12–1

CHAPTER 12

CORPORATIONS: ORGANIZATION, STOCK

TRANSACTIONS, AND DIVIDENDS

DISCUSSION QUESTIONS

2. The broker is not correct. Corporations are not legally liable to pay dividends until the dividends are

3. The company may not have had enough cash on hand to pay a dividend on the common stock, or resources

may be needed for plant expansion, replacement of facilities, payment of liabilities, etc.

b. Stockholders’ equity

7. a. It has no effect on revenue or expense.

b. It reduces stockholders’ equity by $3,000,000.

9. The three classifications of restrictions on retained earnings are legal, contractual, and discretionary.

Restrictions are normally reported in the notes to the financial statements.

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–2

BASIC EXERCISES

BE 12–1

20Y1

20Y2

20Y3

Amount distributed ………………………………….

$28,500

$ 6,000

$110,000

Preferred dividend (15,000 shares) ……………

(7,500)

(6,000)

(9,000)*

Common dividend (100,000 shares) …………..

$21,000

$ 0

$101,000

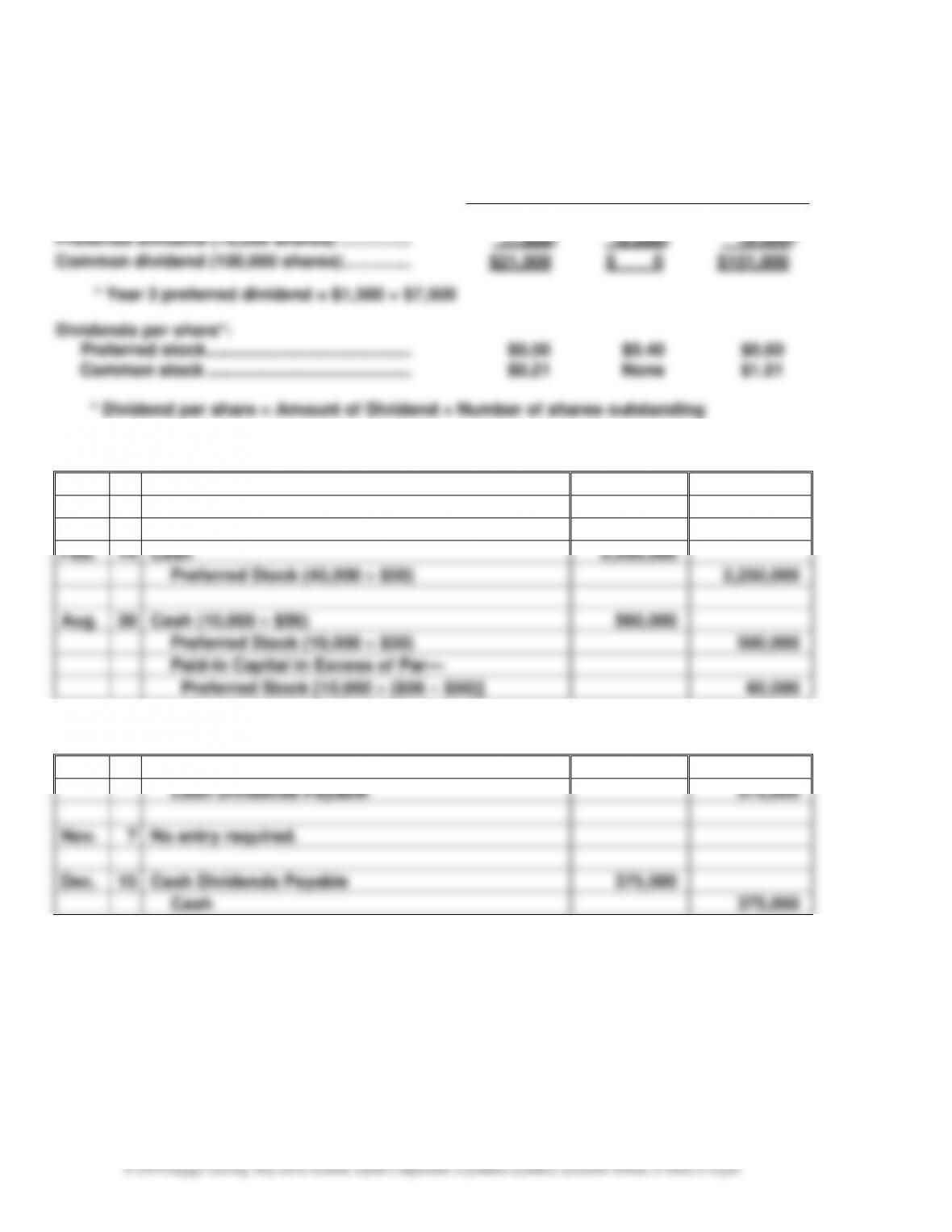

BE 12–2

Jan.

22

Cash

1,280,000

Common Stock (160,000 $8)

1,280,000

Feb.

14

Cash

2,250,000

Preferred Stock (45,000 $50)

2,250,000

Aug.

30

Cash (10,000 $56)

560,000

Preferred Stock (10,000 $50)

500,000

Paid-In Capital in Excess of Par—

Preferred Stock [10,000 ($56 – $50)]

60,000

BE 12–3

Oct.

1

Cash Dividends

375,000

Cash Dividends Payable

375,000

Nov.

7

No entry required.

Dec.

