6–1

CHAPTER 6

INVENTORIES

DISCUSSION QUESTIONS

1. The receiving report should be reconciled to the initial purchase order and the vendor’s invoice before

2. A physical inventory should be taken periodically to test the accuracy of the perpetual records. In

addition, a physical inventory will identify inventory shortages or shrinkage.

6. LIFO. In periods of rising prices, the use of LIFO will result in the lowest net income and thus the

lowest income tax expense.

8. a. Gross profit for the year was understated by $14,750.

CHAPTER 6 Inventories

BASIC EXERCISES

BE 6–1

Gross Profit

April

Ending Inventory

April 30

a.

First-in, first-out (FIFO)

$200 ($300 – $100)

$260 ($120 + $140)

b.

Last-in, first-out (LIFO)

$160 ($300 – $140)

$220 ($100 + $120)

c.

Weighted average cost

$180 ($300 – $120)

$240 ($120 2)

BE 6–2

a. Cost of goods sold (October 24):

40

units @ $30

$1,200

110

units @ $33

3,630

150

$4,830

b. Inventory, October 31: $2,310 = 70 units $33

BE 6–3

a. Cost of goods sold (July 27):

6–3

BE 6–5

a. First-in, first-out (FIFO) method: $14,700 = (60 units $200) + (15 units $180)

BE 6–6

Commodity

Inventory

Quantity

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

Value)

Total

Cost

Market

LCM

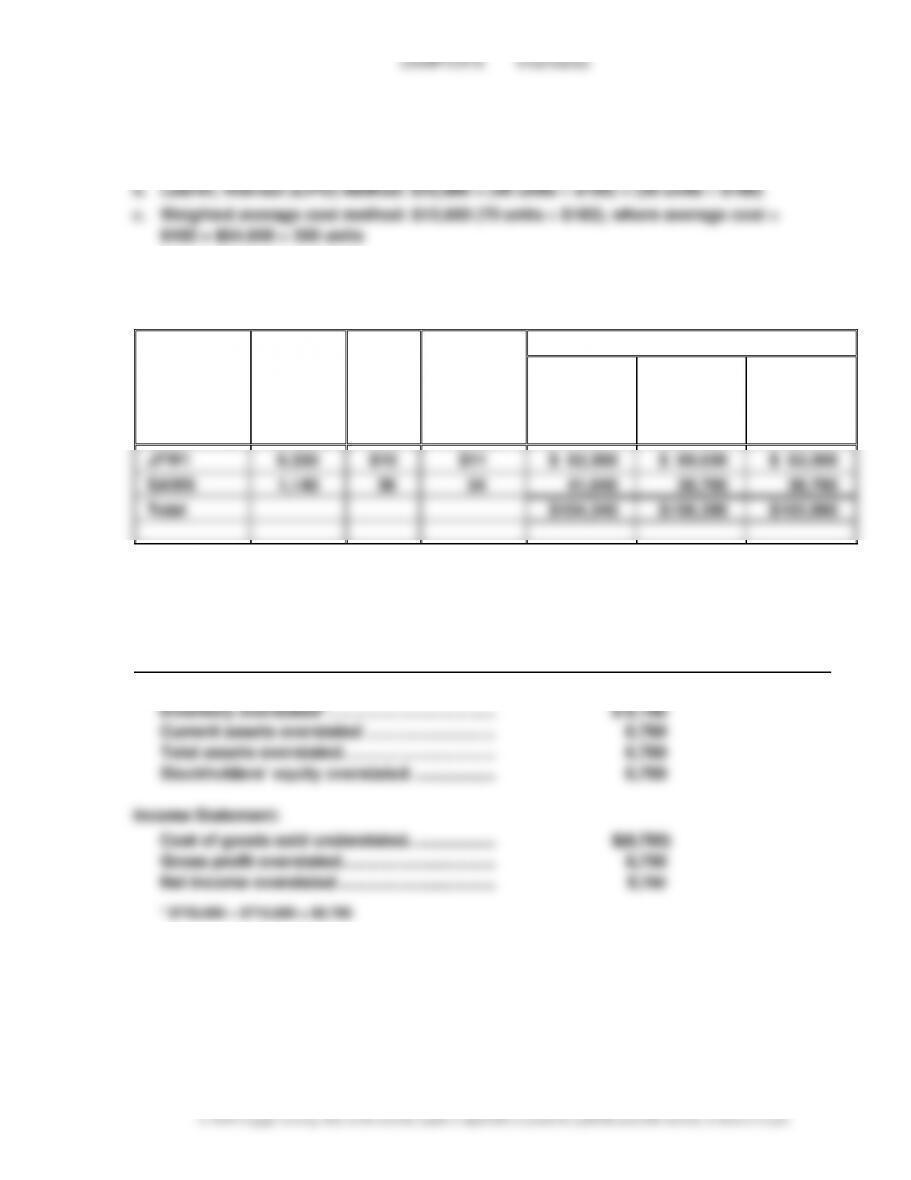

JFW1

6,330

$10

$11

$ 63,300

$ 69,630

$ 63,300

SAW9

1,140

36

34

41,040

38,760

38,760

Total

$104,340

$108,390

$102,060

BE 6–7

Amount of Misstatement

Overstatement (Understatement)

Balance Sheet:

CHAPTER 6 Inventories

6–4

BE 6–8

a.

Inventory Turnover

20Y7

20Y6

Cost of goods sold

$3,864,000

$4,001,500

Inventories:

Beginning of year

$770,000

$740,000

End of year

$840,000

$770,000

Average inventory

$805,000

$755,000

[($770,000 + $840,000)] ÷ 2

[($740,000 + $770,000)] ÷ 2

Inventory turnover

4.8

5.3

($3,864,000 ÷ $805,000)

($4,001,500 ÷ $755,000)

b.

Number of Days’ Sales

in Inventory

20Y7

20Y6

Cost of goods sold

$3,864,000

$4,001,500

Average daily cost of

goods sold

$10,586.3

$10,963.0

($3,864,000 ÷ 365 days)

($4,001,500 ÷ 365 days)

Average inventory

$805,000

$755,000

[($770,000 + $840,000)] ÷ 2

[($740,000 + $770,000)] ÷ 2

Number of days’ sales

in inventory

76.0 days

68.9 days

($805,000 ÷ $10,586.3)

($755,000 ÷ $10,963.0)

c. The decrease in inventory turnover from 5.3 to 4.8 and the increase in the number of

days’ sales in inventory from 68.9 to 76.0 days indicate unfavorable changes in

managing inventory.

CHAPTER 6 Inventories

6–5

EXERCISES

Ex. 6–1

Switching to a perpetual inventory system will strengthen Triple Creek Hardware’s internal

Ex. 6–2

a. Appropriate. The inventory tags will protect the inventory from customer theft.

