CHAPTER 2 Analyzing Transactions

2–54

Continuing Problem (Continued)

1. and 3.

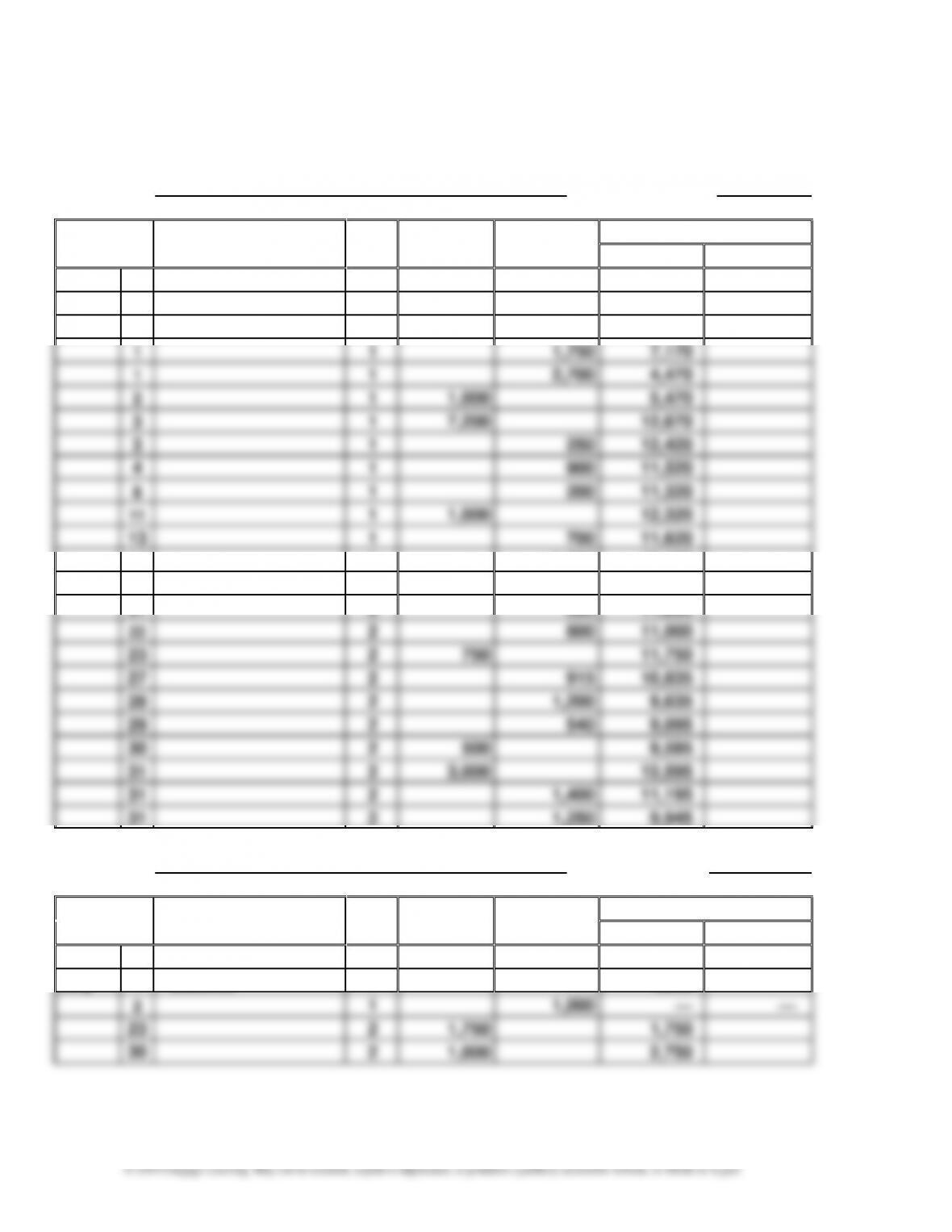

Account:

Cash

Account No.

11

Date

Item

Post.

Ref.