15

Cash Dividends Payable

375,000

Cash

375,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

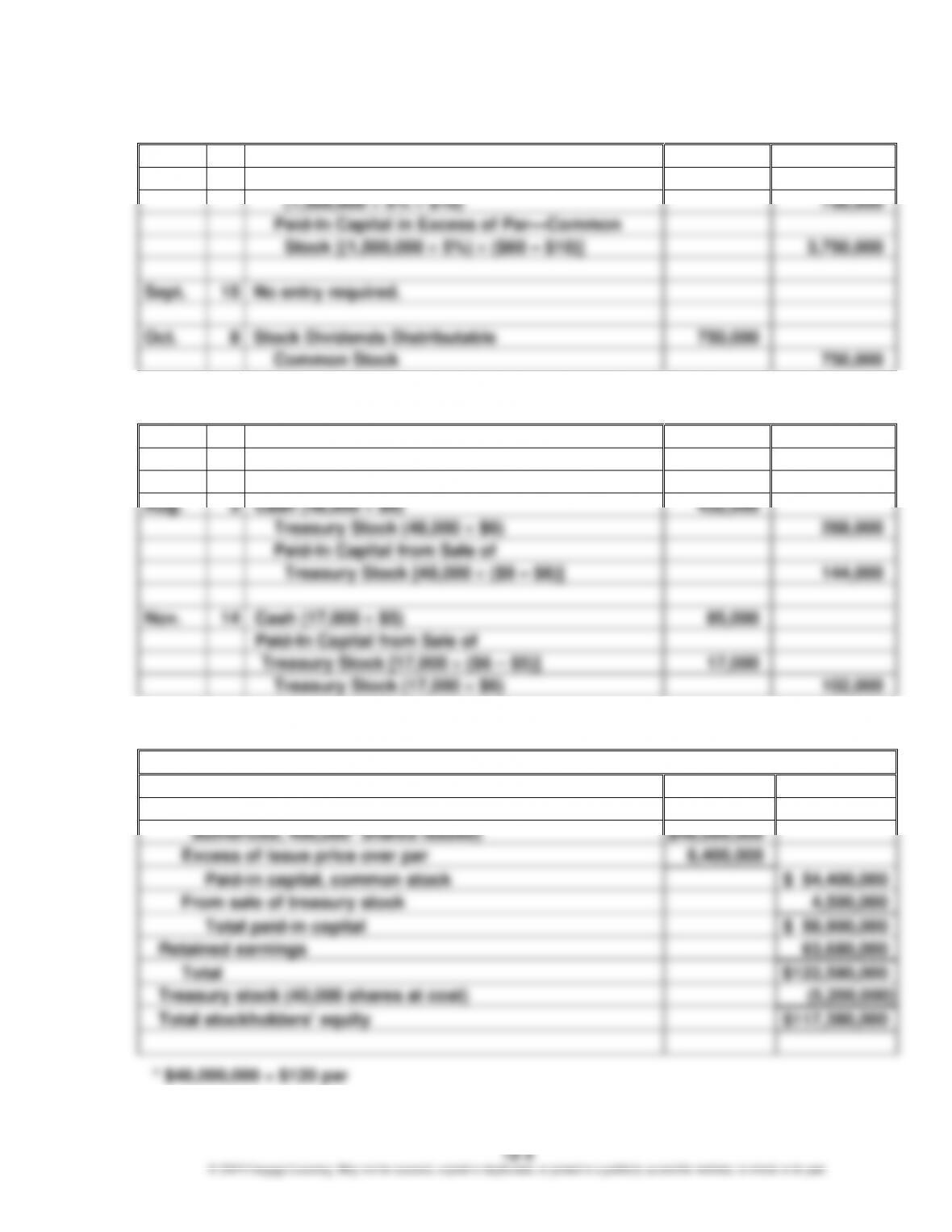

BE 12–4

Aug.

2

Stock Dividends (1,500,000 5% $60)

4,500,000

Stock Dividends Distributable

(1,500,000 5% $10)

750,000

Paid-In Capital in Excess of Par—Common

Stock [(1,500,000 5%) ($60 – $10)]

3,750,000

Sept.

15

No entry required.

Oct.

8

Stock Dividends Distributable

750,000

Common Stock

750,000

BE 12–5

May

27

Treasury Stock (65,000 $6)

390,000

Cash

390,000

Aug.

3

Cash (48,000 $9)

432,000

Treasury Stock (48,000 $6)

288,000

Paid-In Capital from Sale of

Treasury Stock [48,000 ($9 – $6)]

144,000

Nov.

14

Cash (17,000 $5)

85,000

Paid-In Capital from Sale of

Treasury Stock [17,000 ($6 – $5)]

17,000

Treasury Stock (17,000 $6)

102,000

BE 12–6

Stockholders’ Equity

Paid-in capital:

Common stock, $120 par (500,000 shares

authorized, 400,000* shares issued)

$48,000,000

Excess of issue price over par

6,400,000

Paid-in capital, common stock

$ 54,400,000

From sale of treasury stock

4,500,000

Total paid-in capital

$ 58,900,000

Retained earnings

63,680,000

Total

$ 122,580,000

Treasury stock (40,000 shares at cost)

(5,200,000)

Total stockholders’ equity

$117,380,000

12–4

BE 12–7

Noric Cruises Inc.

Statement of Stockholders’ Equity

For the Month Ended October 31

Common

Stock

Additional

Paid-In

Capital

Retained

Earnings

Total

Balances, October 1

$150,000

$3,225,000

$12,400,000

$15,775,000

Issued common stock

50,000

750,000

800,000

Net income

2,350,000

2,350,000

Dividends

(475,000)

(475,000)

Balances, October 31

$200,000

$3,975,000

$14,275,000

$18,450,000

BE 12–8

a.

gOutstandin Shares Common of Number Average

Dividends PreferredIncomeNet

Share per Earnings:20Y5 +

=

$18.60

shares 80,000

$1,488,000

shares 80,000

$50,000 – $1,538,000

==

=

gOutstandin Shares Common of Number Average

Dividends PreferredIncomeNet

Share Per Earnings:20Y6 −

=

$21.18

shares 115,000

$2,435,700

shares 115,000

$50,000$2,485,700

==

−

=

b. The increase in the earnings per share from $18.60 to $21.18 indicates a favorable change

in the company’s profitability.

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–5

EXERCISES

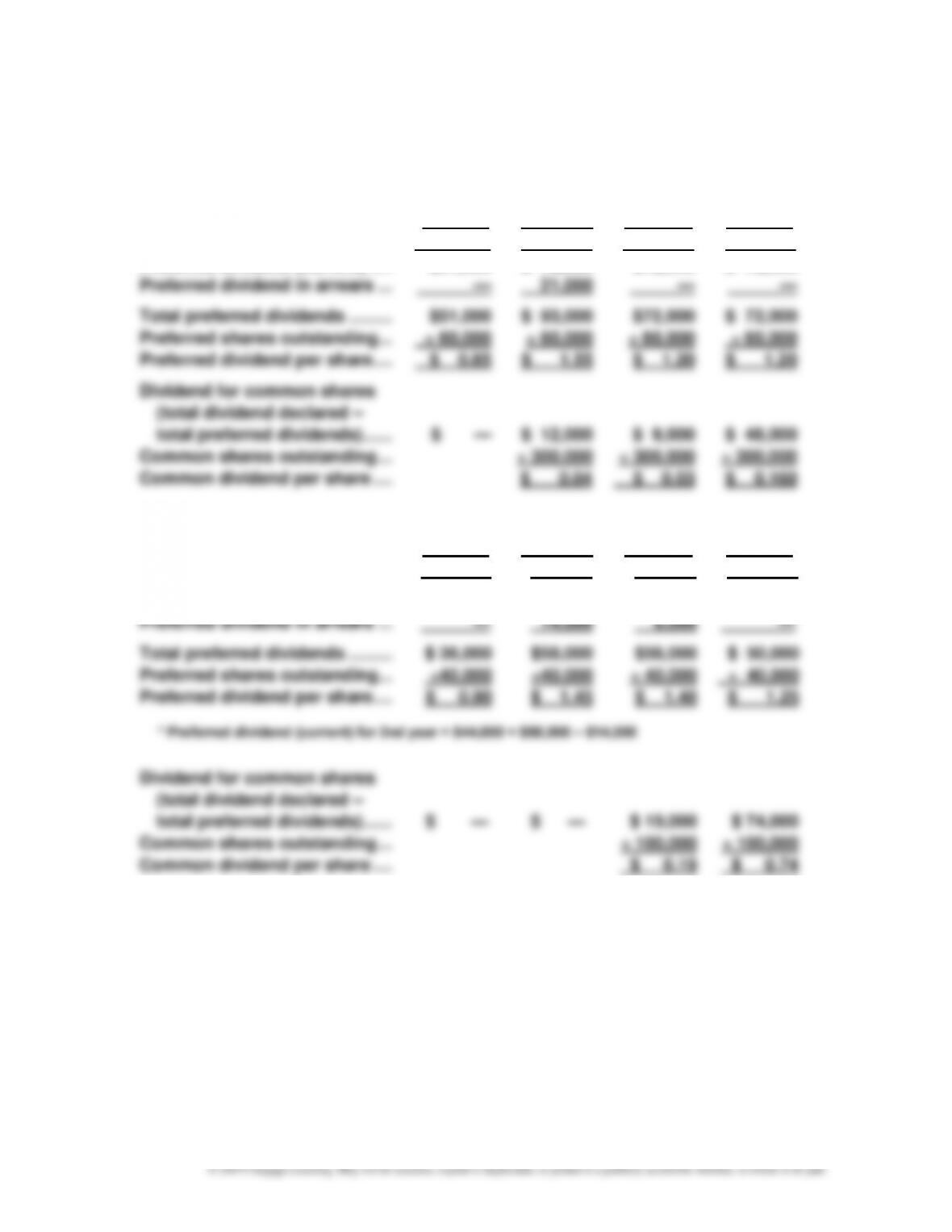

Ex. 12–1

1st Year

2nd Year

3rd Year

4th Year

Total dividend declared …………

$51,000

$105,000

$81,000

$120,000

Preferred dividend (current) …..