CHAPTER 6 Inventories

6–6

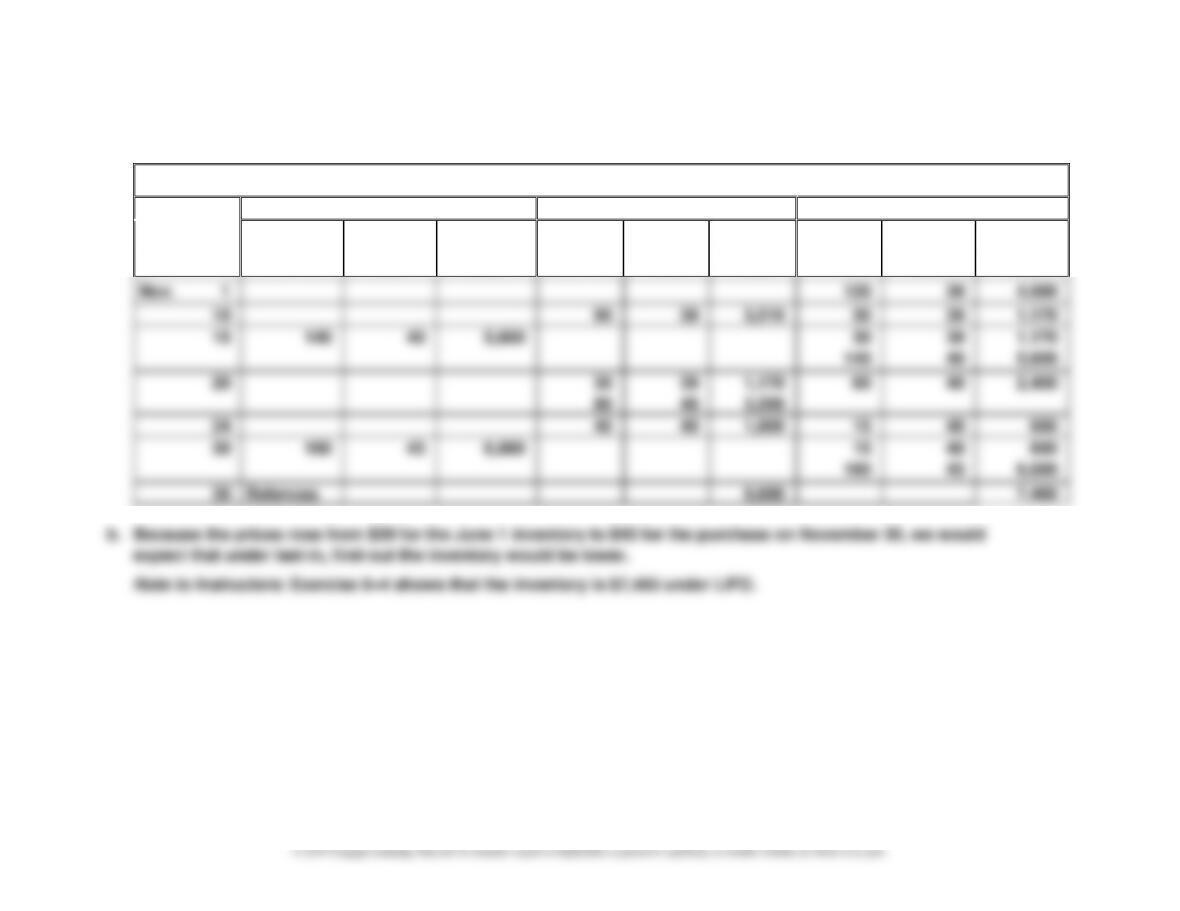

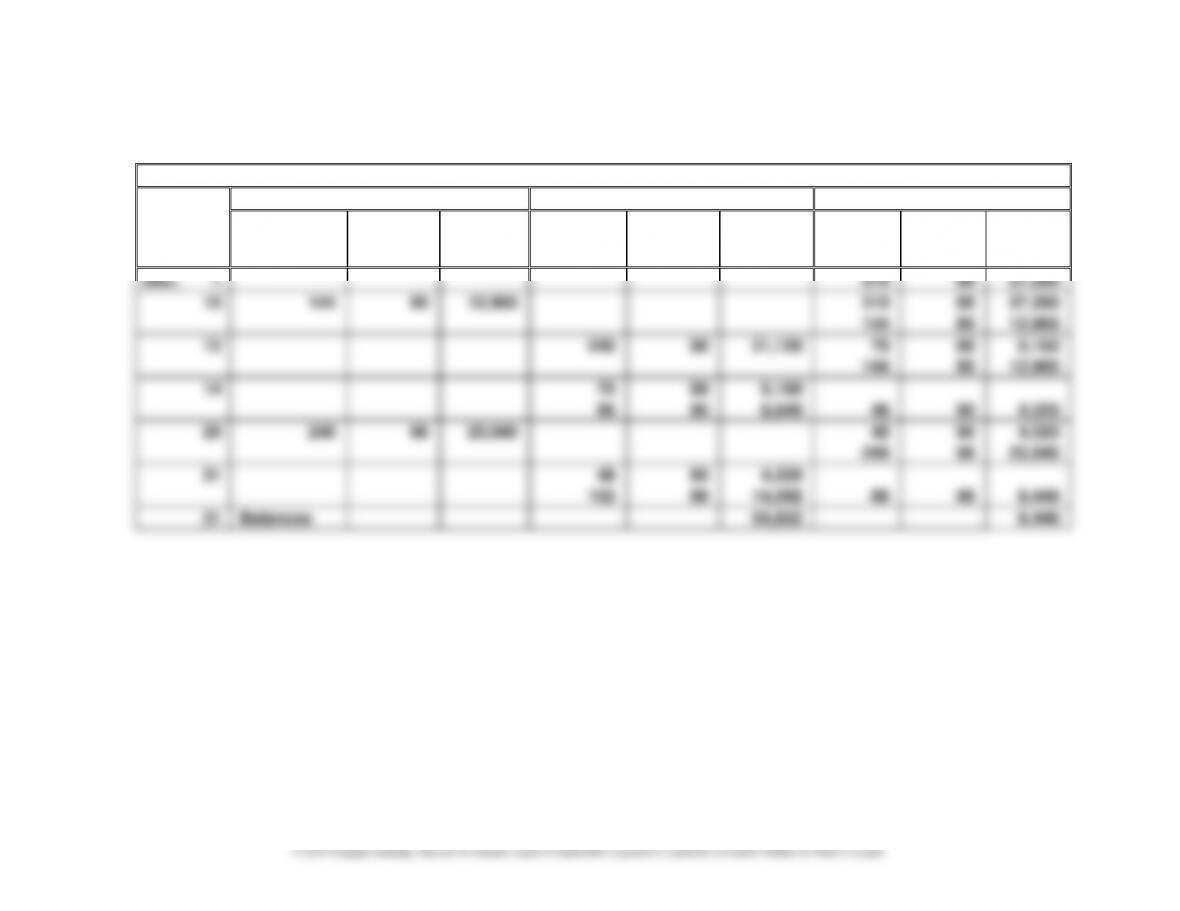

Ex. 6–3

a.

DVD Players

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Nov. 1

120

39

4,680

10

90

39

3,510

30

39

1,170

15

140

40

5,600

30

140

39

40

1,170

5,600

20

30

39

1,170

60

40

2,400

80

40

3,200

24

45

40

1,800

15

40

600

30

160

43

6,880

15

160

40

43

600

6,880

30

Balances

9,680

7,480

b. Because the prices rose from $39 for the June 1 inventory to $43 for the purchase on November 30, we would

expect that under last-in, first-out the inventory would be lower.

Note to Instructors: Exercise 6–4 shows that the inventory is $7,465 under LIFO.

