CHAPTER 4 The Accounting Cycle

4–114

Comp. Prob. 1 (Continued)

7.

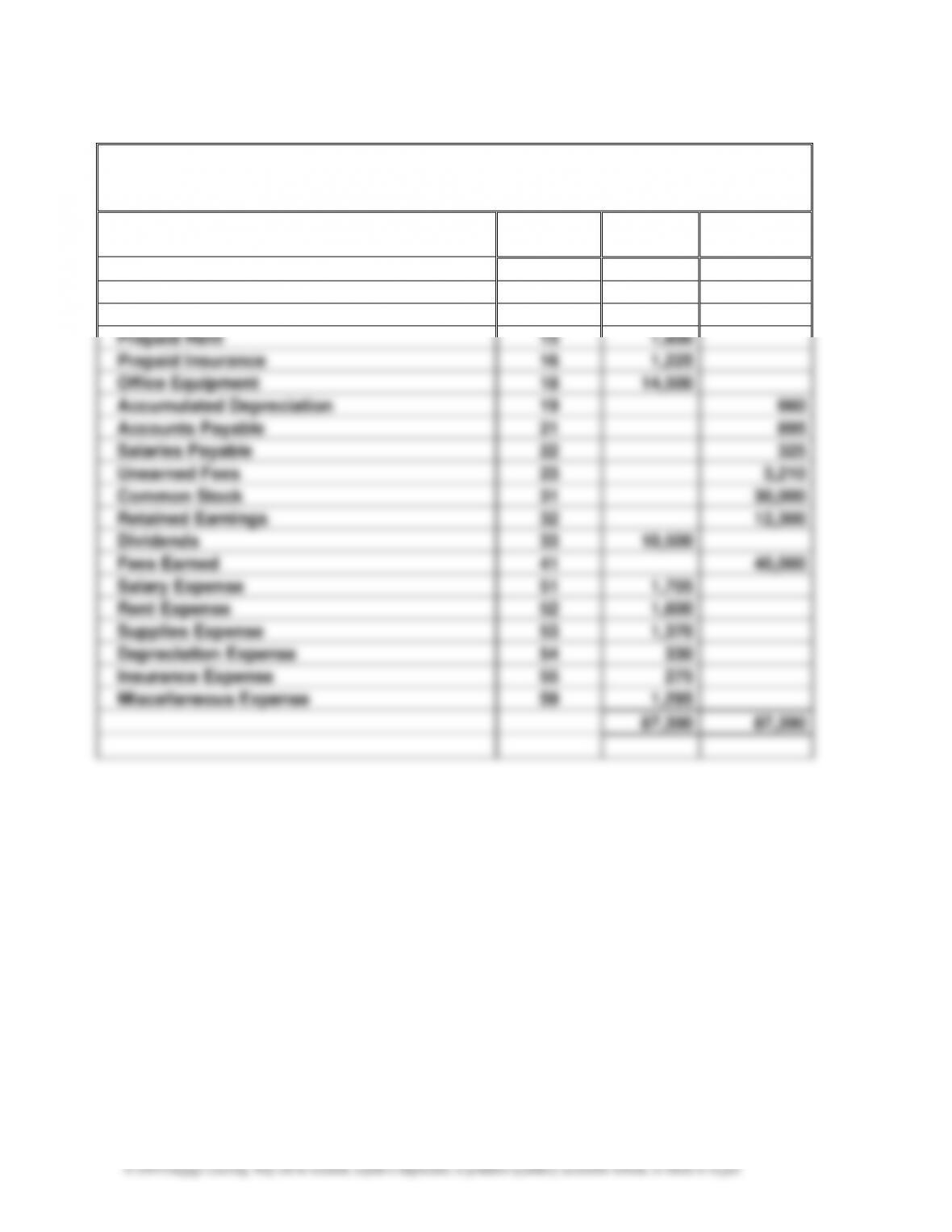

Kelly Consulting

Adjusted Trial Balance

May 31, 20Y8

Account

Debit

Credit

No.

