CHAPTER 6 Inventories

6–34

Prob. 6–5B

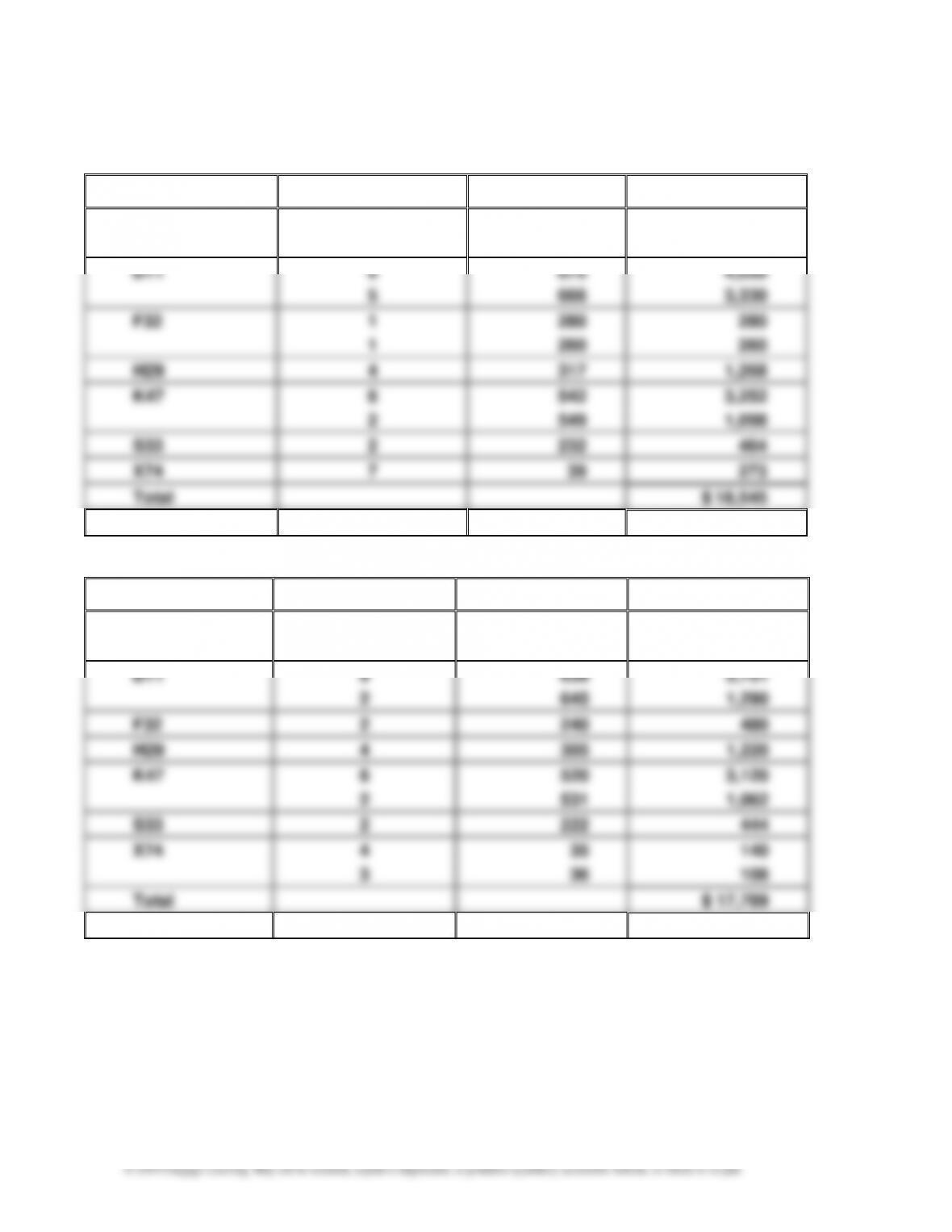

1. First-In, First-Out Method

Model

Quantity

Unit Cost

Total Cost

C55

3

$1,070

$ 3,210

1

1,060

1,060

D11

6

675

4,050

5

666

3,330

F32

1

280

280

1

260

260

H29

4

317

1,268

K47

6

542

3,252

2

549

1,098

S33

2

232

464

X74

7

39

273

Total

$ 18,545

2. Last-In, First-Out Method

Model

Quantity

Unit Cost

Total Cost

C55

3

$1,040

$ 3,120

1

1,054

1,054

D11

9

639

5,751

2

645

1,290

F32

2

240

480

H29

4

305

1,220

K47

6

520

3,120

2

531

1,062

S33

2

222

444

X74

4

35

140

3

36

108

Total

$ 17,789

CHAPTER 6 Inventories

6–35

Prob. 6–5B (Concluded)

