

2,975

Accounts Receivable—Niki Spence

6,630

31

Bad Debt Expense

45,545

Allowance for Doubtful Accounts

45,545

Uncollectible accounts estimate

($47,090 – $1,545).

Computations:

Aging Class

(Number of Days

Past Due)

Receivables

Balance on

December 31

Estimated Doubtful

Accounts

Percent

Amount

0–30 days

$320,000

1%

$ 3,200

31–60 days

110,000

3%

3,300

61–90 days

24,000

10%

2,400

91–120 days

18,000

33%

5,940

More than 120 days

43,000

75%

32,250

Total receivables

$515,000

$47,090

Estimated balance of allowance account from aging schedule ………………………… $47,090

Unadjusted credit balance of allowance account ……………………………………………. (1,545)

Adjustment ………………………………………………………………………………………………….. $45,545

Unadjusted credit balance of allowance account = $36,000 – $8,440 – $9,500 + $8,440 – $24,955 = $1,545

CHAPTER 8 Receivables

8–12

Ex. 8–14 (Concluded)

c. Bad debt expense under:

Ex. 8–15

Ex. 8–16

Ex. 8–17

a.

Bad Debt Expense

30,000

Accounts Receivable—Shawn Brooke

4,650

Accounts Receivable—Eve Denton

5,180

Accounts Receivable—Art Malloy

11,050

Accounts Receivable—Cassie Yost

9,120

b.

Allowance for Doubtful Accounts

30,000

Accounts Receivable—Shawn Brooke

4,650

Accounts Receivable—Eve Denton

5,180

Accounts Receivable—Art Malloy

11,050

Accounts Receivable—Cassie Yost

9,120

Bad Debt Expense

39,375

Allowance for Doubtful Accounts

39,375

Uncollectible accounts estimate

($5,250,000 0.75% = $39,375).