Debit

Balance

Credit

Debit

Credit

20Y5

July

1

Balance

✓

3,920

1

1

5,000

8,920

1

1

1,750

7,170

1

1

2,700

4,470

2

1

1,000

5,470

3

1

7,200

12,670

3

1

250

12,420

4

1

900

11,520

8

1

200

11,320

11

1

1,000

12,320

13

1

700

11,620

14

1

1,200

10,420

16

2

2,000

12,420

21

2

620

11,800

22

2

800

11,000

23

2

750

11,750

27

2

915

10,835

28

2

1,200

9,635

29

2

540

9,095

30

2

500

9,595

31

2

3,000

12,595

31

2

1,400

11,195

31

2

1,250

9,945

Account:

Accounts Receivable

Account No.

12

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

1,000

2

1

1,000

—

—

23

2

1,750

1,750

30

2

1,000

2,750

CHAPTER 2 Analyzing Transactions

2–55

Continuing Problem (Continued)

Account:

Supplies

Account No.

14

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

170

18

2

850

1,020

Account:

Prepaid Insurance

Account No.

15

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

1

2,700

2,700

Account:

Office Equipment

Account No.

17

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

5

1

7,500

7,500

Account:

Accounts Payable

Account No.

21

Date

Item

Post.

Ref.

Debit

Balance

Credit

Debit

Credit

20Y5

July

1

Balance

✓

250

3

1

250

—

—

5

1

7,500

7,500

18

2

850

8,350

Account:

Unearned Revenue

Account No.

23

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

3

1

7,200

7,200

Account:

Common Stock

Account No.

31

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

4,000

1

1

5,000

9,000

CHAPTER 2 Analyzing Transactions

2–56

Continuing Problem (Continued)