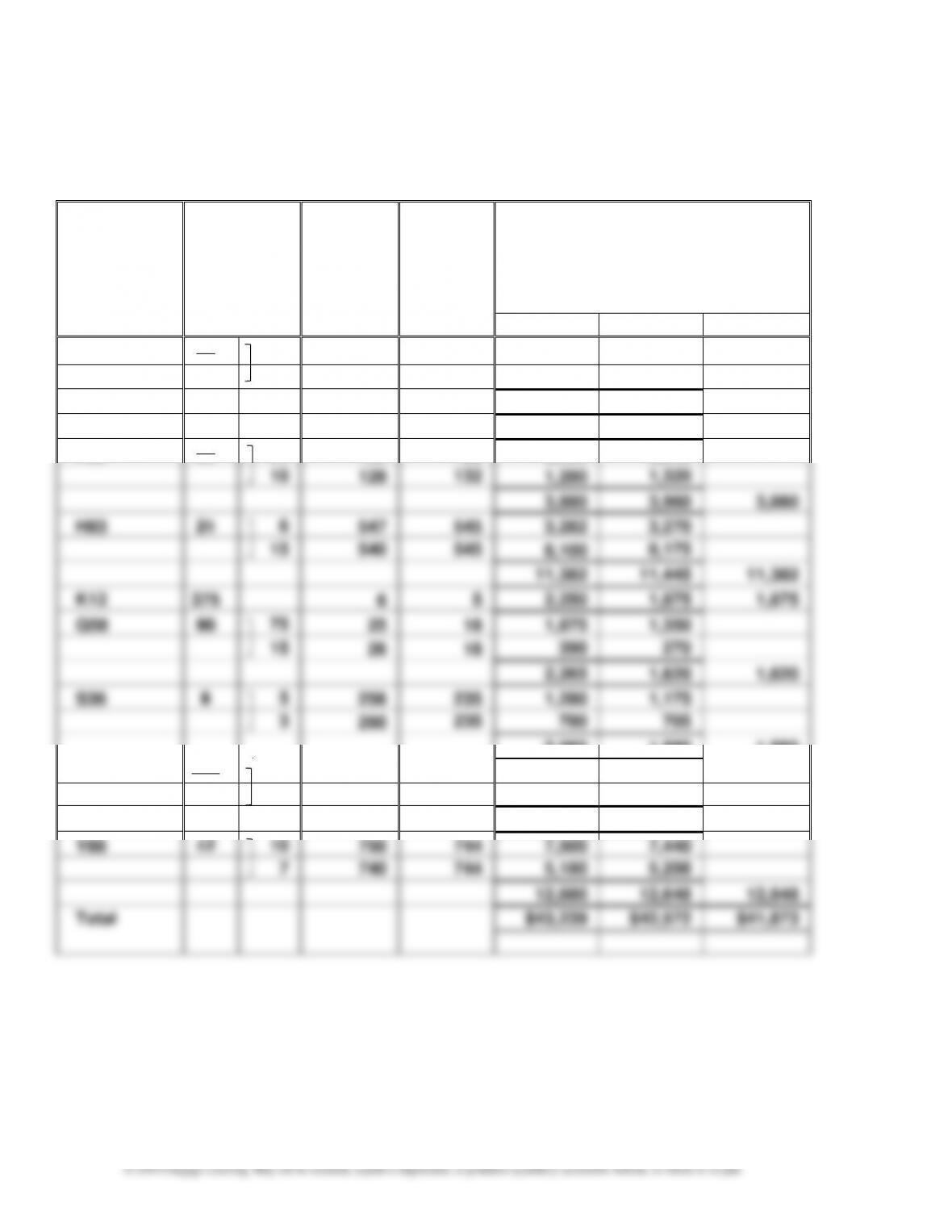

3. Weighted Average Cost Method

Model

Quantity

Unit Cost

Total Cost

C55

4

$1,056

$ 4,224

D11

11

654

7,194

F32

2

252

504

H29

4

311

1,244

K47

8

534

4,272

S33

2

227

454

X74

7

37

259

Total

$18,151

4. a. During periods of rising prices, the LIFO method will result in a lower cost of

inventory, a greater amount of cost of goods sold, and a lesser amount of net

CHAPTER 6 Inventories

6–36

Prob. 6–6B

Inventory Sheet

December 31

Description

Inventory

Quantity

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

Value)