$51,000

$ 72,000

$72,000

$ 72,000

Preferred dividend in arrears …

—

21,000

—

—

Total preferred dividends ………

$51,000

$ 93,000

$72,000

$ 72,000

Preferred shares outstanding…

÷ 60,000

÷ 60,000

÷ 60,000

÷ 60,000

Preferred dividend per share ….

$ 0.85

$ 1.55

$ 1.20

$ 1.20

Dividend for common shares

(total dividend declared –

total preferred dividends) ……

$ —

$ 12,000

$ 9,000

$ 48,000

Common shares outstanding …

÷ 300,000

÷ 300,000

÷ 300,000

Common dividend per share ….

$ 0.04

$ 0.03

$ 0.160

Ex. 12–2

1st Year

2nd Year

3rd Year

4th Year

Total dividend declared …………

$ 36,000

$58,000

$75,000

$124,000

Preferred dividend (current) …..

$ 36,000

$44,000*

$50,000

$ 50,000

Preferred dividend in arrears …

—

14,000

6,000

—

Total preferred dividends ………

$ 36,000

$58,000

$56,000

$ 50,000

Preferred shares outstanding…

÷40,000

÷40,000

÷ 40,000

÷ 40,000

Preferred dividend per share ….

$ 0.90

$ 1.45

$ 1.40

$ 1.25

* Preferred dividend (current) for 2nd year = $44,000 = $58,000 – $14,000

Dividend for common shares

(total dividend declared –

total preferred dividends) ……

$ —

$ —

$ 19,000

$ 74,000

Common shares outstanding …

÷ 100,000

÷ 100,000

Common dividend per share ….

$ 0.19

$ 0.74

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–6

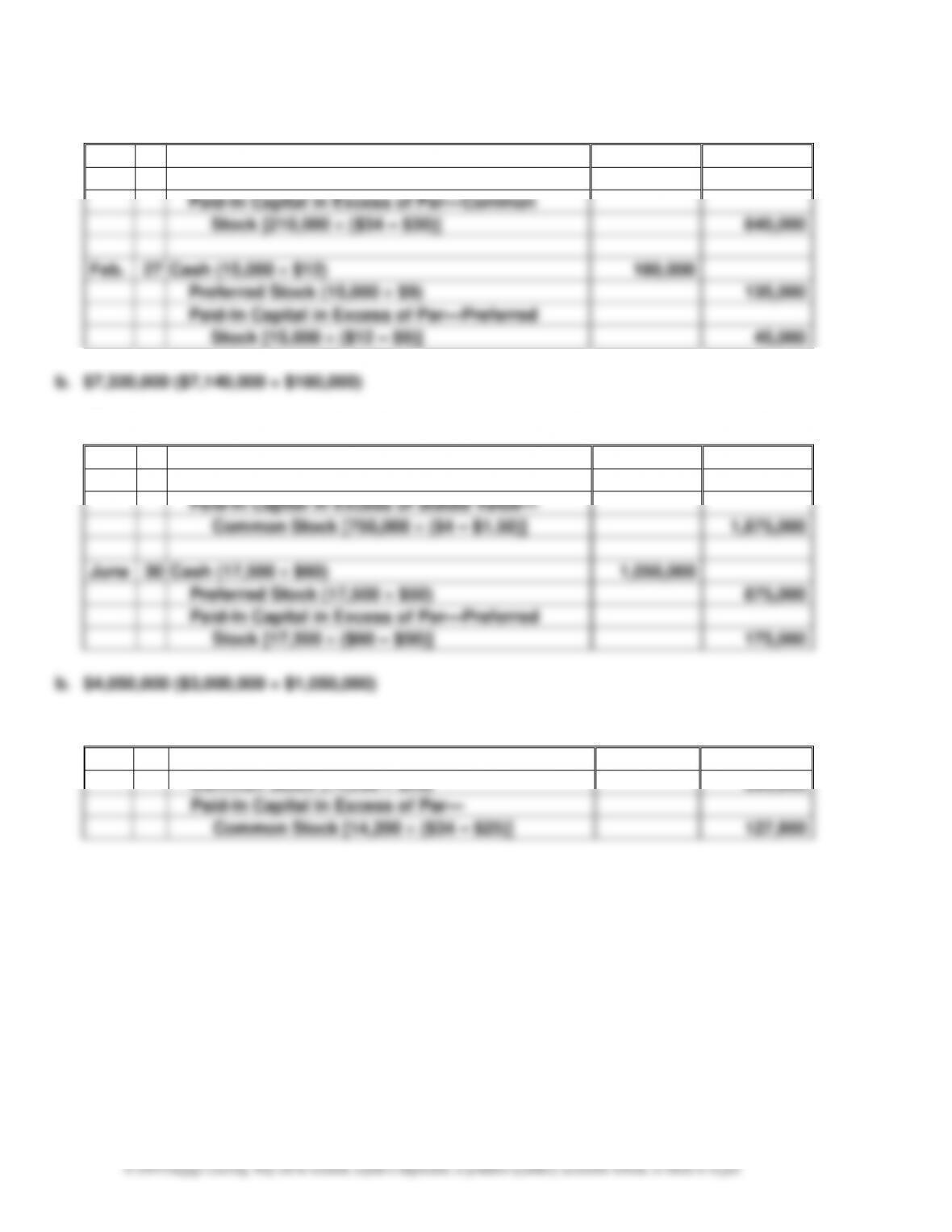

Ex. 12–3

a.

Jan.

22

Cash (210,000 $34)

7,140,000

Common Stock (210,000 $30)

6,300,000

Paid-In Capital in Excess of Par—Common

Stock [210,000 ($34 – $30)]

840,000

Feb.

27

Cash (15,000 $12)

180,000

Preferred Stock (15,000 $9)

135,000

Paid-In Capital in Excess of Par—Preferred

Stock [15,000 ($12 – $9)]

45,000

Ex. 12–4

a.

May

15

Cash (750,000 $4)

3,000,000

Common Stock (750,000 $1.50)

1,125,000

Paid-In Capital in Excess of Stated Value—

Common Stock [750,000 ($4 – $1.50)]

1,875,000

June

30

Cash (17,500 $60)

1,050,000

Preferred Stock (17,500 $50)

875,000

Paid-In Capital in Excess of Par—Preferred

Stock [17,500 ($60 – $50)]

175,000

b. $4,050,000 ($3,000,000 + $1,050,000)

Ex. 12–5

Nov.

23

Land (14,200 $34)

482,800

Common Stock (14,200 $25)

355,000

Paid-In Capital in Excess of Par—

Common Stock [14,200 ($34 – $25)]

127,800

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–7

Ex. 12–6

a.

Cash

100,000

Common Stock (100,000 $1)

100,000

b.

Organizational Expenses

3,000

Common Stock (3,000 $1)

3,000

Cash

45,000

Common Stock (45,000 $1)

45,000

c.

Land

60,000

Building

225,000

Interest Payable*

5,200

Mortgage Note Payable

180,000

Common Stock (99,800 $1)

99,800

* An acceptable alternative would be to credit Interest Expense.

Ex. 12–7

Oct.