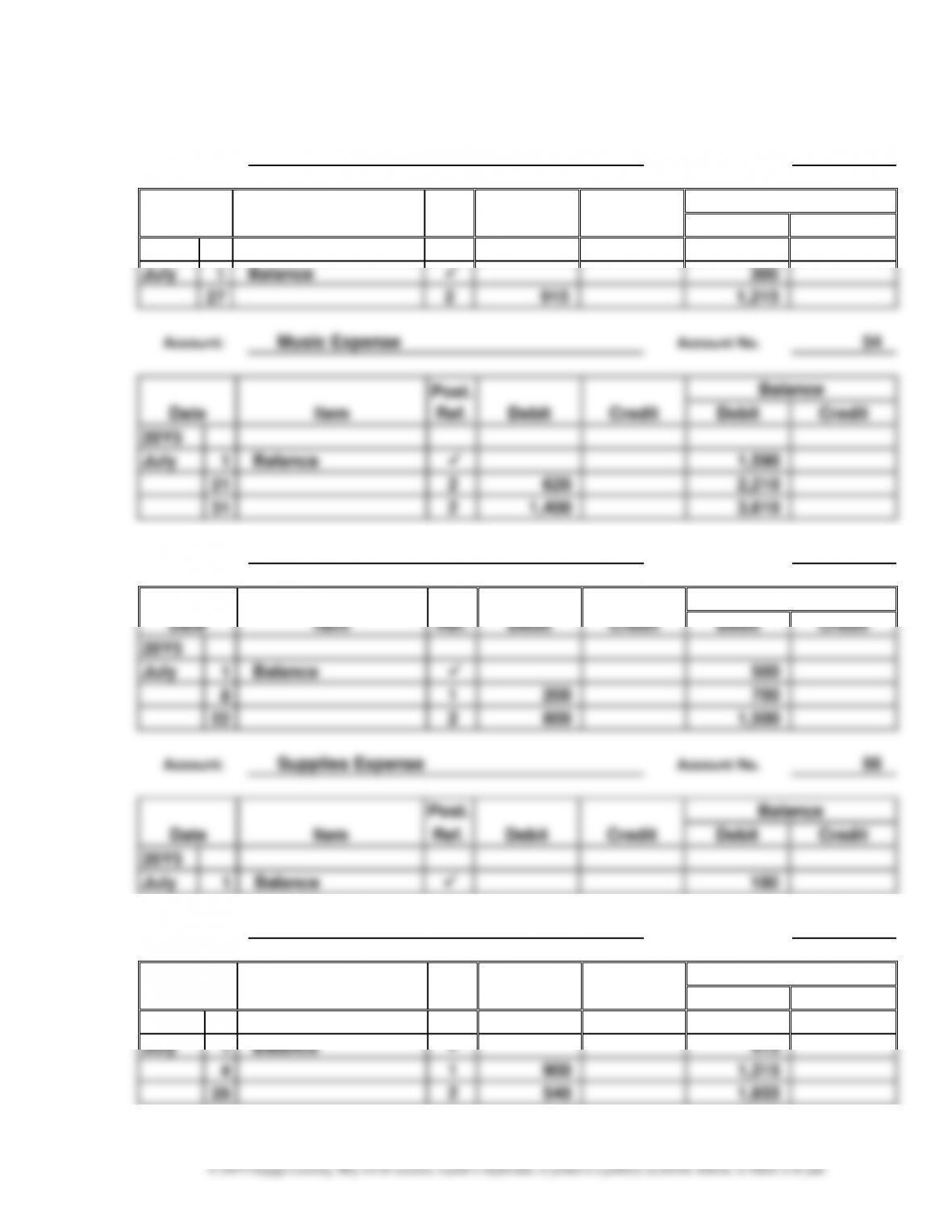

Account:

Dividends

Account No.

33

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

500

31

2

1,250

1,750

Account:

Fees Earned

Account No.

41

Date

Item

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

20Y5

July

1

Balance

✓

6,200

11

1

1,000

7,200

16

2

2,000

9,200

23

2

2,500

11,700

30

2

1,500

13,200

31

2

3,000

16,200

Account:

Wages Expense

Account No.

50

Date

Item

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

20Y5

July

1

Balance

✓

400

14

1

1,200

1,600

28

2

1,200

2,800

Account:

Office Rent Expense

Account No.

51

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

800

1

1

1,750

2,550

Account:

Equipment Rent Expense

Account No.

52

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

675

13

1

700

1,375

CHAPTER 2 Analyzing Transactions

2–57

Continuing Problem (Continued)

Account:

Utilities Expense

Account No.

53

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

300

27

2

915

1,215

Account:

Music Expense

Account No.

54

Date

Item

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

20Y5

July

1

Balance

✓

1,590

21

2

620

2,210

31

2

1,400

3,610

Account:

Advertising Expense

Account No.

55

Date

Item

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

20Y5

July

1

Balance

✓

500

8

1

200

700

22

2

800

1,500

Account:

Supplies Expense

Account No.

56

Post.

Balance

Date

Item

Ref.

Debit

Credit

Debit

Credit

20Y5

July

1

Balance

✓

180

Account:

Miscellaneous Expense

Account No.

59

Date

Item

Post.

Ref.

Debit

Credit

Balance

Debit

Credit

20Y5

July

1

Balance

✓

415

4

1

900

1,315

29

2

540

1,855

CHAPTER 2 Analyzing Transactions

2–58

Continuing Problem (Concluded)

4.