CHAPTER 6 Inventories

6–7

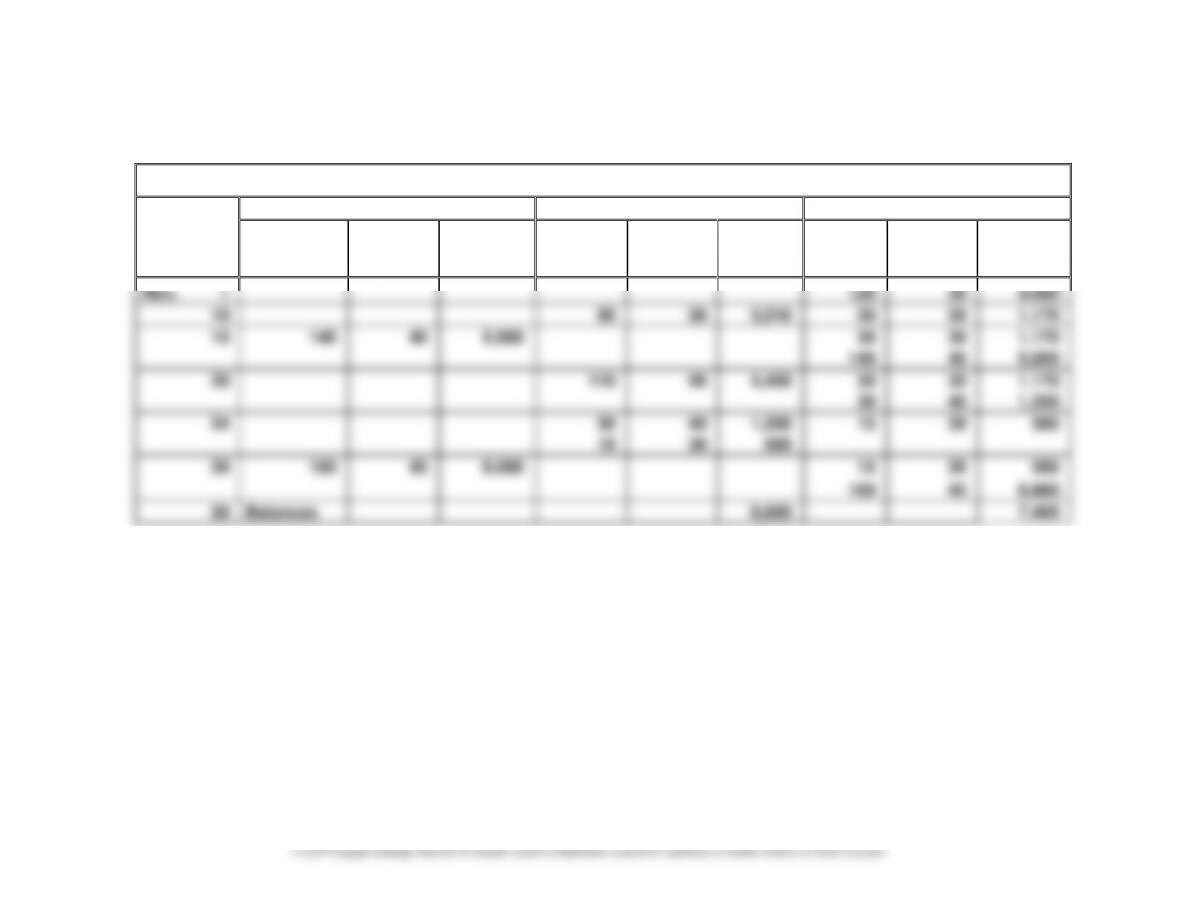

Ex. 6–4

DVD Players

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Nov. 1

120

39

4,680

10

90

39

3,510

30

39

1,170

15

140

40

5,600

30

39

1,170

140

40

5,600

20

110

40

4,400

30

39

1,170

30

40

1,200

24

30

40

1,200

15

39

585

15

39

585

30

160

43

6,880

15

39

585

160

43

6,880

30

Balances

9,695

7,465

CHAPTER 6 Inventories

6–8

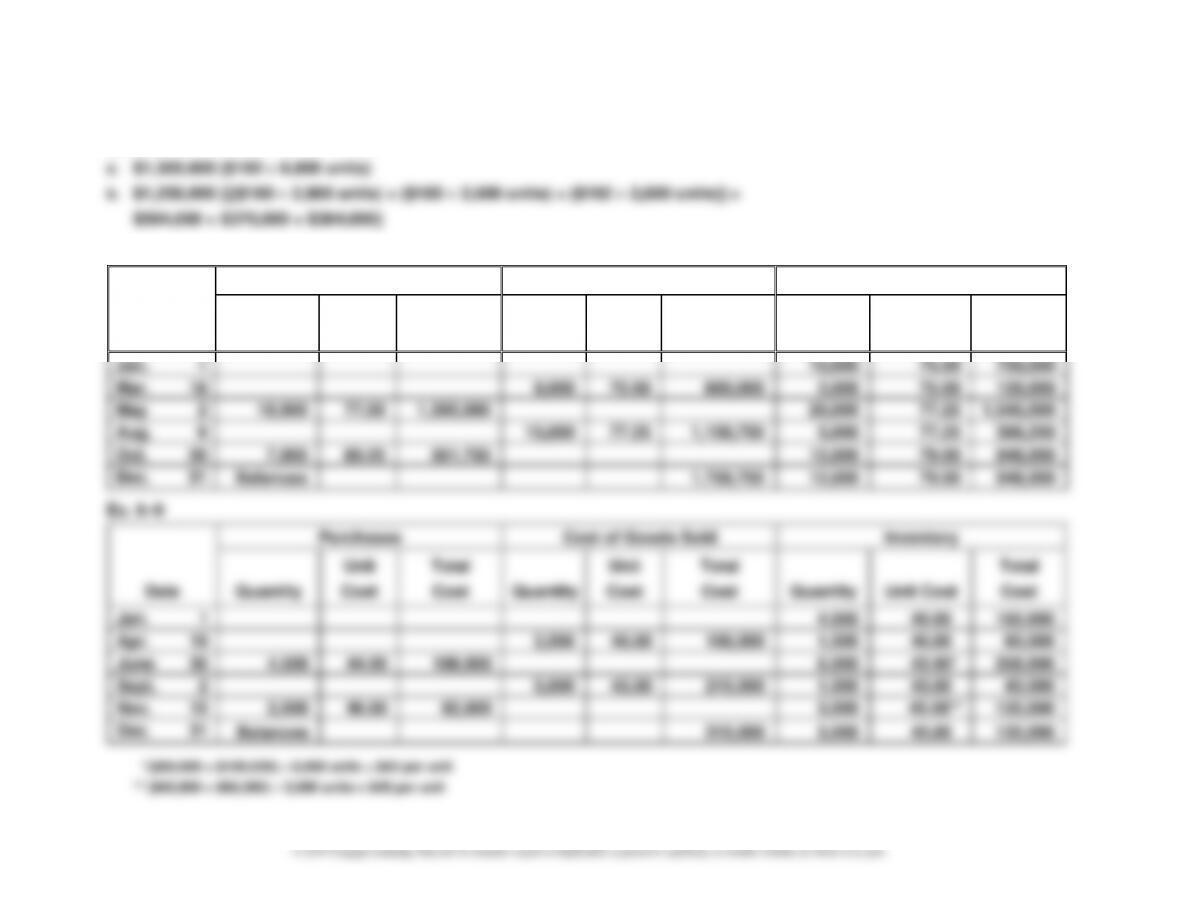

Ex. 6–5

a.