1

Cash (120,000 $31.50)

3,780,000

Common Stock (120,000 $30.00)

3,600,000

Paid-In Capital in Excess of Par—

Common Stock [120,000 ($31.50 – $30.00)]

180,000

1

Buildings

2,380,000

Land

840,000

Preferred Stock (35,000 $80)

2,800,000

Paid-In Capital in Excess of Par—

Preferred Stock [35,000 ($92 – $80)]

420,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–8

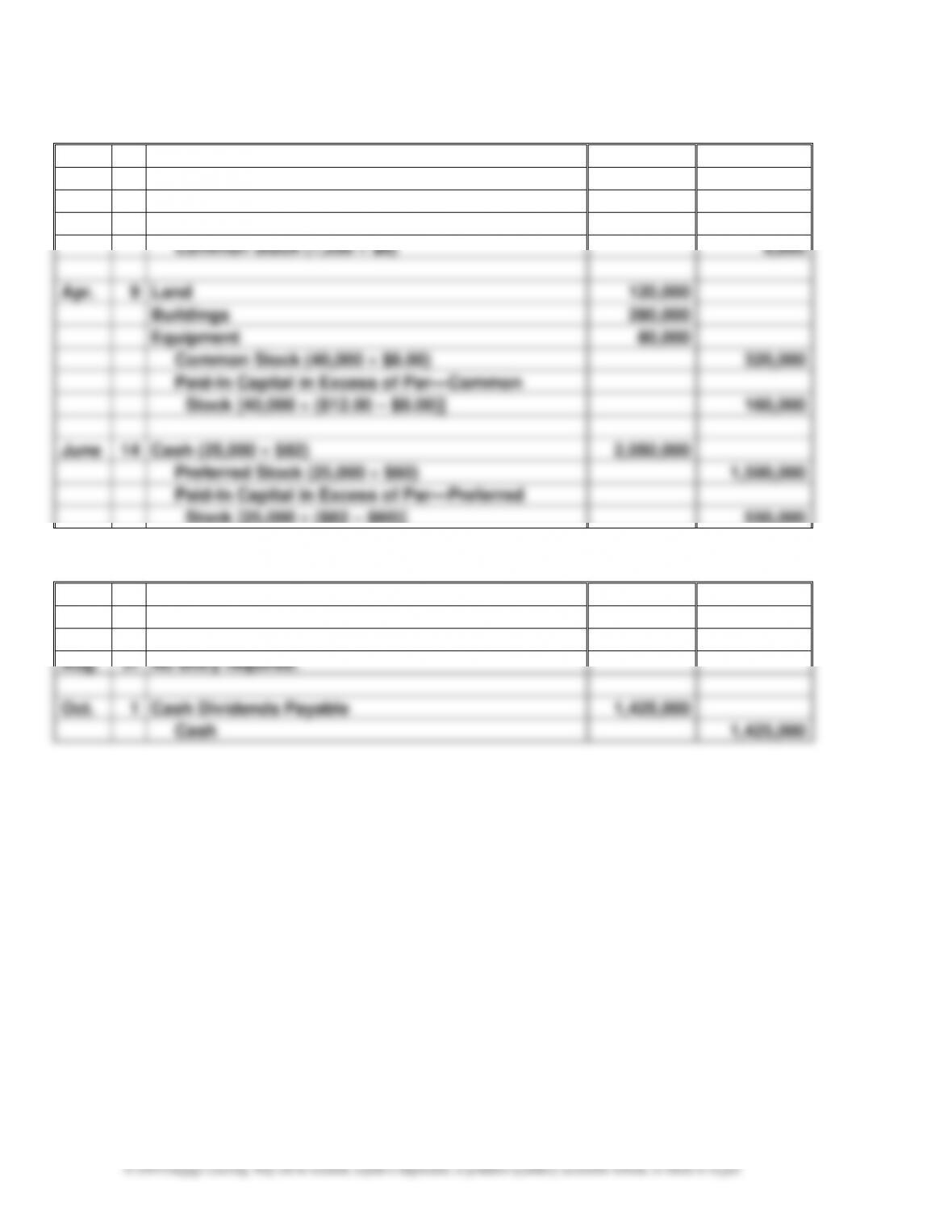

Ex. 12–8

Feb.

5

Cash

5,600,000

Common Stock (700,000 $8)

5,600,000

5

Organizational Expenses

9,600

Common Stock (1,200 $8)

9,600

Apr.

9

Land

120,000

Buildings

280,000

Equipment

80,000

Common Stock (40,000 $8.00)

320,000

Paid-In Capital in Excess of Par—Common

Stock [40,000 ($12.00 – $8.00)]

160,000

June

14

Cash (25,000 $82)

2,050,000

Preferred Stock (25,000 $60)

1,500,000

Paid-In Capital in Excess of Par—Preferred

Stock [25,000 ($82 – $60)]

550,000

Ex. 12–9

July

9

Cash Dividends

1,425,000

Cash Dividends Payable

1,425,000

Aug.

31

No entry required.

Oct.

1

Cash Dividends Payable

1,425,000

Cash

1,425,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–9

Ex. 12–10

a.

(1)

Stock Dividends [(2,200,000 5%) $18]

1,980,000

Stock Dividends Distributable (110,000 $15)

1,650,000

Paid-In Capital in Excess of Par—

Common Stock [110,000 ($18 – $15)]

330,000

(2)

Stock Dividends Distributable

1,650,000

Common Stock

1,650,000

b. (1) $42,000,000 ($33,000,000 + $9,000,000)

Ex. 12–11

Ex. 12–12

Assets

Liabilities

Stockholders’

Equity

a. Authorizing and issuing stock

certificates in a stock split

0

0

0

b. Declaring a stock dividend

0

0

0

c. Issuing stock certificates for the

stock dividend declared in (b)

0

0

0

d. Declaring a cash dividend

0

+

–

e. Paying the cash dividend

declared in (d)