c. Net income would have been $9,375 higher under the direct write-off method

CHAPTER 8 Receivables

8–13

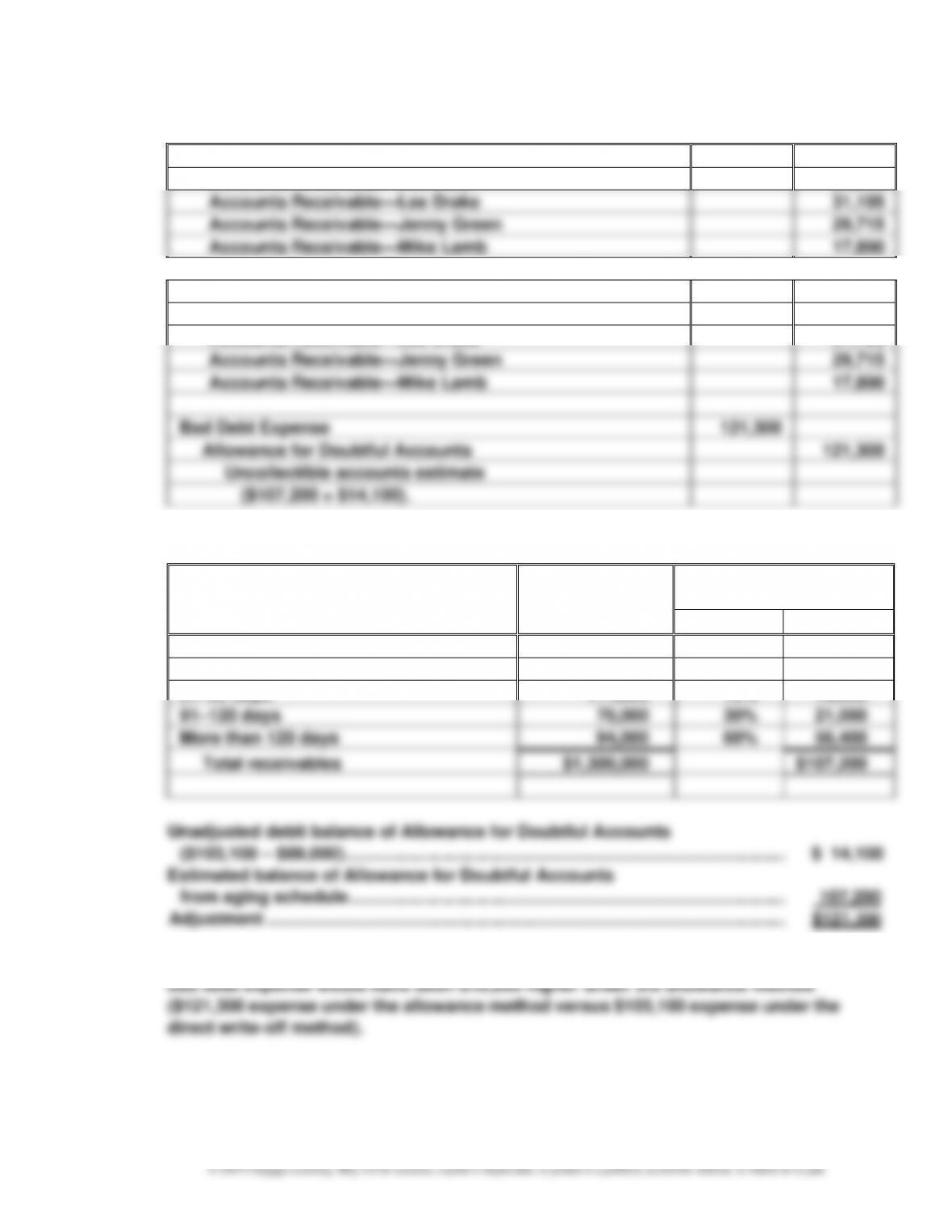

Ex. 8–18

a.

Bad Debt Expense

103,100

Accounts Receivable—Kim Abel

24,300

Accounts Receivable—Lee Drake

31,195

Accounts Receivable—Jenny Green

29,715

Accounts Receivable—Mike Lamb

17,890

b.

Allowance for Doubtful Accounts

103,100

Accounts Receivable—Kim Abel

24,300

Accounts Receivable—Lee Drake

31,195

Accounts Receivable—Jenny Green

29,715

Accounts Receivable—Mike Lamb

17,890

Bad Debt Expense

121,300

Allowance for Doubtful Accounts

121,300

Uncollectible accounts estimate

($107,200 + $14,100).

Computations:

Aging Class

(Number of Days

Past Due)

Receivables

Balance on

December 31

Estimated Doubtful

Accounts

Percent

Amount

0–30 days

$ 735,000

1%

$ 7,350

31–60 days

290,000

2%

5,800

61–90 days

111,000

15%

16,650

91–120 days

70,000

30%

21,000

More than 120 days

94,000

60%

56,400

Total receivables

$1,300,000

$107,200

Unadjusted debit balance of Allowance for Doubtful Accounts

($103,100 – $89,000) ………………………………………………………………………………. $ 14,100

Estimated balance of Allowance for Doubtful Accounts

from aging schedule ……………………………………………………………………………… 107,200

Adjustment …………………………………………………………………………………………….. $121,300

c. Net income would have been $18,200 lower under the allowance method because

CHAPTER 8 Receivables

Ex. 8–19

Due Date Interest

Ex. 8–20

a. August 18 (10 + 31 + 30 + 31 + 18)