Prepaid Cell Phones

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Dec. 1

310

88

27,280

10

144

90

12,960

310

88

27,280

144

90

12,960

12

144

90

12,960

214

88

18,832

96

88

8,448

14

166

88

14,608

48

88

4,224

20

240

96

23,040

48

88

4,224

240

96

23,040

31

200

96

19,200

48

88

4,224

40

96

3,840

31

Balances

55,216

8,064

CHAPTER 6 Inventories

6–9

Ex. 6–6

Prepaid Cell Phones

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Dec. 1

310

88

27,280

10

144

90

12,960

310

88

27,280

144

90

12,960

12

240

88

21,120

70

88

6,160

144

90

12,960

14

70

88

6,160

96

90

8,640

48

90

4,320

20

240

96

23,040

48

90

4,320

240

96

23,040

31

48

90

4,320

152

96

14,592

88

96

8,448

31

Balances

54,832

8,448

CHAPTER 6 Inventories

6–10

Ex. 6–7

Ex. 6–8

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit Cost

Total

Cost

Jan. 1

10,000

75.00

750,000

Mar. 18

8,000

75.00

600,000

2,000

75.00

150,000

May 2

18,000

77.50

1,395,000

20,000

77.25

1,545,000

Aug. 9

15,000

77.25

1,158,750

5,000

77.25

386,250

Oct. 20

7,000

80.25

561,750

12,000

79.00

948,000

Dec. 31

Balances

1,758,750

12,000

79.00

948,000

Ex. 6–9

Purchases

Cost of Goods Sold

Inventory

Date

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit Cost

Total

Cost

Jan. 1

4,000

40.00

160,000

Apr. 19

2,500

40.00

100,000

1,500

40.00

60,000

June 30

4,500

44.00

198,000

6,000

43.00*

258,000

Sept. 2

5,000

43.00

215,000

1,000

43.00

43,000

Nov. 15

2,000

46.00

92,000

3,000

45.00**

135,000

Dec. 31

Balances

315,000

3,000

45.00

135,000

* ($60,000 + $198,000) 6,000 units = $43 per unit

** ($43,000 + $92,000) 3,000 units = $45 per unit

CHAPTER 6 Inventories

6–11

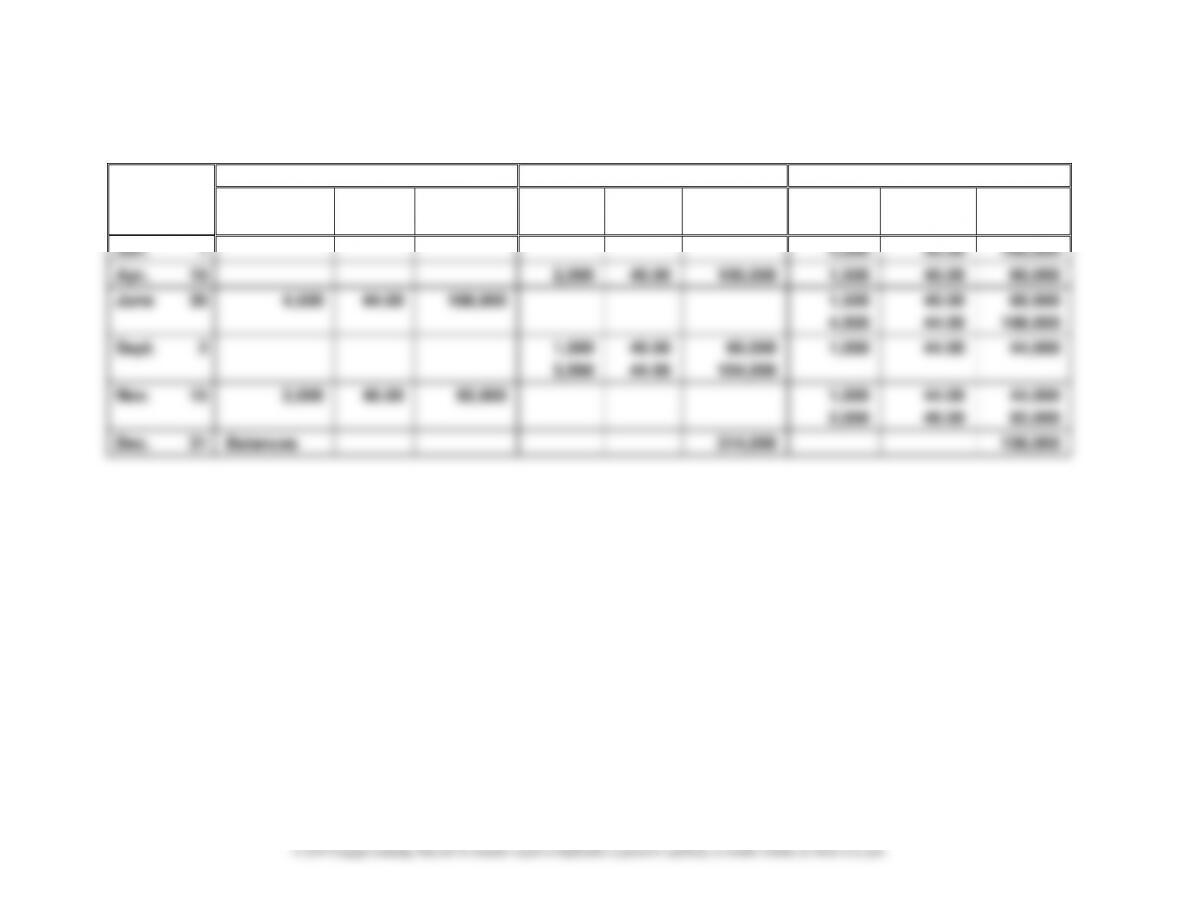