Total

Cost

Market

LCM

A54

37

30

$ 60

$ 56

$ 1,800

$ 1,680

7

58

56

406

392

2,206

2,072

$ 2,072

C77

24

174

178

4,176

4,272

4,176

F66

30

20

130

132

2,600

2,640

10

128

132

1,280

1,320

3,880

3,960

3,880

H83

21

6

547

545

3,282

3,270

15

540

545

8,100

8,175

11,382

11,445

11,382

K12

375

6

5

2,250

1,875

1,875

Q58

90

75

25

18

1,875

1,350

15

26

18

390

270

2,265

1,620

1,620

S36

8

5

256

235

1,280

1,175

3

260

235

780

705

2,060

1,880

1,880

V97

140

100

17

20

1,700

2,000

40

16

20

640

800

2,340

2,800

2,340

Y88

17

10

750

744

7,500

7,440

7

740

744

5,180

5,208

12,680

12,648

12,648

Total

$43,239

$42,572

$41,873

CHAPTER 6 Inventories

6–37

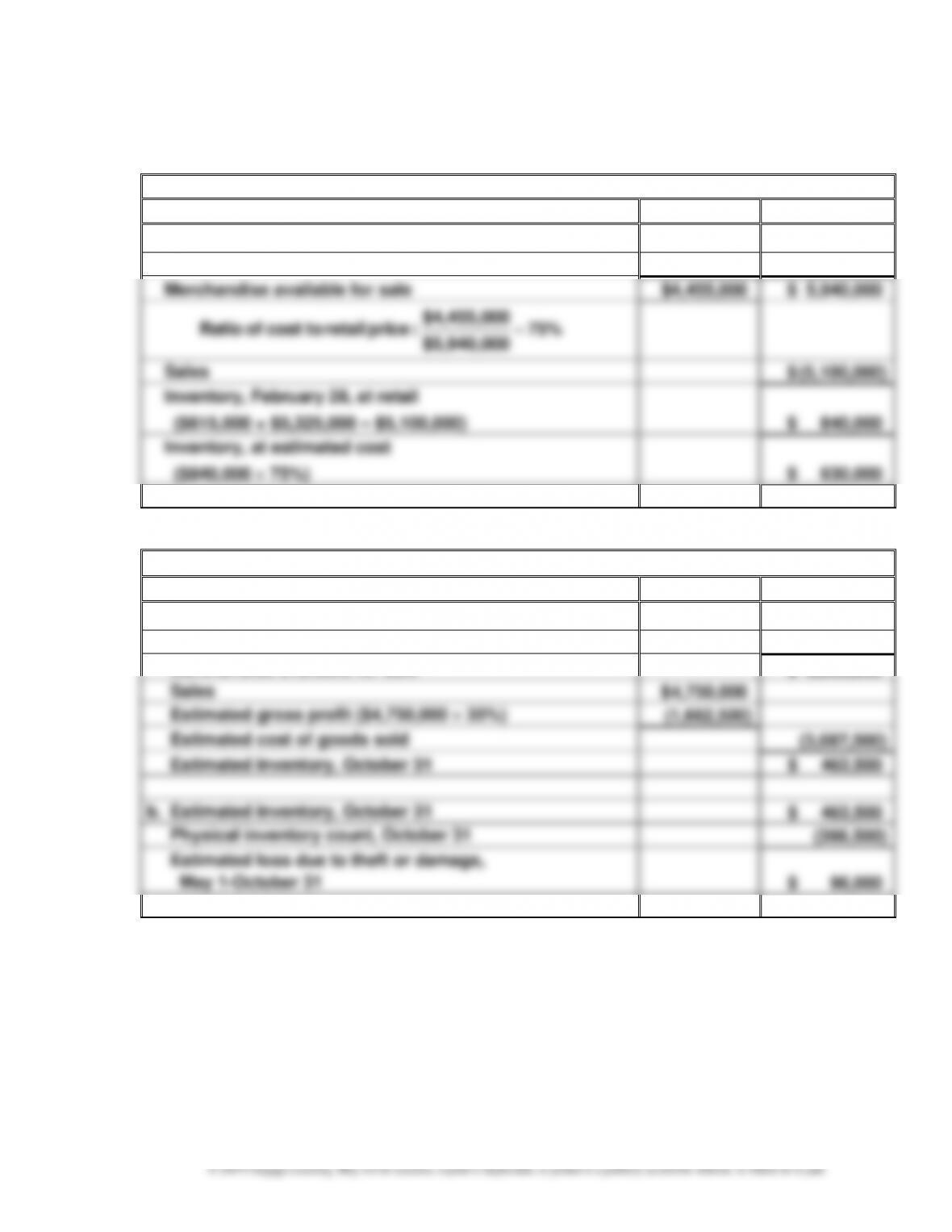

Appendix Prob. 6–7B

1.

Jaffe Co.

Cost

Retail

Inventory, February 1

$ 400,000

$ 615,000

Net purchases

4,055,000

5,325,000

Merchandise available for sale

$4,455,000

$ 5,940,000

75%

$5,940,000

$4,455,000

:price retail tocost of Ratio =

Sales

$ (5,100,000)

Inventory, February 28, at retail

($615,000 + $5,325,000 – $5,100,000)

$ 840,000

Inventory, at estimated cost

($840,000 75%)

$ 630,000

2.

Coronado Co.

Cost

a. Inventory, May 1

$ 400,000

Net purchases

3,150,000

Merchandise available for sale

$ 3,550,000

Sales

$ 4,750,000

Estimated gross profit ($4,750,000 35%)

(1,662,500)

Estimated cost of goods sold

(3,087,500)

Estimated inventory, October 31

$ 462,500

b. Estimated inventory, October 31

$ 462,500

Physical inventory count, October 31

(366,500)

Estimated loss due to theft or damage,

May 1-October 31

$ 96,000

CHAPTER 6 Inventories

6–38

MAKE A DECISION

MD 6–1

a.

Inventory Average

Sold Goods ofCost

Turnover Inventory =

7.7

$9,271

$71,651

