4–1

CHAPTER 4

THE ACCOUNTING CYCLE

DISCUSSION QUESTIONS

1. The end-of-period spreadsheet illustrates the flow of accounting information from the unadjusted trial

2. a. Current assets are composed of cash and other assets that may reasonably be expected to be realized in

3. Current liabilities are liabilities that will be due within a short time (usually one year or less) and that are to

5. Closing entries are necessary at the end of an accounting period (1) to transfer the balances in temporary

6. Adjusting entries bring the accounts up to date, while closing entries reduce the revenue, expense, and

dividends accounts to zero balances for use in recording transactions for the next accounting period.

7. The purpose of the post-closing trial balance is to make sure that the ledger is in balance at the beginning

of the next period.

8. a. The financial statements are the most important output of the accounting cycle.

9. Preparing an end-of-period spreadsheet is an optional step of the accounting cycle.

10. a. Liquidity is the ability of a business to convert assets into cash, while solvency is the ability of a

CHAPTER 4 The Accounting Cycle

BASIC EXERCISES

BE 4–1

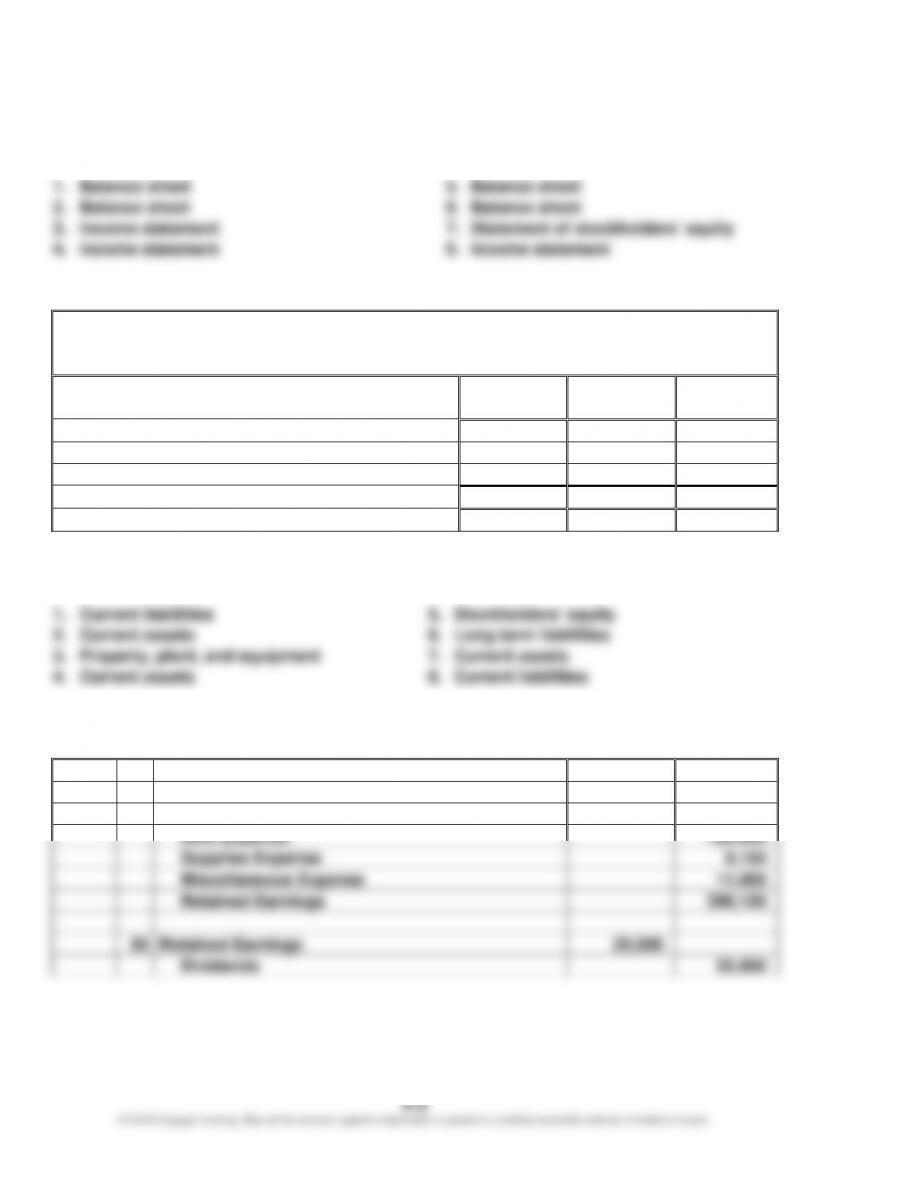

1. Balance sheet

5.

Balance sheet

2. Balance sheet

6.

Balance sheet

3. Income statement

7.

Statement of stockholders’ equity

4. Income statement

8.

Income statement

BE 4–2

AAA Delivery Services

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y7

Common

Stock

Retained

Earnings

Total

Balances, January 1, 20Y7

$40,000

$815,500

$855,500

Net income

67,250

67,250

Dividends

(10,000)

(10,000)

Balances, December 31, 20Y7

$40,000

$872,750

$912,750

BE 4–3

1. Current liabilities

5.

Stockholders’ equity

2. Current assets

6.

Long-term liabilities

3. Property, plant, and equipment

7.

Current assets

4. Current assets

8.

Current liabilities

BE 4–4

Closing Entries

Nov.

30

Fees Earned

1,150,000

Wages Expense

613,750

Rent Expense

120,000

Supplies Expense

9,150

Miscellaneous Expense

11,000

Retained Earnings

396,100

30

Retained Earnings

25,000

Dividends

25,000

4–3

BE 4–5

BE 4–6

a.

20Y4

20Y3

Current assets ……………

$1,586,250

$1,210,000

Current liabilities ………..

705,000

550,000

Working capital …………..

$ 881,250

$ 660,000

Current ratio ……………….

2.25

2.20

($1,586,250 $705,000)

($1,210,000 $550,000)

b. The increase from 2.20 to 2.25 indicates a favorable change.

