CHAPTER 14 Financial Statement Analysis

14–39

Prob. 14–2B

1.

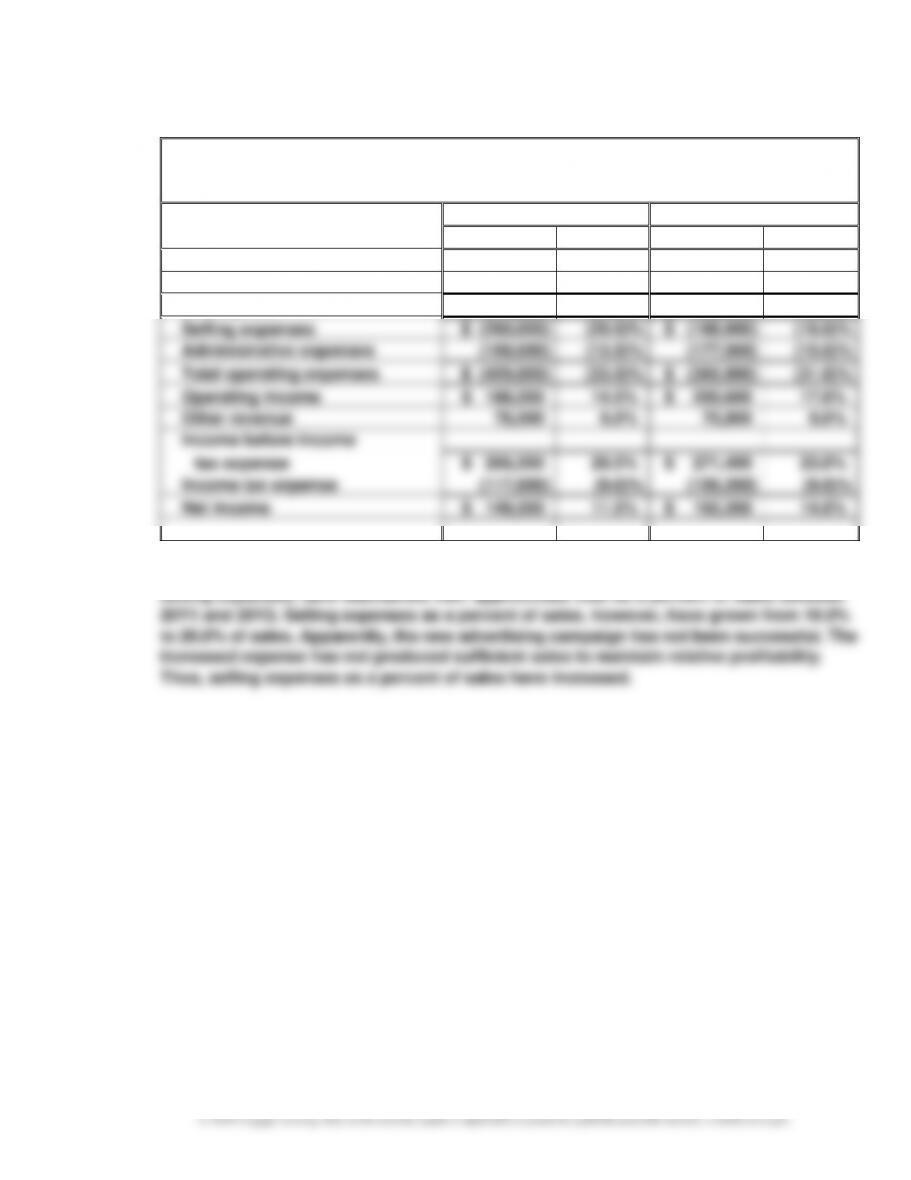

Fielder Industries Inc.

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

20Y2

20Y1

Amount

Percent

Amount

Percent

Sales

$1,300,000

100.0%

$ 1,180,000

100.0%

Cost of goods sold

(682,500)

(52.5)%

(613,600)

(52.0)%

Gross profit

$ 617,500

47.5%

$ 566,400

48.0%

Selling expenses

$ (260,000)

(20.0)%

$ (188,800)

(16.0)%

Administrative expenses

(169,000)

(13.0)%

(177,000)

(15.0)%

Total operating expenses

$ (429,000)

(33.0)%

$ (365,800)

(31.0)%

Operating income

$ 188,500

14.5%

$ 200,600

17.0%

Other revenue

78,000

6.0%

70,800

6.0%

Income before income

tax expense

$ 266,500

20.5%

$ 271,400

23.0%

Income tax expense

(117,000)

(9.0)%

(106,200)

(9.0)%

Net income

$ 149,500

11.5%

$ 165,200

14.0%

2. The net income as a percent of sales has declined. All the costs and expenses, other than

selling expenses, have maintained their approximate cost as a percent of sales between

CHAPTER 14 Financial Statement Analysis

14–40

Prob. 14–3B

1. a. Working Capital = Current Assets – Current Liabilities

1.1

$2,000,000

2. Supporting Data

Transaction

Working

Capital

Current

Ratio

Quick

Ratio

Current

Assets

Quick

Assets

Current

Liabilities

a.

$1,200,000

1.6

1.1

$3,200,000

$2,200,000

$2,000,000

b.

1,200,000

1.7

1.1

2,912,500

1,912,500

1,712,500

c.

1,200,000

1.5

0.9

3,600,000

2,200,000

2,400,000

d.

1,200,000

1.6

1.1

3,075,000

2,075,000

1,875,000

e.

875,000

1.4

0.9

3,200,000

2,200,000

2,325,000

f.

1,200,000

1.6

1.1

3,200,000

2,200,000

2,000,000

g.

2,200,000

2.1

1.6

4,200,000

3,200,000

2,000,000

h.

1,200,000

1.6

1.1

3,200,000

2,200,000

2,000,000

i.

3,200,000

2.6

2.1

5,200,000

4,200,000

2,000,000

j.