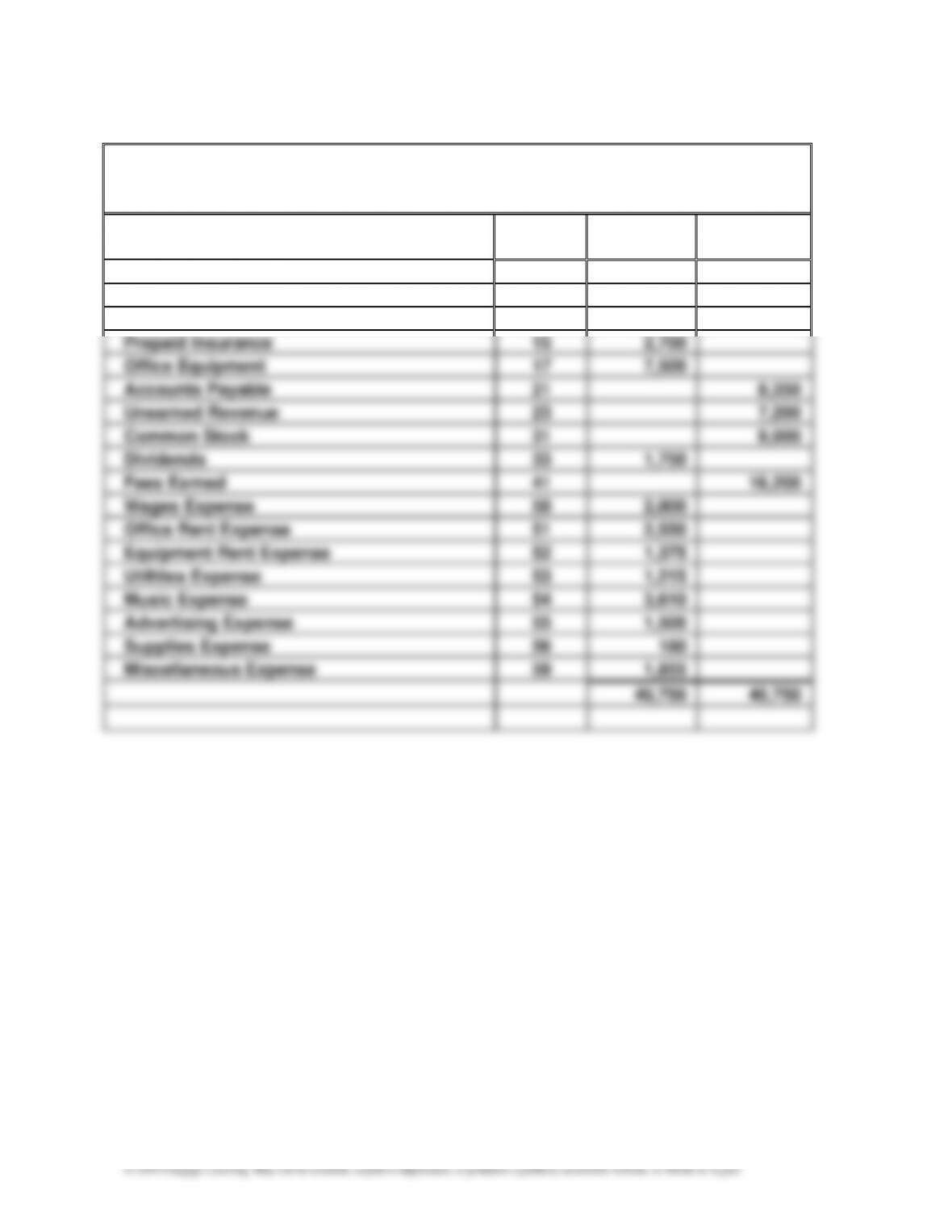

PS Music

Unadjusted Trial Balance

July 31, 20Y5

Account

Debit

Credit

No.

Balances

Balances

Cash

11

9,945

Accounts Receivable

12

2,750

Supplies

14

1,020

Prepaid Insurance

15

2,700

Office Equipment

17

7,500

Accounts Payable

21

8,350

Unearned Revenue

23

7,200

Common Stock

31

9,000

Dividends

33

1,750

Fees Earned

41

16,200

Wages Expense

50

2,800

Office Rent Expense

51

2,550

Equipment Rent Expense

52

1,375

Utilities Expense

53

1,215

Music Expense

54

3,610

Advertising Expense

55

1,500

Supplies Expense

56

180

Miscellaneous Expense

59

1,855

40,750

40,750

CHAPTER 2 Analyzing Transactions

MAKE A DECISION

MAD 2–1

a.

Amazon.com, Inc.

Income Statements

For the Years Ended December 31

(in millions)

Increase/(Decrease)

Year 2

Year 1

Amount

Percent

Revenues:

Product sales

$ 94,665

$ 79,268

$ 15,397

19.4%

Service sales

41,322

27,738

13,584

49.0%

Total revenues

$ 135,987

$ 107,006

$ 28,981

27.1%

Operating expenses:

Cost of sales

$ (88,265)

$ (71,651)

16,614

23.2%

Fulfillment

(17,619)

(13,410)

4,209

31.4%

Marketing

(7,233)

(5,254)

1,979

37.7%

Technology and content

(16,085)

(12,540)

3,545

28.3%

General and administrative

(2,432)

(1,747)

685

39.2%

Other operating expense

(income), net

(167)

(171)

(4)

(2.3)%

Total operating expenses

$(131,801)

$(104,773)

$ 27,028

25.8%

Operating income

$ 4,186

$ 2,233

$ 1,953

87.5%

b. The horizontal analysis shows that total revenues increased by 27.1% between the two

years, with a strong increase in service sales. Service sales are revenues earned from

2–60

MAD 2–3

a.