EXERCISES

Ex. 4–1

Ex. 4–2

Ex. 4–3

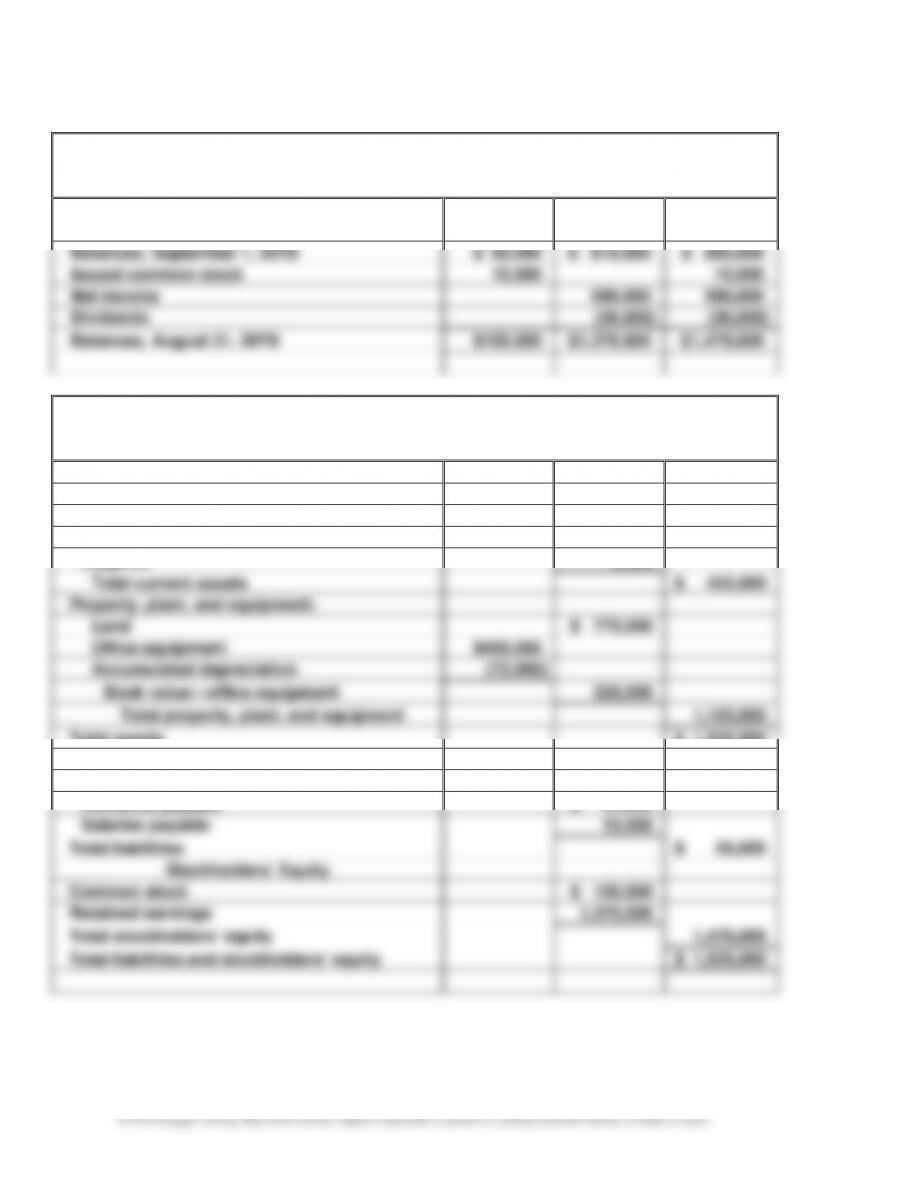

Demo Consulting

Income Statement

For the Year Ended August 31, 20Y9

Fees earned

$ 1,480,000

Expenses:

Salary expense

$843,100

Supplies expense

22,600

Depreciation expense

11,800

Miscellaneous expense

12,500

Total expenses

(890,000)

Net income

$ 590,000

CHAPTER 4 The Accounting Cycle

4–4

Ex. 4–3 (Concluded)

Demo Consulting

Statement of Stockholders’ Equity

For the Year Ended August 31, 20Y9

Common

Stock

Retained

Earnings

Total

Balances, September 1, 20Y8

$ 85,000

$ 810,000

$ 895,000

Issued common stock

15,000

15,000

Net income

590,000

590,000

Dividends

(30,000)

(30,000)

Balances, August 31, 20Y9

$100,000

$1,370,000

$ 1,470,000

Demo Consulting

Balance Sheet

August 31, 20Y9

Assets

Current assets:

Cash

$ 182,500

Accounts receivable

234,500

Supplies

5,000

Total current assets

$ 422,000

Property, plant, and equipment:

Land

$ 775,000

Office equipment

$400,000

Accumulated depreciation

(72,000)

Book value—office equipment

328,000

Total property, plant, and equipment

1,103,000

Total assets

$ 1,525,000

Liabilities

Current liabilities:

Accounts payable

$ 41,500

Salaries payable

13,500

Total liabilities

$ 55,000

Stockholders’ Equity

Common stock

$ 100,000

Retained earnings

1,370,000

Total stockholders’ equity

1,470,000

Total liabilities and stockholders’ equity

$ 1,525,000

CHAPTER 4 The Accounting Cycle

4–5

Ex. 4–4

Triton Consulting

Income Statement

For the Year Ended April 30, 20Y3

Fees earned

$ 279,000

Expenses:

Salary expense

$242,000

Supplies expense

1,650

Depreciation expense

900

Miscellaneous expense

2,000

Total expenses

(246,550)

Net income

$ 32,450

Triton Consulting

Statement of Stockholders’ Equity

For the Year Ended April 30, 20Y3

Common

Stock

Retained

Earnings

Total

Balances, May 1, 20Y2

$15,000

$ 52,200

$ 67,200

Issued common stock

5,000

5,000

Net income

32,450

32,450

Dividends

(10,000)

(10,000)

Balances, April 30, 20Y3

$20,000

$ 74,650

$ 94,650

CHAPTER 4 The Accounting Cycle

4–6

Ex. 4–4 (Concluded)

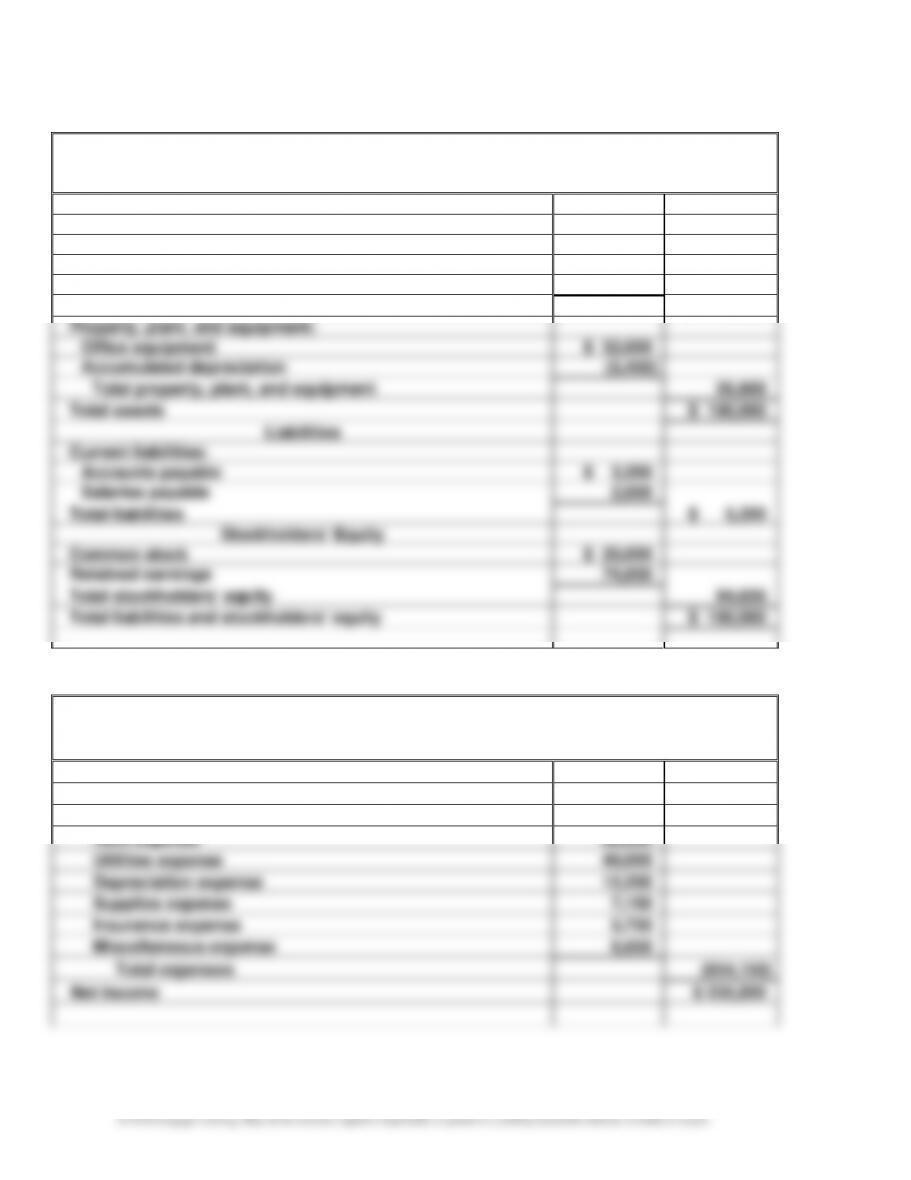

Triton Consulting

Balance Sheet

April 30, 20Y3

Assets

Current assets:

Cash

$ 21,500

Accounts receivable

51,150

Supplies

750

Total current assets

$ 73,400

Property, plant, and equipment:

Office equipment

$ 32,000

Accumulated depreciation

(5,400)

Total property, plant, and equipment

26,600

Total assets

$ 100,000

Liabilities

Current liabilities:

Accounts payable

$ 3,350

Salaries payable

2,000

Total liabilities

$ 5,350

Stockholders’ Equity

Common stock

$ 20,000

Retained earnings

74,650

Total stockholders’ equity

94,650

Total liabilities and stockholders’ equity

$ 100,000

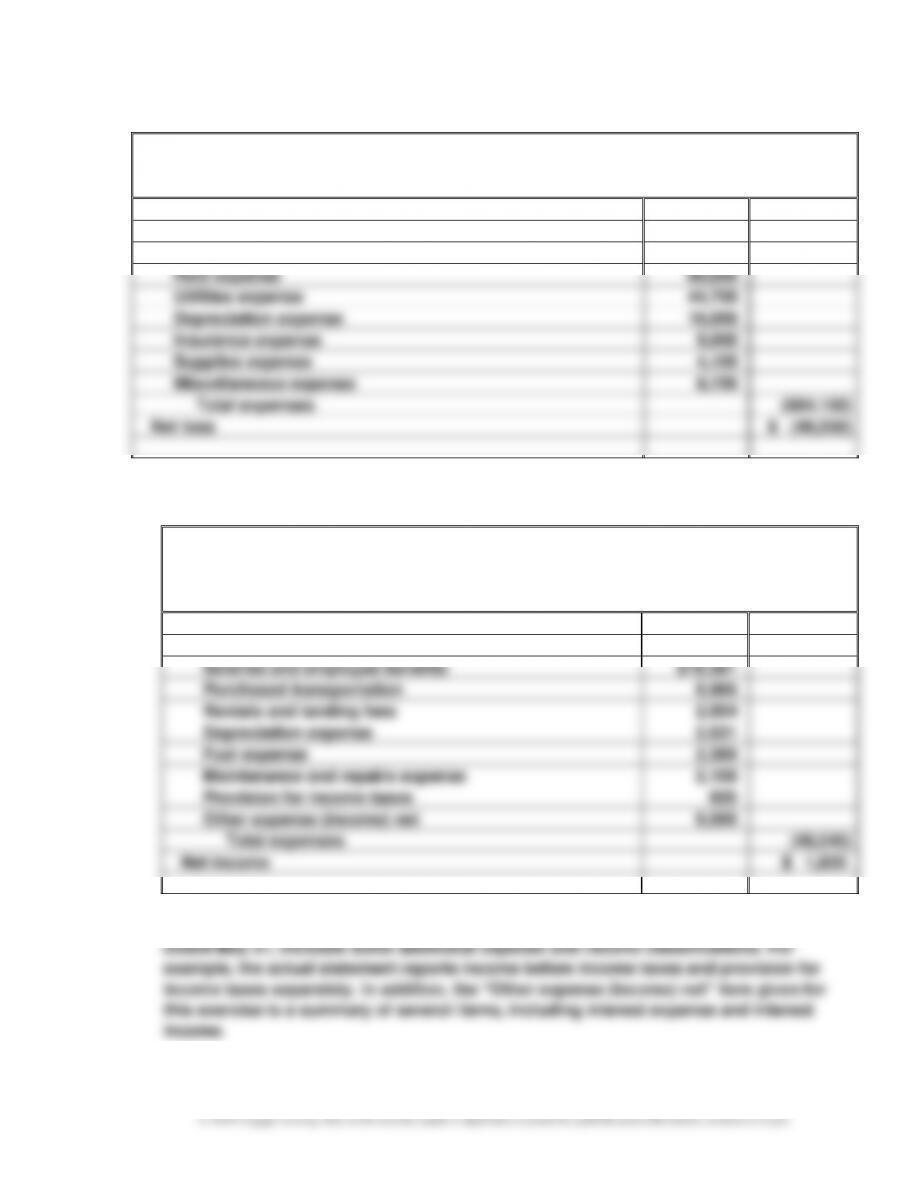

Ex. 4–5

Urgent Messenger Service

Income Statement

For the Year Ended November 30, 20Y1

Fees earned

$ 990,000

Expenses:

Salaries expense

$502,400

Rent expense

80,000

Utilities expense

40,000

Depreciation expense

12,200

Supplies expense

7,150

Insurance expense

5,750

Miscellaneous expense

6,650

Total expenses

(654,150)

Net income

$ 335,850

CHAPTER 4 The Accounting Cycle

4–7

Ex. 4–6

Acorn Health Services Co.

Income Statement

For the Year Ended January 31, 20Y7

Service revenue

$ 634,900

Expenses:

Wages expense

$548,200

Rent expense

60,000

Utilities expense

44,700

Depreciation expense

10,000

Insurance expense

9,000

Supplies expense

4,100

Miscellaneous expense

8,150

Total expenses

(684,150)

Net loss

$ (49,250)

Ex. 4–7

a.

FedEx Corporation

Income Statement

For the Year Ended May 31

(in millions)

Revenues

$ 50,365

Expenses:

Salaries and employee benefits

$18,581

Purchased transportation

9,966

Rentals and landing fees

2,854

Depreciation expense

2,631

Fuel expense

2,399

Maintenance and repairs expense

2,108

Provision for income taxes

920

Other expense (income) net

9,086

Total expenses

(48,545)

Net income

$ 1,820

b. The income statements are very similar. The actual statement, which is for the year

CHAPTER 4 The Accounting Cycle

4–8

Ex. 4–8

Climate Control Systems Co.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y2

Common

Stock

Retained

Earnings

Total

Balances, January 1, 20Y2

$ 75,000

$4,150,800

$4,225,800

Issued common stock

25,000

25,000

Net income

700,000

700,000

Dividends

(160,000)

(160,000)

Balances, December 31, 20Y2

$100,000

$4,690,800

$4,790,800

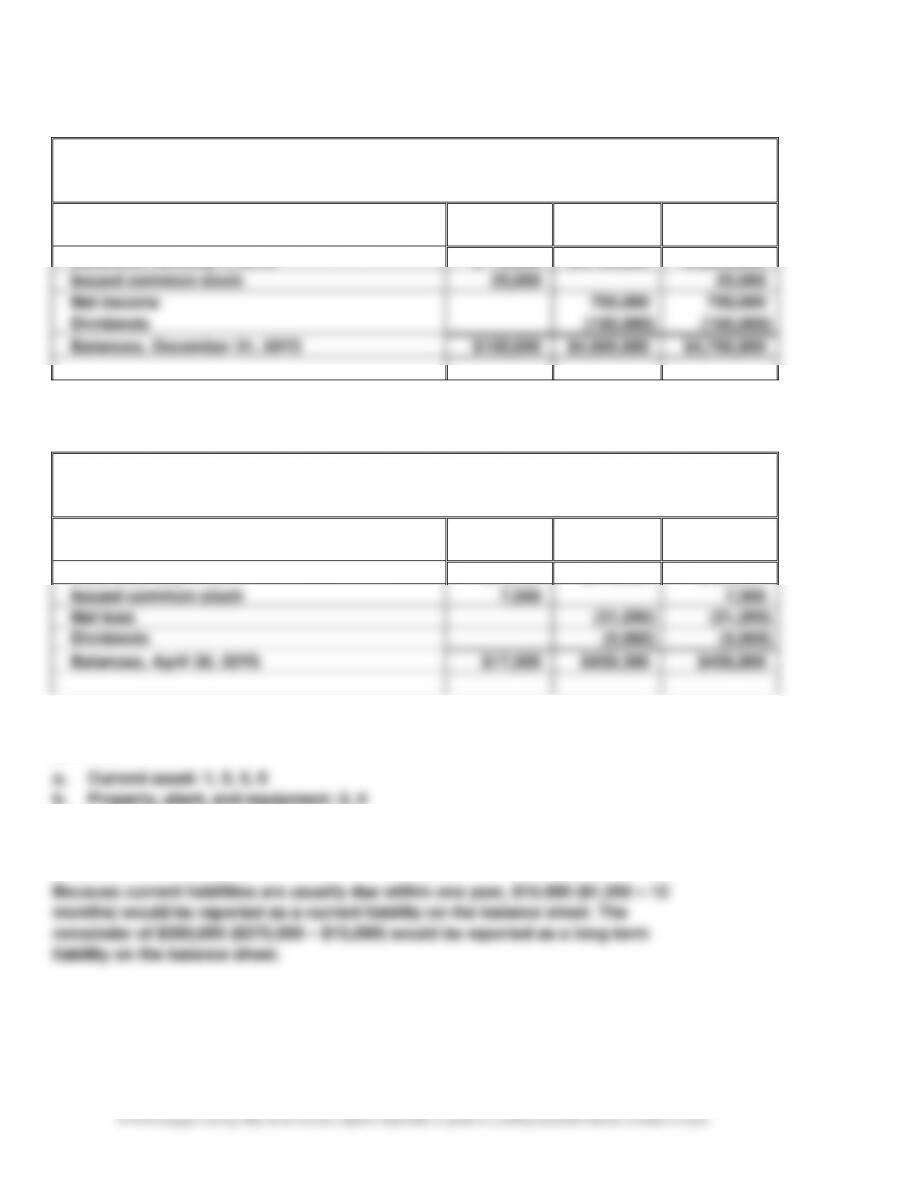

Ex. 4–9

Restoration Arts

Statement of Stockholders’ Equity

For the Year Ended April 30, 20Y5

Common

Retained

Stock

Earnings

Total

Balances, May 1, 20Y4

$10,000

$475,500

$485,500

Issued common stock

7,500

7,500

Net loss

(31,200)

(31,200)

Dividends

(5,000)

(5,000)

Balances, April 30, 20Y5

$17,500

$439,300

$456,800

Ex. 4–10

Ex. 4–11

CHAPTER 4 The Accounting Cycle

4–9

Ex. 4–12

Dynamic Weight Loss Co.

Balance Sheet

June 30, 20Y7

Assets

Current assets:

Cash

$ 72,000

Accounts receivable

187,500

Supplies

11,200

Prepaid insurance

8,400

Prepaid rent

6,000

Total current assets

$285,100

Property, plant, and equipment:

Land

$375,000

Equipment

$ 325,900

Accumulated depreciation—equipment

(186,000)

Book value—equipment

139,900

Total property, plant, and equipment

514,900

Total assets

$800,000

Liabilities

Current liabilities:

Accounts payable

$ 51,200

Salaries payable

7,500

Unearned fees

21,000

Total liabilities

$ 79,700

Stockholders’ Equity

Common stock

$100,000

Retained earnings

620,300

Total stockholders’ equity

720,300

Total liabilities and stockholders’ equity

$800,000

CHAPTER 4 The Accounting Cycle

4–10

Ex. 4–13

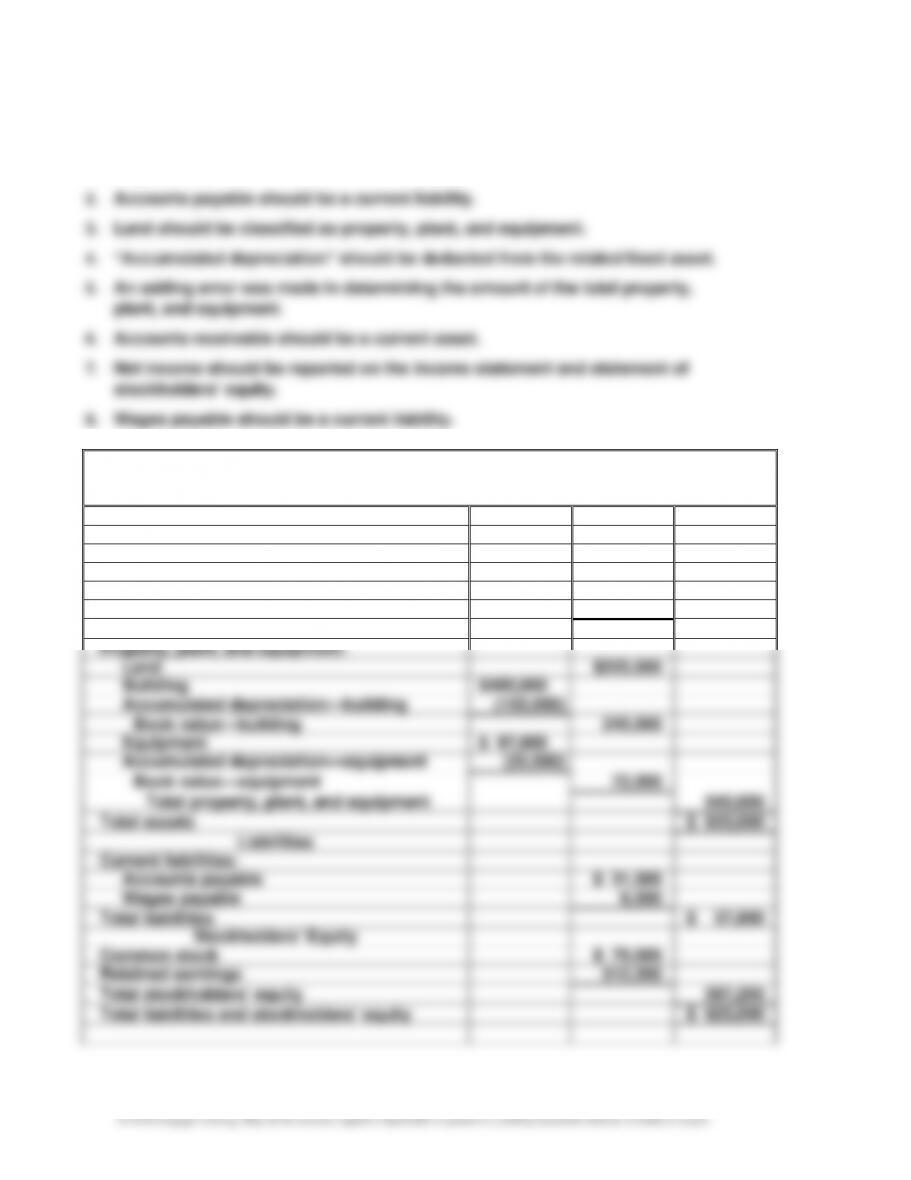

a. 1. The date of the statement should be “August 31, 20Y3” and not “For the Year Ended

August 31, 20Y3.”

b.

Labyrinth Services Co.

Balance Sheet

August 31, 20Y3

Assets

Current assets:

Cash

$ 18,500

Accounts receivable

41,400

Supplies

6,500

Prepaid insurance

16,600

Total current assets

$ 83,000

Property, plant, and equipment:

Land

$225,000

Building

$400,000

Accumulated depreciation—building

(155,000)

Book value—building

245,000

Equipment

$ 97,000

Accumulated depreciation—equipment

(25,000)

Book value—equipment

72,000

Total property, plant, and equipment

542,000

Total assets

$ 625,000

Liabilities

Current liabilities:

Accounts payable

$ 31,300

Wages payable

6,500

Total liabilities

$ 37,800

Stockholders’ Equity

Common stock

$ 75,000

Retained earnings

512,200

Total stockholders’ equity

587,200

Total liabilities and stockholders’ equity

$ 625,000

CHAPTER 4 The Accounting Cycle

4–11

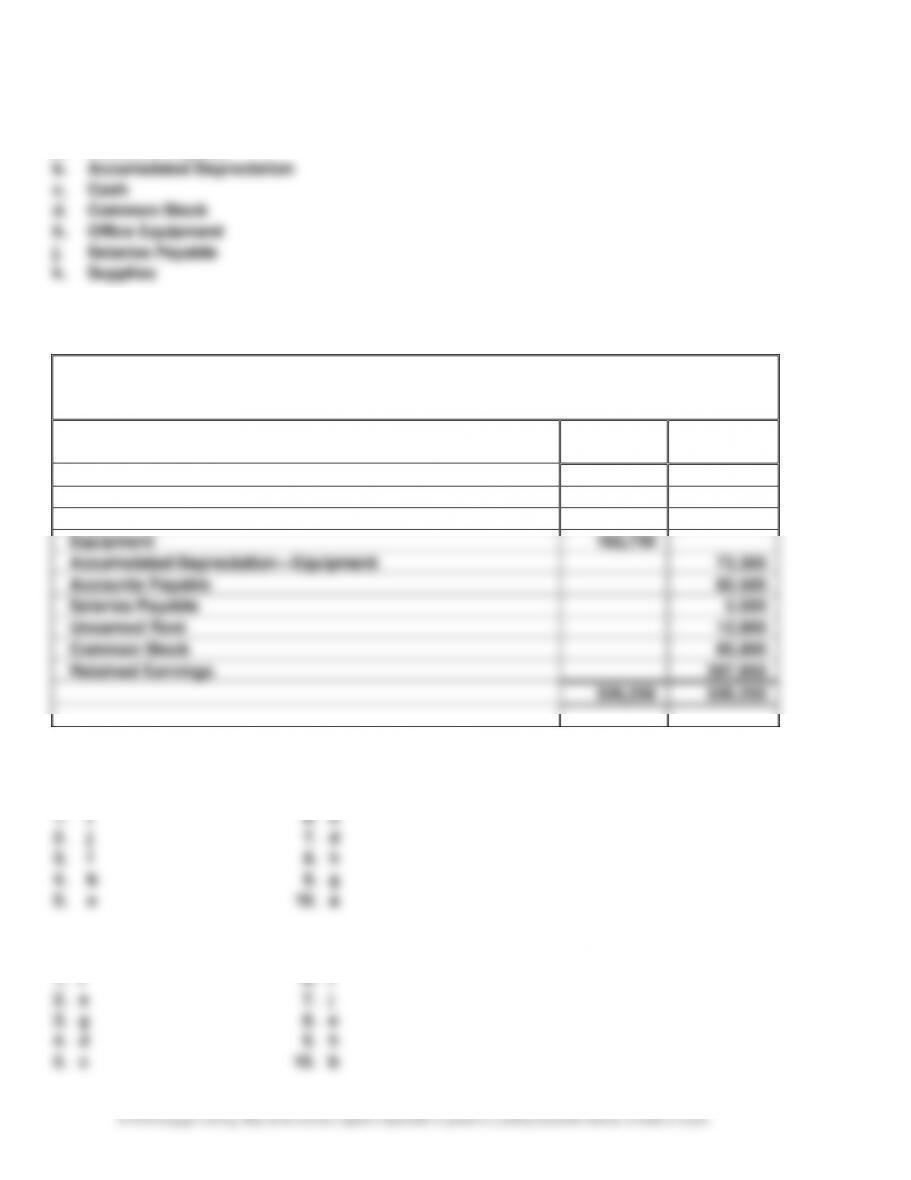

Ex. 4–14

c. Depreciation Expense—Equipment

Ex. 4–15

Closing Entries

Dec.

31

Fees Earned

614,500

Wages Expense

320,000

Rent Expense

140,000

Supplies Expense

18,200

Miscellaneous Expense

8,700

Retained Earnings

127,600

31

Retained Earnings

45,000

Dividends

45,000

Ex. 4–16

Closing Entries

May

31

Fees Earned

1,150,000

Retained Earnings

16,200

Wages Expense

915,000

Rent Expense

200,000

Supplies Expense

19,300

Miscellaneous Expense

31,900

31

Retained Earnings

5,000

Dividends

5,000

CHAPTER 4 The Accounting Cycle

4–12

Ex. 4–17

a. Accounts Payable

Ex. 4–18

Security Services Co.

Post-Closing Trial Balance

July 31, 20Y0

Debit

Credit

Balances

Balances

Cash

41,100

Accounts Receivable

317,400

Supplies

5,000

Equipment

162,750

Accumulated Depreciation—Equipment

73,300

Accounts Payable

82,500

Salaries Payable

5,500

Unearned Rent

12,000

Common Stock

65,000

Retained Earnings

287,950

526,250

526,250

Ex.

4–19

1.

i

6.

c

2.

j

7.

d

3.

f

8.

h

4.

b

9.

g

5.

e

10.

a

Appendix 1 Ex. 4–20

1.

i

6.

f

2.

a

7.

j

3.

g

8.

e

4.

d

9.

h

5.

c

10.

b

CHAPTER 4 The Accounting Cycle

4–13

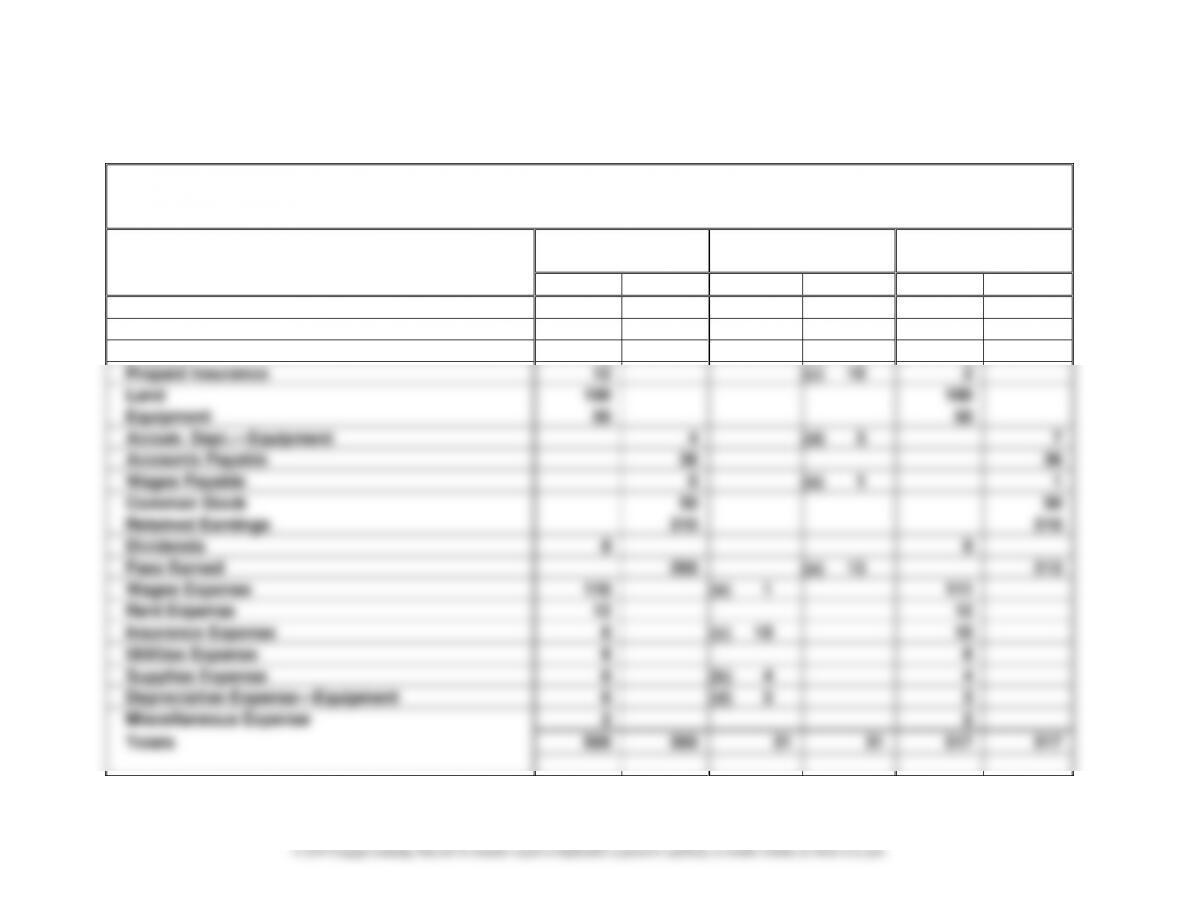

Appendix 1 Ex. 4–21

Alert Security Services Co.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 20Y3

Account Title

Unadjusted

Trial Balance

Adjustments

Adjusted

Trial Balance

Debit

Credit

Debit

Credit

Debit

Credit

Cash

12

12

Accounts Receivable

90

(a) 13

103

Supplies

8

(b) 4

4

Prepaid Insurance

12

(c) 10

2

Land

190

190

Equipment

50

50

Accum. Depr.—Equipment

4

(d) 3

7

Accounts Payable

36

36

Wages Payable

0

(e) 1

1

Common Stock

50

50

Retained Earnings

210

210

Dividends

8

8

Fees Earned

200

(a) 13

213

Wages Expense

110

(e) 1

111

Rent Expense

12

12

Insurance Expense

0

(c) 10

10

Utilities Expense

6

6

Supplies Expense

0

(b) 4

4

Depreciation Expense—Equipment

0

(d) 3

3

Miscellaneous Expense

2

2

Totals

500

500

31

31

517

517

CHAPTER 4 The Accounting Cycle

4–14

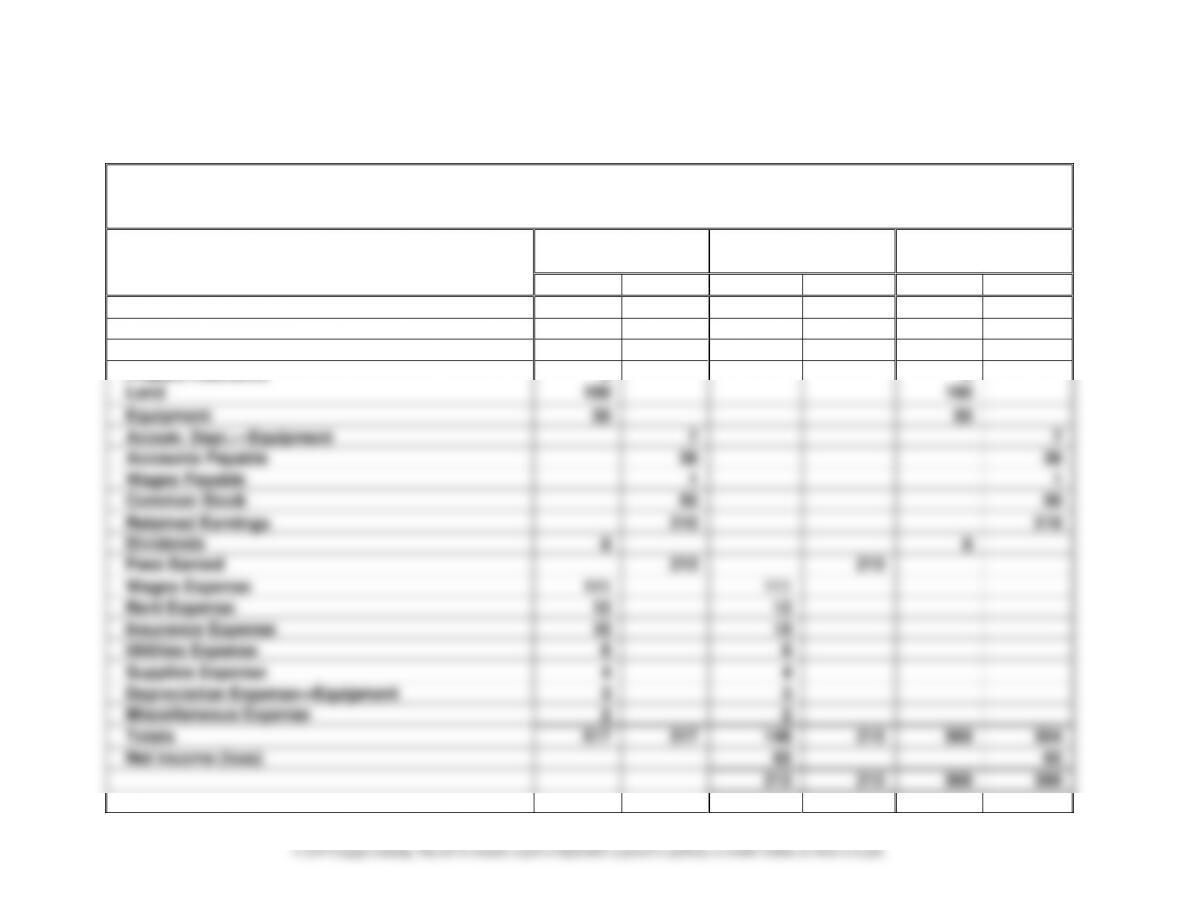

Appendix 1 Ex. 4–22

Alert Security Services Co.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended October 31, 20Y3

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Account Title

Debit

Credit

Debit

Credit

Debit

Credit

Cash

12

12

Accounts Receivable

103

103

Supplies

4

4

Prepaid Insurance

2

2

Land

190

190

Equipment

50

50

Accum. Depr.—Equipment

7

7

Accounts Payable

36

36

Wages Payable

1

1

Common Stock

50

50

Retained Earnings

210

210

Dividends

8

8

Fees Earned

213

213

Wages Expense

111

111

Rent Expense

12

12

Insurance Expense

10

10

Utilities Expense

6

6

Supplies Expense

4

4

Depreciation Expense—Equipment

3

3

Miscellaneous Expense

2

2

Totals

517

517

148

213

369

304

Net income (loss)

65

65

213

213

369

369

CHAPTER 4 The Accounting Cycle

4–15

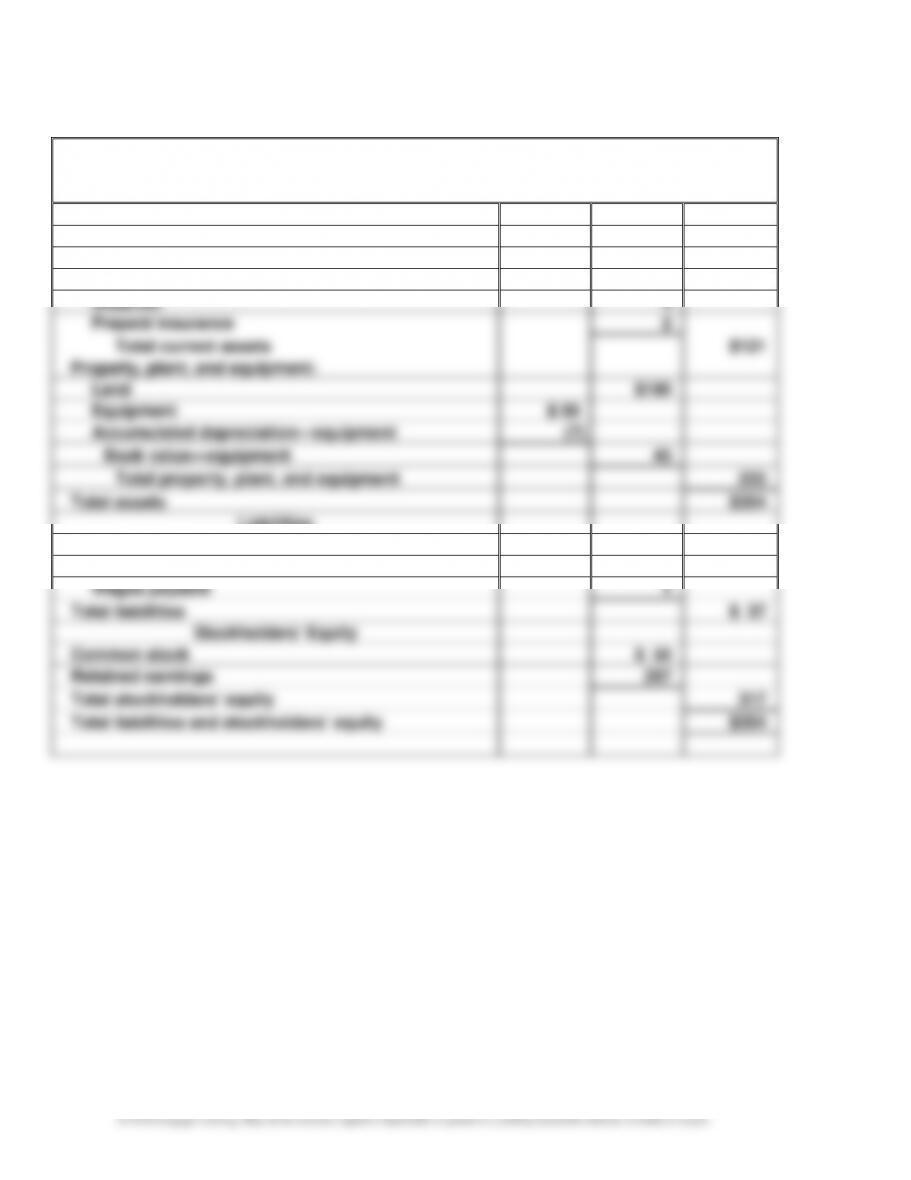

Appendix 1 Ex. 4–23

Alert Security Services Co.

Income Statement

For the Year Ended October 31, 20Y3

Fees earned

$ 213

Expenses:

Wages expense

$111

Rent expense

12

Insurance expense

10

Utilities expense

6

Supplies expense

4

Depreciation expense—equipment

3

Miscellaneous expense

2

Total expenses

(148)

Net income

$ 65

Alert Security Services Co.

Statement of Stockholders’ Equity

For the Year Ended October 31, 20Y3

Common

Stock

Retained

Earnings

Total

Balances, November 1, 20Y2

$40

$210

$250

Issued common stock

10

10

Net income

65

65

Dividends

(8)

(8)

Balances, October 31, 20Y3

$50

$267

$317

CHAPTER 4 The Accounting Cycle

4–16

Appendix 1 Ex. 4–23 (Concluded)

Alert Security Services Co.

Balance Sheet

October 31, 20Y3

Assets

Current assets:

Cash

$ 12

Accounts receivable

103

Supplies

4

Prepaid insurance

2

Total current assets

$121

Property, plant, and equipment:

Land

$190

Equipment

$ 50

Accumulated depreciation—equipment

(7)

Book value—equipment

43

Total property, plant, and equipment

233

Total assets

$354

Liabilities

Current liabilities:

Accounts payable

$ 36

Wages payable

1

Total liabilities

$ 37

Stockholders’ Equity

Common stock

$ 50

Retained earnings

267

Total stockholders’ equity

317

Total liabilities and stockholders’ equity

$354

CHAPTER 4 The Accounting Cycle

4–17

Appendix 1 Ex. 4–24

20Y3

Adjusting Entries

Oct.

31

Accounts Receivable

13

Fees Earned

13

Accrued fees.

31

Supplies Expense

4

Supplies

4

Supplies used ($8 – $4).

31

Insurance Expense

10

Prepaid Insurance

10

Insurance expired.

31

Depreciation Expense—Equipment

3

Accumulated Depreciation—Equipment

3

Equipment depreciation.

31

Wages Expense

1

Wages Payable

1

Accrued wages.

Appendix 1 Ex. 4–25

20Y3

Closing Entries

Oct.

31

Fees Earned

213

Wages Expense

111

Rent Expense

12

Insurance Expense

10

Utilities Expense

6

Supplies Expense

4

Depreciation Expense—Equipment

3

Miscellaneous Expense

2

Retained Earnings

65

31

Retained Earnings

8

Dividends

8

CHAPTER 4 The Accounting Cycle

4–18

Appendix 2 Ex. 4–26

a.

Jan.

1

Wages Payable

5,500

Wages Expense

5,500

b.

Jan.

6

Wages Expense

61,375

Cash

61,375

c.

Jan.

6

Wages Expense

55,875

Wages Payable

5,500

Cash

61,375

d. $55,875 ($61,375 – $5,500)

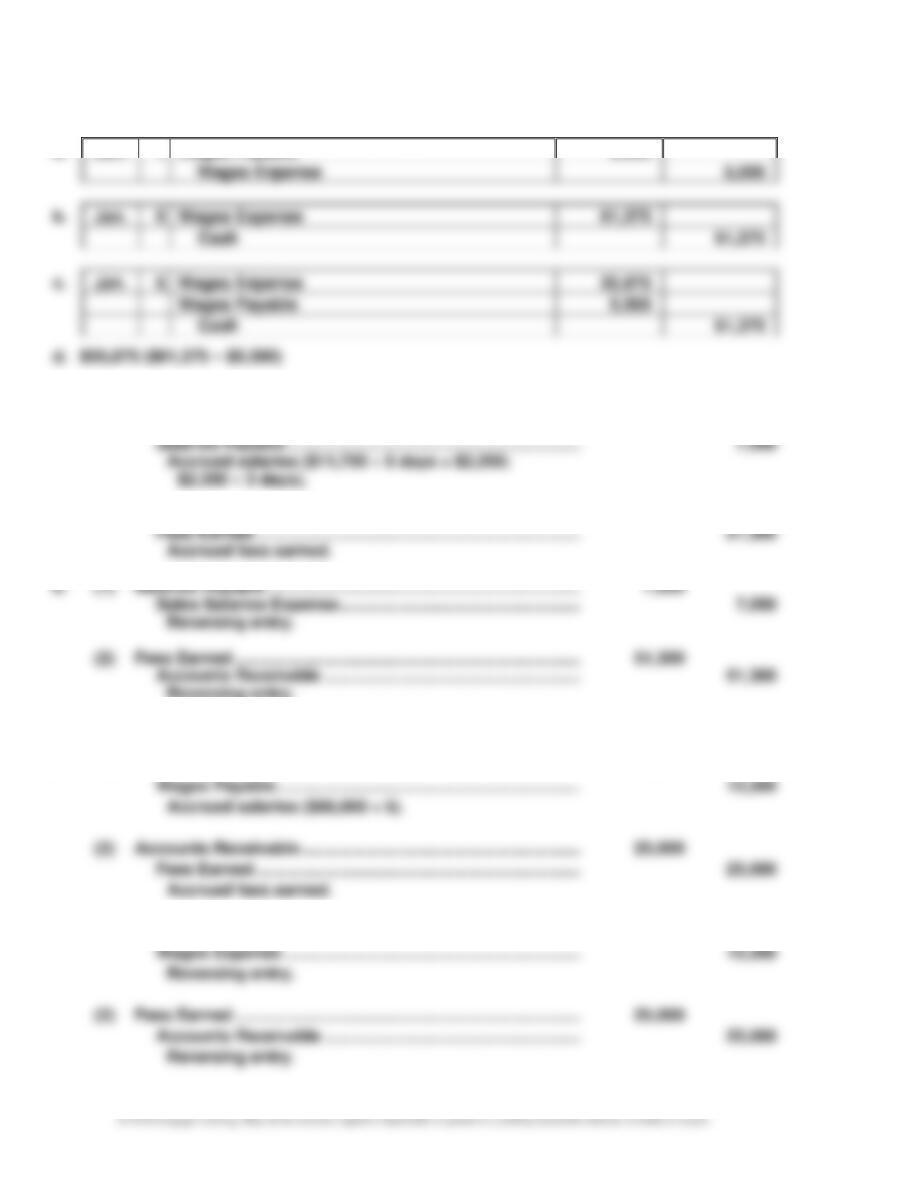

Appendix 2 Ex. 4–27

a.

(1)

Sales Salaries Expense ………………………………………………..

7,050

Salaries Payable ………………………………………………………

7,050

Accrued salaries ($11,750 5 days = $2,350;

$2,350 3 days).

(2)

Accounts Receivable ……………………………………………………

51,300

Fees Earned …………………………………………………………….

51,300

Accrued fees earned.

b.

(1)

Salaries Payable …………………………………………………………..

7,050

Sales Salaries Expense …………………………………………….

7,050

Reversing entry.

(2)

Fees Earned ………………………………………………………………..

51,300

Accounts Receivable ……………………………………………….

51,300

Reversing entry.

Appendix 2 Ex. 4–28

a.

(1)

Wages Expense ……………………………………………………………

13,200

Wages Payable ………………………………………………………..

13,200

Accrued salaries ($66,000 ÷ 5).

(2)

Accounts Receivable ……………………………………………………

25,000

Fees Earned …………………………………………………………….

25,000

Accrued fees earned.

b.

(1)

Wages Payable …………………………..………………………………..

13,200

Wages Expense ……………………………………………………….

13,200

Reversing entry.

(2)

Fees Earned ………………………………………………………………..

25,000

Accounts Receivable ……………………………………………….

25,000

Reversing entry.

CHAPTER 4 The Accounting Cycle

4–19

Appendix 2 Ex. 4–29

a. (1) Payment (last payday in year)

b.

(1)

Wages Expense ……………………………………………………………

15,400

Cash ……………………………………………………………………….

15,400

Paid wages.

(2)

Wages Expense ……………………………………………………………

9,250

Wages Payable ………………………………………………………..

9,250

Accrued wages.

(3)

Retained Earnings (Closing Entry) ………………………………..

809,250

Wages Expense ……………………………………………………….

809,250

Closing entry.

(4)

Wages Payable …………………………………………………………….

9,250

Wages Expense ……………………………………………………….

9,250

Reversing entry.

(5)

Wages Expense ……………………………………………………………

14,800

Cash ……………………………………………………………………….

14,800

Paid wages.

Appendix 2 Ex. 4–30

a. (1) Payment (last payday in year)

b.

(1)

Salaries Expense ………………………………………………………….

22,000

Cash ……………………………………………………………………….

22,000

Paid salaries.

(2)

Salaries Expense ………………………………………………………….

13,200

Salaries Payable ………………………………………………………

13,200

Accrued salaries.

(3)

Retained Earnings (Closing Entry) ………………………………..

1,213,200

Salaries Expense ……………………………………………………..

1,213,200

Closing entry.

(4)

Salaries Payable …………………………………………………………..

13,200

Salaries Expense ……………………………………………………..

13,200

Reversing entry.

(5)

Salaries Expense ………………………………………………………….

24,000

Cash ……………………………………………………………………….

24,000

Paid salaries.

CHAPTER 4 The Accounting Cycle

PROBLEMS

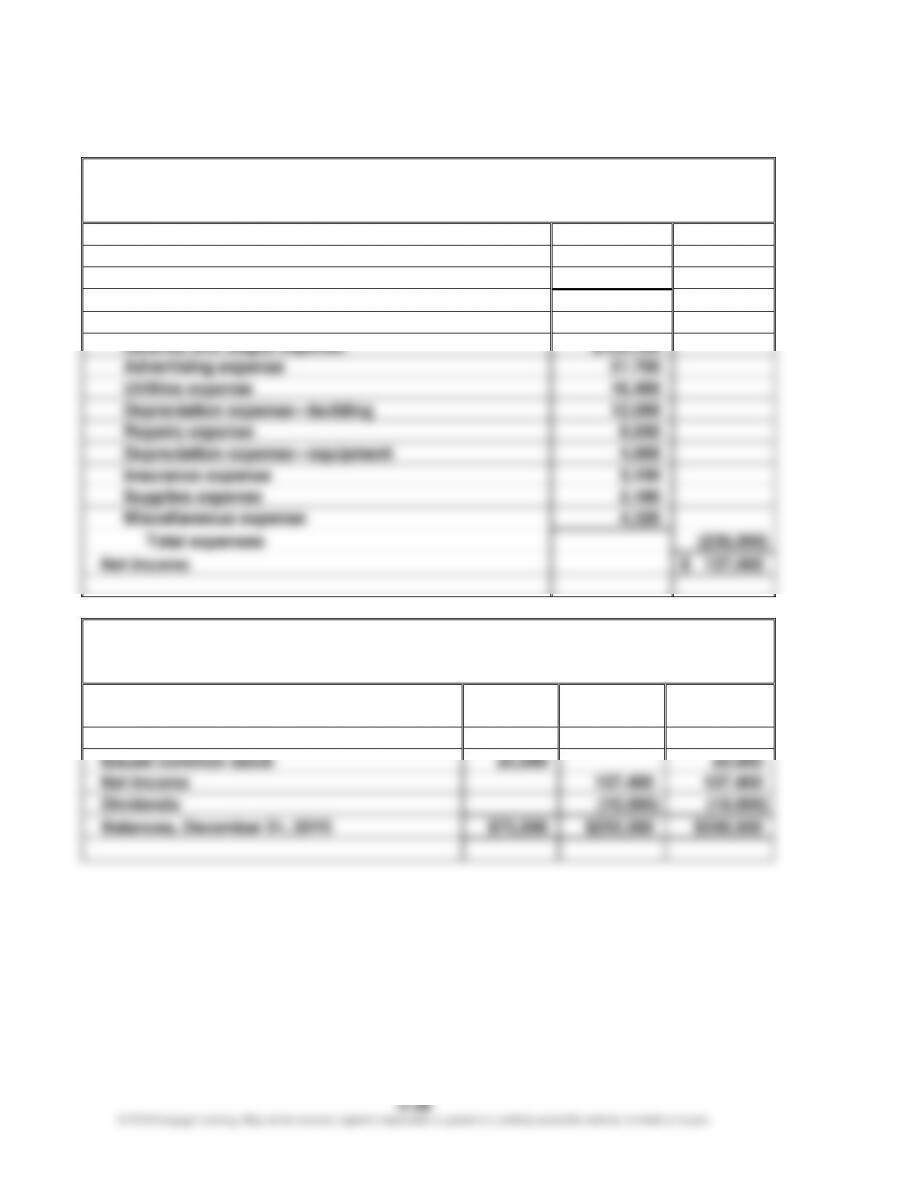

Prob. 4–1A

1.

Beacons Company

Income Statement

For the Year Ended December 31, 20Y5

Revenues:

Fees earned

$372,800

Rent revenue

1,100

Total revenues

$ 373,900

Expenses:

Salaries and wages expense

$163,100

Advertising expense

21,700

Utilities expense

16,400

Depreciation expense—building

12,000

Repairs expense

8,850

Depreciation expense—equipment

4,800

Insurance expense

3,150

Supplies expense

2,180

Miscellaneous expense

4,320

Total expenses

(236,500)

Net income

$ 137,400

2.

Beacons Company

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y5

Common

Stock

Retained

Earnings

Total

Balances, January 1, 20Y5

$50,000

$128,100

$178,100

Issued common stock

25,000

25,000

Net income

137,400

137,400

Dividends

(10,000)

(10,000)

Balances, December 31, 20Y5

$75,000

$255,500

$330,500