1,200,000

1.6

1.0

3,200,000

2,000,000

2,000,000

CHAPTER 14 Financial Statement Analysis

14–41

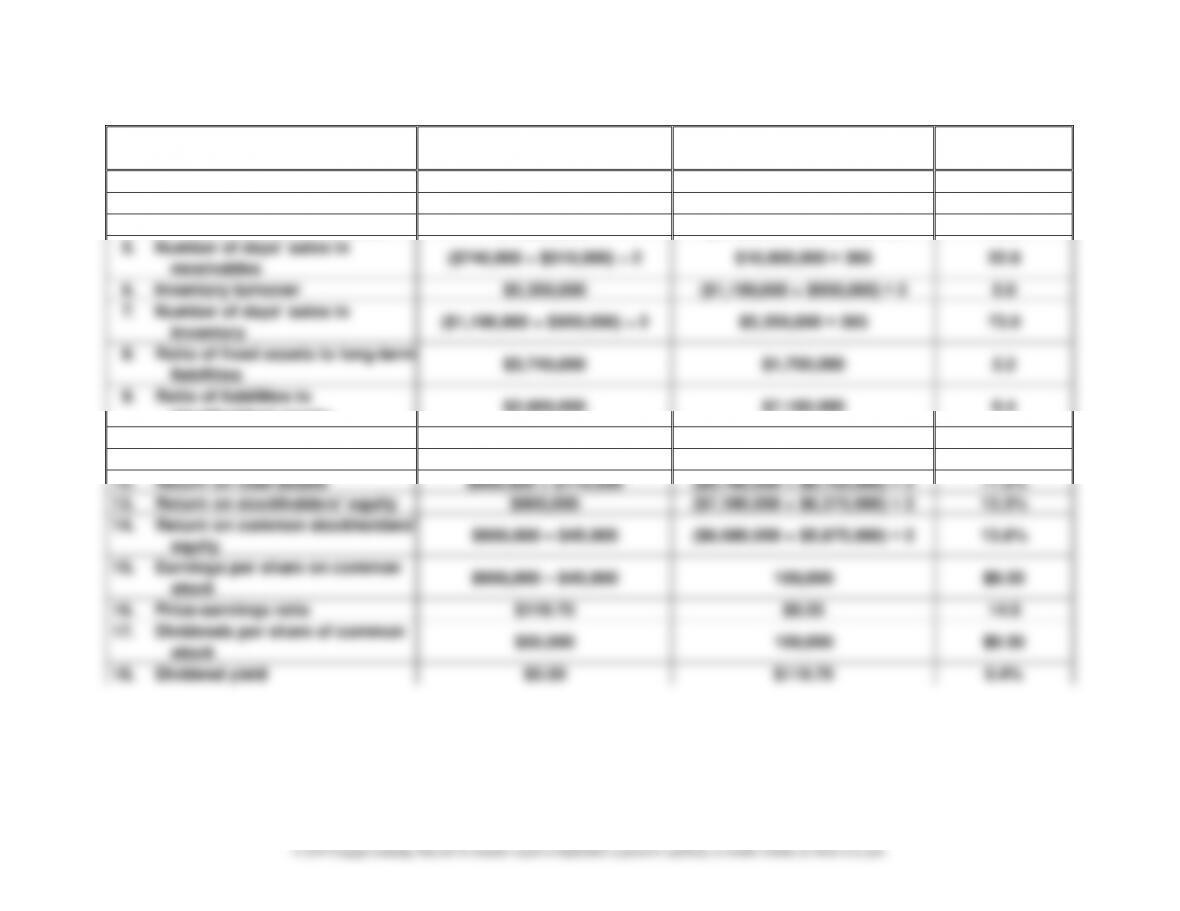

Prob.14–4B

1. Working Capital: $3,690,000 – $900,000 = $2,790,000

Calculated

Value

Ratio

Numerator

Denominator

2.

Current ratio

$3,690,000

$900,000

4.1

3.

Quick ratio

$2,250,000

$900,000

2.5

4.

Accounts receivable turnover

$10,000,000

($740,000 + $510,000) ÷ 2

16.0

5.

Number of days’ sales in

receivables

($740,000 + $510,000) ÷ 2

$10,000,000 ÷ 365

22.8

6.

Inventory turnover

$5,350,000

($1,190,000 + $950,000) ÷ 2

5.0

7.

Number of days’ sales in

inventory

($1,190,000 + $950,000) ÷ 2

$5,350,000 ÷ 365

73.0

8.

Ratio of fixed assets to long-term

liabilities

$3,740,000

$1,700,000

2.2

9.

Ratio of liabilities to

stockholders’ equity

$2,600,000

$7,180,000

0.4

10.

Times interest earned

$1,130,000 + $170,000

$170,000

7.6

11.

Asset turnover

$10,000,000

($7,430,000 + $6,455,000) ÷ 2

1.4

12.

Return on total assets

$900,000 + $170,000

($9,780,000 + $8,755,000) ÷ 2

11.5%

13.

Return on stockholders’ equity

$900,000

($7,180,000 + $6,375,000) ÷ 2

13.3%

14.

Return on common stockholders’

equity

$900,000 – $45,000

($6,680,000 + $5,875,000) ÷ 2

13.6%

15.

Earnings per share on common

stock

$900,000 – $45,000

100,000

$8.55

16.

Price-earninqs ratio

$119.70

$8.55

14.0

17.

Dividends per share of common

stock

$50,000

100,000

$0.50

18.