Chipotle Mexican Grill, Inc.

Income Statements

For the Years Ended December 31

(in thousands)

Year 2

Year 1

Increase/(Decrease)

Amount

Percent

Revenue

$ 3,904,384

$ 4,501,223

$(596,839)

(13.3)%

Expenses:

Food, beverage, packing

$(1,365,580)

$(1,503,835)

$(138,255)

(9.2)%

Labor

(1,105,001)

(1,045,726)

59,275

5.7%

Rent (occupancy)

(293,636)

(262,412)

31,224

11.9%

General and administrative

(641,953)

(514,963)

126,990

24.7%

Other

(463,647)

(410,698)

52,949

12.9%

Total expenses

$(3,869,817)

$(3,737,634)

$ 132,183

3.5%

Operating income

$ 34,567

$ 763,589

$(729,022)

(95.5)%

b. Revenue decreased by 13.3% in Year 2, while total expenses increased 3.5%. Food,

c. The significant decrease in revenue and operating income in Year 2 was caused by

CHAPTER 2 Analyzing Transactions

2–61

MAD 2–4

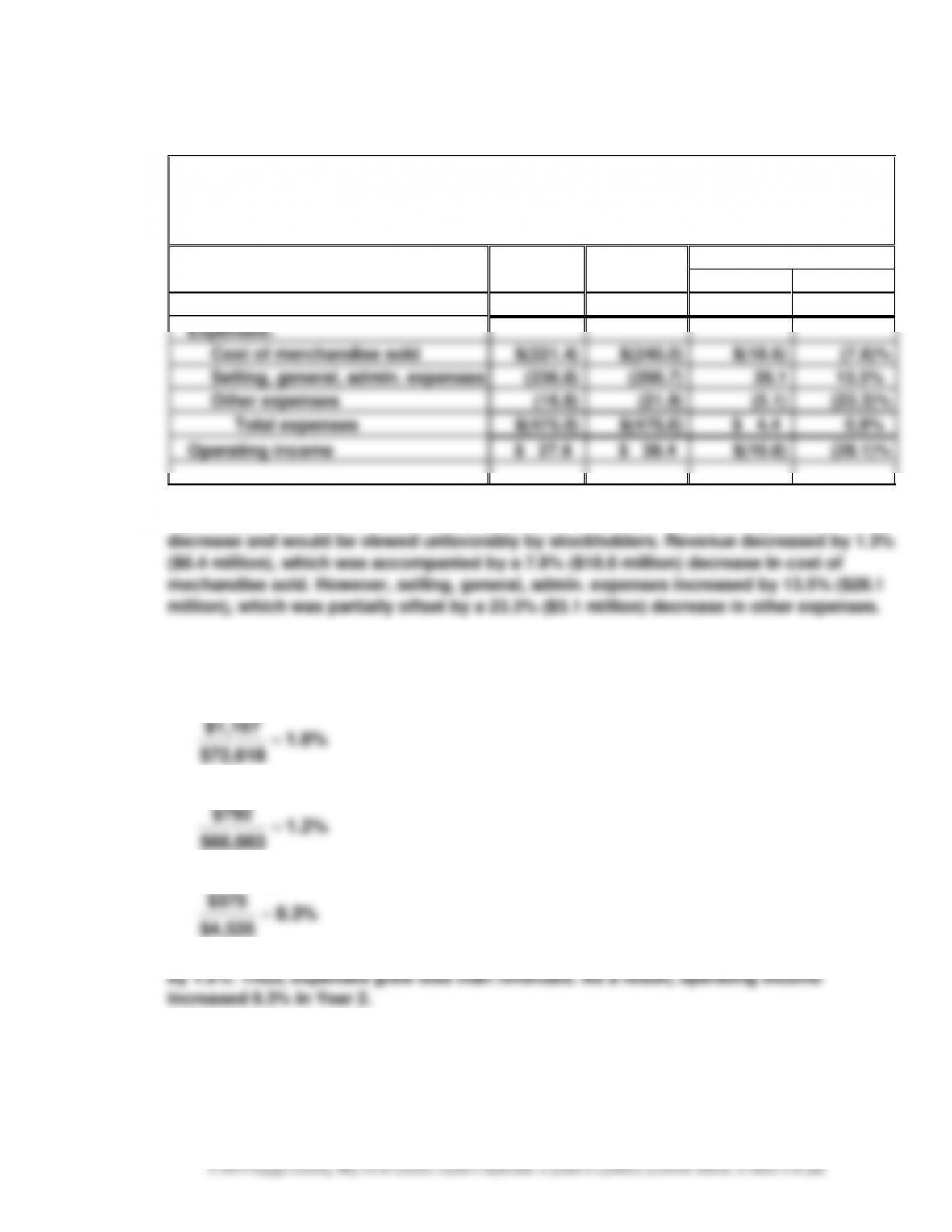

a.

Vera Bradley, Inc.

Income Statements

For the Years Ended January 31

(in millions)

Year 2

Year 1

Increase/(Decrease)

Amount

Percent

Revenue

$ 502.6

$ 509.0

$ (6.4)

(1.3)%

Expenses:

Cost of merchandise sold

$(221.4)

$(240.0)

$(18.6)

(7.8)%

Selling, general, admin. expenses

(236.8)

(208.7)

28.1

13.5%

Other expenses

(16.8)

(21.9)

(5.1)

(23.3)%

Total expenses

$(475.0)

$(470.6)

$ 4.4

0.9%

Operating income

$ 27.6

$ 38.4

$(10.8)

(28.1)%

b. Operating income decreased $10.8 million or 28.1% in Year 2. This is a significant

MAD 2–4

a. 1. Revenue: $73,785 – $72,618 = $1,167

1.6%

$72,618

$1,167 =

2. Operating expenses: $68,875 – $68,083 = $792

1.2%

$68,083

$792 =

3. Operating income: $4,910 – $4,535 = $375

8.3%

$4,535

$375 =

b. The revenue increased by 1.6% between the two years, while the operating expenses grew

CHAPTER 2 Analyzing Transactions

2–62

MAD 2–5

a. 1. Revenue: $482,130 – $485,651 = $(3,521)

(0.7)%

$485,651

$(3,521) =

2. Operating expenses: $458,025 – $458,504 = $(479)

(0.1)%

$458,504

$(479) =

3. Operating income: $24,105 – $27,147 = $(3,042)

(11.2)%

$27,147

$(3,042) =

b. Revenue decreased by 0.7%, while operating expenses decreased only 0.1%. As a result,

MAD 2–6

CHAPTER 2 Analyzing Transactions