2 $10,243) ($8,299

$71,651

:Amazon.com ==

+

6.2

$8,441.5

$51,997

2 $8,601) ($8,282

$51,997

:Target ==

+

b.

Sold Goods ofCost Daily Average

Inventory Average

Inventory in Sales Days’ of Number =

days 47.2

$196.3

$9,271

365 $71,651

2 $10,243) ($8,299

:Amazon.com ==

+

days 59.2

$142.5

$8,441.5

365 $51,997

2 $8,601) ($8,282

:Target ==

+

c. Amazon appears to more efficiently manage its inventories compared to Target. Amazon

has an inventory turnover of 7.7 and number of days’ sales in inventory of 47.2 days.

d. The difference in inventory efficiency is likely due to the difference in the companies’

merchandising strategies. Amazon sells all of its products over the Internet. Some of its

CHAPTER 6 Inventories

MD 6–2

a.

Inventory Average

Sold Goods ofCost

Turnover Inventory =

12.0

$169.7

$2,039.7

2 $175.4) ($163.9

$2,039.7

:sRestaurant Darden ==

+

31.5

$22.7

$715.5

2 $22.5) ($22.8

$715.5

:Bread Panera ==

+

b.

Sold Goods ofCost Daily Average

Inventory Average

Inventory in Sales Days’ of Number =

days 30.3

5.6

$169.7

365 $2,039.7

2 $175.4) ($163.9

:sRestaurant Darden ==

+

days 11.4

$2.0

$22.7

365 $715.5

2 $22.5) ($22.8

:Bread Panera ==

+

c. Panera appears to manage its food, beverage, and packaging inventories more

efficiently. Panera has an inventory turnover of 31.5 and number of days’ sales in

6–40

MD 6–3

a.

(In millions)

Costco

Wal-Mart

Nordstrom

Cost of goods sold

$102,901

$360,984

$9,168

Inventories:

Beginning of year

$8,908

$45,141

$1,733

End of year

$8,969

$44,469

$1,945

Average inventory:

($8,908 + $8,969) 2

$8,938.5

($45,141 + $44,469) 2

$44,805.0

($1,733 + $1,945) 2

$1,839.0

Inventory turnover:

($102,901 $8,938.5)

11.5

($360,984 $44,805.0)

8.1

($9,168 $1,839.0)

5.0

b.