Dividend yield

$0.50

$119.70

0.4%

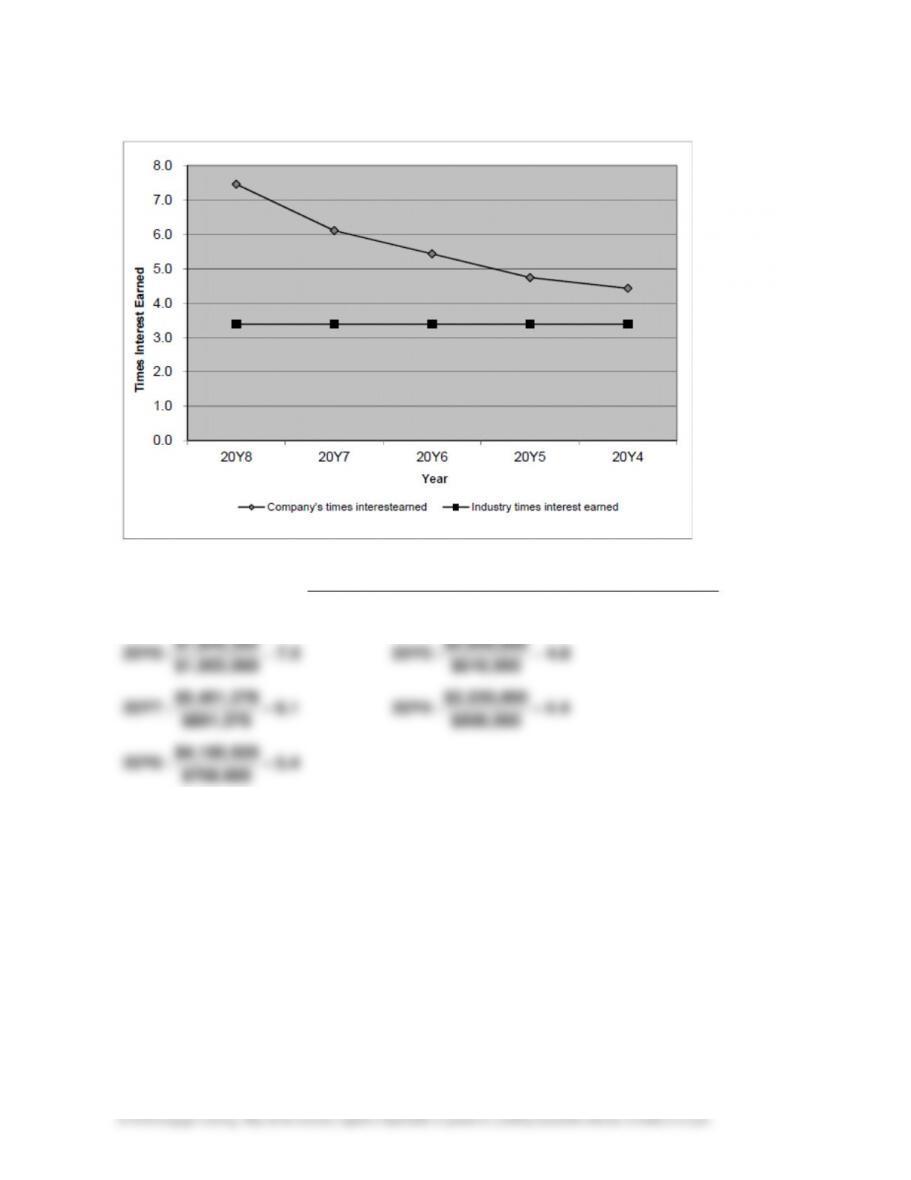

CHAPTER 14 Financial Statement Analysis

14–42

Prob. 14–5B

1.

a.

AssetsTotal Average

ExpenseInterest IncomeNet

AssetsTotal on Return +

=

23.8%

6$14,854,40

$3,540,600

:20Y6

21.9%

$8,676,000

$1,900,000

:20Y423.2%

6$19,859,58

$4,606,056

:20Y7

21.6%

0$11,370,24

$2,458,000

:20Y525.5%

5$25,988,66

$6,623,780

:20Y8

=

==

==

CHAPTER 14 Financial Statement Analysis

14–43

Prob. 14–5B (Continued)

1.

b.

Equity rs’Stockholde Total Average

IncomeNet

Equity rs’Stockholde on Return =

34.5%

$8,034,000

$2,772,000

:20Y6

34.1%

$4,100,000

$1,400,000

:20Y432.9%

0$11,277,24

$3,714,480

:20Y7

32.3%

$5,724,000

$1,848,000

:20Y535.0%

0$15,920,34

$5,571,720

:20Y8

=

==

==

CHAPTER 14 Financial Statement Analysis

14–44

Prob. 14–5B (Continued)

1.

c.