CHAPTER 8 Receivables

8–15

Ex. 8–22

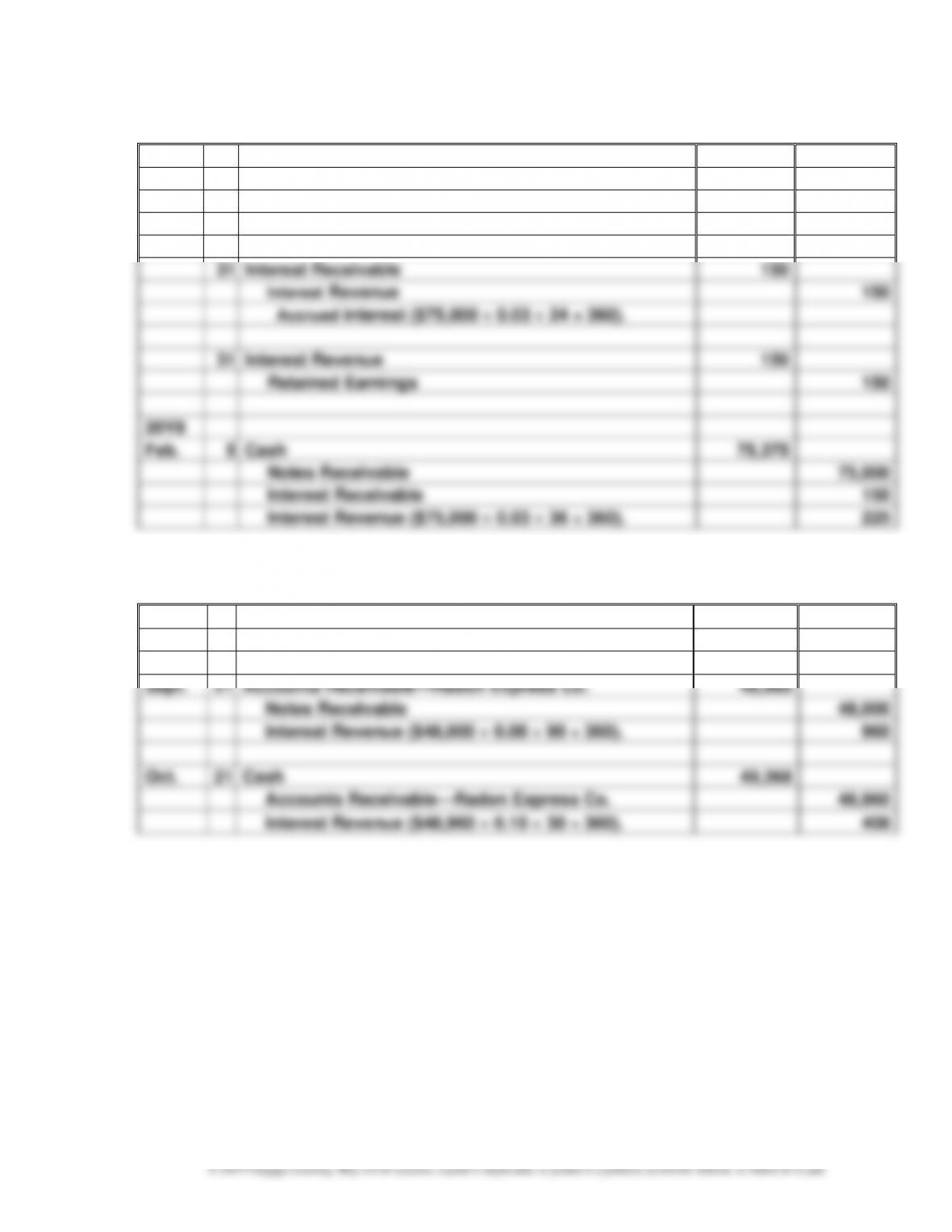

20Y7

Dec.

7

Notes Receivable

75,000

Accounts Receivable—Unitarian Clothing &

Bags Co.

75,000

31

Interest Receivable

150

Interest Revenue

150

Accrued interest ($75,000 0.03 24 ÷ 360).

31

Interest Revenue

150

Retained Earnings

150

20Y8

Feb.

5

Cash

75,375

Notes Receivable

75,000

Interest Receivable

150

Interest Revenue ($75,000 0.03 36 ÷ 360).

225

Ex. 8–23

June

23

Notes Receivable

48,000

Accounts Receivable—Radon Express Co.

48,000

Sept.

21

Accounts Receivable—Radon Express Co.

48,960

Notes Receivable

48,000

Interest Revenue ($48,000 0.08 90 ÷ 360).

960

Oct.

21

Cash

49,368

Accounts Receivable—Radon Express Co.

48,960

Interest Revenue ($48,960 0.10 30 ÷ 360).