Balances

Balances

Cash

11

44,195

Accounts Receivable

12

8,080

Supplies

14

715

Prepaid Rent

15

1,600

Prepaid Insurance

16

1,225

Office Equipment

18

14,500

Accumulated Depreciation

19

660

Accounts Payable

21

895

Salaries Payable

22

325

Unearned Fees

23

3,210

Common Stock

31

30,000

Retained Earnings

32

12,300

Dividends

33

10,500

Fees Earned

41

40,000

Salary Expense

51

1,705

Rent Expense

52

1,600

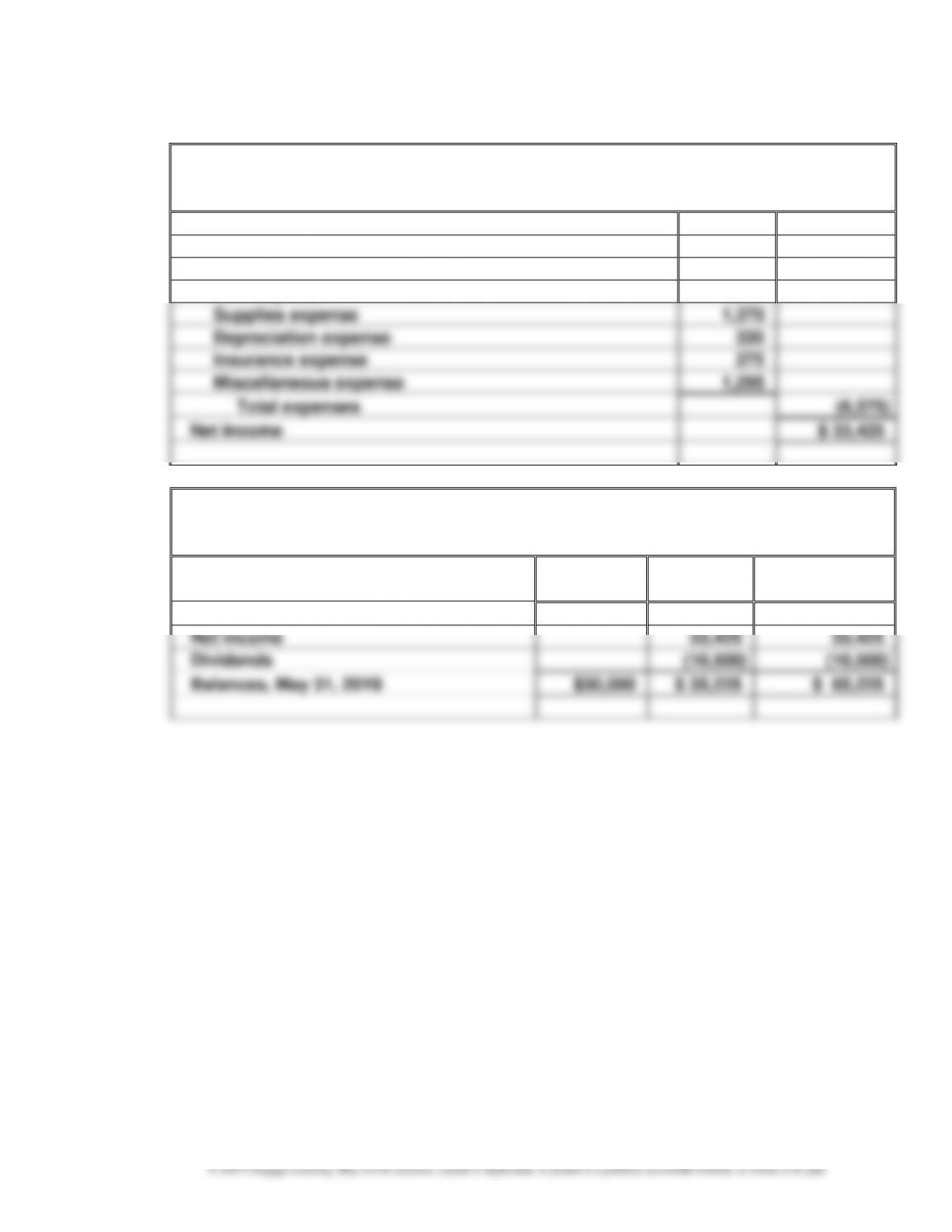

Supplies Expense

53

1,370

Depreciation Expense

54

330

Insurance Expense

55

275

Miscellaneous Expense

59

1,295

87,390

87,390

CHAPTER 4 The Accounting Cycle

4–115

Comp. Prob. 1 (Continued)

8.