Ex. 6–10

Date

Purchases

Cost of Goods Sold

Inventory

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Jan. 1

4,000

40.00

160,000

Apr. 19

2,500

40.00

100,000

1,500

40.00

60,000

June 30

4,500

44.00

198,000

1,500

4,500

40.00

44.00

60,000

198,000

Sept. 2

1,500

3,500

40.00

44.00

60,000

154,000

1,000

44.00

44,000

Nov. 15

2,000

46.00

92,000

1,000

2,000

44.00

46.00

44,000

92,000

Dec. 31

Balances

314,000

136,000

CHAPTER 6 Inventories

6–12

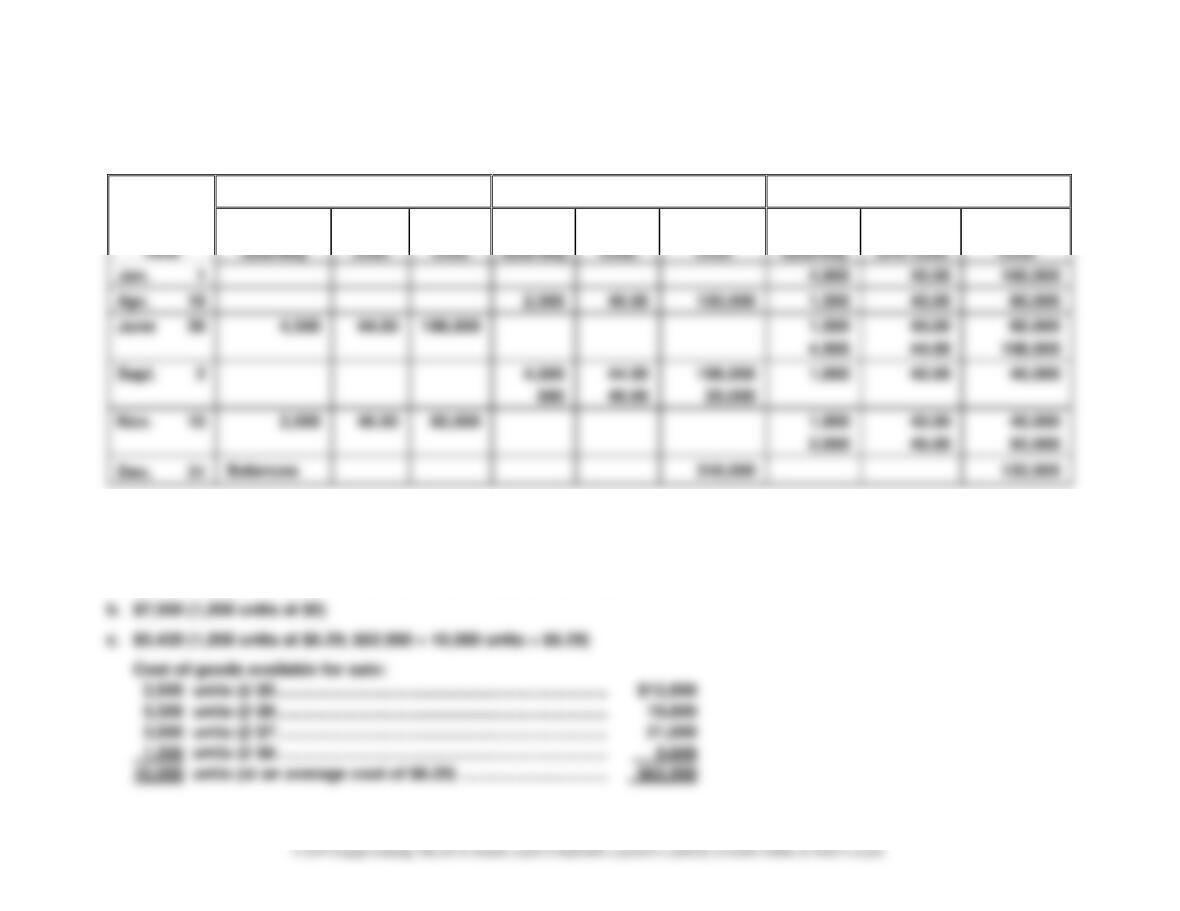

Ex. 6–11

Date

Purchases

Cost of Goods Sold

Inventory

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit Cost

Total

Cost

Jan. 1

4,000

40.00

160,000

Apr. 19

2,500

40.00

100,000

1,500

40.00

60,000

June 30

4,500

44.00

198,000

1,500

4,500

40.00

44.00

60,000

198,000

Sept. 2

4,500

500

44.00

40.00

198,000

20,000

1,000

40.00

40,000

Nov. 15

2,000

46.00

92,000

1,000

2,000

40.00

46.00

40,000

92,000

Dec. 31

Balances

318,000

132,000

Ex. 6–12

a. $11,700 [(1,200 units at $8 + 300 units at $7) = $9,600 + $2,100]

CHAPTER 6 Inventories

6–13

Ex. 6–13

Inventory Method

Ending

Inventory

Cost of

Goods Sold

a.

First-in, first-out

$24,912

$65,888

b.

Last-in, first-out

22,520

68,280

c.

Weighted average cost

23,608

67,192

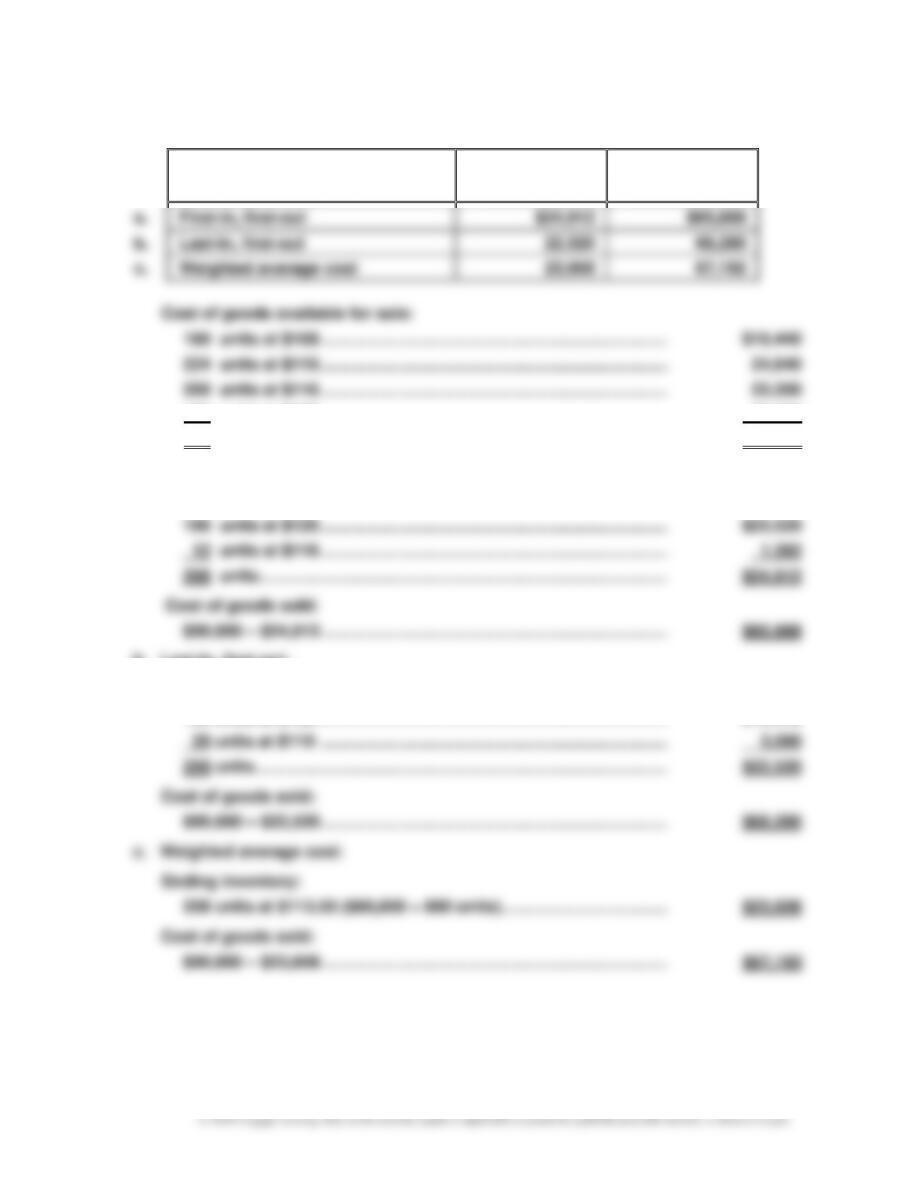

Cost of goods available for sale:

180 units at $108 ………………………………………………………………… $19,440

224 units at $110 ………………………………………………………………… 24,640

200 units at $116 ………………………………………………………………… 23,200

196 units at $120 ………………………………………………………………… 23,520

800 units (at an average cost of $113.50) ……………………………… $90,800

a. First-in, first-out:

Ending inventory:

b. Last-in, first-out:

Ending inventory:

180 units at $108 …………………………………………………………………. $19,440

CHAPTER 6 Inventories

Ex. 6–14

a. 1.