ExpenseInterest

ExpenseInterest Expense Tax Income IncomeNet

EarnedInterest Times ++

=

5.4

$768,600

$4,180,920

:20Y6

4.4

$500,000

$2,220,000

:20Y46.1

$891,576

$5,451,278

:20Y7

4.8

$610,000

$2,899,600

:20Y57.5

$1,052,060

$7,849,352

:20Y8

=

==

==

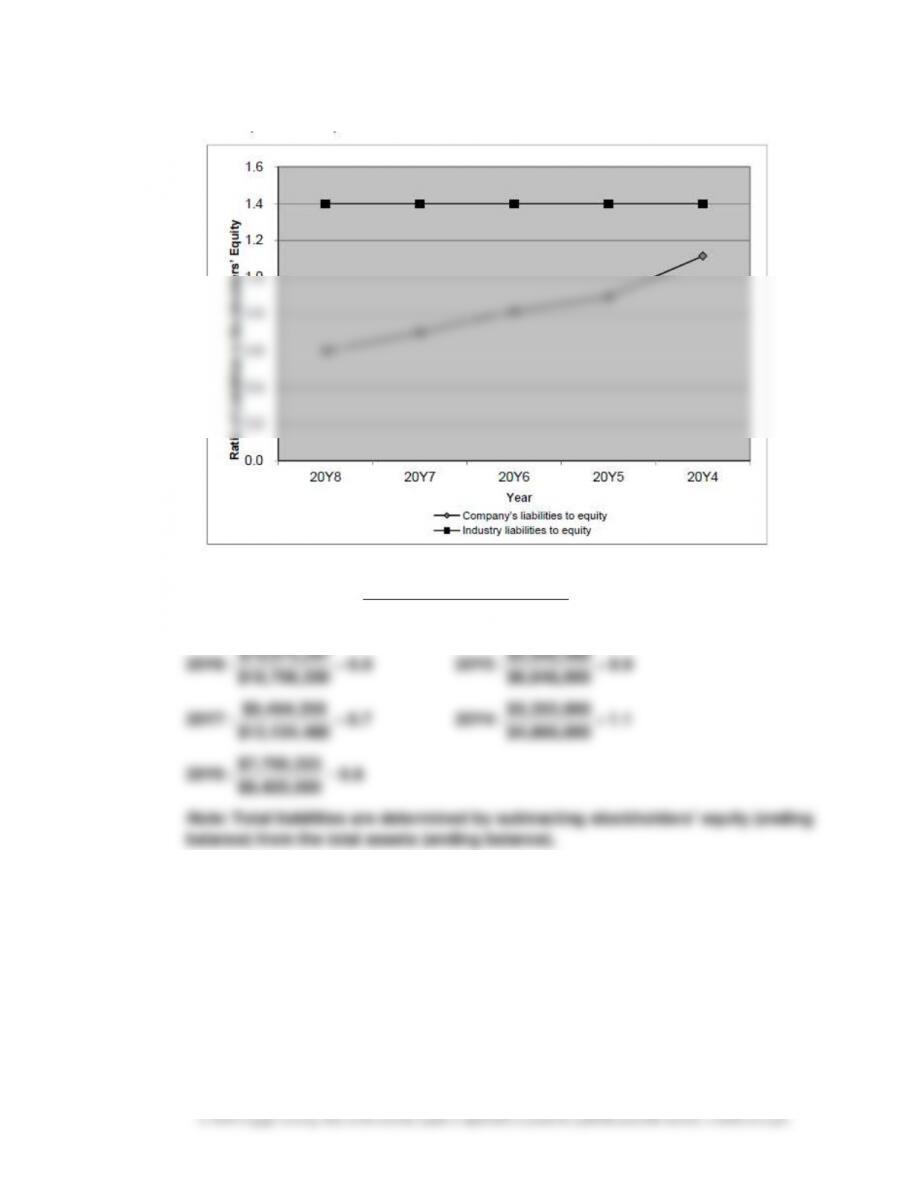

CHAPTER 14 Financial Statement Analysis

14–45

Prob. 14–5B (Continued)

1.

d.

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde

to sLiabilitie of Ratio =

0.8

$9,420,000

$7,700,333

:20Y6

1.1

$4,800,000

$5,352,000

:20Y40.7

0$13,134,48

$9,464,359

:20Y7

0.9

$6,648,000

$5,940,480

:20Y50.6

0$18,706,20

1$10,672,29

:20Y8

=

==

==

Note: Total liabilities are determined by subtracting stockholders’ equity (ending

balance) from the total assets (ending balance).

CHAPTER 14 Financial Statement Analysis

14–46

Prob. 14–5B (Concluded)

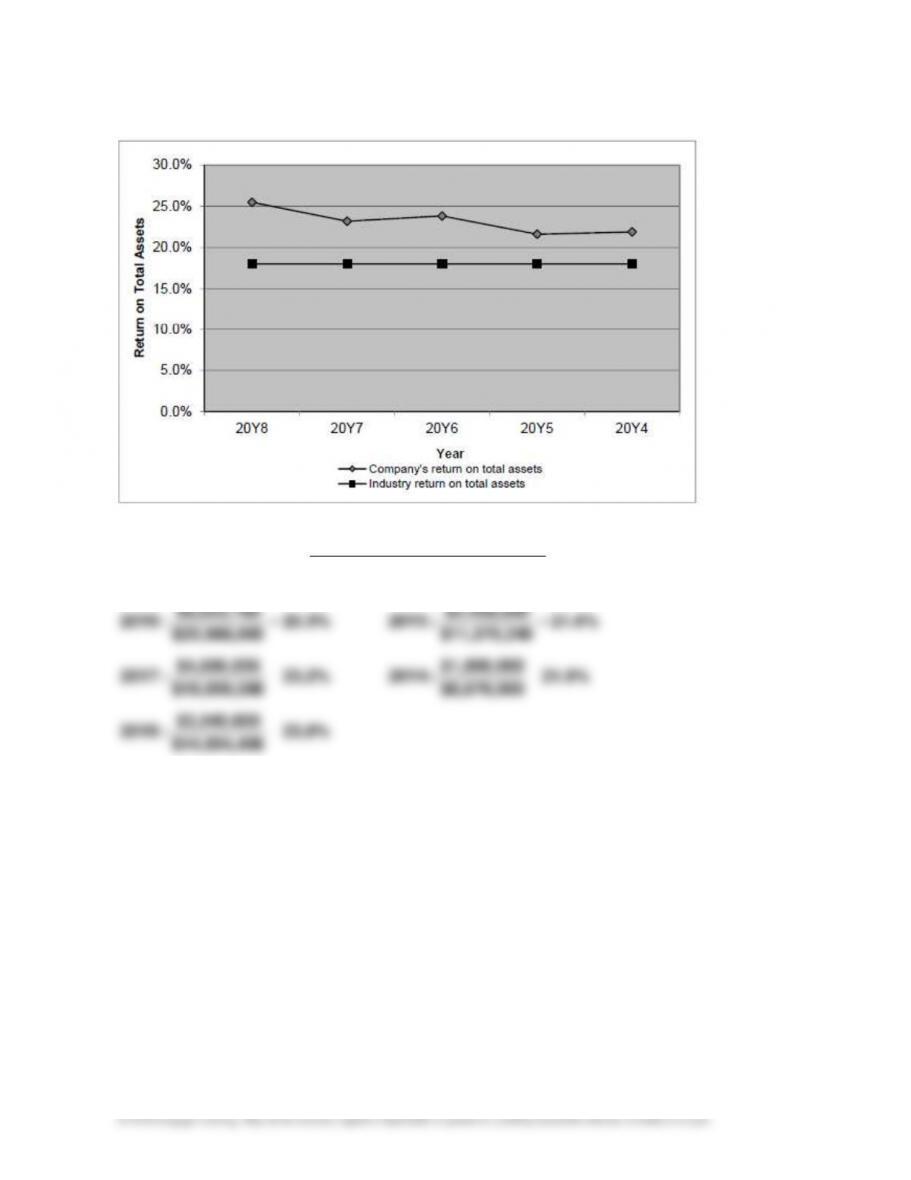

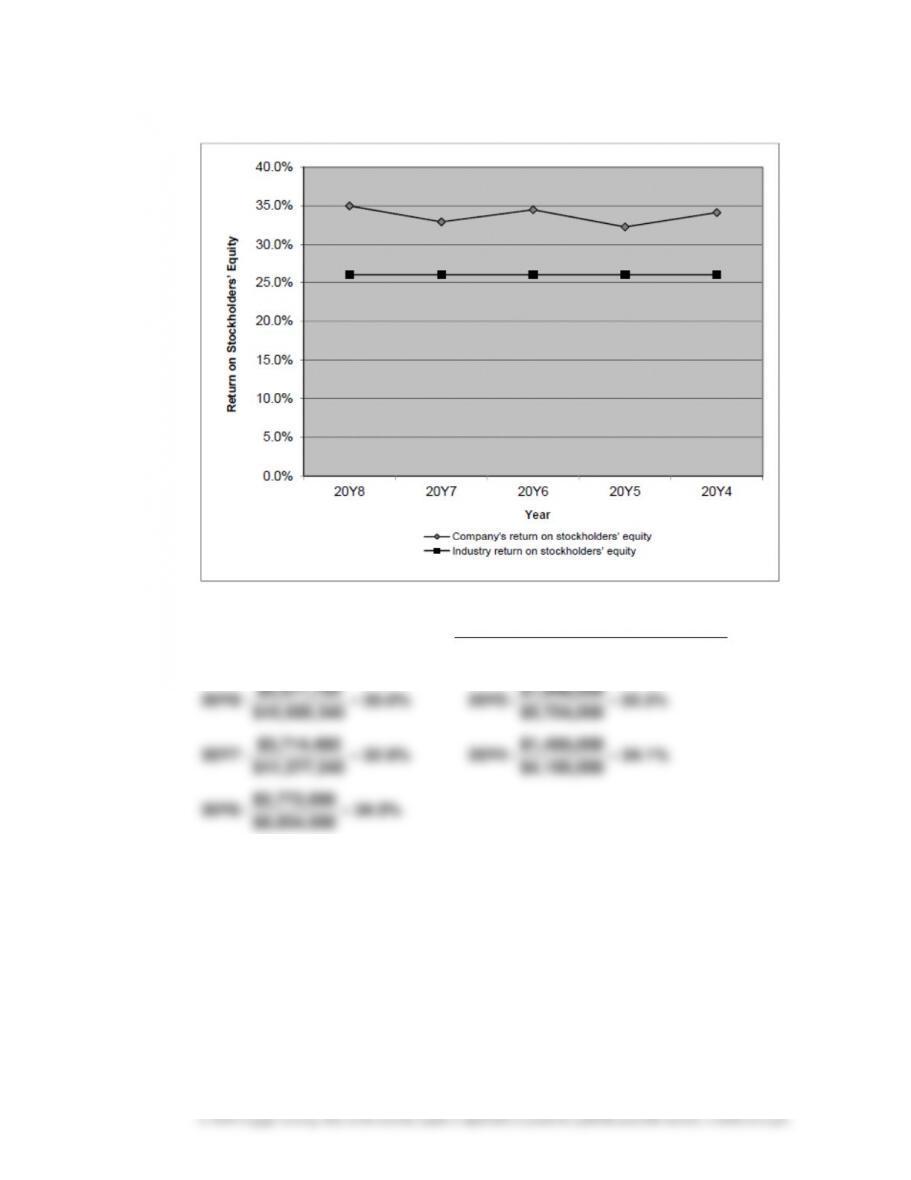

2. Both the return on total assets and the return on stockholders’ equity are above the

industry average for all five years. The return on total assets is actually improving

gradually. The return on stockholders’ equity exceeds the return earned on total assets,

CHAPTER 14 Financial Statement Analysis

14–47

MAKE A DECISION

MAD 14–1

1.

Amazon

Best Buy

Wal-Mart

Sales

100.0%

100.0%

100.0%

Cost of sales

(64.9)%

(76.0)%

(74.4)%

Gross profit

Selling, general, and administrative

35.1%

24.0%

25.6%

expenses

(31.9)%

(19.2)%

(20.9)%

Operating expenses

(0.1)%

(0.1)%

(0.0)%

Operating income

3.1%

4.7%

4.7%

2. Amazon has the highest gross profit on a percentage basis, but has the lowest operating

income on a percentage basis. This is because of the relatively large percentage of sales

MAD 14–2

1.

Alphabet

PepsiCo

Caterpillar

Earnings per share

$ 22.84

$ 3.71

$ 4.23

Market price per share of common stock

Earnings per share

Price-earnings ratio (a)

$ 778.01

÷ 22.84

$ 34.06

$99.92

÷ 3.71

$26.93

$67.96

÷ 4.23

$ 16.07

Dividends per share

Market price per share of common stock

Dividend yield (b)

$ 0.00

÷ 778.01

0.0%

$ 2.76

÷ 99.92

2.8%

$ 3.01

÷67.96

4.4%

2. Caterpillar has the largest dividend yield and strong earnings per share but has the lowest

price-earnings ratio. Stock market participants seem to be skeptical about Caterpillar’s

future prospects and are discounting its stock price despite its relatively solid

CHAPTER 14 Financial Statement Analysis

MAD 14–3

1. a.

AssetsTotal Average

ExpenseInterest IncomeNet

AssetsTotal on Return +

=

6.3%

$60,429

$664.0 $3,161.7

:1 Year

$59,642

$680.0 $1,940.0

3.9%

$57,965

$763.7 $1,523.9

:3 Year

=

+

+

=

+

b.

Equity rs’Stockholde Average

IncomeNet

Equity rs’Stockholde

Total on Return =

32.7%

$9,667

$3,161.7

:1 Year

$7,912

$1,940.0

22.9%

$6,644

$1,523.9

:3 Year

=

=

c.

gOutstandin Stock Common of Shares

Dividends Preferred – IncomeNet

Share per Earnings =

$8.71

363

$0 – $3,161.7

:1 Year

334

$0 – $1,940.0

$4.84

315

$0 – $1,523.9

:3 Year

=

=

d.

Stock Common of Share per PriceMarket

Stock Common of Share per Dividend

Yield Dividend =

$2.40

2.6%

$92.03

$2.40

:3 Year

=

MAD 14–3 (Concluded)

e.

Share per Earnings

Stock Common of Share per PriceMarket

Ratio Earnings–Price =

$81.10

19.0

$4.84

$92.03

:3 Year

=

CHAPTER 14 Financial Statement Analysis

MAD 14–4 (Concluded)

d.

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde

to sLiabilitie of Ratio =

3.5

$5,357

$18,783

:Marriott

=

CHAPTER 14 Financial Statement Analysis

TAKE IT FURTHER

TIF 14–1

No, Josh did not behave ethically. The Sarbanes-Oxley Act of 2002 requires a report on

14–52

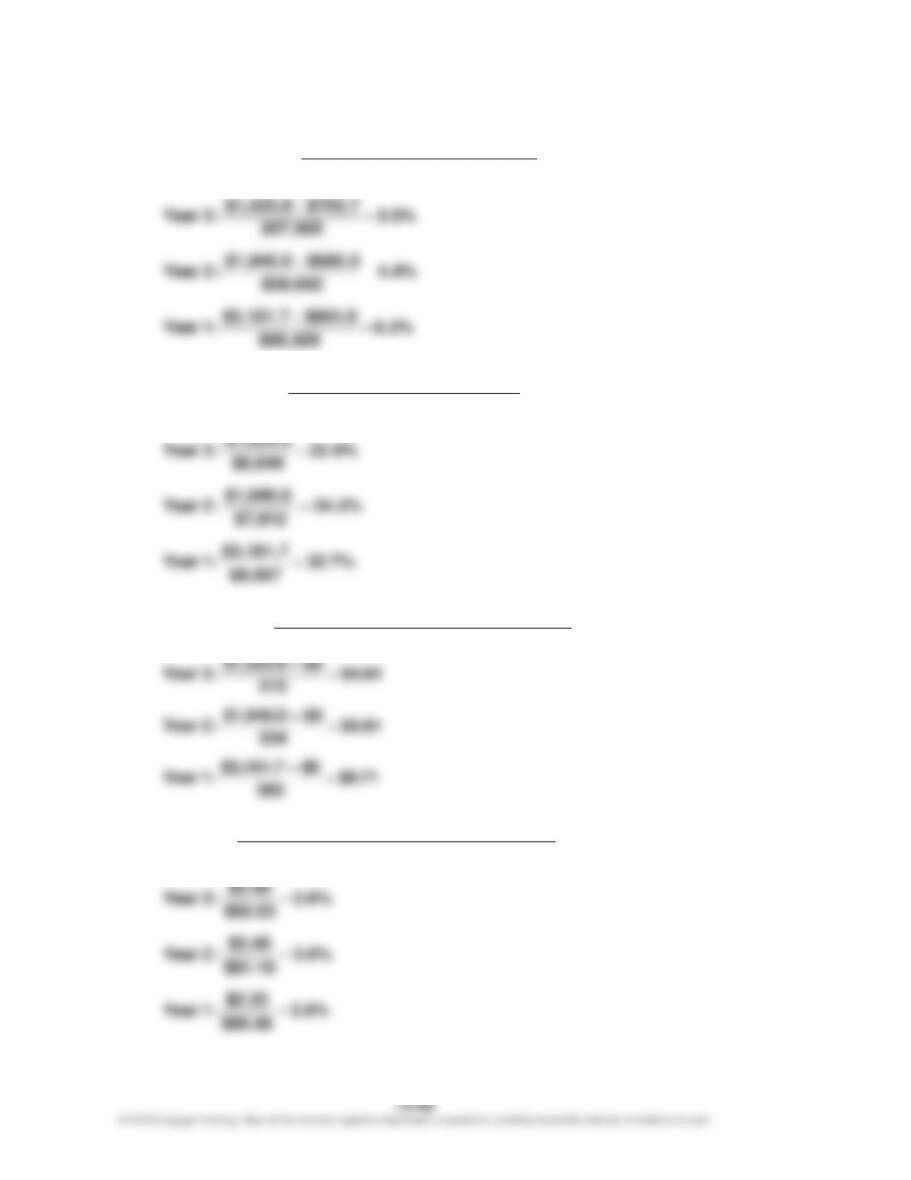

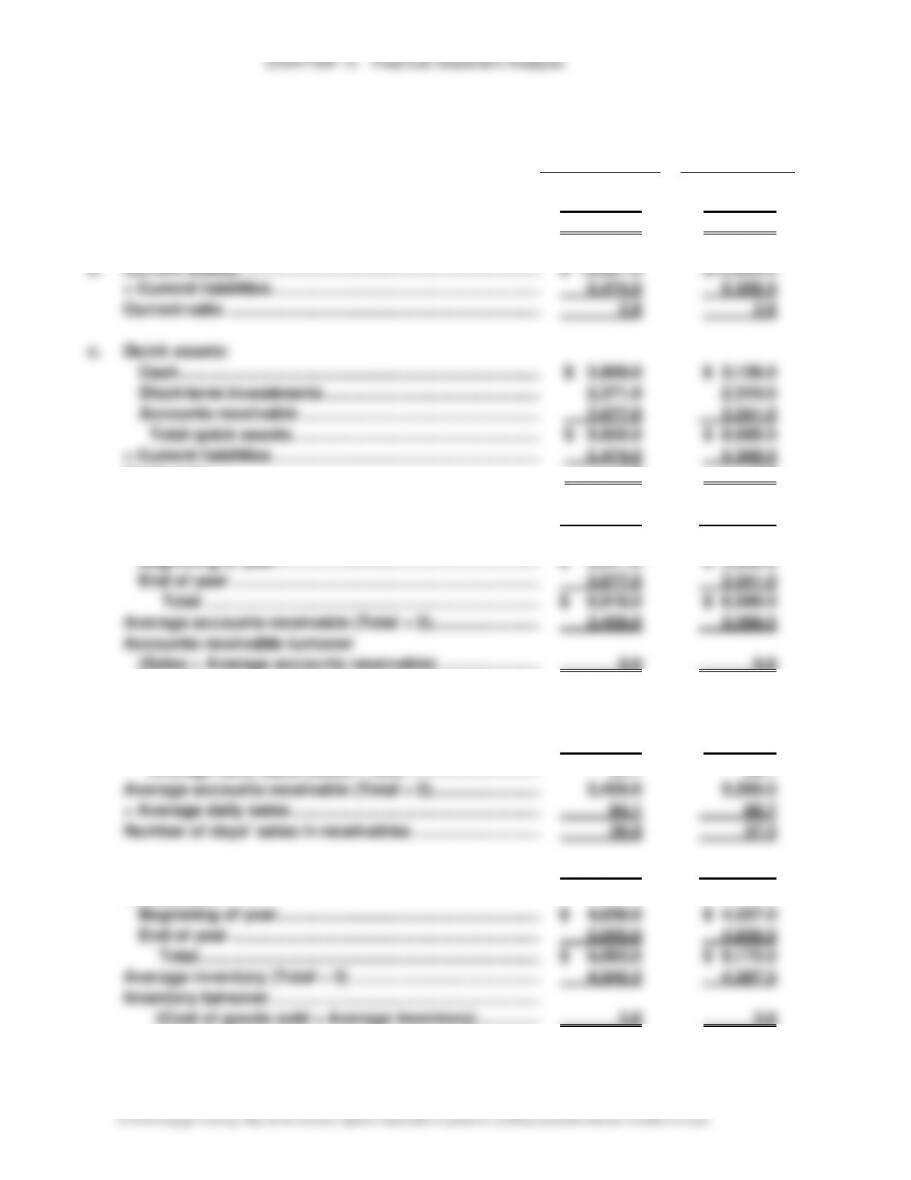

TIF 14–2

Fiscal

2017

Fiscal

2016

1.

a.

Current assets ………………………………………………………………..

$ 16,061.0

$15,025.0

Current liabilities ……………………………………………………….

5,474.0

5,358.0

Working capital……………………………………………………….

$ 10,587.0

$ 9,667.0

b.

Current assets ………………………………………………………………..

$ 16,061.0

$15,025.0

÷ Current liabilities ……………………………………………………….

5,474.0

5,358.0

Current ratio …………………………………………………………………..

2.9

2.8

c.

Quick assets:

Cash ……………………………………………………………………………

$ 3,808.0

$ 3,138.0

Short-term investments ………………………………………………..

2,371.0

2,319.0

Accounts receivable …………………………………………………….

3,677.0

3,241.0

Total quick assets ………………………………………………………

$ 9,856.0

$ 8,698.0

÷ Current liabilities ……………………………………………………….

5,474.0

5,358.0

Quick ratio ……………………………………………………………………..

1.8

1.6

d.

Sales ………………………………………………………………………………

$ 34,350.0

$ 32,376.0

Accounts receivable (net):

Beginning of year ……………………………………………………….

$ 3,241.0

$ 3,358.0

End of year ………………………………………………………………….

3,677.0

3,241.0

Total ……………………………………………………………………….

$ 6,918.0

$ 6,599.0

Average accounts receivable (Total ÷ 2) …………………………..

3,459.0

3,299.5

Accounts receivable turnover

(Sales ÷ Average accounts receivable) ………………………….

9.9

9.8

e.

Average daily sales:

Sales …………………………………………………………………………..

$ 34,350.0

$32,376.0

÷ 365 ………………………………………………………………………………

365

365

Average daily sales (Sales ÷ 365) …………………………..

94.1

88.7

Average accounts receivable (Total ÷ 2) …………………………..

3,459.0

3,299.5

÷ Average daily sales ………………………………………………………

94.1

88.7

Number of days’ sales in receivables …………………………..

36.8

37.2

f.

Cost of goods sold ……………………………………………………….

$ 19,038.0

$17,405.0

Inventories:

Beginning of year ……………………………………………………….

$ 4,838.0

$ 4,337.0

End of year ………………………………………………………………….

5,055.0

4,838.0

Total ………………………………………………………………………..

$ 9,893.0

$ 9,175.0

Average inventory (Total ÷ 2) …………………………………………..

4,946.5

4,587.5

Inventory turnover ……………………………………………………….

(Cost of goods sold ÷ Average inventory) …………………..

3.8

3.8

CHAPTER 14 Financial Statement Analysis

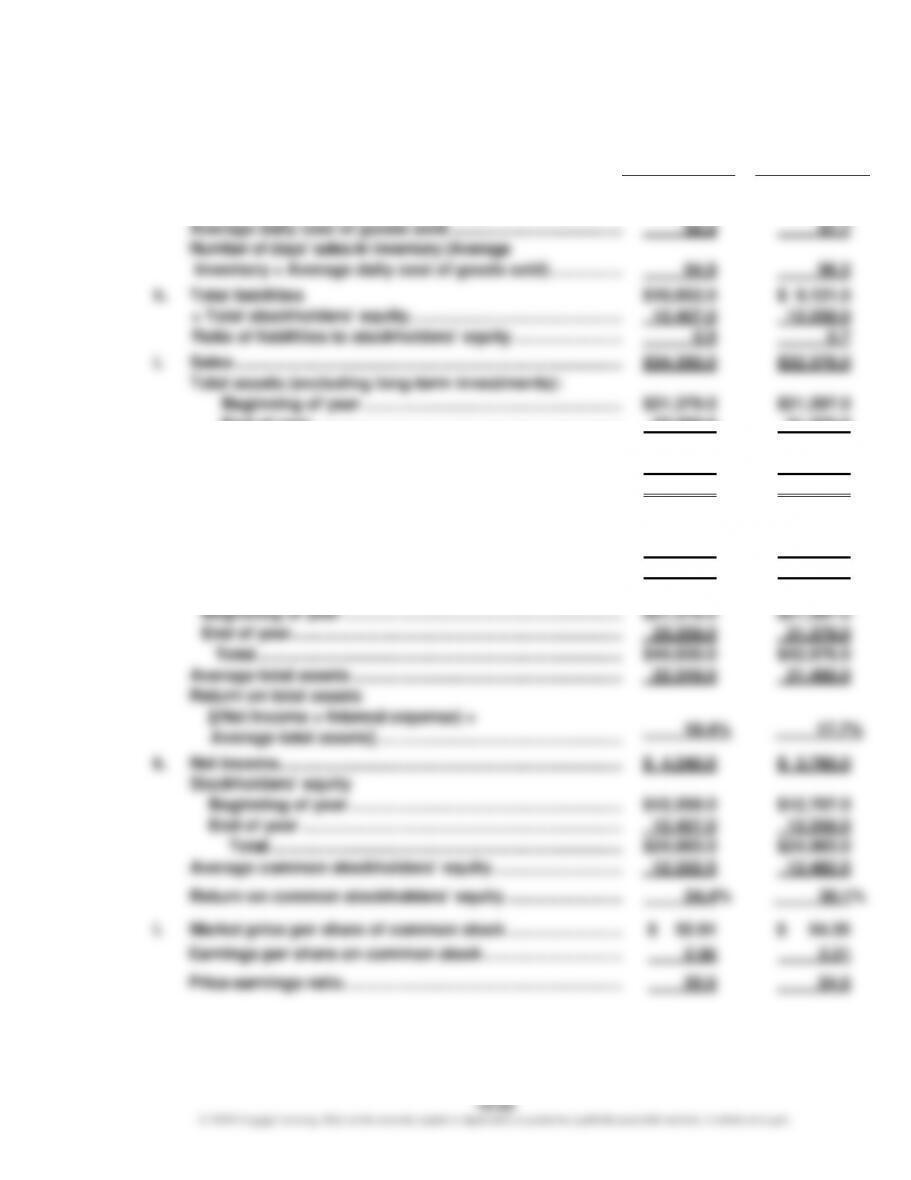

TIF 14–2 (Continued)

Fiscal

2017

Fiscal

2016

g.

Inventory (average) ……………………………………………………….

$ 4,946.5

$ 4,587.5

Cost of goods sold ……………………………………………………….

19,038.0

17,405.0

Average daily cost of goods sold …………………………………….

52.2

47.7

Number of days’ sales in inventory (Average

inventory ÷ Average daily cost of goods sold) …………………

94.8

96.2

h.

Total liabilities

$10,852.0

$ 9,121.0

÷ Total stockholders’ equity…………………………………………….

12,407.0

12,258.0

Ratio of liabilities to stockholders’ equity ………………………..

0.9

0.7

i.

Sales ……………………………………………………………………………..

$34,350.0

$32,376.0

Total assets (excluding long-term investments):

Beginning of year ……………………………………………………..

$21,379.0

$21,597.0

End of year ………………………………………………………………

23,259.0

21,379.0

Total ……………………………………………………………………..

$44,638.0

$42,976.0

Average total assets ……………………………………………………….

22,319.0

21,488.0

Asset turnover ………………………………………………………………..

1.5

1.5

j.

Net income……………………………………………………………………..

$ 4,240.0

$ 3,760.0

Interest expense ……………………………………………………………..

82.0

33.0

Total ………………………………………………………………………..

$ 4,322.0

$ 3,793.0

Total assets:

Beginning of year ……………………………………………………….

$21,379.0

$21,597.0

End of year …………………………………………………………………..

23,259.0

21,379.0

Total ………………………………………………………………………….

$44,638.0

$42,976.0

Average total assets ……………………………………………………….

22,319.0

21,488.0

Return on total assets

[(Net income + Interest expense) ÷

Average total assets] …………………………………………………..

19.4%

17.7%

k.

Net income……………………………………………………………………..

$ 4,240.0

$ 3,760.0

Stockholders’ equity

Beginning of year ……………………………………………………….

$12,258.0

$12,707.0

End of year …………………………………………………………………

12,407.0

12,258.0

Total ……………………………………………………………………….

$24,665.0

$24,965.0

Average common stockholders’ equity …………………………..

12,332.5

12,482.5

Return on common stockholders’ equity ………………………….

34.4%

30.1%

l.

Market price per share of common stock ………………………….

$ 52.81

$ 54.35

Earnings per share on common stock …………………………..

2.56

2.21

Price-earnings ratio ……………………………………………………….

20.6

24.6

14–54

TIF 14–2 (Concluded)

Fiscal

2017

Fiscal

2016

m.

Net income ……………………………………………………….

$ 4,240.0

$ 3,760.0

Sales ……………………………………………………………………………..

34,350.0

32,376.0

Net income to sales ……………………………………………………….

12.3%

11.6%

2. Before reaching definitive conclusions, each measure should be compared with past

years, industry averages, and similar firms in the industry.

a. The working capital increased between 2016 and 2017.

b. and c. The current and quick ratios both increased during 2017.

d. and e. The accounts receivable turnover and the number of days’ sales in receivables

indicate an increase in the efficiency of collecting accounts receivable. The

time to purchase, sell, and replace its inventory.

h. The margin of protection to creditors declined slightly as liabilities increased relative

to stockholders’ equity. Overall, Nike still provides sound protection to its creditors.

CHAPTER 14 Financial Statement Analysis

TIF 14–3

To: Boss Freeman

From: A+ Student

Re: Debt vs. Equity Financing

I have reviewed your company history and appreciate the challenges your company has faced

during economic downturns. While your conservative approach to debt financing is

commendable, your unwillingness to issue debt could limit your potential for future success.

Financing future growth exclusively through retained earnings and additional stock sales

14–56