–

–

0

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–10

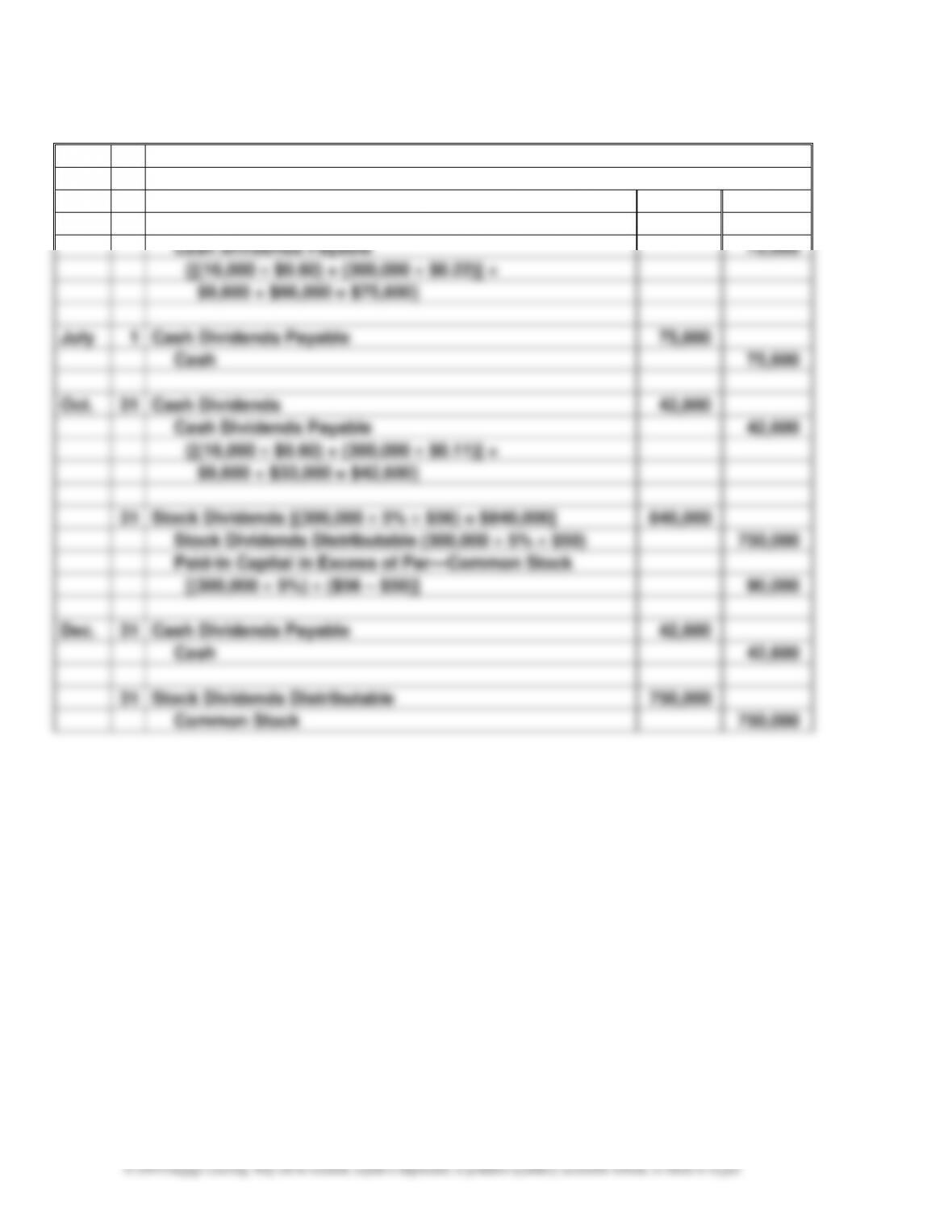

Ex. 12–13

Jan.

8

No entry required. The stockholders’ ledger would be revised to

record the increased number of shares held by each stockholder.

Apr.

30

Cash Dividends

75,600

Cash Dividends Payable

75,600

{[(16,000 $0.60) + (300,000 $0.22)] =

$9,600 + $66,000 = $75,600}

July

1

Cash Dividends Payable

75,600

Cash

75,600

Oct.

31

Cash Dividends

42,600

Cash Dividends Payable

42,600

{[(16,000 $0.60) + (300,000 $0.11)] =

$9,600 + $33,000 = $42,600}

31

Stock Dividends [(300,000 5% $56) = $840,000]

840,000

Stock Dividends Distributable (300,000 5% $50)

750,000

Paid-In Capital in Excess of Par—Common Stock

[(300,000 5%) ($56 – $50)]

90,000

Dec.

31

Cash Dividends Payable

42,600

Cash

42,600

31

Stock Dividends Distributable

750,000

Common Stock

750,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–11

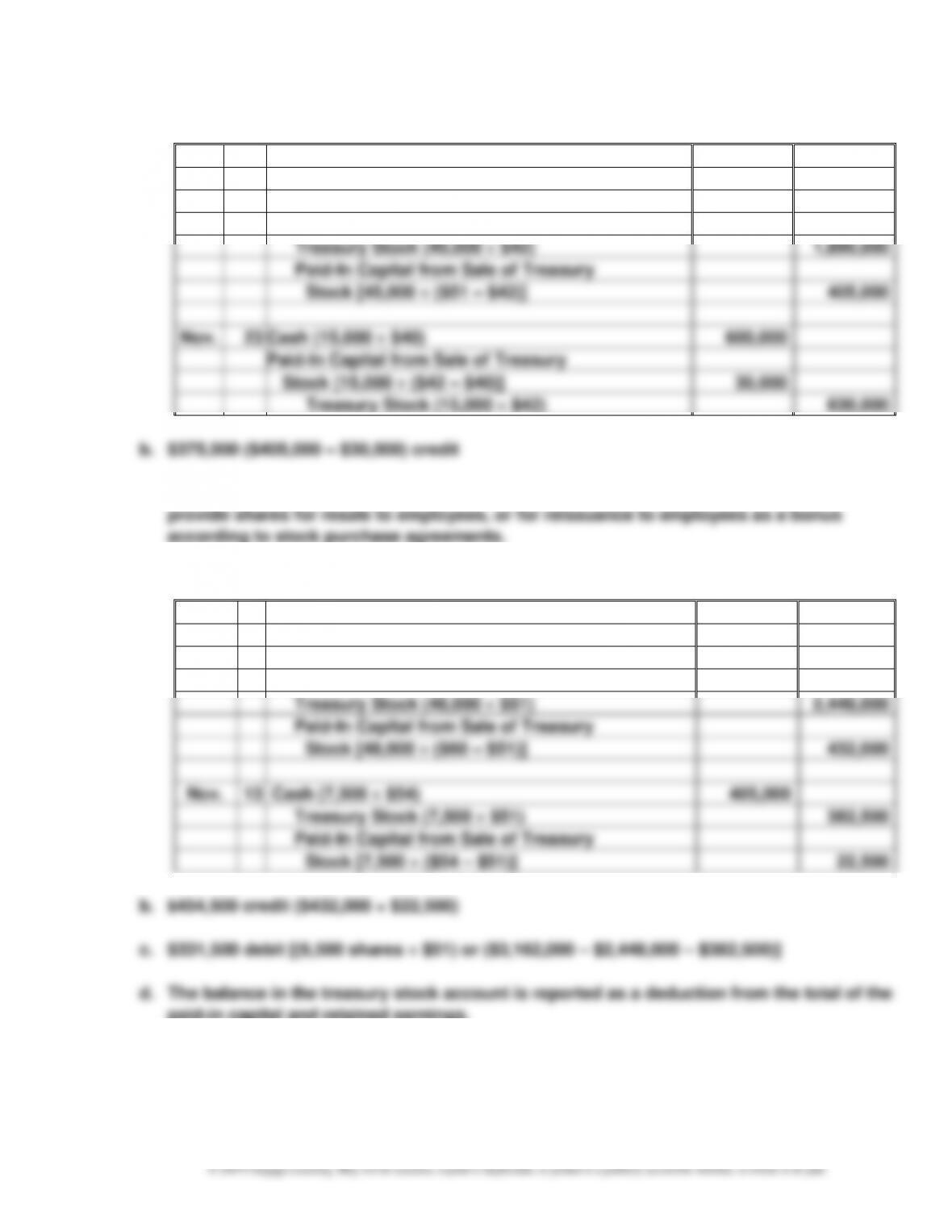

Ex. 12–14

a.

July

9

Treasury Stock (60,000 $42)

2,520,000

Cash

2,520,000

Sept.

22

Cash (45,000 $51)

2,295,000

Treasury Stock (45,000 $42)

1,890,000

Paid-In Capital from Sale of Treasury

Stock [45,000 ($51 – $42)]

405,000

Nov.

23

Cash (15,000 $40)

600,000

Paid-In Capital from Sale of Treasury

Stock [15,000 ($42 – $40)]

30,000

Treasury Stock (15,000 $42)

630,000

c. Mystic Lake may have purchased the stock to support the market price of the stock, to

according to stock purchase agreements.

Ex. 12–15

a.

Mar.

9

Treasury Stock (62,000 $51)

3,162,000

Cash

3,162,000

June

9

Cash (48,000 $60)

2,880,000

Treasury Stock (48,000 $51)

2,448,000

Paid-In Capital from Sale of Treasury

Stock [48,000 ($60 – $51)]

432,000

Nov.

13

Cash (7,500 $54)

405,000

Treasury Stock (7,500 $51)

382,500

Paid-In Capital from Sale of Treasury

Stock [7,500 ($54 – $51)]

22,500

paid-in capital and retained earnings.

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–12

Ex. 12–16

a.

May

14

Treasury Stock (23,500 $75)

1,762,500

Cash

1,762,500

Sept.

6

Cash (14,000 $81)

1,134,000

Treasury Stock (14,000 $75)

1,050,000

Paid-In Capital from Sale of Treasury

Stock [14,000 ($81 – $75)]

84,000

Nov.