Kelly Consulting

Income Statement

For the Month Ended May 31, 20Y8

Fees earned

$ 40,000

Expenses:

Salary expense

$1,705

Rent expense

1,600

Supplies expense

1,370

Depreciation expense

330

Insurance expense

275

Miscellaneous expense

1,295

Total expenses

(6,575)

Net income

$ 33,425

Kelly Consulting

Statement of Stockholders’ Equity

For the Month Ended May 31, 20Y8

Common

Stock

Retained

Earnings

Total

Balances, May 1, 20Y8

$30,000

$ 12,300

$ 42,300

Net income

33,425

33,425

Dividends

(10,500)

(10,500)

Balances, May 31, 20Y8

$30,000

$ 35,225

$ 65,225

CHAPTER 4 The Accounting Cycle

4–116

Comp. Prob. 1 (Continued)

Kelly Consulting

Balance Sheet

May 31, 20Y8

Assets

Current assets:

Cash

$44,195

Accounts receivable

8,080

Supplies

715

Prepaid rent

1,600

Prepaid insurance

1,225

Total current assets

$55,815

Property, plant, and equipment:

Office equipment

$14,500

Accumulated depreciation

(660)

Total property, plant, and equipment

13,840

Total assets

$69,655

Liabilities

Current liabilities:

Accounts payable

$ 895

Salaries payable

325

Unearned fees

3,210

Total liabilities

$ 4,430

Stockholders’ Equity

Common stock

$30,000

Retained earnings

35,225

Total stockholders’ equity

65,225

Total liabilities and stockholders’ equity

$69,655

CHAPTER 4 The Accounting Cycle

4–117

Comp. Prob. 1 (Concluded)