408

CHAPTER 8 Receivables

8–16

Ex. 8–24

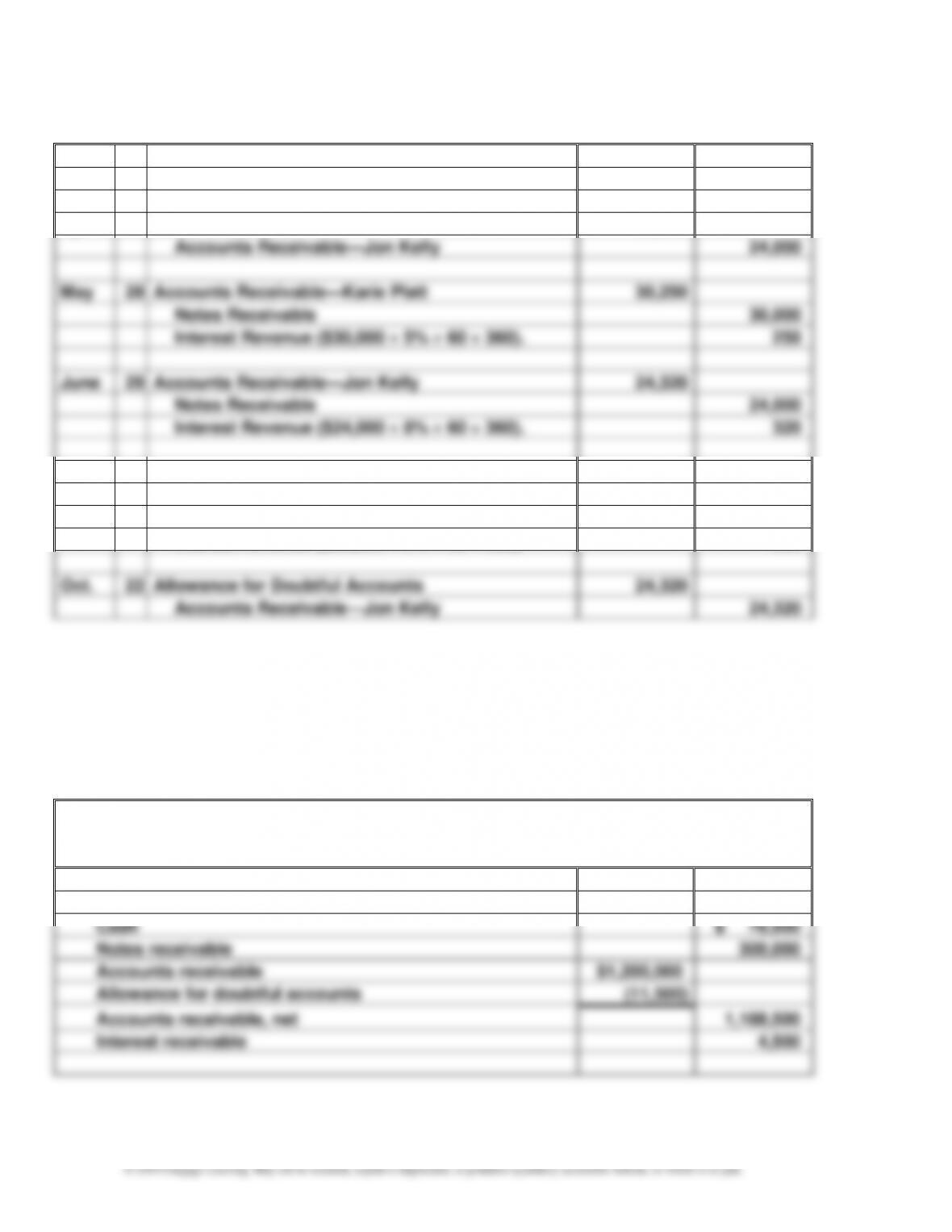

Mar.

29

Notes Receivable

30,000

Accounts Receivable—Karie Platt

30,000

Apr.

30

Notes Receivable

24,000

Accounts Receivable—Jon Kelly

24,000

May

28

Accounts Receivable—Karie Platt

30,250

Notes Receivable

30,000

Interest Revenue ($30,000 5% 60 360).

250

June

29

Accounts Receivable—Jon Kelly

24,320

Notes Receivable

24,000

Interest Revenue ($24,000 8% 60 360).

320

Aug.

26

Cash

30,855

Accounts Receivable—Karie Platt

30,250

Interest Revenue ($30,250 8% 90 360).

605

Oct.

22

Allowance for Doubtful Accounts

24,320

Accounts Receivable—Jon Kelly

24,320

Ex. 8–25

1. The interest receivable should be reported separately as a current asset. It should not be

deducted from notes receivable.

2. The allowance for doubtful accounts should be deducted from accounts receivable.

A corrected partial balance sheet would be as follows:

Napa Vino Company

Balance Sheet

December 31, 20Y6

Assets

Current assets:

Cash

$ 78,500

Notes receivable

300,000

Accounts receivable

$1,200,000

Allowance for doubtful accounts

(11,500)

Accounts receivable, net

1,188,500

Interest receivable

4,500

CHAPTER 8 Receivables

8–17

PROBLEMS

Prob. 8–1A

2.

Feb.

8

Cash

7,200

Allowance for Doubtful Accounts

10,800

Accounts Receivable—DeCoy Co.

18,000

May

27

Accounts Receivable—Seth Nelsen

7,350

Allowance for Doubtful Accounts

7,350

27

Cash

7,350

Accounts Receivable—Seth Nelsen

7,350

Aug.

13

Allowance for Doubtful Accounts

6,400

Accounts Receivable—Kat Tracks Co.

6,400

Oct.

31

Accounts Receivable—Crawford Co.

3,880

Allowance for Doubtful Accounts

3,880

31

Cash

3,880

Accounts Receivable—Crawford Co.

3,880

Dec.

31

Allowance for Doubtful Accounts

23,200

Accounts Receivable—Newbauer Co.

7,190

Accounts Receivable—Bonneville Co.

5,500

Accounts Receivable—Crow Distributors

9,400

Accounts Receivable—Fiber Optics

1,110

31

Bad Debt Expense

38,870

Allowance for Doubtful Accounts

38,870

Uncollectible accounts estimate

($35,700 + $3,170).

CHAPTER 8 Receivables

Prob. 8–1A (Concluded)

1. and 2.

Allowance for Doubtful Accounts

Feb.

8

10,800

Jan.

1

Balance

26,000

Aug.

13

6,400

May

27

7,350

Dec.

31

23,200

Oct.

31

3,880

Dec.

31

Unadjusted Balance

3,170

Dec.

31

Adjusting Entry

38,870

Dec.

31

Adjusted Balance

35,700

Dec.