30

Cash (9,500 $72)

684,000

Paid-In Capital from Sale of Treasury

Stock [9,500 ($75 – $72)]

28,500

Treasury Stock (9,500 $75)

712,500

d. Biscayne Bay Water Inc. may have purchased the stock to support the market price of the

stock, to provide shares for resale to employees, or for reissuance to employees as a

bonus according to stock purchase agreements.

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–13

Ex. 12–17

Stockholders’ Equity

Paid-in capital:

Preferred 2% stock, $120 par

(85,000 shares authorized,

70,000 shares issued)

$8,400,000

Excess of issue price over par

210,000

Paid-in capital, preferred stock

$8,610,000

Common stock, no par, $14 stated

value (375,000 shares authorized,

320,000 shares issued)

$4,480,000

Excess of issue price over par

480,000

Paid-in capital, common stock

4,960,000

From sale of treasury stock

45,000

Total paid-in capital

$13,615,000

Ex. 12–18

Stockholders’ Equity

Paid-in capital:

Common stock, $45 par

(80,000 shares authorized,

68,000 shares issued)

$3,060,000

Excess of issue price over par

272,000

Paid-in capital, common stock

$3,332,000

From sale of treasury stock

115,000

Total paid-in capital

$ 3,447,000

Retained earnings

20,553,000

Total

$24,000,000

Treasury stock

(9,000 shares at cost)

(324,000)

Total stockholders’ equity

$23,676,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–14

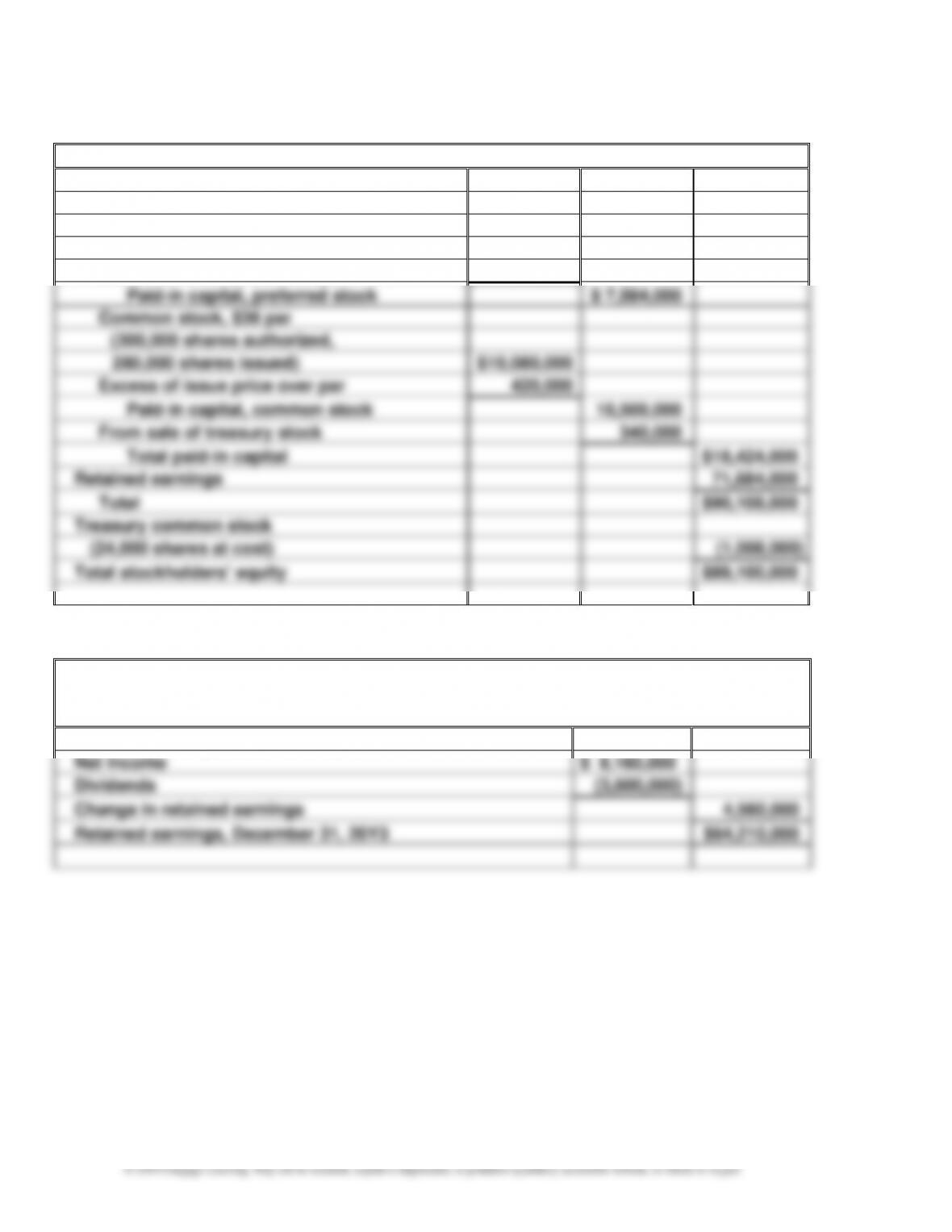

Ex. 12–19

Stockholders’ Equity

Paid-in capital:

Preferred 1% stock, $150 par

(50,000 shares authorized,

48,000 shares issued)

$ 7,200,000

Excess of issue price over par

384,000

Paid-in capital, preferred stock

$ 7,584,000

Common stock, $36 par

(300,000 shares authorized,

280,000 shares issued)

$10,080,000

Excess of issue price over par

420,000

Paid-in capital, common stock

10,500,000

From sale of treasury stock

340,000

Total paid-in capital

$18,424,000

Retained earnings

71,684,000

Total

$90,108,000

Treasury common stock

(24,000 shares at cost)

(1,008,000)

Total stockholders’ equity

$89,100,000

Ex. 12–20

Sumter Pumps Corporation

Retained Earnings Statement

For the Year Ended December 31, 20Y3

Retained earnings, January 1, 20Y3

$59,650,000

Net income

$ 8,160,000

Dividends

(3,600,000)

Change in retained earnings

4,560,000

Retained earnings, December 31, 20Y3

$64,210,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–15

Ex. 12–21

1. Retained earnings is not part of paid-in capital.

3. Dividends payable should be included as part of current liabilities and not as part of

stockholders’ equity.

5. The amount of shares of common stock issued of 825,000 times the par value per share of

6. Organizing costs should be expensed as Organizational Expenses when incurred and not

included as a part of stockholders’ equity.

One possible corrected “Stockholders’ Equity” section of the balance sheet is as follows:

Stockholders’ Equity

Paid-in capital:

Preferred 2% stock, $80 par (125,000

shares authorized and issued)

$10,000,000

Excess of issue price over par

500,000

Paid-in capital, preferred stock

$ 10,500,000

Common stock, $20 par (1,000,000 shares

authorized, 825,000 shares issued)

$16,500,000

Excess of issue price over par

1,155,000

Paid-in capital, common stock

17,655,000

Total paid-in capital

$ 28,155,000

Retained earnings*

96,400,000

Total

$124,555,000

Treasury stock (75,000 shares at cost)

(1,755,000)

Total stockholders’ equity

$122,800,000

* $96,700,000 – $300,000. Since the organizing costs should have been expensed, the

retained earnings should be $300,000 less.