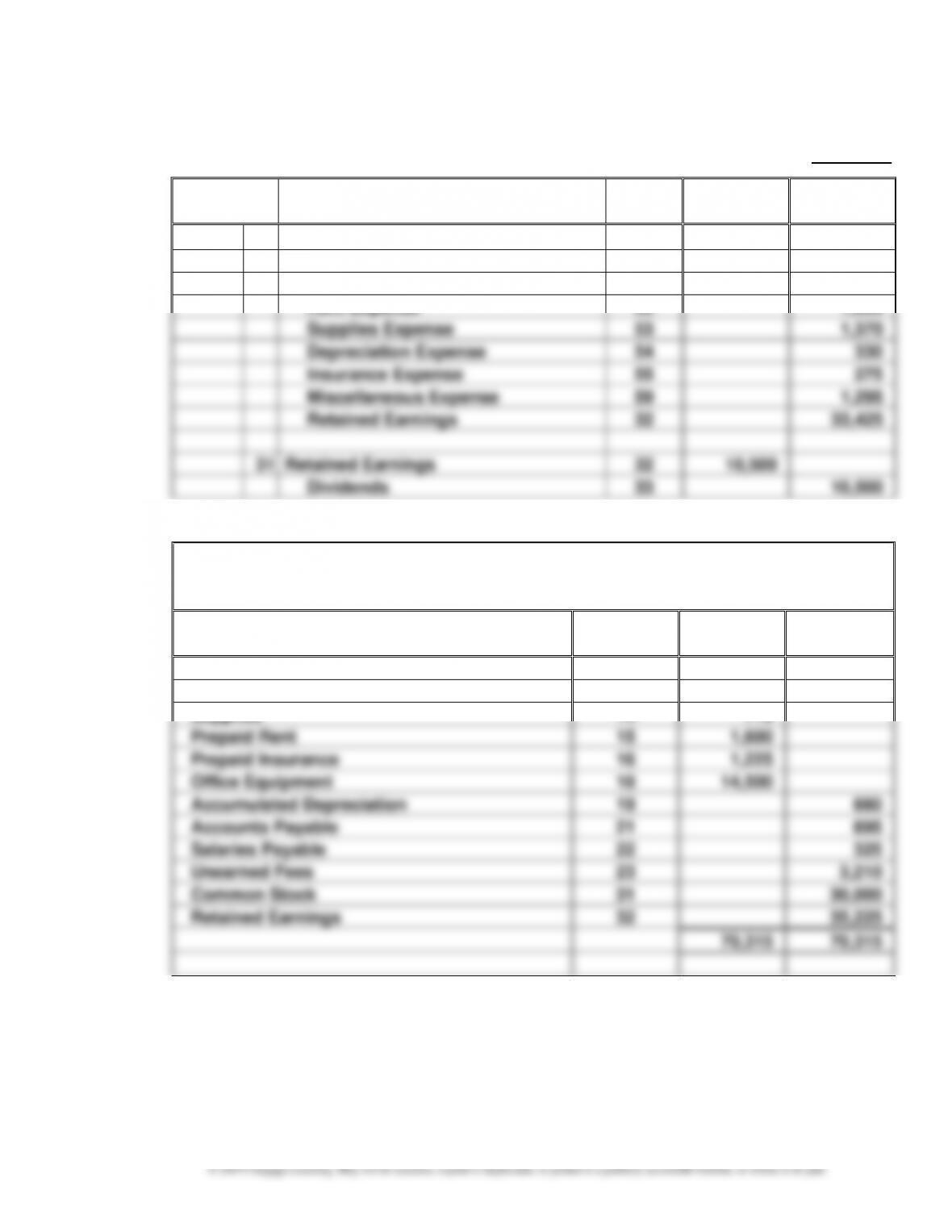

9. JOURNAL Page _____ 8_

Date

Post.

Ref.

Debit

Credit

20Y8

Closing Entries

May

31

Fees Earned

41

40,000

Salary Expense

51

1,705

Rent Expense

52

1,600

Supplies Expense

53

1,370

Depreciation Expense

54

330

Insurance Expense

55

275

Miscellaneous Expense

59

1,295

Retained Earnings

32

33,425

31

Retained Earnings

32

10,500

Dividends

33

10,500

10.

Kelly Consulting

Post-Closing Trial Balance

May 31, 20Y8

Account

Debit

Credit

No.

Balances

Balances

Cash

11

44,195

Accounts Receivable

12

8,080

Supplies

14

715

Prepaid Rent

15

1,600

Prepaid Insurance

16

1,225

Office Equipment

18

14,500

Accumulated Depreciation

19

660

Accounts Payable

21

895

Salaries Payable

22

325

Unearned Fees

23

3,210

Common Stock

31

30,000

Retained Earnings

32

35,225

70,315

70,315

CHAPTER 4 The Accounting Cycle

MAKE A DECISION

MAD 4–1

a. Amazon Best Buy

Working capital $1,965 $ 2,961

b. Best Buy has a larger working capital balance than does Amazon ($2,961 million

c. Working capital is a poor measure for comparing liquidity across firms. Amazon has

d.

(rounded)1.0

$43,816

$45,871

:Amazon

sLiabilitieCurrent

setsCurrent As

RatioCurrent

=

=

4–119

MAD 4–2 (Concluded)

d. Based upon the current ratio for Year 2, Zynga is the most liquid company followed by

Electronic Arts and Take-Two, as follows:

Ranking

Current Ratio for Year 2

1

Zynga

4.0

2

Electronic Arts

1.8

3

Take-Two

1.7

MAD 4–3

a.

Foot Locker

The Finish Line

Year 2

Year 1

Year 2

Year 1

Current assets

$2,606

$2,456

$ 521

$ 531

Current liabilities

(700)

(696)

(221)

(191)

Working capital

$1,906

$1,760

$ 300

$ 340

b.

Foot Locker

The Finish Line

Year 2

Year 1

Year 2

Year 1

Current Ratio =

Current Assets _

=

$2,606

$2,456

$521

$531

Current Liabilities

$700

$696

$221

$191

=

3.7

3.5

2.4

2.8

c. For both years, it appears that Foot Locker has the greater relative liquidity, as measured

d. Foot Locker’s current ratio increased from 3.5 to 3.7. In contrast, The Finish Line’s

CHAPTER 4 The Accounting Cycle

MAD 4–4

a.

Dec. 31,

Dec. 31,

Year 2

Year 1

Current assets

$1,965.2

$1,498.8

Current liabilities

(685.8)

(478.8)

Working capital

$1,279.4

$1,020.0

Year 1

Current assets

Current liabilities

(5,595)

Working capital

$ 268

CHAPTER 4 The Accounting Cycle

4–121

MAD 4–6

a.