Adjusting Entry

CHAPTER 8 Receivables

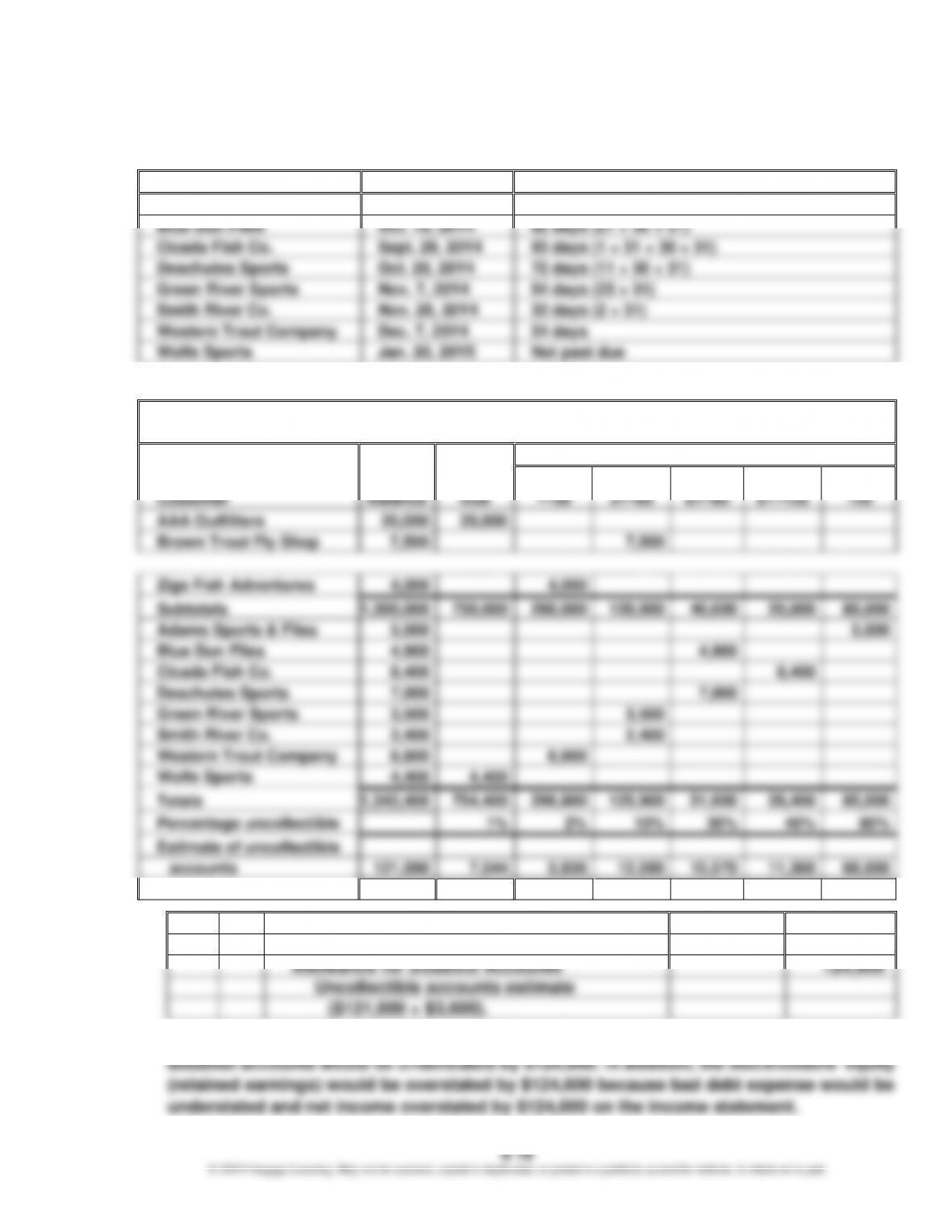

Prob. 8–2A

1.

Customer

Due Date

Number of Days Past Due

Adams Sports & Flies

May 22, 20Y4

223 days (9 + 30 + 31 + 31 + 30 + 31 + 30 + 31)

Blue Dun Flies

Oct. 10, 20Y4

82 days (21 + 30 + 31)

Cicada Fish Co.

Sept. 29, 20Y4

93 days (1 + 31 + 30 + 31)

Deschutes Sports

Oct. 20, 20Y4

72 days (11 + 30 + 31)

Green River Sports

Nov. 7, 20Y4

54 days (23 + 31)

Smith River Co.

Nov. 28, 20Y4

33 days (2 + 31)

Western Trout Company

Dec. 7, 20Y4

24 days

Wolfe Sports

Jan. 20, 20Y5

Not past due

2. and 3.

Aging of Receivables Schedule

December 31, 20Y4

Customer

Balance

Not

Past

Due

Days Past Due

1–30

31–60

61–90

91–120

Over

120

AAA Outfitters

20,000

20,000

Brown Trout Fly Shop

7,500

7,500

Zigs Fish Adventures

Subtotals

20,000

Adams Sports & Flies

5,000

Blue Dun Flies

Cicada Fish Co.

8,400

8,400

Deschutes Sports

Green River Sports

3,500

3,500

Smith River Co.

Western Trout Company

6,800

6,800

Wolfe Sports

Totals

28,400

Percentage uncollectible

Estimate of uncollectible

accounts

5,936

12,590

11,360