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–16

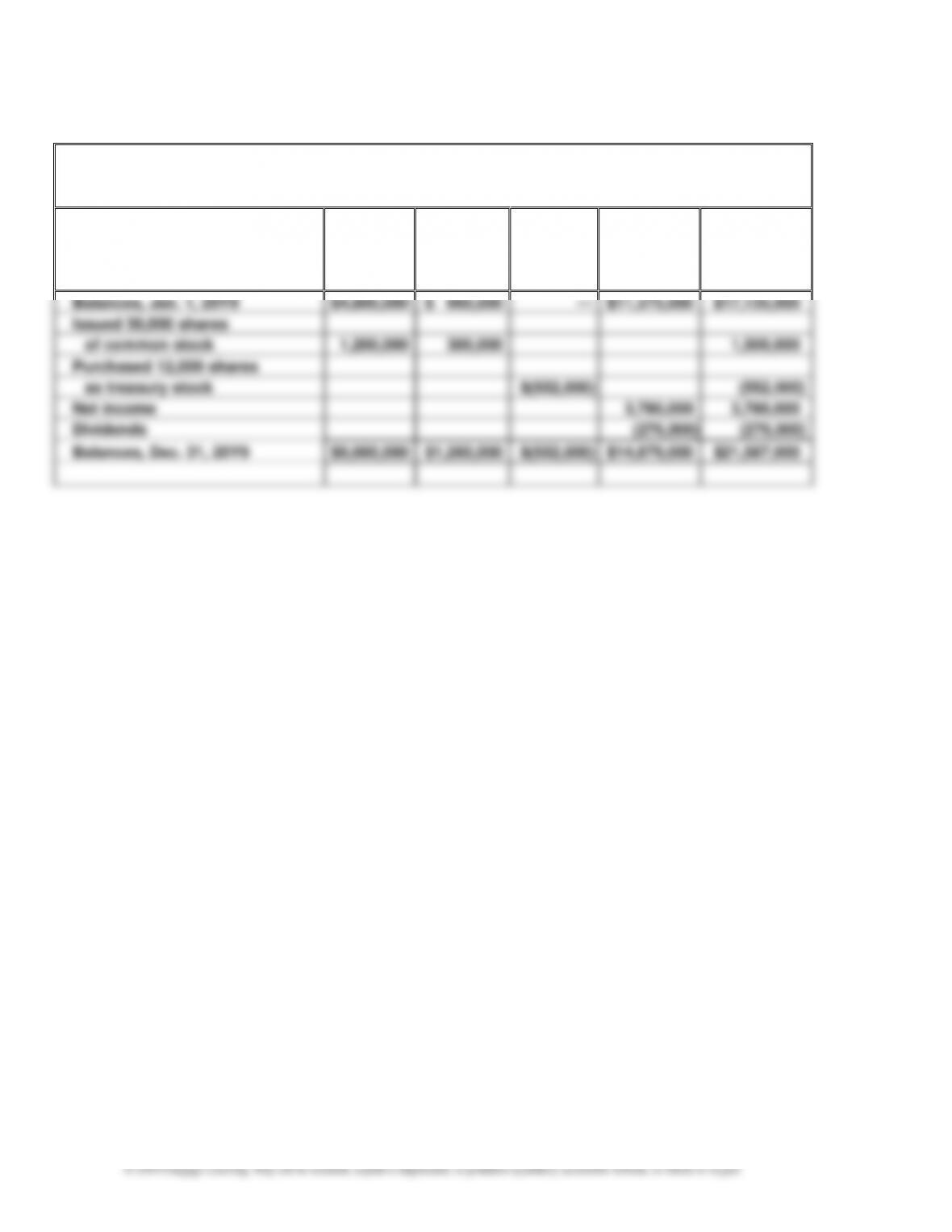

Ex. 12–22

I-Cards Inc.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y9

Common

Stock,

$40 par

Paid-In

Capital in

Excess of

Par

Treasury

Stock

Retained

Earnings

Total

Balances, Jan. 1, 20Y9

$4,800,000

$ 960,000

—

$11,375,000

$17,135,000

Issued 30,000 shares

of common stock

1,200,000

300,000

1,500,000

Purchased 12,000 shares

as treasury stock

$(552,000)

(552,000)

Net income

3,780,000

3,780,000

Dividends

(276,000)

(276,000)

Balances, Dec. 31, 20Y9

$6,000,000

$1,260,000

$(552,000)

$14,879,000

$21,587,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–17

PROBLEMS

Prob. 12–1A

1.

Preferred Dividends

Common Dividends

Year

Total

Dividends

Total

Per

Share

Total

Per

Share

20Y1 ……..

$ 80,000

$ 80,000

$0.32

$ 0

$0.00

20Y2 ……..

90,000

90,000

0.36

0

0.00

20Y3 ……..

150,000

130,000*

0.52

20,000

0.04

20Y4 ……..

150,000

100,000

0.40

50,000

0.10

20Y5 ……..

160,000

100,000

0.40

60,000

0.12

20Y6 ……..

180,000

100,000

0.40

80,000

0.16

$2.40

$0.42

Prob. 12–2A

May

11

Building

3,375,000

Land

1,500,000

Common Stock (125,000 $35)

4,375,000

Paid-In Capital in Excess of Par—

Common Stock [125,000 ($39* – $35)]

500,000

20

Cash (40,000 $52)

2,080,000

Preferred Stock (40,000 $50)

2,000,000

Paid-In Capital in Excess of Par—

Preferred Stock [40,000 ($52** – $50)]