FIFO inventory

> (greater than)

LIFO inventory

2.

FIFO cost of goods sold

< (less than)

LIFO cost of goods sold

3.

FIFO net income

> (greater than)

LIFO net income

4.

FIFO income taxes

> (greater than)

LIFO income taxes

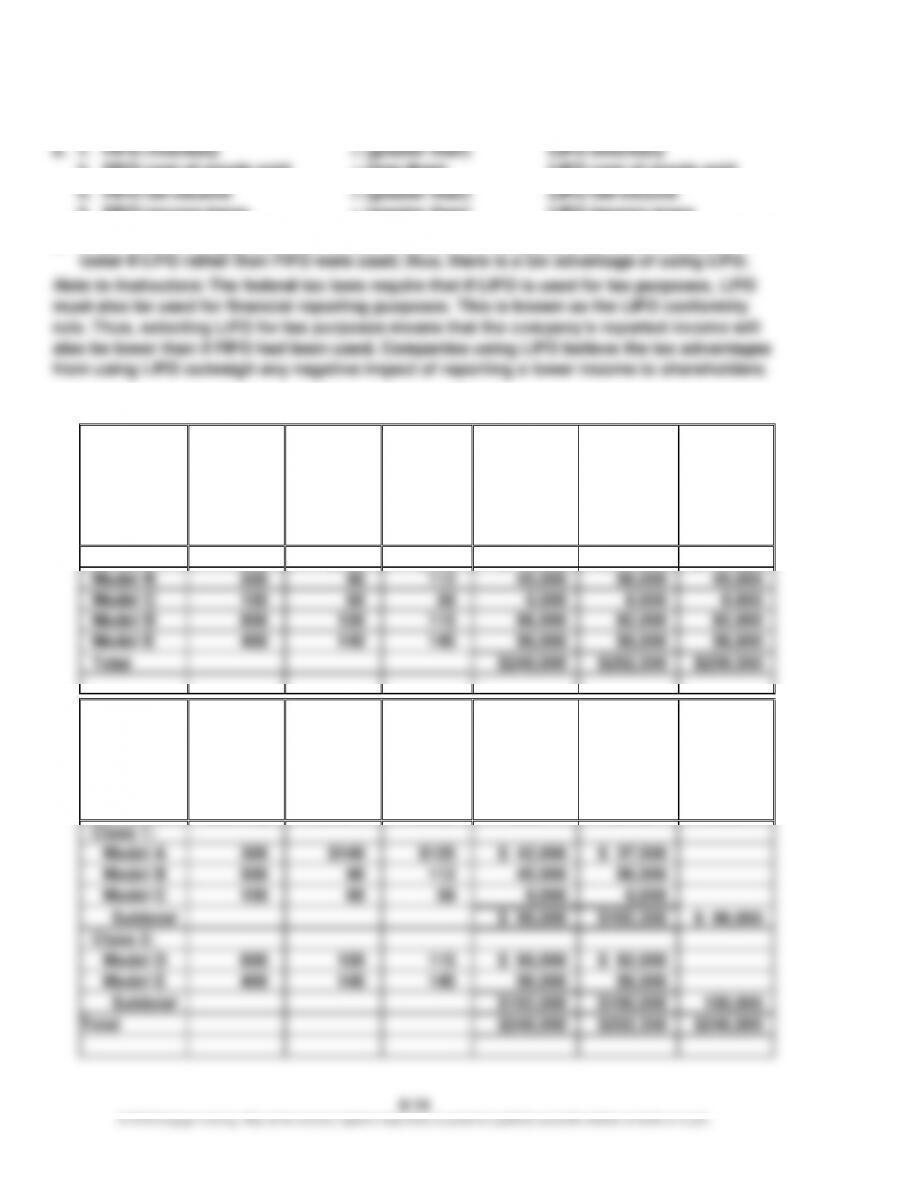

b. In periods of rising prices, the income shown on the company’s tax return would be

Ex. 6–15

a.

Product

Inventory

Quantity

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

Value)

Cost

Market

LCM

Model A

300

$140

$125

$ 42,000

$ 37,500

$ 37,500

Model B

500

90

112

45,000

56,000

45,000

Model C

150

60

59

9,000

8,850

8,850

Model D

800

120

115

96,000

92,000

92,000

Model E

400

140

145

56,000

58,000

56,000

Total

$248,000

$252,350

$239,350

b.

Product

Inventory

Quantity

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

Value)

Cost

Market

LCM

Class 1:

Model A

300

$140

$125

$ 42,000

$ 37,500

Model B

500

90

112

45,000

56,000

Model C

150

60

59

9,000

8,850

Subtotal

$ 96,000

$102,350

$ 96,000

Class 2:

Model D

800

120

115

$ 96,000

$ 92,000

Model E

400

140

145

56,000

58,000

Subtotal

$152,000

$150,000

150,000

Total

$248,000

$252,350

$246,000

CHAPTER 6 Inventories

6–15

Ex. 6–15 (Concluded)

c.

Product

Inventory

Quantity

Cost

per

Unit

Market

Value per

Unit (Net

Realizable

Value)

Cost

Market

LCM

Model A

300

$140

$125

$ 42,000

$ 37,500

Model B

500

90

112

45,000

56,000

Model C

150

60

59

9,000

8,850

Model D

800

120

115

96,000

92,000

Model E

400

140

145

56,000

58,000

Total

$248,000

$252,350

$248,000

Ex. 6–16

The inventory would appear in the Current assets section, as follows:

Ex. 6–17

a. 20Y8 Balance Sheet

Inventory ………………………………………………………………………….. $10,400 understated

CHAPTER 6 Inventories

6–16

Ex. 6–18

a. 20Y1 Balance Sheet

Inventory ………………………………………………………………………… $27,000 overstated

Gross profit ……………………………………………………………………. $27,000 understated

Net income ……………………………………………………………………… $27,000 understated

d. The December 31, 20Y2, balance sheet would be correct, since the 20Y1

inventory error reverses itself in 20Y2.

