14–1

CHAPTER 14

FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

1. Liquidity is the ability of a company to convert assets into cash. Short-term creditors such as banks and

financial institutions are most concerned with liquidity. Solvency is the ability of a company to pay its

3. Before this question can be answered, the increase in net income should be compared with changes in sales,

4. Generally, the two ratios would be very close because most service businesses sell services and hold very

little inventory.

5. a. A high inventory turnover minimizes the amount invested in inventories, thus freeing funds for other

uses. Storage costs, administrative expenses, losses caused by obsolescence, and potential decreases in

6. The ratio of fixed assets to long-term liabilities increased from 3.4 ($1,360,000 ÷ $400,000) in the

7. a. The return on total assets measures the profitability of the total assets, without regard for how the assets

CHAPTER 14 Financial Statement Analysis

14–2

DISCUSSION QUESTIONS (Concluded)

8. The price-earnings ratio measures the market’s expectations of a company’s future earnings prospects.

9. The dividend yield measures the return common stockholders receive from a cash dividend. The high

10. One report is the Report on Internal Control, which verifies management’s conclusions on internal

CHAPTER 14 Financial Statement Analysis

BASIC EXERCISES

BE 14–1

Accounts payable ……………………………….. $12,240 increase ($114,240 – $102,000), or 12%

Long-term debt …………………………………… $7,200 increase ($127,200 – $120,000), or 6%

BE 14–2

Amount

Percentage

Sales ………………………………………………….. $1,500,000

100% ($1,500,000 ÷ $1,500,000)

Cost of goods sold. ……………………………. 900,000

60% ($900,000 ÷ $1,500,000)

Gross profit ………………………………………… $ 600,000

40% ($600,000 ÷ $1,500,000)

BE 14–3

a. Current Ratio = Current Assets ÷ Current Liabilities

BE 14–4

a. Accounts Receivable Turnover = Sales ÷ Average Accounts Receivable

= 12.0

b.

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number =

14–5

BE 14–8

Asset Turnover = Sales ÷ Average Total Assets

= 2.7

BE 14–9

12.0%

$4,200,000

$504,000

$4,200,000

$80,000 $424,000

AssetsTotal Average

ExpenseInterest IncomeNet

AssetsTotal on Return

=

=

+

=

+

=

BE 14–10

a.

14.0%

Equity

rs’

Stockholde Common Average

IncomeNet

Equity

rs’

Stockholde on Return

=

=

b.

21.8%

$5,400,000

$47,800 – $1,225,000

Equity rs’Stockholde Common Average

Dividends Preferred – IncomeNet

Equity rs’Stockholde

Common on Return

=

=

BE 14–11

a.

gOutstandin Stock Common of Shares

Dividends Preferred – IncomeNet

Stock Common on

Share per Earnings =

80,000 $50,000) – ($562,000 =

$6.40=

b.

5.0

$6.40 $32.00

Stock Common on Share per Earnings

Stock Common of Share per PriceMarket

Ratio EarningsPrice

=

=

=–

CHAPTER 14 Financial Statement Analysis

14–6

EXERCISES

Ex. 14–1

a.

Innovation Quarter Inc.

Comparative Income Statement

For the Years Ended December 31

Current Year

Previous Year

Amount

Percent

Amount

Percent

Sales

$ 4,000,000

100%

$ 3,600,000

100%

Cost of goods sold

(2,280,000)

(57)%

(1,872,000)

(52)%

Gross profit

$ 1,720,000

43%

$ 1,728,000

48%

Selling expenses

$ (600,000)

(15)%

$ (648,000)

(18)%

Administrative expenses

(520,000)

(13)%

(360,000)

(10)%

Total operating expenses

$ (1,120,000)

(28)%

$(1,008,000)

(28)%

Operating income

$ 600,000

15%

$ 720,000

20%

Income tax expense

(240,000)

(6)%

(216,000)

(6)%

Net income

$ 360,000

9%

$ 504,000

14%

b. The vertical analysis indicates that the cost of goods sold as a percent of sales

CHAPTER 14 Financial Statement Analysis

14–7

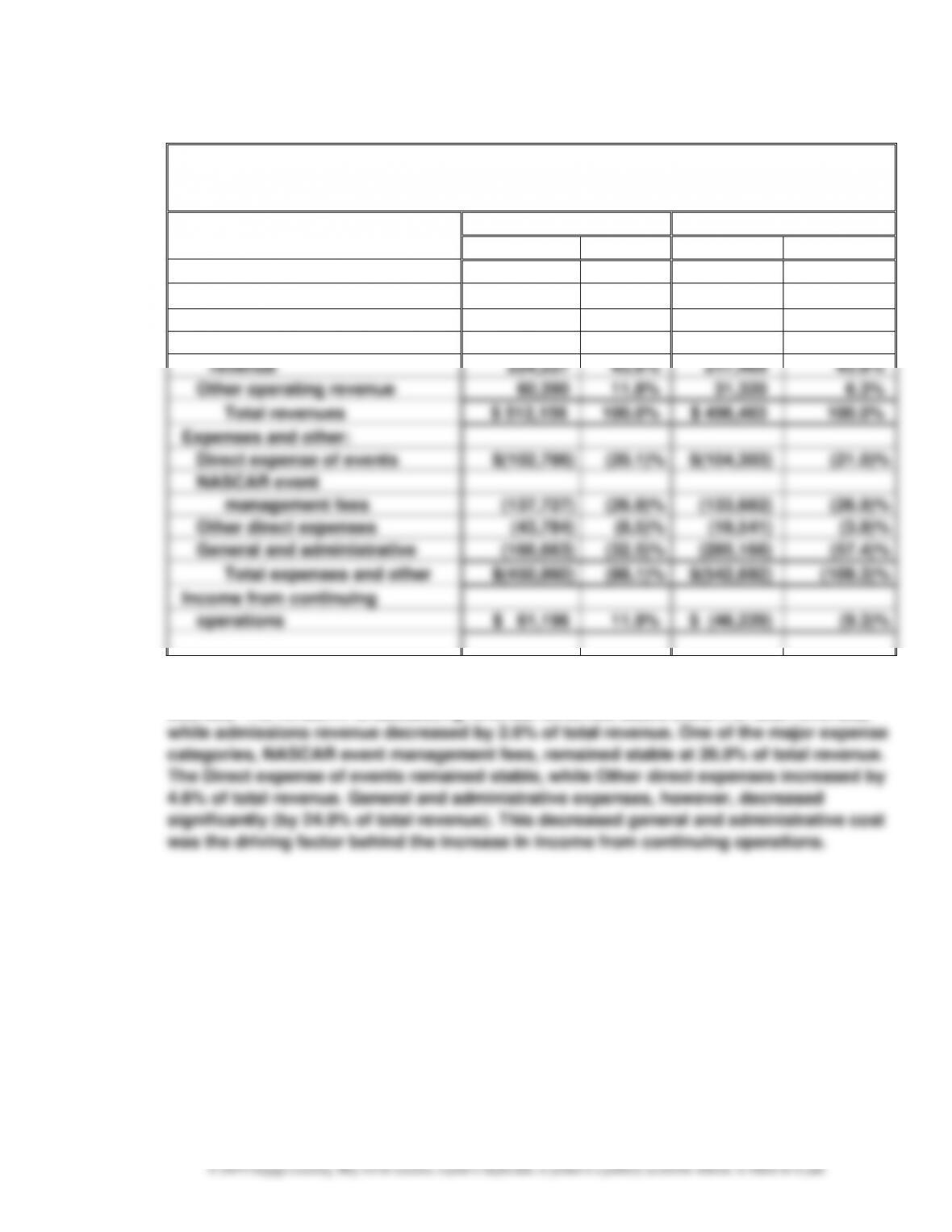

Ex. 14–2

a.

Speedway Motorsports, Inc.

Comparative Income Statement (in thousands of dollars)

For the Years Ended December 31

Current Year

Prior Year

Amount

Percent

Amount

Percent

Revenues:

Admissions

$ 90,639

17.7%

$ 100,694

20.3%

Event-related revenue

136,900

26.7%

146,980

29.6%

NASCAR broadcasting

revenue

224,227

43.8%

217,469

43.8%

Other operating revenue

60,390

11.8%

31,320

6.3%

Total revenues

$ 512,156

100.0%

$ 496,463

100.0%

Expenses and other:

Direct expense of events

$(102,786)

(20.1)%

$(104,303)

(21.0)%

NASCAR event

management fees

(137,727)

(26.9)%

(133,682)

(26.9)%

Other direct expenses

(43,784)

(8.5)%

(19,541)

(3.9)%

General and administrative

(166,663)

(32.5)%

(285,166)

(57.4)%

Total expenses and other

$(450,960)

(88.1)%

$(542,692)

(109.3)%

Income from continuing

operations

$ 61,196

11.9%

$ (46,229)

(9.3)%

b. Overall revenue increased between the two years, with changes in the mix of revenue

sources. The NASCAR broadcasting revenue remained stable (43.8% of total revenue),

CHAPTER 14 Financial Statement Analysis

14–8

Ex. 14–3

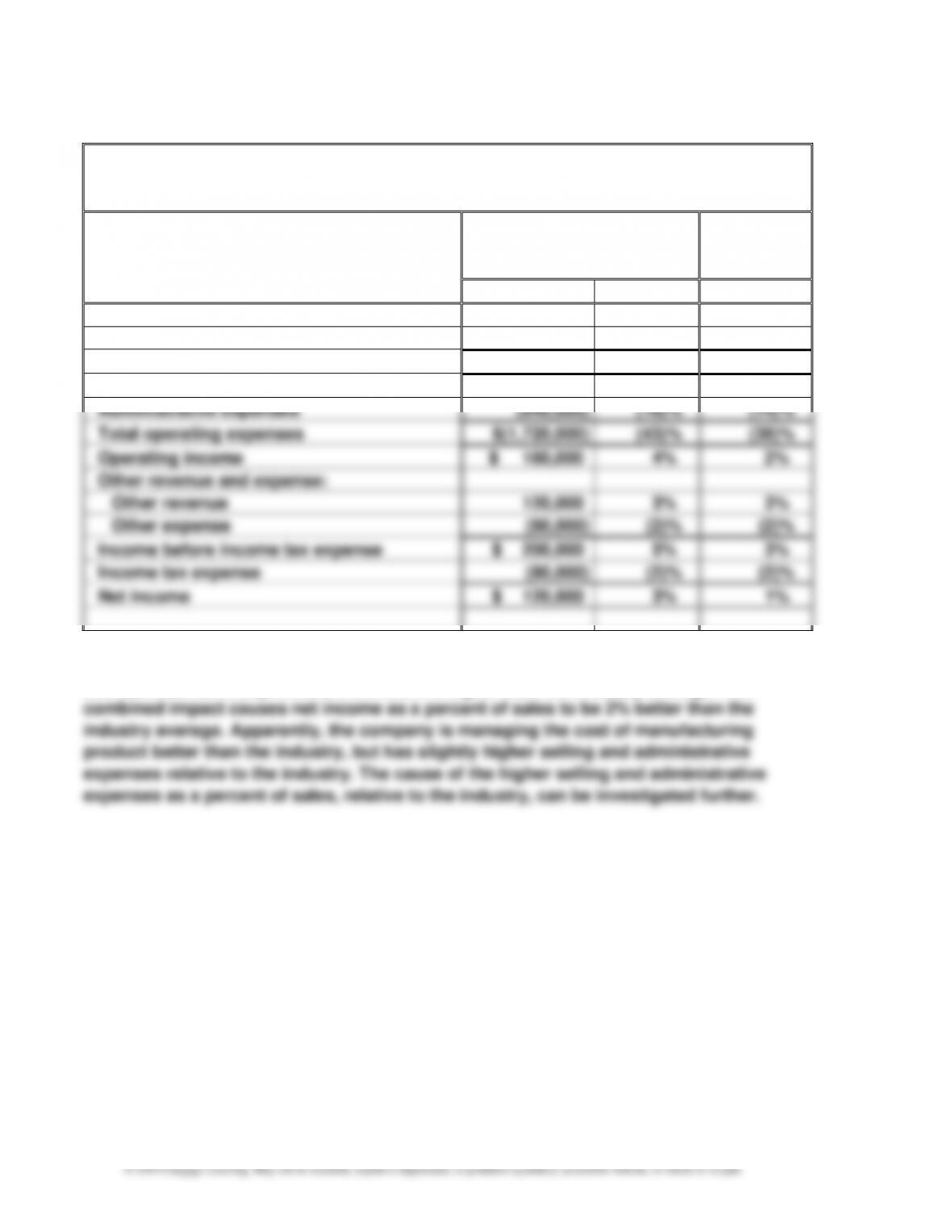

a.

Tannenhill Company

Common-Sized Income Statement

For the Year Ended December 31

Tannenhill

Company

Electronics

Industry

Average

Amount

Percent

Sales

$ 4,000,000

100%

100%

Cost of goods sold

(2,120,000)

(53)%

(60)%

Gross profit

$ 1,880,000

47%

40%

Selling expenses

$(1,080,000)

(27)%

(24)%

Administrative expenses

(640,000)

(16)%

(14)%

Total operating expenses

$(1,720,000)

(43)%

(38)%

Operating income

$ 160,000

4%

2%

Other revenue and expense:

Other revenue

120,000

3%

3%

Other expense

(80,000)

(2)%

(2)%

Income before income tax expense

$ 200,000

5%

3%

Income tax expense

(80,000)

(2)%

(2)%

Net income

$ 120,000

3%

1%

b. The cost of goods sold is 7% lower than the industry average, but the selling expenses

and administrative expenses are 3% and 2% higher than the industry average. The

CHAPTER 14 Financial Statement Analysis

14–9

Ex. 14–4

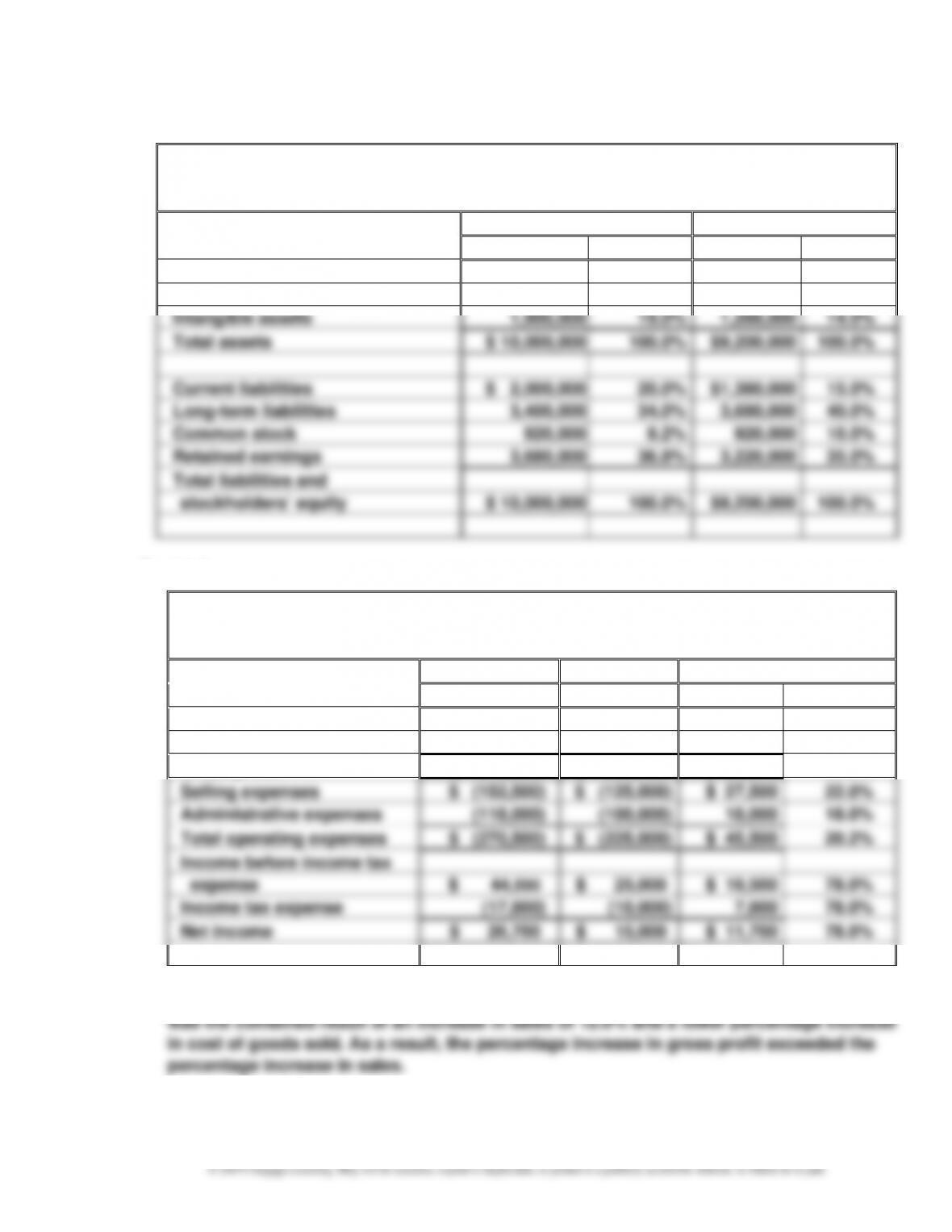

Alvarez Company

Comparative Balance Sheet

For the Years Ended December 31

Current Year

Previous Year

Amount

Percent

Amount

Percent

Current assets

$ 2,500,000

25.0%

$1,840,000

20.0%

Property, plant, and equipment

5,600,000

56.0%

6,072,000

66.0%

Intangible assets

1,900,000

19.0%

1,288,000

14.0%

Total assets

$ 10,000,000

100.0%

$9,200,000

100.0%

Current liabilities

$ 2,000,000

20.0%

$1,380,000

15.0%

Long-term liabilities

3,400,000

34.0%

3,680,000

40.0%

Common stock

920,000

9.2%

920,000

10.0%

Retained earnings

3,680,000

36.8%

3,220,000

35.0%

Total liabilities and

stockholders’ equity

$ 10,000,000

100.0%

$9,200,000

100.0%

Ex. 14–5

a.

Winthrop Company

Comparative Income Statement

For the Years Ended December 31

Current Year

Previous Year

Increase/(Decrease)

Amount

Amount

Amount

Percent

Sales

$ 2,240,000

$ 2,000,000

$240,000

12.0%

Cost of goods sold

(1,925,000)

(1,750,000)

175,000

10.0%

Gross profit

$ 315,000

$ 250,000

$ 65,000

26.0%

Selling expenses

$ (152,500)

$ (125,000)

$ 27,500

22.0%

Administrative expenses

(118,000)

(100,000)

18,000

18.0%

Total operating expenses

$ (270,500)

$ (225,000)

$ 45,500

20.2%

Income before income tax

expense

$ 44,500

$ 25,000

$ 19,500

78.0%

Income tax expense

(17,800)

(10,000)

7,800

78.0%

Net income

$ 26,700

$ 15,000

$ 11,700

78.0%

b. The net income for Winthrop Company increased by 78.0% between years. This increase

CHAPTER 14 Financial Statement Analysis

14–10

Ex. 14–6

a. (1) Working Capital = Current Assets – Current Liabilities

1.6

$900,000

$1,440,000

:Year Previous2.1

$1,000,000

$2,090,000

:YearCurrent

==

1.2

$900,000

$1,080,000

:Year Previous1.5

$1,000,000

$1,540,000

:YearCurrent

sLiabilitieCurrent

AssetsQuick

Ratio Quick(3)

==

=

b. The liquidity of Nilo has improved from the preceding year to the current year. The

working capital, current ratio, and quick ratio have all increased. Most of these changes

are the result of an increase in current assets relative to current liabilities.

Ex. 14–7

a. (1)

1.3

$17,578

$23,031

:Year Previous1.3

$21,135

$27,089

:YearCurrent

sLiabilitieCurrent

setsCurrent As

RatioCurrent

==

=

1.0

$17,578

$18,446

:Year Previous1.1

$21,135

$22,819

:YearCurrent

sLiabilitieCurrent

AssetsQuick

Ratio Quick(2)

==

=

b. The liquidity of PepsiCo has increased slightly over this time period. The current ratio has

CHAPTER 14 Financial Statement Analysis

14–11

Ex. 14–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The working

capital and current ratio incorrectly include intangible assets and property, plant, and

0.9

$300,000

$120,000 $48,000 $102,000

=

++

=

CHAPTER 14 Financial Statement Analysis

14–12

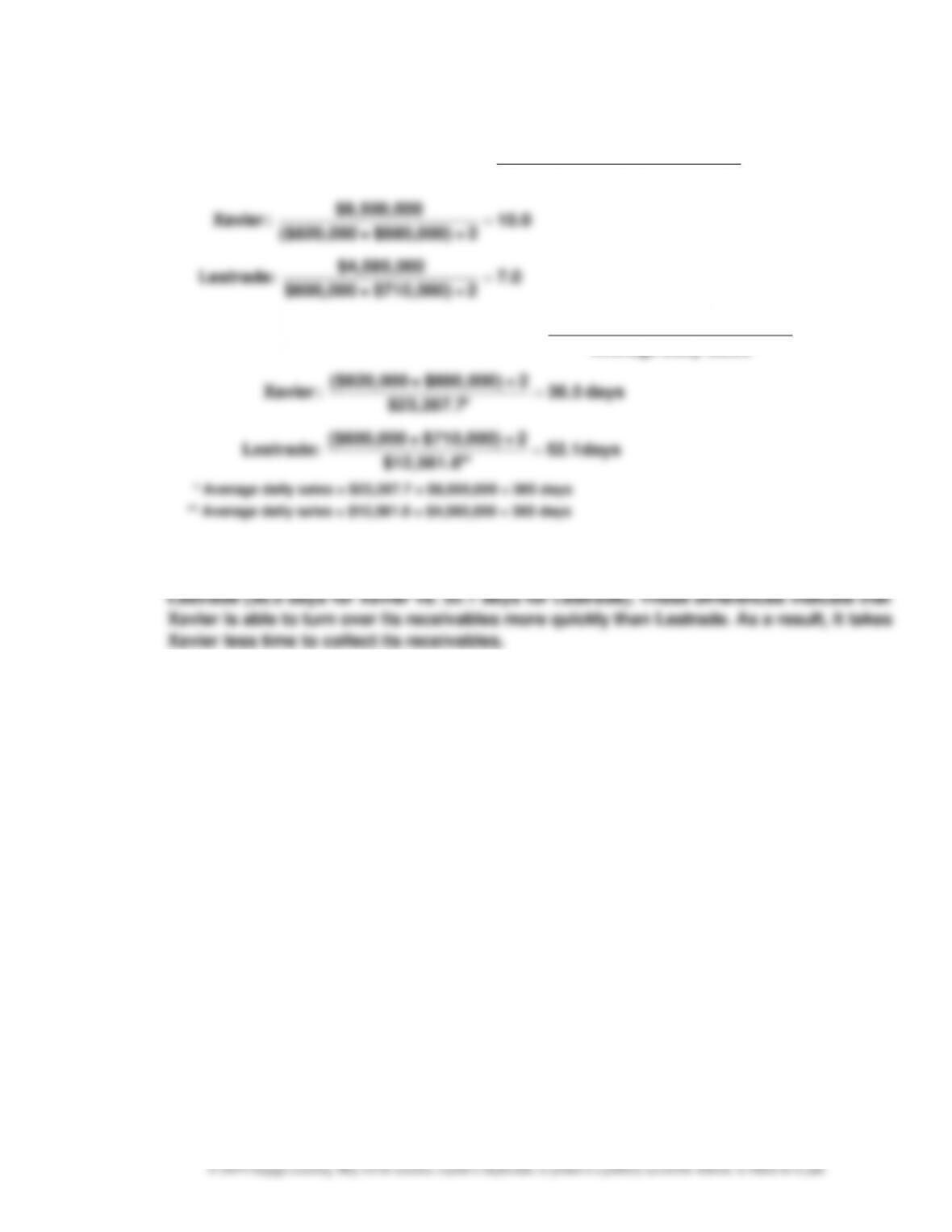

Ex. 14–9

a.

days 48.7

$12,842

$625,000

:20Y2days 44.5

$15,445

$687,500

:20Y3

Sales Daily Average

Receivable AccountsAverage

sReceivable in Sales Days’ of Number(2)

7.5

**$625,00

0$4,687,500

:20Y28.2

*$687,500

$5,637,500

:20Y3

Receivable AccountsAverage

Sales

Turnover Receivable Accounts(1)

4

3

2

1

2 $600,000) ($650,000 $625,000 **2 $650,000) ($725,000 $687,500*

==

=

==

=

+=+=

1 Average accounts receivable = $687,500 = ($725,000 + $650,000) ÷ 2

2 Average daily sales = $15,445 = $5,637,500 ÷ 365 days

3 Average accounts receivable = $625,000 = ($650,000 + $600,000) ÷ 2

4 Average daily sales = $12,842 = $4,687,500 ÷ 365 days

b. The collection of accounts receivable has improved. This can be seen in both the increase

CHAPTER 14 Financial Statement Analysis

14–13

Ex. 14–10

a.

Receivable AccountsAverage

Sales

=Turnover Receivable Accounts(1)

CHAPTER 14 Financial Statement Analysis

14–14

Ex. 14–11

a.

12.0

2 ÷ $860,000) + ($940,000

0$10,800,00

:Year Previous

9.0

2 ÷ $940,000) + 0($1,120,00

$9,270,000

:YearCurrent

InventoryAverage

Sold Goods ofCost

=Turnover Inventory(1)

=

=

CHAPTER 14 Financial Statement Analysis

14–15

Ex. 14–12

a.

$44,754

InventoryAverage

Sold Goods ofCost

=Turnover Inventory(1)

CHAPTER 14 Financial Statement Analysis

14–16

Ex. 14–13

a.

$2,124,000

Equity rs’Stockholde Total

sLiabilitie Total

=Equity rs’Stockholde to sLiabilitie of Ratio

CHAPTER 14 Financial Statement Analysis

14–17

Ex. 14–14

a.

1.7

$2,407,782

$4,086,012

:Inc. Mattel,

1.7

$1,862,736

$3,205,926

:Inc. Hasbro,

Equity rs’Stockholde Total

sLiabilitie Total

=Equity rs’Stockholde to sLiabilitie of Ratio

=

=

b.

5.3

$95,118

$95,118 + $409,472

:Inc. Mattel,

8.1

$97,405

$97,405 + $692,489

:Inc. Hasbro,

ExpenseInterest

ExpenseInterest + Expense Tax Income Before Income

=EarnedInterest Times

=

=

c. Hasbro carries the same proportion of debt to stockholders’ equity as Mattel (1.7

times stockholders’ equity). Both companies have strong interest coverage;

CHAPTER 14 Financial Statement Analysis

14–18

Ex. 14–15

a.

5.7

$827,687

$439,748 + $2,347,455 + $1,909,443

:Hershey

0$25,215,00

$8,689,000 + 0$13,217,00 + 0$14,417,00

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde to sLiabilitie of Ratio

=

=

b.

0.8

$2,787,203

$2,177,248

:Hershey

0$21,906,00

$8,229,000

sLiabilitie Term–Long

(net) AssetsFixed

sLiabilitie Term–Long to AssetsFixed of Ratio

=

=

c. Hershey’s total liabilities to stockholders’ equity ratio is higher than Mondelez’s (5.7 vs.

1.4), meaning Hershey uses more debt than Mondelez. Mondelez has a lower ratio of fixed

assets to long-term liabilities than Hershey. This ratio divides the property, plant, and

equipment (net) by the long-term debt. The ratio for Mondelez is aggressive, with fixed

CHAPTER 14 Financial Statement Analysis

14–19

Ex. 14–16

a.

2.6

$1,824,700

$4,697,500

: WorldwideYRC

AssetsTotal Average

Sales

TurnoverAsset

=

=

CHAPTER 14 Financial Statement Analysis

Ex. 14–17

a.

$180,000 + $372,000

AssetsTotal Average

ExpenseInterest + IncomeNet

AssetsTotal on Return

1

=