CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–21

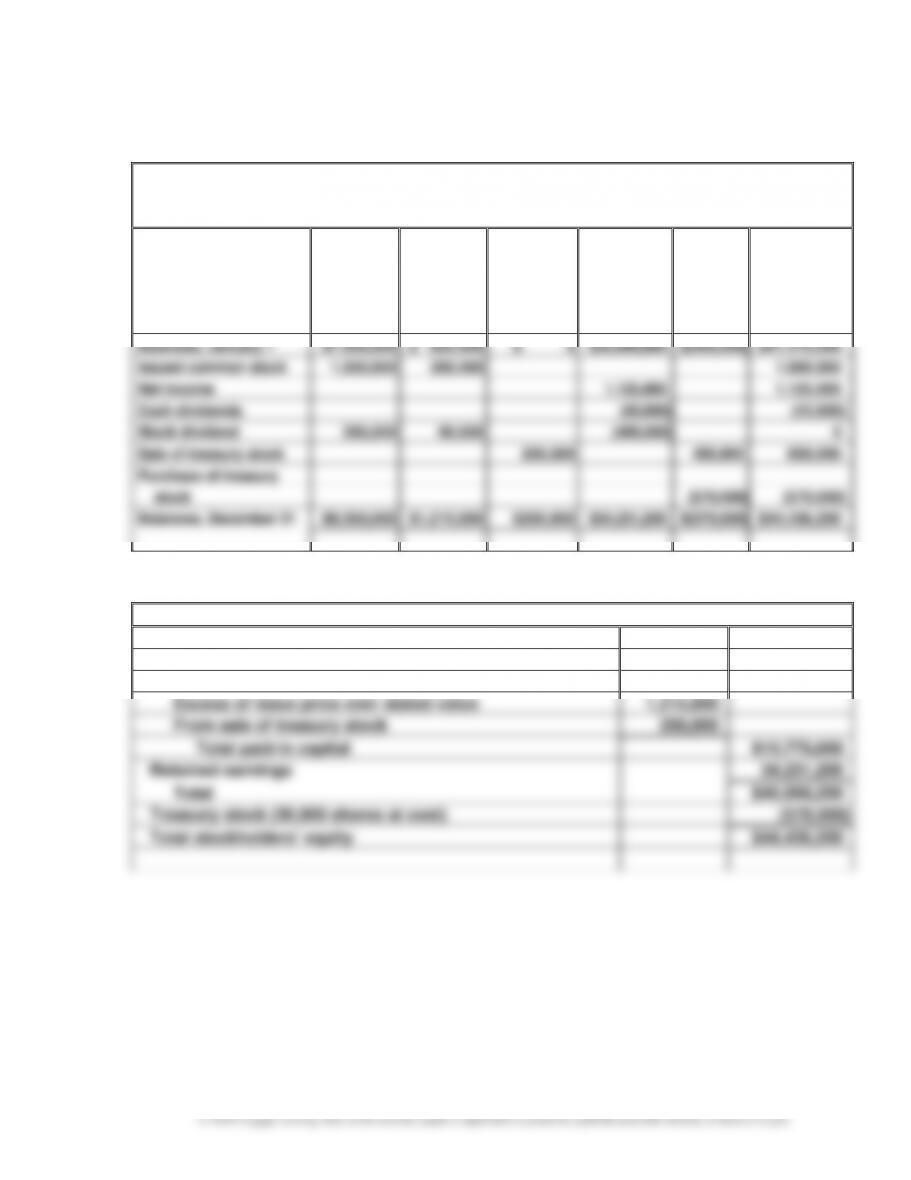

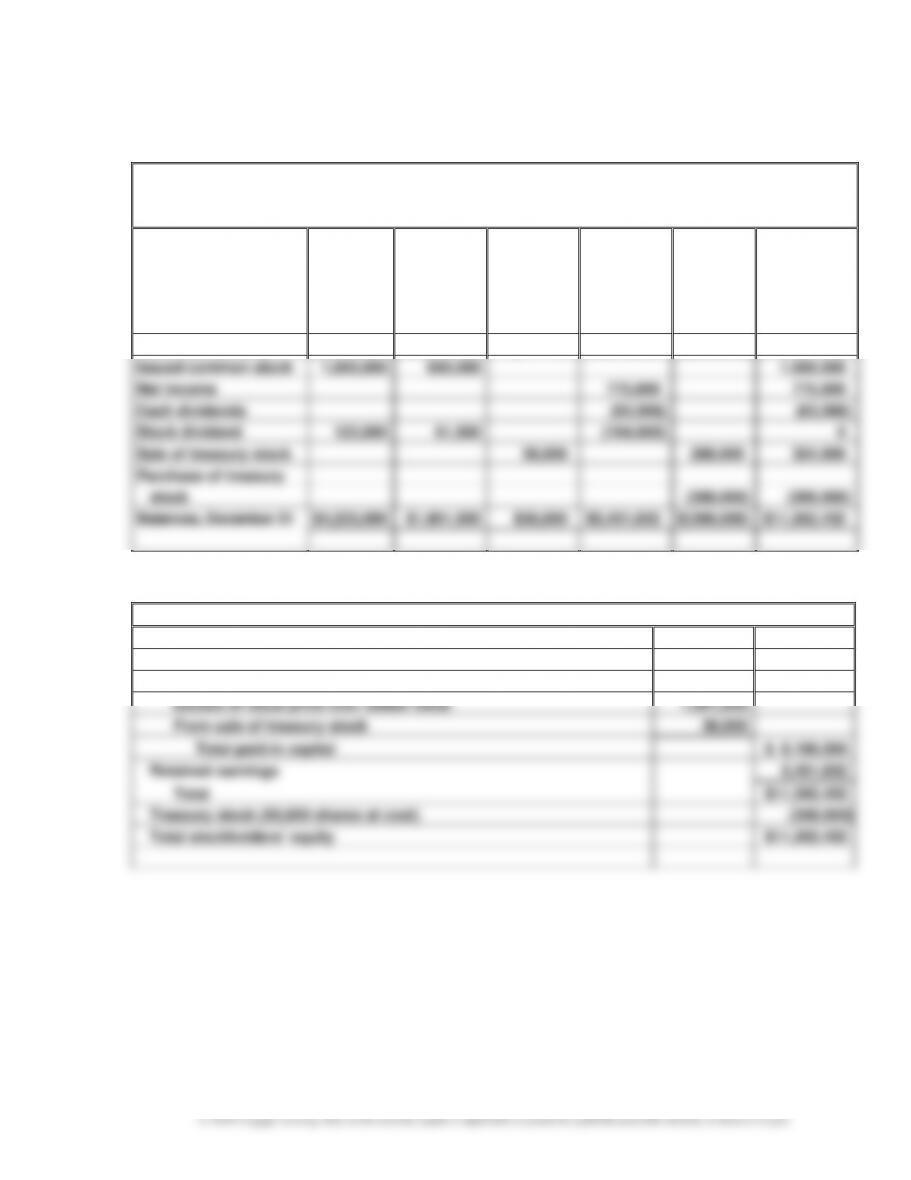

Prob. 12–4A (Concluded)

3.