Ex. 6–19

When an error is discovered affecting the prior period, it should be corrected. In this case,

CHAPTER 6 Inventories

6–17

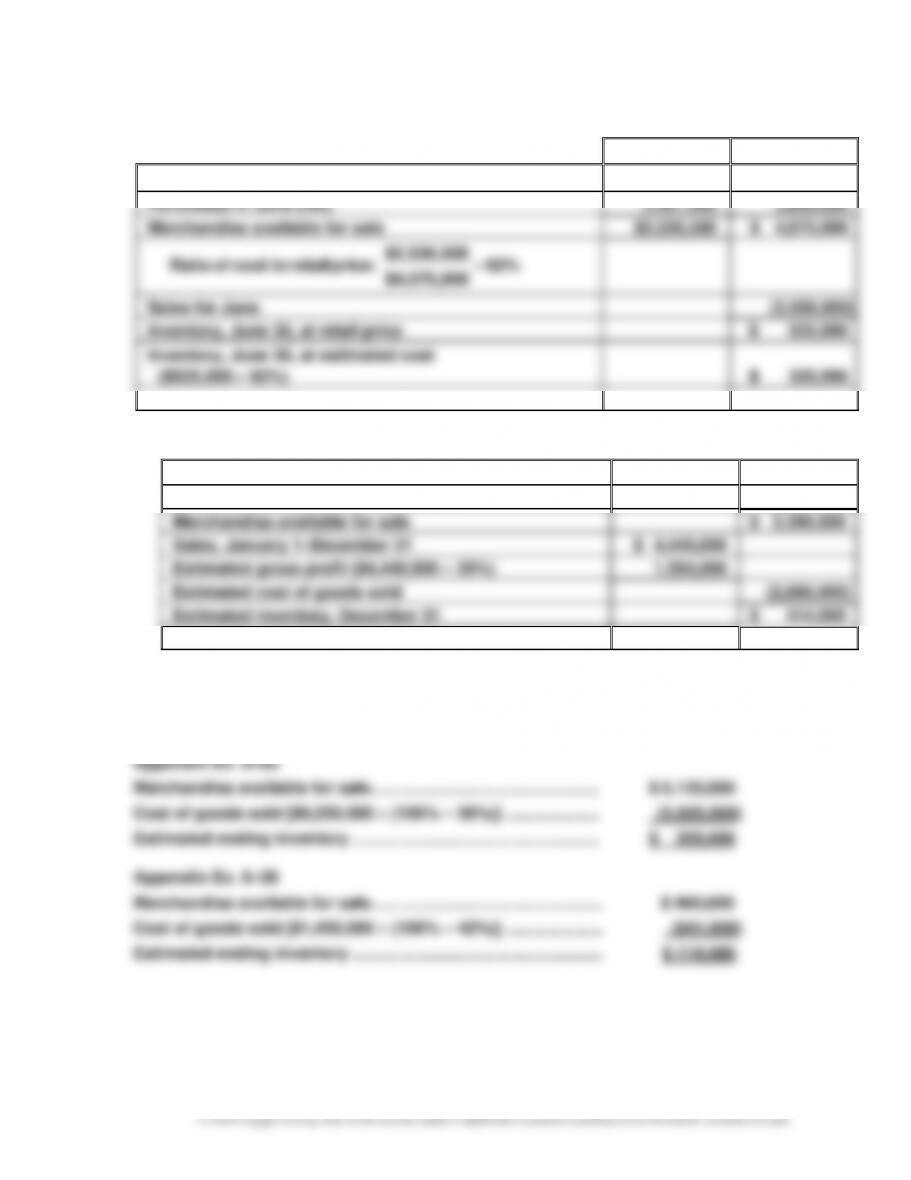

Appendix Ex. 6–23

Cost

Retail

Inventory, June 1

$ 165,000

$ 275,000

Purchases in June (net)

2,361,500

3,800,000

Merchandise available for sale

$2,526,500

$ 4,075,000

62%

$4,075,000

$2,526,500

:price retail tocost of Ratio =

Sales for June

(3,550,000)

Inventory, June 30, at retail price

$ 525,000

Inventory, June 30, at estimated cost

($525,000 62%)

$ 325,500

Appendix Ex. 6–24

a.

Inventory, January 1

$ 350,000

Purchases (net), January 1–December 31

2,950,000

Merchandise available for sale

$ 3,300,000

Sales, January 1–December 31

$ 4,440,000

Estimated gross profit ($4,440,000 35%)

1,554,000

Estimated cost of goods sold

(2,886,000)

Estimated inventory, December 31

$ 414,000

b. The gross profit method is useful for estimating inventories for monthly or quarterly

financial statements. It is also useful in estimating the cost of inventory destroyed by fire

or other disasters.