(In millions)

Costco

Wal-Mart

Nordstrom

Cost of goods sold

$102,901

$360,984

$9,168

Average daily cost of goods sold:

$102,901 365 days

$281.9

$360,984 365 days

$989.0

$9,168 365 days

$25.1

Average inventory:

($8,908 + $8,969) 2

$8,938.5

($45,141 + $44,469) 2

$44,805.0

($1,733 + $1,945) 2

$1,839.0

Number of days’ sales in inventory:

$8,938.5 $281.9

31.7 days

$44,805.0 $989

45.3 days

$1,839.0 $25.1

73.3 days

c. Both the inventory turnover ratio and the number of days’ sales in inventory reflect the

merchandising approaches of the three companies.

CHAPTER 6 Inventories

6–41

MAD 6–3 (Concluded)

Nordstrom is a high-end fashion retailer. It provides a wide assortment of specialty and

MAD 6–4

a.

Monster

Brown-

(In millions)

Beverage

Forman

Cost of goods sold

$1,090

$945

Inventories:

Beginning of year

$175

$953

End of year

$156

$1,054

Average inventory:

($175+ $156) 2

$165.5

($953 + $1,054) 2

$1,003.5

Inventory turnover:

($1,090 $165.5)

6.6

($945 $1,003.5)

0.9

b.

Monster

Brown-

(In millions)

Beverage

Forman

Cost of goods sold

$1,090

$945

Average daily cost of goods sold:

$1,090 365 days

$3.0

$945 365 days

$2.6

Average inventory:

($175+ $156) 2

$165.5

($953 + $1,054) 2

$1,003.5

Number of days’ sales in inventory:

$165.5 $3.0

55.2 days

$1,003.5 $2.6

386.0 days

c. Both companies produce beverage products. However, Monster Beverage produces and

CHAPTER 6 Inventories

6–42

TAKE IT FURTHER

TIF 6–1

1. In the short run, Sizemo Electroniks may benefit slightly from the inflated inventory

values and higher earnings. However, at some point in the future, the inventory will either

2. The users of Sizemo’s financial statements are harmed by this decision, as it does not

result in financial statements that fairly present the company’s financial results.

3. No. Tina is acting unethically by instructing Jay to intentionally ignore a lower- of–cost–

or–market adjustment. As Jay’s supervisor, Tina has a responsibility to ensure her

TIF 6–2

Because the title to merchandise shipped FOB shipping point passes to the buyer

CHAPTER 6 Inventories

TIF 6–3

A sample solution based on Best Buy’s Form 10-K for the fiscal year ended May 31, 2016,

follows:

1. a. Inventory costs primarily consist of product cost from the company’s suppliers as

well as inbound freight and certain vendor allowances that are not a reimbursement

2. The company’s inventory turnover has remained the same between 2015 and 2016.

2016 2015

Cost of goods sold ………………………………………….. $30,334 $31,292

6–44

TIF 6–4

Memo

To: Ms. Connie Kilmer

President, Golden Eagle Company

From: A+ Student

Re: Comparison of LIFO and FIFO inventory methods

LIFO and FIFO are alternative methods of applying unit cost to the units that are sold during

the year and those units that remain in ending inventory at the end of the year. The LIFO

method is often viewed as the best basis for reflecting income from operations. This is

because the LIFO method matches the most current cost of merchandise purchases against

CHAPTER 6 Inventories

TIF 6–4 (Concluded)

Supporting computations:

The cost of ending inventory under the last-in, first-out and first-in, first-out methods is as

follows:

Last-in, first-out method:

The cost of goods sold and gross profit under each method are as follows:

FIFO

LIFO

Sales ……………………………………………………………………….

Cost of goods sold (see below) …………………………………

Gross profit

Cost of goods sold calculation:

Cost of goods available for sale ……………………………………………..

Ending inventory ……………………………………………………………………

Cost of goods sold …………………………………………………………………

$10,000,000

6,974,400

$ 3,025,600

$8,148,000

1,173,600

$6,974,400

$10,000,000

6,711,600

$ 3,288,400

$8,148,000

1,436,400

$6,711,600