Morrow Enterprises Inc.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y6

Common

Stock

Paid-In

Capital in

Excess of

Stated

Value

Paid-In

Capital from

Sale of

Treasury

Stock

Retained

Earnings

Treasury

Stock

Total

Balances, January 1

$7,500,000

$ 825,000

$ 0

$33,600,000

$(450,000)

$41,475,000

Issued common stock

1,500,000

300,000

1,800,000

Net income

1,125,000

1,125,000

Cash dividends

(43,800)

(43,800)

Stock dividend

360,000

90,000

(450,000)

0

Sale of treasury stock

200,000

450,000

650,000

Purchase of treasury

stock

(570,000)

(570,000)

Balances, December 31

$9,360,000

$1,215,000

$200,000

$34,231,200

$(570,000)

$44,436,200

4.

Stockholders’ Equity

Paid-in capital:

Common stock, $20 stated value (500,000 shares

authorized, 468,000 shares issued)

$9,360,000

Excess of issue price over stated value

1,215,000

From sale of treasury stock

200,000

Total paid-in capital

$10,775,000

Retained earnings

34,231,200

Total

$45,006,200

Treasury stock (30,000 shares at cost)

(570,000)

Total stockholders’ equity

$44,436,200

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–22

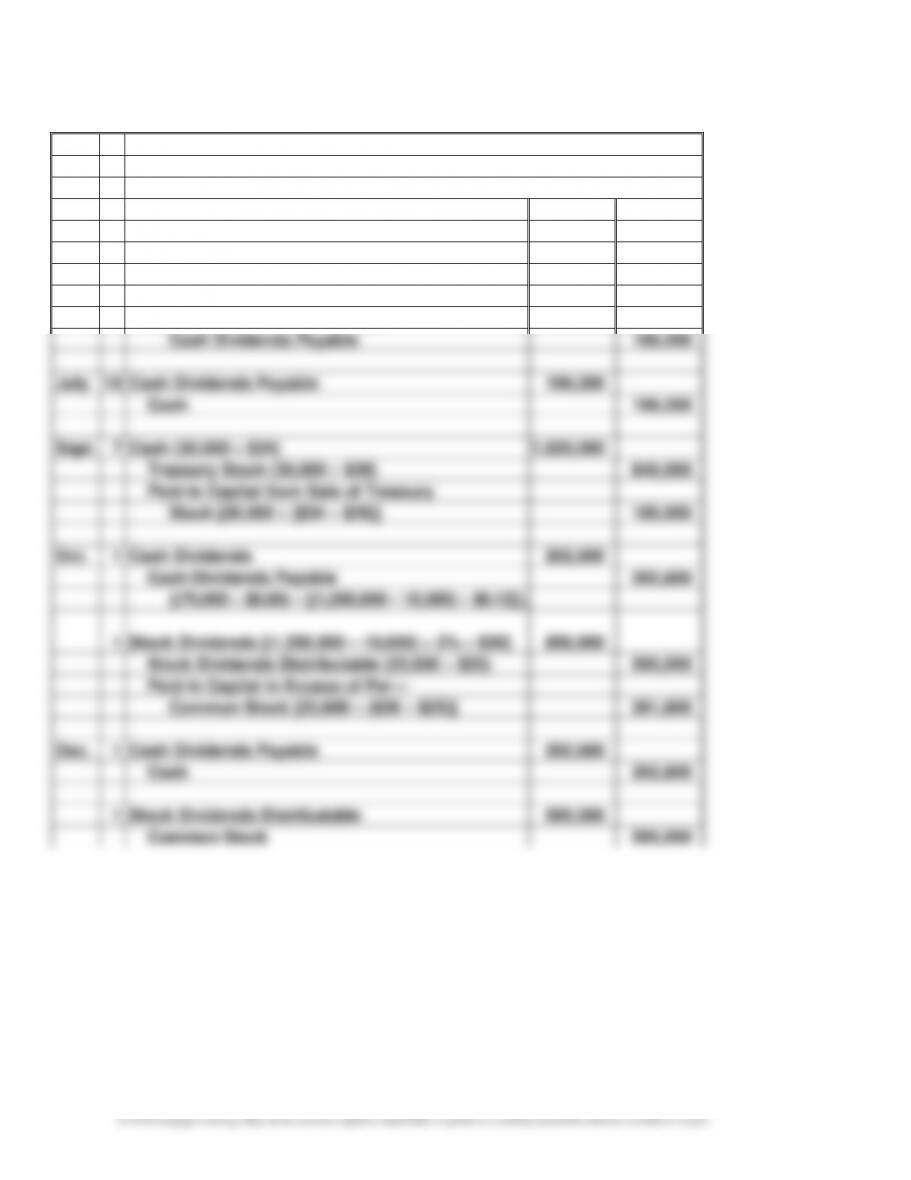

Prob. 12–5A

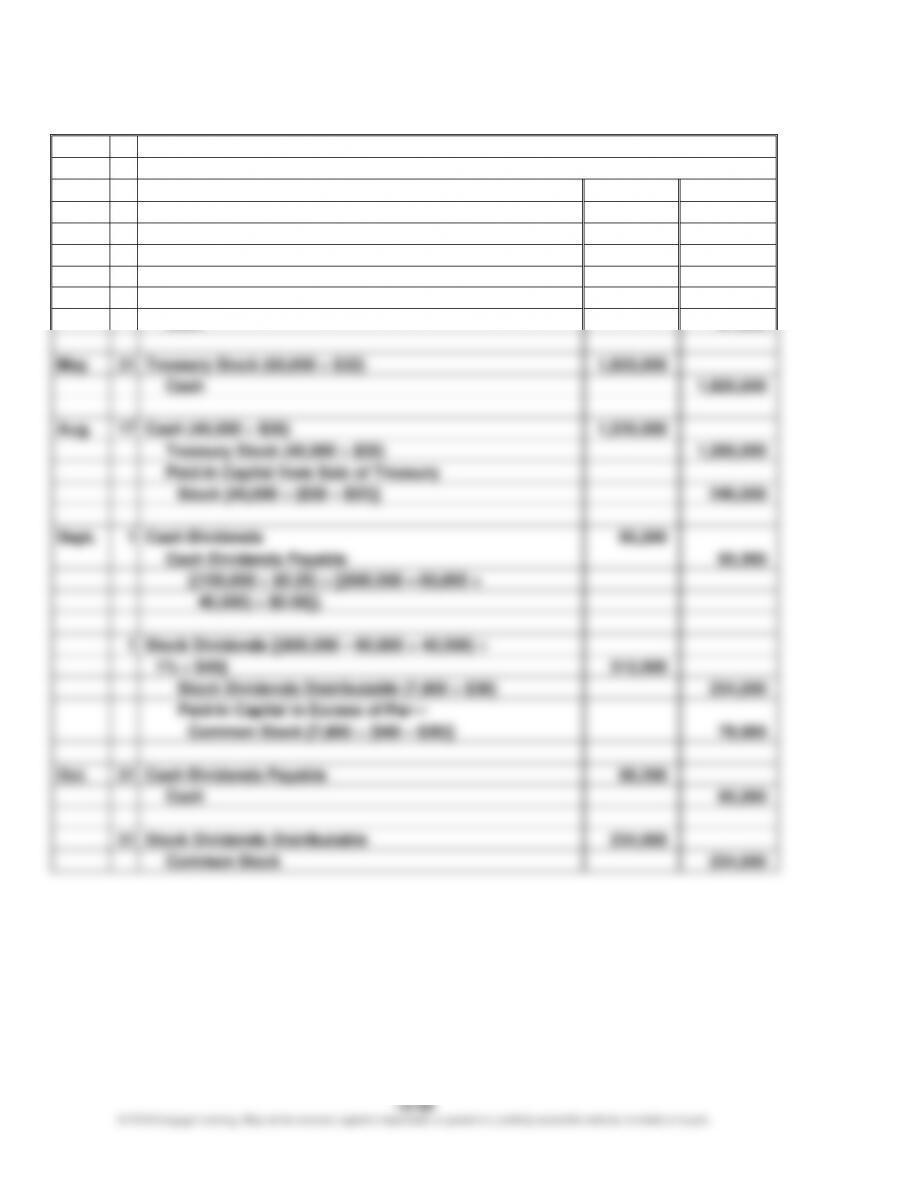

Jan.

9

No entry required. The stockholders’ ledger would be revised to

record the increased number of shares held by each stockholder

and new par value.

Feb.

28

Treasury Stock (40,000 $28)

1,120,000

Cash

1,120,000

May

1

Cash Dividends {(75,000 $0.80) +

[(1,200,000 – 40,000) $0.12]}

199,200

Cash Dividends Payable

199,200

July

10

Cash Dividends Payable

199,200

Cash

199,200

Sept.

7

Cash (30,000 $34)

1,020,000

Treasury Stock (30,000 $28)

840,000

Paid-In Capital from Sale of Treasury

Stock [30,000 ($34 – $28)]

180,000

Oct.

1

Cash Dividends

202,800

Cash Dividends Payable

202,800

{(75,000 $0.80) – [(1,200,000 – 10,000) $0.12]}.

1

Stock Dividends [(1,200,000 – 10,000) 2% $36]

856,800

Stock Dividends Distributable (23,800 $25)

595,000

Paid-In Capital in Excess of Par—

Common Stock [23,800 ($36 – $25)]

261,800

Dec.

1

Cash Dividends Payable

202,800

Cash

202,800

1

Stock Dividends Distributable

595,000

Common Stock

595,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–23

Prob. 12–1B

1.

Preferred Dividends

Common Dividends

Total

Per

Per

Year

Dividends

Total

Share

Total

Share

20Y1……..

$ 24,000

$ 24,000

$ 0.96

$ 0

$0.00

20Y2……..

10,000

10,000

0.40

0

0.00

20Y3……..

126,000

101,000*

4.04

25,000

0.25

20Y4……..

100,000

45,000

1.80

55,000

0.55

20Y5……..

125,000

45,000

1.80

80,000

0.80

20Y6……..

125,000

45,000

1.80

80,000

0.80

$10.80

$2.40

* $101,000 = (20Y1 dividends in arrears of $21,000) +

(20Y2 dividends in arrears of $35,000) +

(20Y3 current dividend of $45,000)

3. a. 1.8% ($1.80 ÷ $100)

b. 8.0% ($0.40 ÷ $5)

Prob. 12–2B

Oct.

9

Cash

1,500,000

Mortgage Note Payable

1,500,000

17

Cash (20,000 $126)

2,520,000

Preferred Stock (20,000 $120)

2,400,000

Paid-In Capital in Excess of Par—

Preferred Stock [20,000 ($126 – $120)]

120,000

28

Building

4,150,000

Land

800,000

Common Stock (300,000 $15)

4,500,000

Paid-In Capital in Excess of Par—

Common Stock [300,000 ($16.50* – $15.00)]

450,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–24

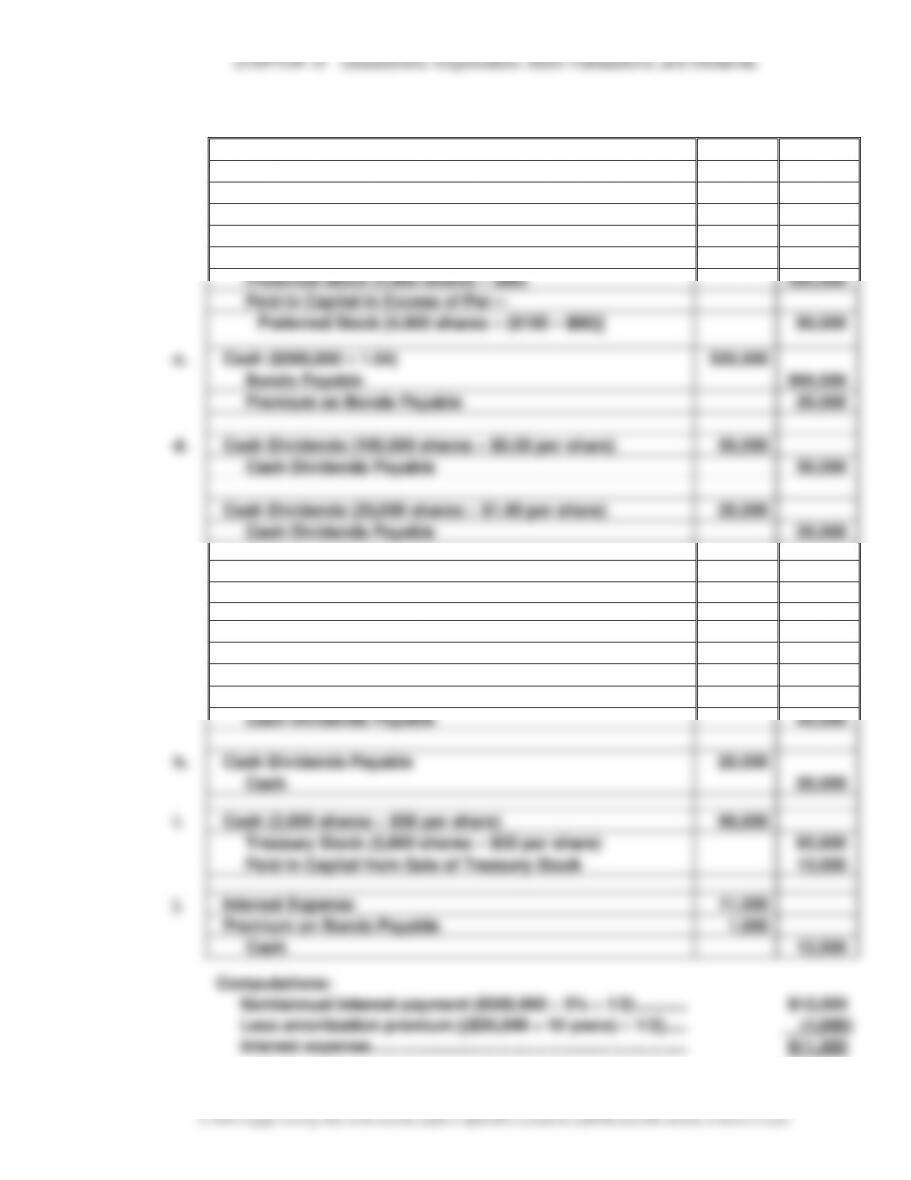

Prob. 12–3B

a.

Treasury Stock (87,500 $8)

700,000

Cash

700,000

b.

Cash (55,000 $11)

605,000

Treasury Stock (55,000 $8)

440,000

Paid-In Capital from Sale of Treasury Stock

[55,000 ($11 – $8)]

165,000

c.

Cash (20,000 $84)

1,680,000

Preferred Stock (20,000 $80)

1,600,000

Paid-In Capital in Excess of Par—Preferred

Stock [20,000 ($84 – $80)]

80,000

d.

Cash (400,000 $13)

5,200,000

Common Stock (400,000 $9)

3,600,000

Paid-In Capital in Excess of Par—Common

Stock [400,000 ($13 – $9)]

1,600,000

e.

Cash (18,000 $7.50)

135,000

Paid-In Capital from Sale of Treasury Stock

[18,000 ($8.00 – $7.50)]

9,000

Treasury Stock (18,000 $8)

144,000

f.

Cash Dividends

234,775*

Cash Dividends Payable

234,775

g.

Cash Dividends Payable

234,775

Cash

234,775

* Calculation of cash dividends:

Outstanding Shares of Stock

Preferred Stock

Common Stock

Beginning of year

60,000 shares

1,750,000 shares

(a)

(87,500)

(b)

55,000

(c)

20,000

(d)

400,000

(e)

18,000

80,000 shares

2,135,500 shares

Cash dividends per share

$1.60

$0.05

Dividends paid in (f)

$128,000

$106,775

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

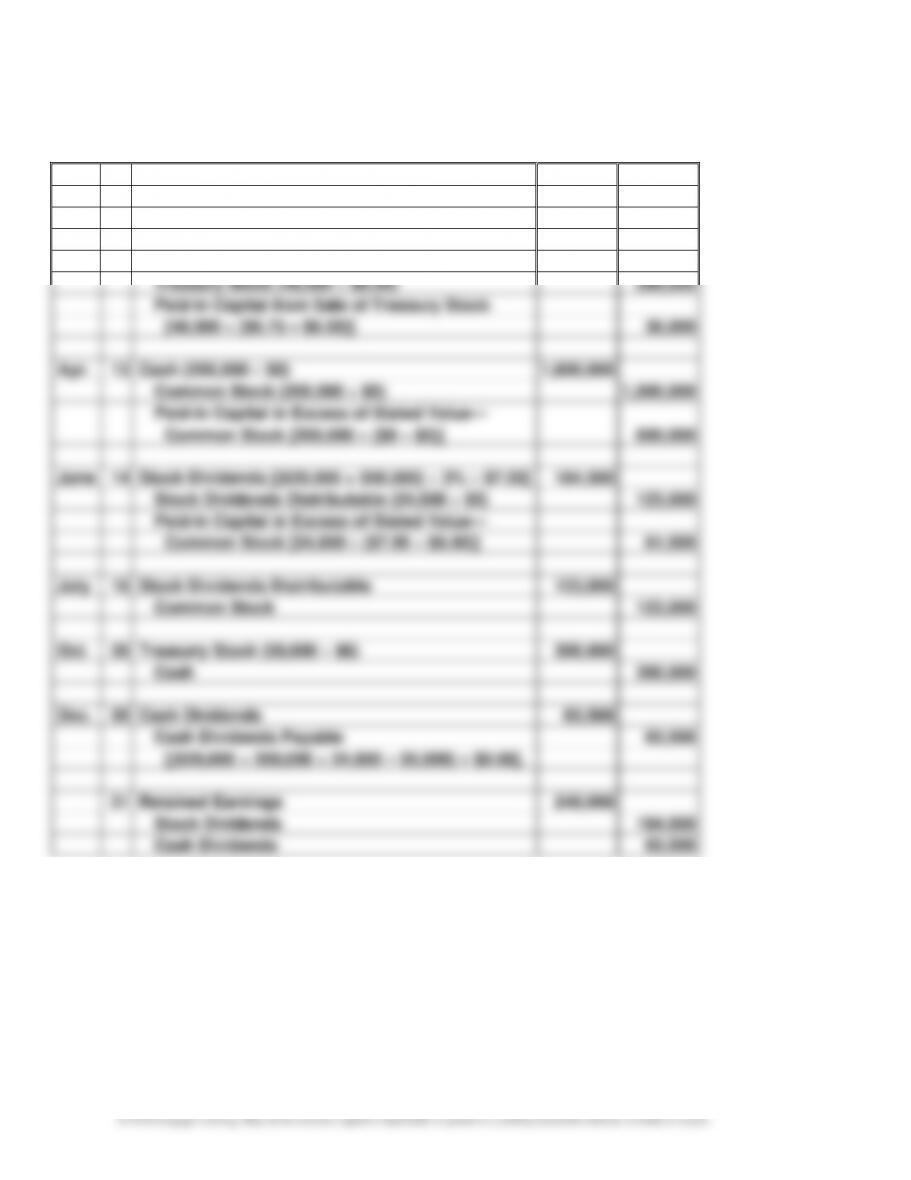

Prob. 12–4B

1. and 2.

Common Stock

Jan.

1

Bal.

3,100,000

Apr.

13

1,000,000

July

16

123,000

Dec.

31

Bal.

4,223,000

Paid-In Capital in Excess of Stated Value

—Common Stock

Jan.

1

Bal.

1,240,000

Apr.

13

600,000

June

14

61,500

Dec.

31

Bal.

1,901,500

Dec.

31

Jan.

Bal.

Dec.

31

Dec.

31

Bal.

Jan.

Mar.

15

Oct.

Dec.

Mar.

15

July

123,000

June

Dec.

31

184,500

Dec.

Dec.

31

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–26

Prob. 12–4B (Continued)

2.

20Y1

Jan.

15

Cash Dividends Payable

34,320

Cash [(620,000 – 48,000 $0.06]

34,320

Mar.

15

Cash (48,000 $6.75)

324,000

Treasury Stock (48,000 $6.00)

288,000

Paid-In Capital from Sale of Treasury Stock

[48,000 ($6.75 – $6.00)]

36,000

Apr.

13

Cash (200,000 $8)

1,600,000

Common Stock (200,000 $5)

1,000,000

Paid-In Capital in Excess of Stated Value—

Common Stock [200,000 ($8 – $5)]

600,000

June

14

Stock Dividends [(620,000 + 200,000) 3% $7.50]

184,500

Stock Dividends Distributable (24,600 $5)

123,000

Paid-In Capital in Excess of Stated Value—

Common Stock [24,600 ($7.50 – $5.00)]

61,500

July

16

Stock Dividends Distributable

123,000

Common Stock

123,000

Oct.

30

Treasury Stock (50,000 $6)

300,000

Cash

300,000

Dec.

30

Cash Dividends

63,568

Cash Dividends Payable

63,568

[(620,000 + 200,000 + 24,600 – 50,000) $0.08].

31

Retained Earnings

248,068

Stock Dividends

184,500

Cash Dividends

63,568

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–27

Prob. 12–4B (Concluded)

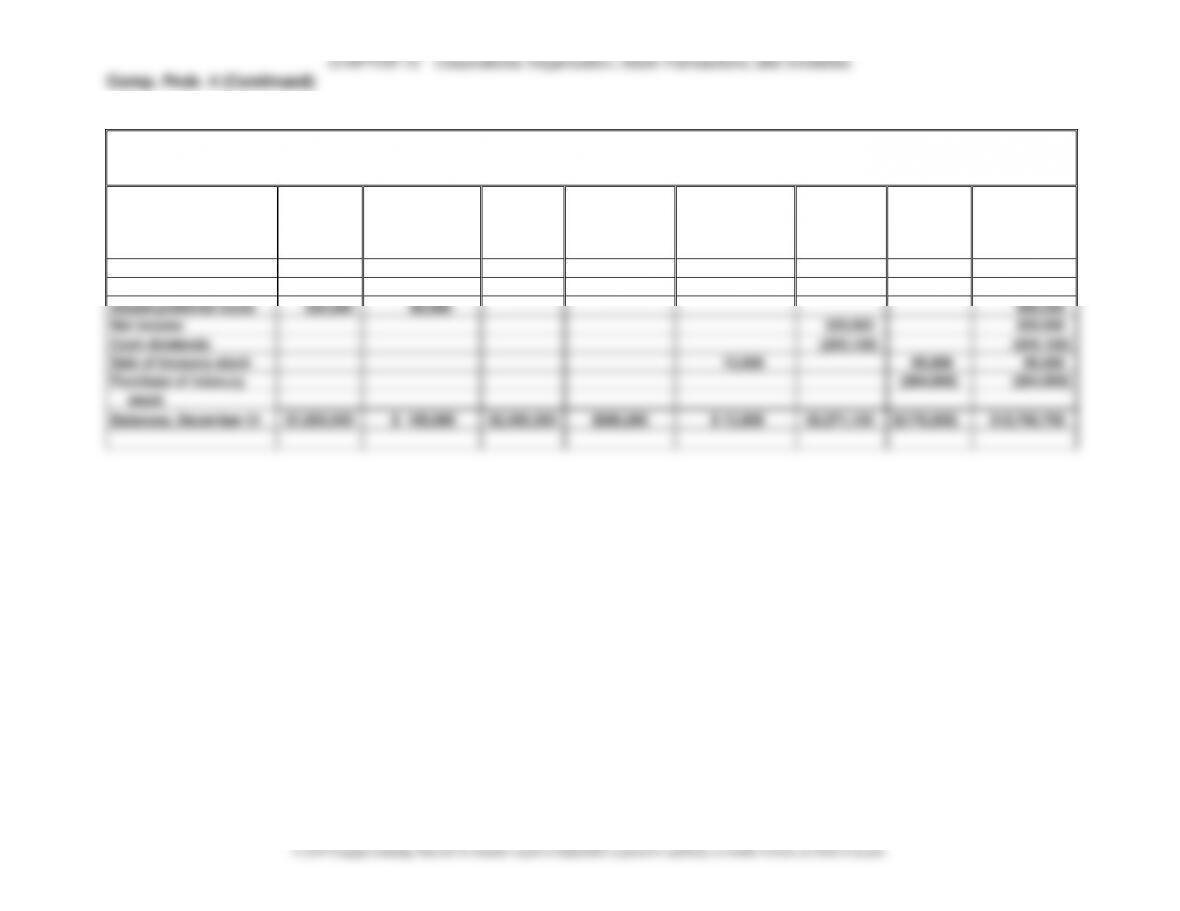

3.

Nav-Go Enterprises Inc.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y1

Common

Stock

Paid-In

Capital in

Excess of

Stated Value

Paid-In

Capital from

Sale of

Treasury

Stock

Retained

Earnings

Treasury

Stock

Total

Balances, January 1

$3,100,000

$1,240,000

$ 0

$4,875,000

$(288,000)

$ 8,927,000

Issued common stock

1,000,000

600,000

1,600,000

Net income

775,000

775,000

Cash dividends

(63,568)

(63,568)

Stock dividend

123,000

61,500

(184,500)

0

Sale of treasury stock

36,000

288,000

324,000

Purchase of treasury

stock

(300,000)

(300,000)

Balances, December 31

$4,223,000

$1,901,500

$36,000

$5,401,932

$(300,000)

$11,262,432

4.

Stockholders’ Equity

Paid-in capital:

Common stock, $5 stated value (900,000 shares

authorized, 844,600 shares issued)

$4,223,000

Excess of issue price over stated value

1,901,500

From sale of treasury stock

36,000

Total paid-in capital

$ 6,160,500

Retained earnings

5,401,932

Total

$11,562,432

Treasury stock (50,000 shares at cost)

(300,000)

Total stockholders’ equity

$11,262,432

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

Prob. 12–5B

Jan.

15

No entry required. The stockholders’ ledger would be revised to record the

increased number of shares held by each stockholder and new par value.

Mar.

1

Cash Dividends

81,000

Cash Dividends Payable

81,000

[(100,000 $0.25) + (800,000 $0.07)].

Apr.

30

Cash Dividends Payable

81,000

Cash

81,000

May

31

Treasury Stock (60,000 $32)

1,920,000

Cash

1,920,000

Aug.

17

Cash (40,000 $38)

1,520,000

Treasury Stock (40,000 $32)

1,280,000

Paid-In Capital from Sale of Treasury

Stock [40,000 ($38 – $32)]

240,000

Sept.

1

Cash Dividends

95,200

Cash Dividends Payable

95,200

{(100,000 $0.25) + [(800,000 – 60,000 +

40,000) $0.09]}.

1

Stock Dividends [(800,000 – 60,000 + 40,000)

1% $40]

312,000

Stock Dividends Distributable (7,800 $30)

234,000

Paid-In Capital in Excess of Par—

Common Stock [7,800 ($40 – $30)]

78,000

Oct.

31

Cash Dividends Payable

95,200

Cash

95,200

31

Stock Dividends Distributable

234,000

Common Stock

234,000

12–29

COMPREHENSIVE PROBLEM 4

1.

a.

Cash (15,000 $30)

450,000

Common Stock (15,000 $20)

300,000

Paid-In Capital in Excess of Par—

Common Stock [15,000 ($30 – $20)]

150,000

b.

Cash (4,000 shares $100)

400,000

Preferred Stock (4,000 shares $80)

320,000

Paid-In Capital in Excess of Par—

Preferred Stock [4,000 shares ($100 – $80)]

80,000

c.

Cash ($500,000 1.04)

520,000

Bonds Payable

500,000

Premium on Bonds Payable

20,000

d.

Cash Dividends (100,000 shares $0.50 per share)

50,000

Cash Dividends Payable

50,000

Cash Dividends (20,000 shares $1.00 per share)

20,000

Cash Dividends Payable

20,000

e.

Cash Dividends Payable

70,000

Cash

70,000

f.

Treasury Stock (8,000 shares $33 per share)

264,000

Cash

264,000

g.

Cash Dividends

20,000

Cash Dividends Payable

20,000

h.

Cash Dividends Payable

20,000

Cash

20,000

i.

Cash (2,600 shares $38 per share)

98,800

Treasury Stock (2,600 shares $33 per share)

85,800

Paid-In Capital from Sale of Treasury Stock

13,000

j.

Interest Expense

11,500

Premium on Bonds Payable

1,000

Cash

12,500

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–30

Comp. Prob. 4 (Continued)

2. a.

Equinox Products Inc.

Income Statement

For the Year Ended December 31, 20Y8

Sales

$ 5,313,000

Cost of goods sold

(3,700,000)

Gross profit

$ 1,613,000

Operating expenses:

Selling expenses:

Sales salaries expense

$385,000

Sales commissions

185,000

Advertising expense

150,000

Depreciation expense—store

buildings and equipment

100,000

Delivery expense

30,000

Store supplies expense

21,000

Miscellaneous selling expense

14,000

$885,000

Administrative expenses:

Office salaries expense

$170,000

Office rent expense

50,000

Depreciation expense—office

buildings and equipment

30,000

Office supplies expense

10,000

Miscellaneous administrative

expense

7,500

267,500

Total operating expenses

(1,152,500)

Operating income

$ 460,500

Other revenue and expense:

Interest revenue

$ 30,000

Interest expense

(21,000)

9,000

Income before income tax

$ 469,500

Income tax

(140,500)

Net income

$ 329,000

12–31

© 2019 Cengage Learning. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Comp. Prob. 4 (Continued)

2. b.

Equinox Products Inc.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y8

Preferred

Stock

Paid-in Capital in

Excess of

Par—Preferred

Stock

Common

Stock

Paid-In Capital in

Excess of Par—

Common Stock

Paid-In Capital

From Sale of

Treasury Stock

Retained

Earnings

Treasury

Stock

Total

Balances, January 1

$1,280,000

$ 70,000

$1,700,000

$736,800

$ 0

$8,197,220

$ 0

$11,984,020

Issued common stock

300,000

150,000

450,000

Issued preferred stock

320,000

80,000

400,000

Net income

329,000

329,000

Cash dividends

(255,120)

(255,120)

Sale of treasury stock

13,000

85,800

98,800

Purchase of treasury

(264,000)

(264,000)

stock

Balances, December 31

$1,600,000

$ 150,000

$2,000,000

$886,800

$ 13,000

$8,271,100

$(178,200)

$12,742,700

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–32

Comp. Prob. 4 (Continued)

2. c.

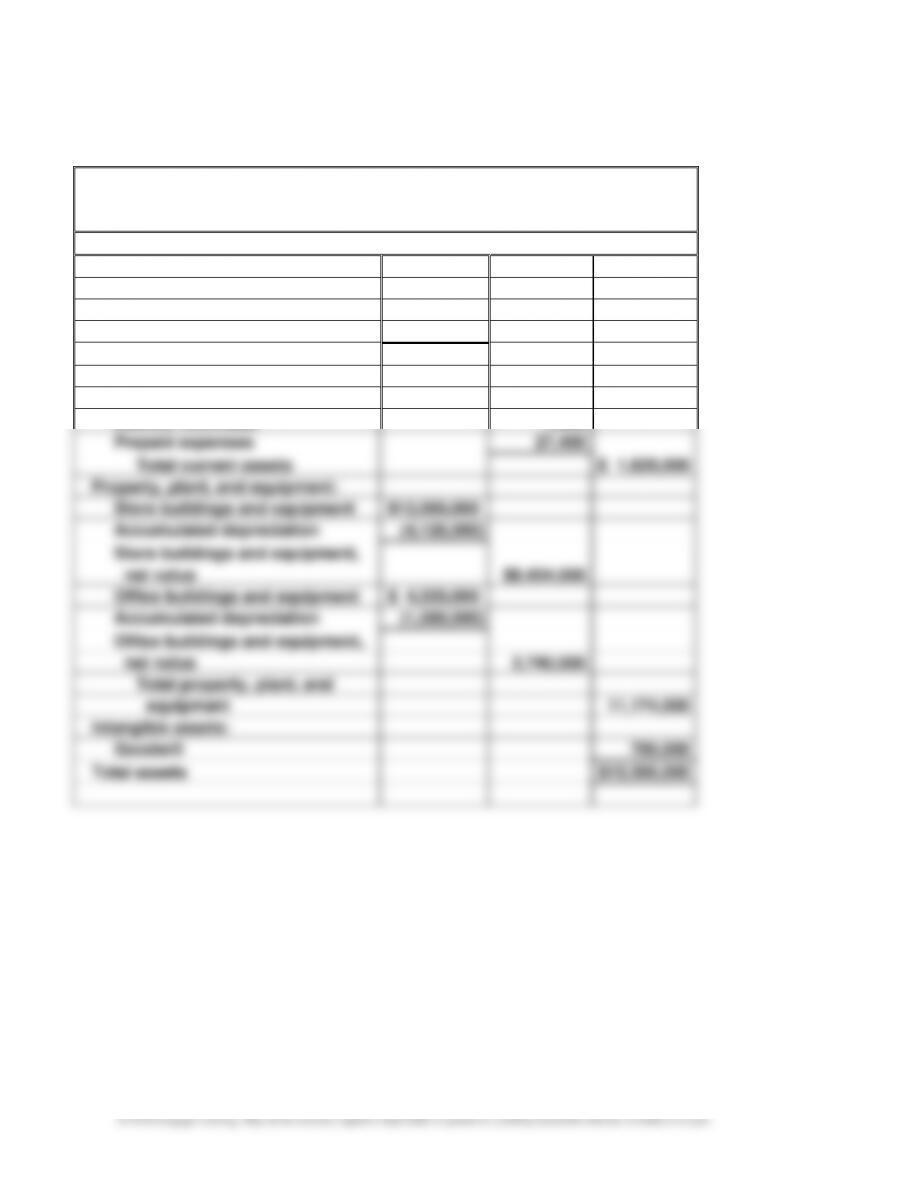

Equinox Products Inc.

Balance Sheet

December 31, 20Y8

Assets

Current assets:

Cash

$ 282,850

Accounts receivable

$ 545,000

Allowance for doubtful accounts

(8,450)

Accounts receivable, net

536,550

Inventory, at lower of cost

(FIFO) or market

778,000

Interest receivable

1,200

Prepaid expenses

27,400

Total current assets

$ 1,626,000

Property, plant, and equipment:

Store buildings and equipment

$12,560,000

Accumulated depreciation

(4,126,000)

Store buildings and equipment,

net value

$8,434,000

Office buildings and equipment

$ 4,320,000

Accumulated depreciation

(1,580,000)

Office buildings and equipment,

net value

2,740,000

Total property, plant, and

equipment

11,174,000

Intangible assets:

Goodwill

700,000

Total assets

$13,500,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–33

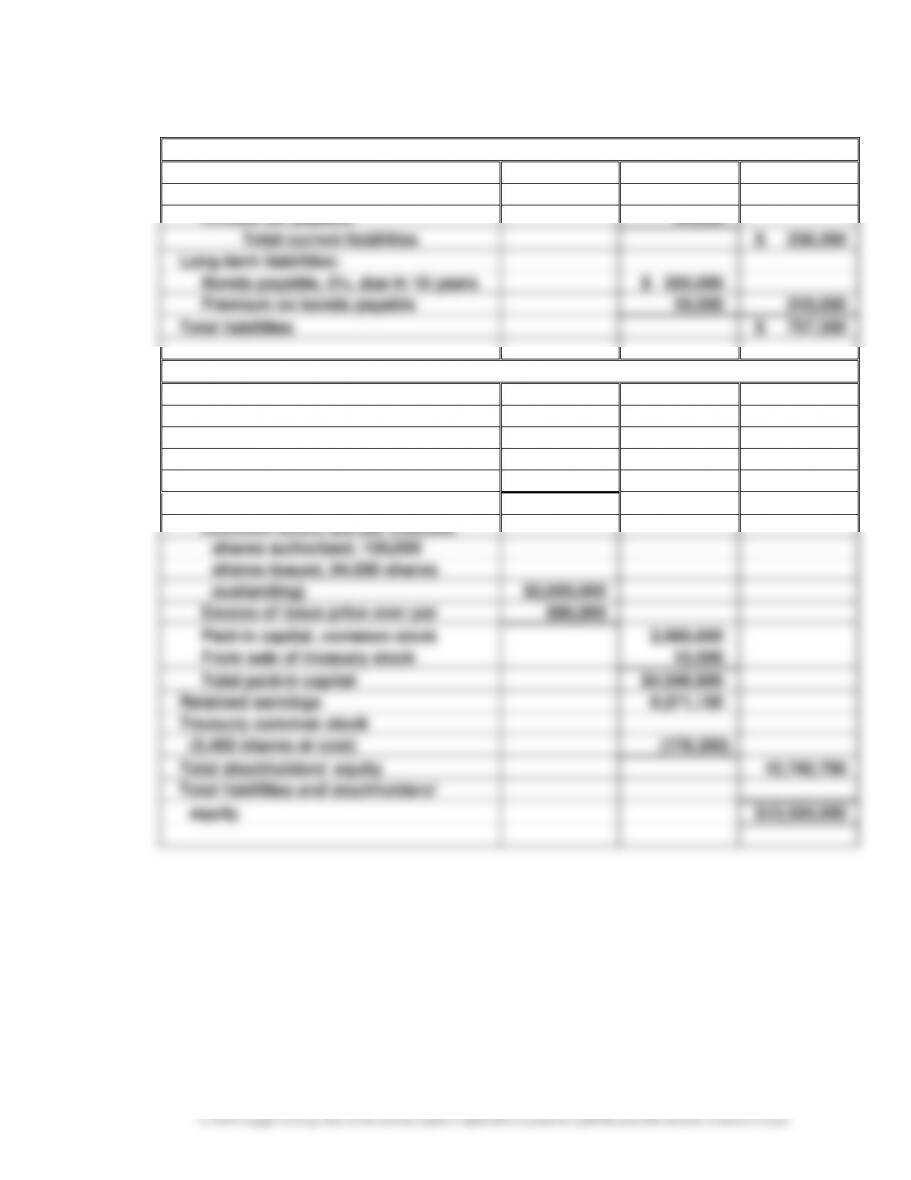

Comp. Prob. 4 (Concluded)

Liabilities

Current liabilities:

Accounts payable

$ 194,300

Income tax payable

44,000

Total current liabilities

$ 238,300

Long-term liabilities:

Bonds payable, 5%, due in 10 years

$ 500,000

Premium on bonds payable

19,000

519,000

Total liabilities

$ 757,300

Stockholders’ Equity

Paid-in capital:

Preferred 5% stock, $80 par

(30,000 shares authorized;

20,000 shares issued)

$1,600,000

Excess of issue price over par

150,000

Paid-in capital, preferred stock

$1,750,000

Common stock, $20 par (400,000

shares authorized; 100,000

shares issued, 94,600 shares

oustanding)

$2,000,000

Excess of issue price over par

886,800

Paid-in capital, common stock

2,886,800

From sale of treasury stock

13,000

Total paid-in capital

$4,649,800

Retained earnings

8,271,100

Treasury common stock

(5,400 shares at cost)

(178,200)

Total stockholders’ equity

12,742,700

Total liabilities and stockholders’

equity

$13,500,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–34

MAKE A DECISION

MAD 12–1

a.

gOutstandin Shares Common of Number Average

Dividends PreferredIncomeNet

Share per Earnings −

=

$0

–

$2,371 =

3,207

b. Amazon’s earnings per share is $5.00, while Wal-Mart has an earnings per share of $4.58.

While both companies are profitable, Amazon is more profitable than Wal-Mart from an

earnings-per-share perspective.

c. Amazon’s market price was $750, while Wal-Mart’s was $69; Amazon’s market price is

almost eleven times as large as Wal-Mart’s ($750 $69). This may seem unusual, given

MAD 12–2

a.

gOutstandin Shares Common of Number Average

Dividends PreferredIncomeNet

Share per Earnings −

=

$1,662$17,906 =

−

5,052.8

b. Wells Fargo’s earnings per share is $4.03, compared to Bank of America’s earnings per

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

MAD 12–2 (Concluded)

c. We would expect the market price of Wells Fargo to be higher than the market price of

MAD 12–3

a.

Year 3

Year 2

Year 1

Net income

$1,407

$ 888

$1,450

Preferred dividends

(14)

(14)

(14)

Numerator

$1,393

$ 874

$1,436

Denominator: Average

number of common shares

outstanding

÷ 499

÷ 484

÷ 468

Earnings per share

$ 2.79

$ 1.81

$ 3.07

b. The earnings per share declined from $3.07 to $1.81 between Year 1 and Year 2. In Year 3,

the earnings per share increased from $1.81 to $2.79, or 54% [($2.79 – $1.81) ÷ $1.81].

A horizontal analysis of the net income and the average number of common shares

outstanding with Year 1 as the base year is as follows:

Year 3

Year 2

Year 1

Net income

Average number of common

97%

($1,407 ÷ $1,450)

61%

($888 ÷ $1,450)

100%

shares outstanding

107%

(499 ÷ 468)

103%

(484 ÷ 468)

100%

The decrease in earnings per share in Year 2 and the subsequent increase in Year 3

is mostly explained by the change in net income growth over the three years. The

average number of common shares outstanding grew modestly, which has the effect

of reducing the growth in earnings per share. Thus, for example, the earnings per

share between Year 2 and Year 3 grew 54% [($2.79 – $1.81) ÷ $1.81], while the net

income grew 58% [($1,407 – $888) ÷ $888].

12–37

MAD 12–5 (Concluded)

d. From a stockholder’s perspective, the earnings per share is a better relative measure

of earnings between the two banks. BB&T has stronger earnings and is able to divide

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

TAKE IT FURTHER

TIF 12–1

Tommy is clearly acting unethically for several reasons. First, he is violating the

company’s policy on stock purchases. This policy was established to ensure the fair and

timely dissemination of information that gives all potential investors the same chance to

TIF 12–2

Lou and Shirley are behaving in a professional manner as long as full and complete

TIF 12–3

A sample solution based on Alphabet’s Form 10-K for the fiscal year ended December 31,

2016, follows:

1. Alphabet Inc.

3. Alphabet is a collection of businesses, the largest of which is Google. At its core, Google

4. $167,497 million

6. $139,036 million ($167,497 million total assets – $28,461 million total liabilities)

8. $19,478 million

9. Common stock: Class A authorized, 9 million; Class B authorized, 3 million; Class C

11. $771.82 at December 30, 2016

13. Alphabet has never declared or paid a cash dividend.

12–39

TIF 12–4

Memo

To: Chairman of the Board

From: A+ Student

Re: Fourth Quarter 20Y8 Cash Dividend

In order to prudently declare a dividend for the fourth quarter, the company must have a

sufficient retained earnings balance from which to declare the dividend. On December

31, 20Y8, Motion Designs has a $4,630,000 balance in retained earnings. This balance is

more than enough to cover the $90,000 declaration of the normal quarterly cash dividend

Before declaring a dividend, the company should also consider its working capital and

the effect of plant expansion on the current ratio requirement of the loan. On December

31, 20Y8, the company has working capital of $5,000,000 ($7,000,000 – $2,000,000),