CHAPTER 6 Inventories

6–18

PROBLEMS

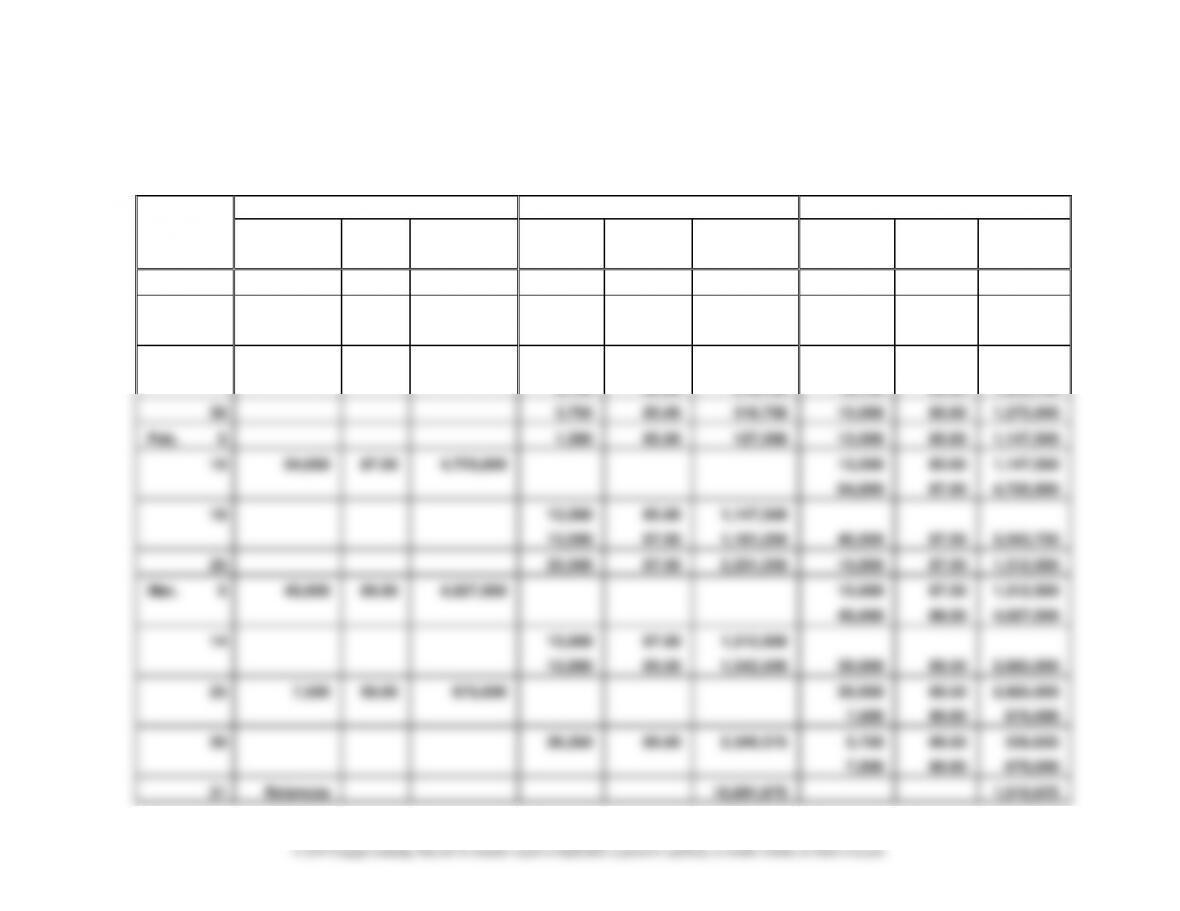

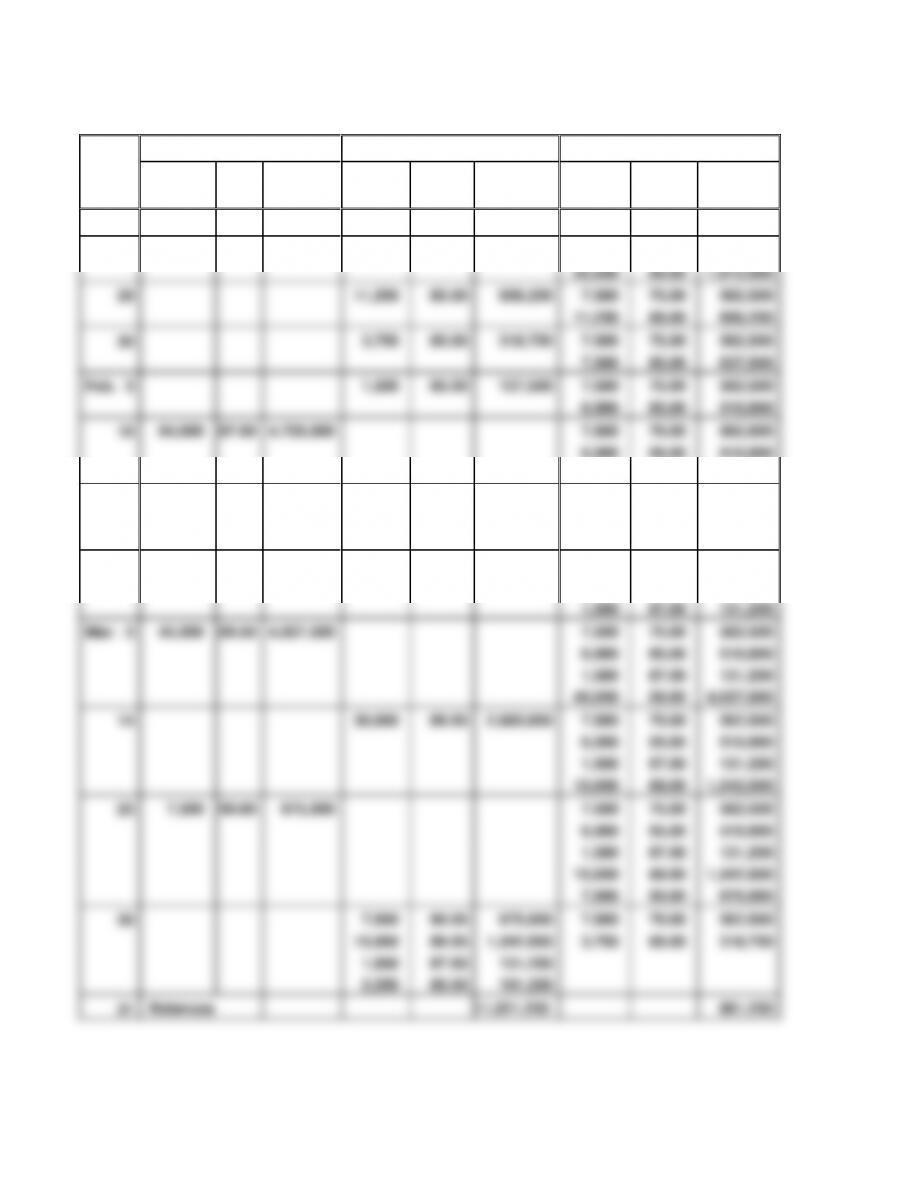

Prob. 6–1A

1.

Date

Purchases

Cost of Goods Sold

Inventory

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total

Cost

Jan. 1

7,500

75.00

562,500

10

22,500

85.00

1,912,500

7,500

22,500

75.00

85.00

562,500

1,912,500

28

7,500

3,750

75.00

85.00

562,500

318,750

18,750

85.00

1,593,750

30

3,750

85.00

318,750

15,000

85.00

1,275,000

Feb. 5

1,500

85.00

127,500

13,500

85.00

1,147,500

10

54,000

87.50

4,725,000

13,500

54,000

85.00

87.50

1,147,500

4,725,000

16

13,500

13,500

85.00

87.50

1,147,500

1,181,250

40,500

87.50

3,543,750

28

25,500

87.50

2,231,250

15,000

87.50

1,312,500

Mar. 5

45,000

89.50

4,027,500

15,000

45,000

87.50

89.50

1,312,500

4,027,500

14

15,000

15,000

87.50

89.50

1,312,500

1,342,500

30,000

89.50

2,685,000

25

7,500

90.00

675,000

30,000

7,500

89.50

90.00

2,685,000

675,000

30

26,250

89.50

2,349,375

3,750

7,500

89.50

90.00

335,625

675,000

31

Balances

10,891,875

1,010,625

CHAPTER 6 Inventories

6–19

Prob. 6–1A (Concluded)

2.

Accounts Receivable

19,875,000

Sales

19,875,000*

Cost of Goods Sold

10,891,875

Inventory

10,891,875

*$19,875,000 = $1,687,500 + $562,500 + $225,000 + $4,320,000 + $4,080,000 + $4,800,000 + $4,200,000

3. $8,983,125 ($19,875,000 – $10,891,875)

CHAPTER 6 Inventories

Prob. 6–2A

1.

Purchases

Cost of Goods Sold

Inventory

Unit

Total

Unit

Total

Unit

Total

Date

Quantity

Cost

Cost

Quantity

Cost

Cost

Quantity

Cost

Cost

Jan. 1

7,500

75.00

562,500

10

22,500

85.00

1,912,500

7,500

75.00

562,500

22,500

85.00

1,912,500

28

11,250

85.00

956,250

7,500

75.00

562,500

11,250

85.00

956,250

30

3,750

85.00

318,750

7,500

75.00

562,500

7,500

85.00

637,500

Feb. 5

1,500

85.00

127,500

7,500

75.00

562,500

6,000

85.00

510,000

10

54,000

87.50

4,725,000

7,500

75.00

562,500

6,000

85.00

510,000

54,000

87.50

4,725,000

16

27,000

87.50

2,362,500

7,500

75.00

562,500

6,000

85.00

510,000

27,000

87.50

2,362,500

28

25,500

87.50

2,231,250

7,500

75.00

562,500

6,000

85.00

510,000

1,500

87.50

131,250

Mar. 5

45,000

89.50

4,027,500

7,500

75.00

562,500

6,000

85.00

510,000

1,500

87.50

131,250

45,000

89.50

4,027,500

14

30,000

89.50

2,685,000

7,500

75.00

562,500

6,000

85.00

510,000

1,500

87.50

131,250

15,000

89.50

1,342,500

25

7,500

90.00

675,000

7,500

75.00

562,500

6,000

85.00

510,000

1,500

87.50

131,250

15,000

89.50

1,342,500

7,500

90.00

675,000

30

7,500

90.00

675,000

7,500

75.00

562,500

15,000

89.50

1,342,500

3,750

85.00

318,750

1,500

87.50

131,250

2,250

85.00

191,250

31

Balances

11,021,250

881,250