Microsoft

Alphabet

Year 2

Year 1

Year 2

Year 1

Current assets

$139,660

$122,797

$105,408

$ 90,114

Current liabilities

(59,357)

(49,647)

(16,756)

(19,310)

Working capital

$ 80,303

$ 73,150

$ 88,652

$ 70,804

b. Microsoft and Alphabet have similar amounts of working capital. Alphabet had slightly

more at the end of Year 2, but slightly less at the end of Year 1.

c. Working capital does not measure the “relative” liquidity between two companies. Size

d.

(rounded)6.3

$16,756

$105,408

:2 Year

(rounded)4.7

$19,310

$90,114

:1 Year :Alphabet

(rounded)2.4

$59,357

$139,660

:2 Year

(rounded)2.5

$49,647

$122,797

:1 Year:Microsoft

sLiabilitieCurrent

setsCurrent As

RatioCurrent

=

=

=

=

=

e. Alphabet has greater short-term liquidity as measured by the current ratio than does

CHAPTER 4 The Accounting Cycle

4–122

TAKE IT FURTHER

TIF 4–1

1. No. By knowingly recording a personal loan as a trade account receivable, Manny is

reporting financial information that does not accurately reflect the company’s financial

2. The users who rely upon this financial information, such as potential investors and

TIF 4–2

2. Cash (and cash equivalents)

Accounts receivable

3. Inventory is the primary balance sheet account that is different. Wal-Mart reports over $40

billion in inventory, while Zynga doesn’t report any inventory. This difference is due to the

TIF 4–3

To: Daniel Nat

From: A+ Student

Re: Balance Sheet Presentation

The balance sheet describes the financial condition of the company as of a given date and is

CHAPTER 4 The Accounting Cycle

TIF 4–3 (Concluded)

The “Assets” section of the balance sheet should have separate sections for current assets

and property, plant, and equipment, and assets should be presented in the order in which

Presuming that the amounts recorded in the accounts are accurately reported, a correctly

presented balance sheet would appear as follows:

Asheville Company

Balance Sheet

December 31, 20Y5

Assets

Current assets:

Cash

$ 10,000

Accounts receivable

12,500

Total current assets

$ 22,500

Property, plant, and equipment:

Land

$100,000

Equipment

125,000

Total property, plant, and equipment

225,000

Total assets

$247,500

Liabilities

Current liabilities:

Accounts payable

$ 10,000

Wages payable

2,500

Total liabilities

$ 12,500

Stockholders’ Equity

Common stock

$115,000

Retained earnings

120,000

Total stockholders’ equity

235,000

Total liabilities and stockholders’ equity

$247,500

CHAPTER 4 The Accounting Cycle

4–124

TIF 4–4

1. a. With the decreasing cost of computers and related software, Main Street Co. may find

accounting function.

b. A computerized accounting system would allow for eliminating the end-of– period

c. In designing a computerized financial reporting (accounting) system, proper

accounting principles, concepts, and procedures must be followed. At a minimum,

basic controls such as the use of the double-entry accounting system should be

2. Supplies cannot have a credit balance, because the supplies account is an asset account.

CHAPTER 4 The Accounting Cycle

4–125

TIF 4–5

1. A set of financial statements provides useful information concerning the economic

condition of a company. For example, the balance sheet describes the financial condition

2. The following adjustments might be necessary before an accurate set of financial

statements could be prepared:

• No supplies expense is shown. The supplies account should be adjusted for the

supplies used during the year.

• No depreciation expense or accumulated depreciation is shown for the building or

Accounts.”

The following items should be relabeled for greater clarity:

• Billings Due from Others—Accounts Receivable

Note to Instructors: The preceding items are not intended to include all adjustments

that might need to be made to the accounts. The possible adjustments listed include

only items that have been covered in Chapters 1–4. For example, uncollectible

accounts expense (discussed in a later chapter) is not mentioned.

CHAPTER 4 The Accounting Cycle

4–126

© 2019 Cengage Learning. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

TIF 4–5 (Concluded)

3. In general, the decision to extend a loan is based on an assessment of the profitability and

riskiness of the loan. Although the financial statements provide useful data for this

purpose, other factors such as the following might also be significant: