CHAPTER 13 Statement of Cash Flows

13–33

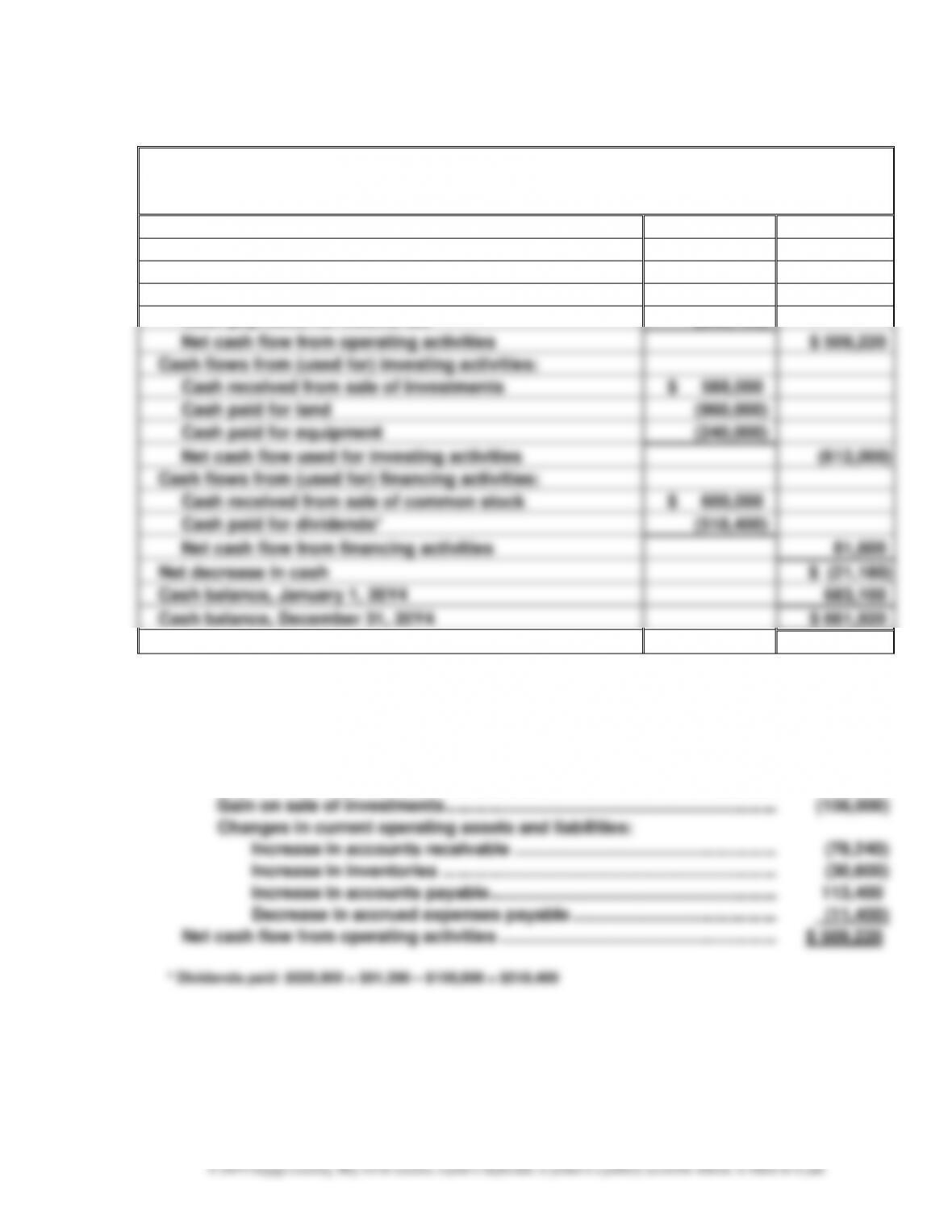

Appendix 2 Prob. 13–4B

Martinez Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y4

Cash flows from (used for) operating activities:

Cash received from customers1

$ 4,433,760

Cash payments for merchandise2

(2,269,200)

Cash payments for operating expenses3

(1,356,240)

Cash payments for income tax

(299,100)

Net cash flow from operating activities

$ 509,220

Cash flows from (used for) investing activities:

Cash received from sale of investments

$ 588,000

Cash paid for land

(960,000)

Cash paid for equipment

(240,000)

Net cash flow used for investing activities

(612,000)

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$ 600,000

Cash paid for dividends*

(518,400)

Net cash flow from financing activities

81,600

Net decrease in cash

$ (21,180)

Cash balance, January 1, 20Y4

683,100

Cash balance, December 31, 20Y4

$ 661,920

Reconciliation of Net Income with Cash Flows from Operating Activities:

Net income …………………………………………………………………………………………. $ 558,960

Adjustments to reconcile net income to net cash flow

from operating activities:

Depreciation expense …………………………………………………………………… 113,100

CHAPTER 13 Statement of Cash Flows

13–34

Appendix 2 Prob. 13–4B (Concluded)

Computations:

1. Sales …………………………………………………………………………………….. $4,512,000

2. Cost of goods sold ………………………………………………………………… $2,352,000

3. Operating expenses other than depreciation …………………………... $1,344,840

CHAPTER 13 Statement of Cash Flows

13–35

Appendix 2 Prob. 13–5B

Merrick Equipment Co.

Statement of Cash Flows

For the Year Ended December 31, 20Y9

Cash flows from (used for) operating activities:

Cash received from customers1

$ 2,004,858

Cash payments for merchandise2

(1,242,586)

Cash payments for operating expenses3

(513,559)

Cash payments for income taxes

(94,453)

Net cash flow from operating activities

$154,260

Cash flows from (used for) investing activities:

Cash received from sale of investments

$ 91,800

Cash paid for purchase of land

(295,800)

Cash paid for purchase of equipment

(80,580)

Net cash flow used for investing activities

(284,580)

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$ 250,000

Cash paid for dividends*

(96,900)

Net cash flow from financing activities

153,100

Net increase in cash

$ 22,780

Cash balance, January 1, 20Y9

47,940

Cash balance, December 31, 20Y9

$ 70,720

Reconciliation of Net Income with Cash Flows from Operating Activities:

Net income ………………………………………………………………………………………….. $141,680

Adjustments to reconcile net income to net cash flow from operating

activities:

Depreciation …………………………………………………………………………………. 14,790

CHAPTER 13 Statement of Cash Flows

13–36

Appendix 2 Prob. 13–5B (Concluded)

Computations:

1. Sales …………………………………………………………………………………… $2,023,898

2. Cost of goods sold ………………………………………………………………. $1,245,476

3. Operating expenses other than depreciation …………………………. $ 517,299

CHAPTER 13 Statement of Cash Flows

MAKE A DECISION

MAD 13–1

a.

Amazon

Best Buy

Wal-Mart

Cash flows from operating activities

Cash used to purchase property,

$16,443

$2,545

$ 31,530

plant, and equipment

(6,737)

(582)

(10,619)

Free cash flow

$ 9,706

$1,963

$ 20,911

b.

Amazon

Best Buy

Wal-Mart

Ratio of free cash flow to sales

7.1%

5.0%

4.3%

($9,706 ÷

($1,963 ÷

($20,911 ÷

$135,987)

$39,403)

$485,873)

c. Amazon’s free cash flow is $9,706 million, which is higher than Best Buy’s but lower than

Wal-Mart’s. However, these companies vary greatly in size; thus, comparing absolute free

cash flow across these companies is not very meaningful. A relative measure that can be

MAD 13–2

a.

Apple

Coca-Cola

Verizon

Cash flows from operating activities

Cash used to purchase property,

$ 65,824

$ 8,796

$ 22,715

plant, and equipment

(12,734)

(2,262)

(17,059)

Free cash flow

$ 53,090

$ 6,534

$ 5,656

b.

Apple

Coca-Cola

Verizon

Ratio of free cash flow to sales

24.6%

15.6%

4.5%

($53,090 ÷

$215,639)

($6,534 ÷

$41,863)

($5,656 ÷

$125,980)

c. Apple has the largest free cash flow. The ratio of free cash flow to sales is the best metric

for comparing the three companies. In this comparison, ranking from largest to smallest,

13–38

MAD 13–3

a.

Year 3

Year 2

Year 1

Cash flows from operating activities

Cash used to purchase property,

$(68)

$(56)

$ (38)

plant, and equipment

(16)

(24)

(84)

Free cash flow

$(84)

$(80)

$(122)

b.

Year 3

Year 2

Year 1

Ratio of free cash flow to sales

–5.6%

–4.4%

–5.8%

[$(84) ÷

[$(80) ÷

[$(122) ÷

$1,507]

$1,839]

$2,091]

c. The free cash flow information does accurately show the financial stress on Aeropostale.

The free cash flow and ratio of free cash flow to sales were negative in the most recent

MAD 13–4

a. Total revenue is a good measure for assessing the relative size of the two companies.

b. Total revenue growth is measured horizontally for each company using Year 1 as the base

year as follows:

Year 3

Year 2

Year 1

AT&T

124%

111%

100%

Facebook

222%

144%

100%

AT&T

124% = $163,786 ÷ $132,447

111% = $146,801 ÷ $132,447

Facebook

222% = $27,638 ÷ $12,466

144% = $17,928 ÷ $12,466

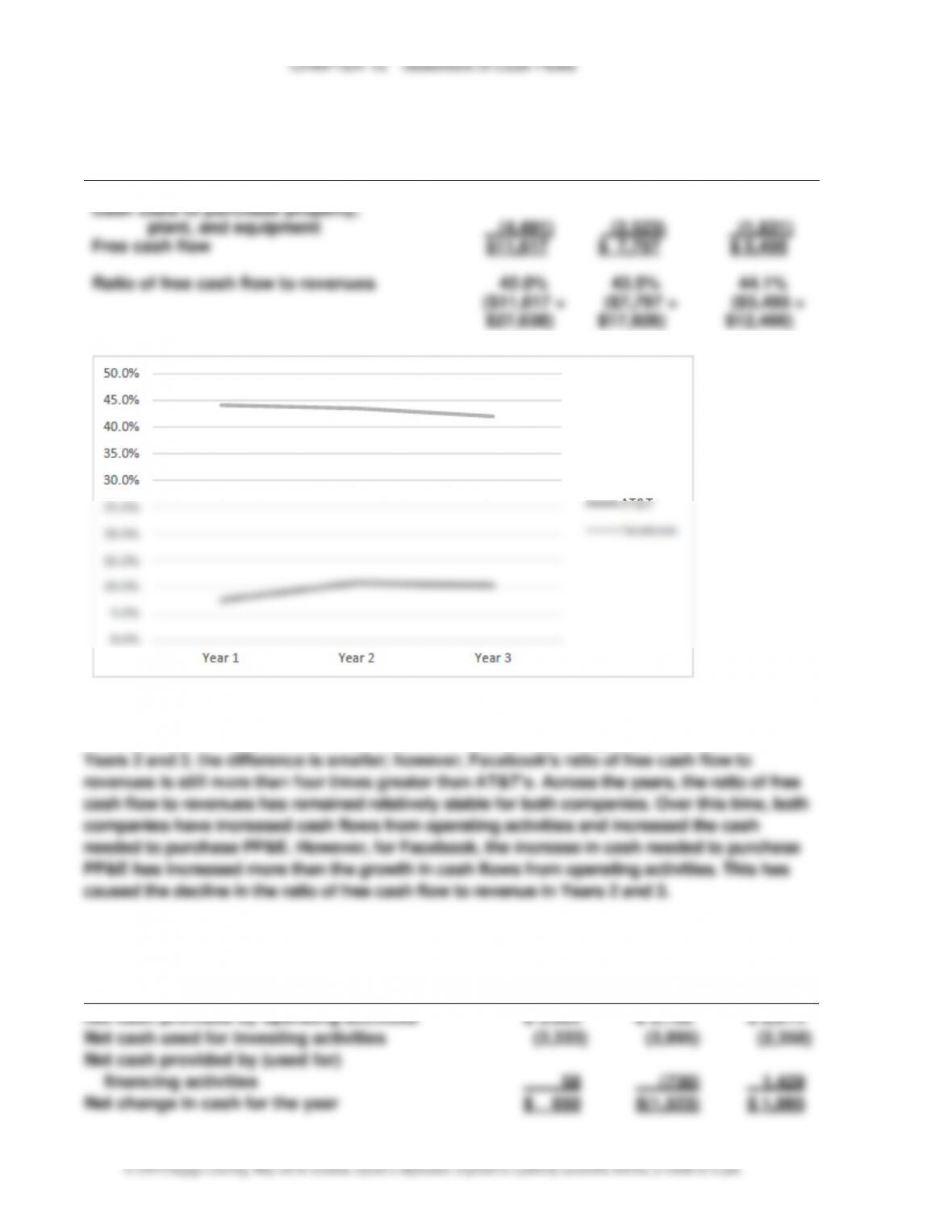

CHAPTER 13 Statement of Cash Flows

MAD 13–4 (Continued)

It is clear from these data that Facebook is growing much faster than AT&T. This is no

surprising in that Facebook is a young company that is expanding services and regions.

c. Cash used to purchase PP&E as a percentage of the cash flows from operating activities:

Year 3

Year 2

Year 1

AT&T

57%

56%

68%

Facebook

28%

24%

25%

AT&T

57% = $22,408 ÷ $39,344

56% = $20,015 ÷ $35,880

68% = $21,433 ÷ $31,338

Facebook

28% = $4,491 ÷ $16,108

24% = $2,523 ÷ $10,320

25% = $1,831 ÷ $7,326

d. The data indicate that AT&T requires more cash to purchase PP&E than does Facebook.

In Year 1, the percent of cash flows from operations that is used to purchase PP&E is

e. AT&T:

Year 3

Year 2

Year 1

Cash flows from operating activities

$ 39,344

$ 35,880

$ 31,338

Cash used to purchase property,

plant, and equipment

(22,408)

(20,015)

(21,433)

Free cash flow

$ 16,936

$ 15,865

$ 9,905

Ratio of free cash flow to revenues

10.3%

($16,936 ÷

$163,786)

10.8%

($15,865 ÷

$146,801)

7.5%

($9,905 ÷

$132,447)

13–40

MAD 13–4 (Continued)

Facebook:

Year 3

Year 2

Year 1

Cash flows from operating activities

$16,108

$10,320

$ 7,326

Cash used to purchase property,

plant, and equipment

(4,491)

(2,523)

(1,831)

Free cash flow

$11,617

$ 7,797

$ 5,495

Ratio of free cash flow to revenues

42.0%

($11,617 ÷

$27,638)

43.5%

($7,797 ÷

$17,928)

44.1%

($5,495 ÷

$12,466)

f. Facebook appears to have a better free cash flow position than does AT&T. In Year 1,

Facebook’s ratio of free cash flow to revenues is almost six times greater than AT&T’s. In

MAD 13–5

a. Net change in cash:

Year 3

Year 2

Year 1

Net cash provided by operating activities

$ 3,925

$ 3,102

$ 2,914

Net cash used for investing activities

Net cash provided by (used for)

(3,333)

(3,895)

(2,358)

financing activities

58

(730)

1,429

Net change in cash for the year

$ 650

$(1,523)

$ 1,985

CHAPTER 13 Statement of Cash Flows

13–41

MAD 13–5 (Concluded)

b. Free cash flow:

Year 3

Year 2

Year 1

Net cash provided by operating activities

$3,925

$3,102

$2,914

Additions to property, plant, and equipment

(220)

(174)

(132)

Free cash flow

$3,705

$2,928

$2,782

c. The free cash flow is almost $4 billion in Year 3. Over the three-year period, free cash flow

grew from $2,782 million to $3,705 million, or a 33% increase [($3,705 – $2,782) $2,782].

d. The cash flow available for investment, dividends, debt repayments, and stock

CHAPTER 13 Statement of Cash Flows

13–42

TAKE IT FURTHER

TIF 13–1

Although this situation might seem harmless at first, it is, in fact, a violation of generally

accepted accounting principles. The operating cash flow per share figure should not be

shown on the face of the income statement. The income statement is constructed under

accrual accounting concepts, while operating cash flow fiundoes” the accounting accruals.

TIF 13–2

A sample solution based on National Beverage Corp.’s Form 10-K for the fiscal year ended

April 30, 2016, follows:

1. a. $78,955 thousand

CHAPTER 13 Statement of Cash Flows

TIF 13–3

Memo

To: My Instructor

From: A+ Student

Re: Tidewater Inc. Financial Condition

Tidewater Inc. is a retailer that has been unprofitable in recent years. While the company has

returned to profitability, there are several fired flags” indicating that the company’s future

prospects are highly uncertain. These red flags are discussed below.

• The company has initiated a new marketing campaign that significantly increased the

number of customers who are purchasing merchandise on credit using the company’s

branded credit card. This campaign significantly increased revenue and has helped the

customer appeal, and it is questionable whether the company will be able to sell the

merchandise.

• The company has not been able to pay off its accounts payable in a timely manner,

resulting in significant overdue accounts payable balances. While the company reports

13–44

TIF 13–4

Start-up companies are unique in that they frequently have negative retained earnings

earnings and operating cash flows. The negative retained earnings are often due to losses

from high start-up expenses. The negative operating cash flows are typical because growth