2–63

TAKE IT FURTHER

TIF 2–1

1. No. For financial accounting information to be useful, it must accurately reflect an entity’s

3. Buddy should have discussed the issue with his supervisor and asked for more time to

find the error.

TIF 2–2

A sample solution based on Apple Inc.’s Form 10-K for the fiscal year ended

September 24, 2016, follows:

1. $321,686 million

CHAPTER 2 Analyzing Transactions

TIF 2–3

Note to Instructors: The purpose of this activity is to familiarize students with the job

opportunities available in accounting, and allow them to demonstrate their ability to

communicate the role of accounting in the context of a specific position that requires

knowledge of accounting. An example of an advertisement for such a position is shown

below. Individual student answers will vary depending on the specific scenario they select.

ABOUT THE COMPANY

Our client is looking to add a Financial Analyst. With a large and growing finance team, there

is significant opportunity for growth and advancement within the department.

RESPONSIBILITIES OF THE FINANCIAL ANALYST

The Financial Analyst will:

• Conduct special studies to analyze complex financial actions and prepare

2–65

TIF 2–4

The following general journal entry should be used to record the receipt of tuition payments

received in advance of classes:

TIF 2–5

The journal is called the book of original entry. It provides a time-ordered history of the

transactions that have occurred for the firm. This time-ordered history is very important

because it allows one to trace ledger account balances back to the original transactions that

CHAPTER 2 Analyzing Transactions

2–66

TIF 2–6

1. The rules of debit and credit must be memorized. Dot is correct in that the rules of

debit and credit could be reversed as long as everyone accepted and abided by the

rules. However, the important point is that everyone accepts the rules as the way in

which transactions should be recorded. This generates uniformity across the

2. The accounting system may be designed to capture information about the buying

habits of various customers or vendors, such as the quantity normally ordered,