80,000

31

Cash

4,000,000

Mortgage Note Payable

4,000,000

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–18

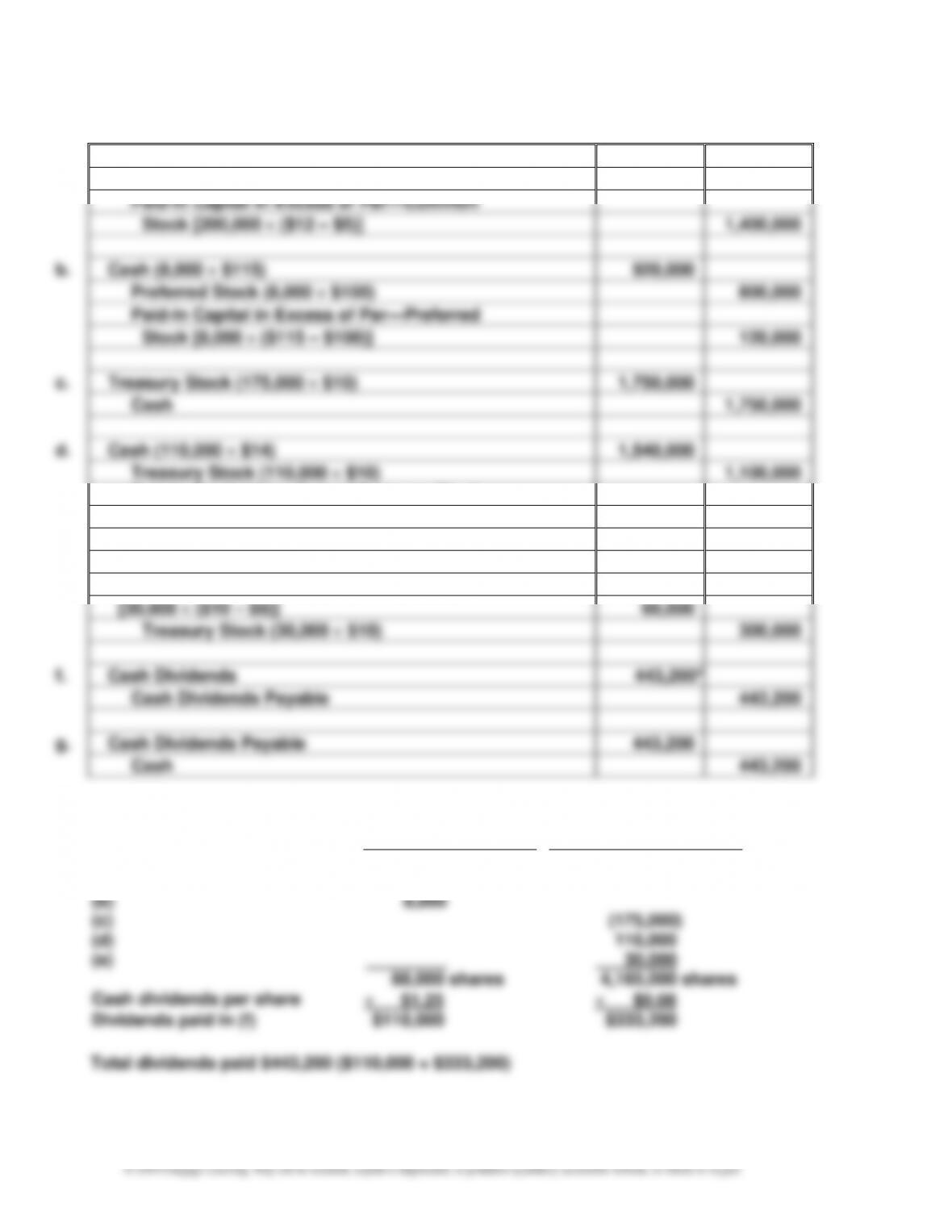

Prob. 12–3A

a.

Cash (200,000 $12)

2,400,000

Common Stock (200,000 $5)

1,000,000

Paid-In Capital in Excess of Par—Common

Stock [200,000 ($12 – $5)]

1,400,000

b.

Cash (8,000 $115)

920,000

Preferred Stock (8,000 $100)

800,000

Paid-In Capital in Excess of Par—Preferred

Stock [8,000 ($115 – $100)]

120,000

c.

Treasury Stock (175,000 $10)

1,750,000

Cash

1,750,000

d.

Cash (110,000 $14)

1,540,000

Treasury Stock (110,000 $10)

1,100,000

Paid-In Capital from Sale of Treasury Stock

[110,000 ($14 – $10)]

440,000

e.

Cash (30,000 $8)

240,000

Paid-In Capital from Sale of Treasury Stock

[30,000 ($10 – $8)]

60,000

Treasury Stock (30,000 $10)

300,000

f.

Cash Dividends

443,200*

Cash Dividends Payable

443,200

g.

Cash Dividends Payable

443,200

Cash

443,200

* Calculation of cash dividends:

Outstanding Shares of Stock

Beginning of year

Preferred Stock

80,000 shares

Common Stock

4,000,000 shares

(a)

200,000

(b)

8,000

(c)

(175,000)

(d)

110,000

(e)

0 0

30,000

88,000 shares

4,165,000 shares

Cash dividends per share

$1.25

$0.08

Dividends paid in (f)

$110,000

$333,200

Total dividends paid $443,200 ($110,000 + $333,200)

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

12–19

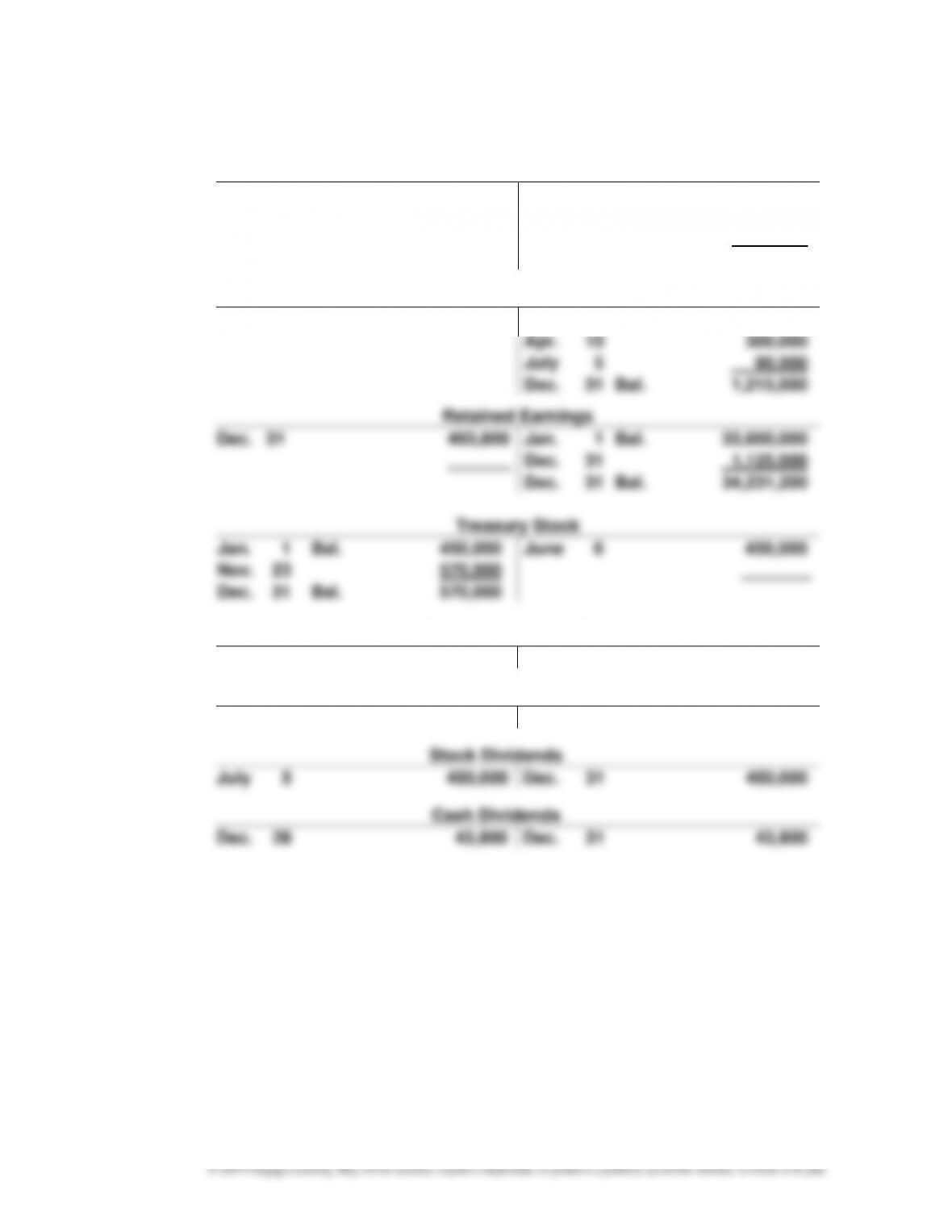

Prob. 12–4A

1. and 2.

Common Stock

Jan.

1

Bal.

7,500,000

Apr.

10

1,500,000

Aug.

15

360,000

Dec.

31

Bal.

9,360,000

Paid-In Capital in Excess of Stated Value—Common Stock

Jan.

1

Bal.

825,000

Apr.

10

300,000

July

5

90,000

Dec.

31

Bal.

1,215,000

Retained Earnings

Dec.

31

493,800

Jan.

1

Bal.

33,600,000

Dec.

31

1,125,000

Dec.

31

Bal.

34,231,200

Treasury Stock

Jan.

1

Bal.

450,000

June 6

450,000

Nov.

23

570,000

Dec.

31

Bal.

570,000

Paid-In Capital from Sale of Treasury Stock

June 6

200,000

Stock Dividends Distributable

Aug.

15

360,000

July 5

360,000

Stock Dividends

July

5

450,000

Dec. 31

450,000

Cash Dividends

Dec.

28

43,800

Dec. 31

43,800

CHAPTER 12 Corporations: Organization, Stock Transactions, and Dividends

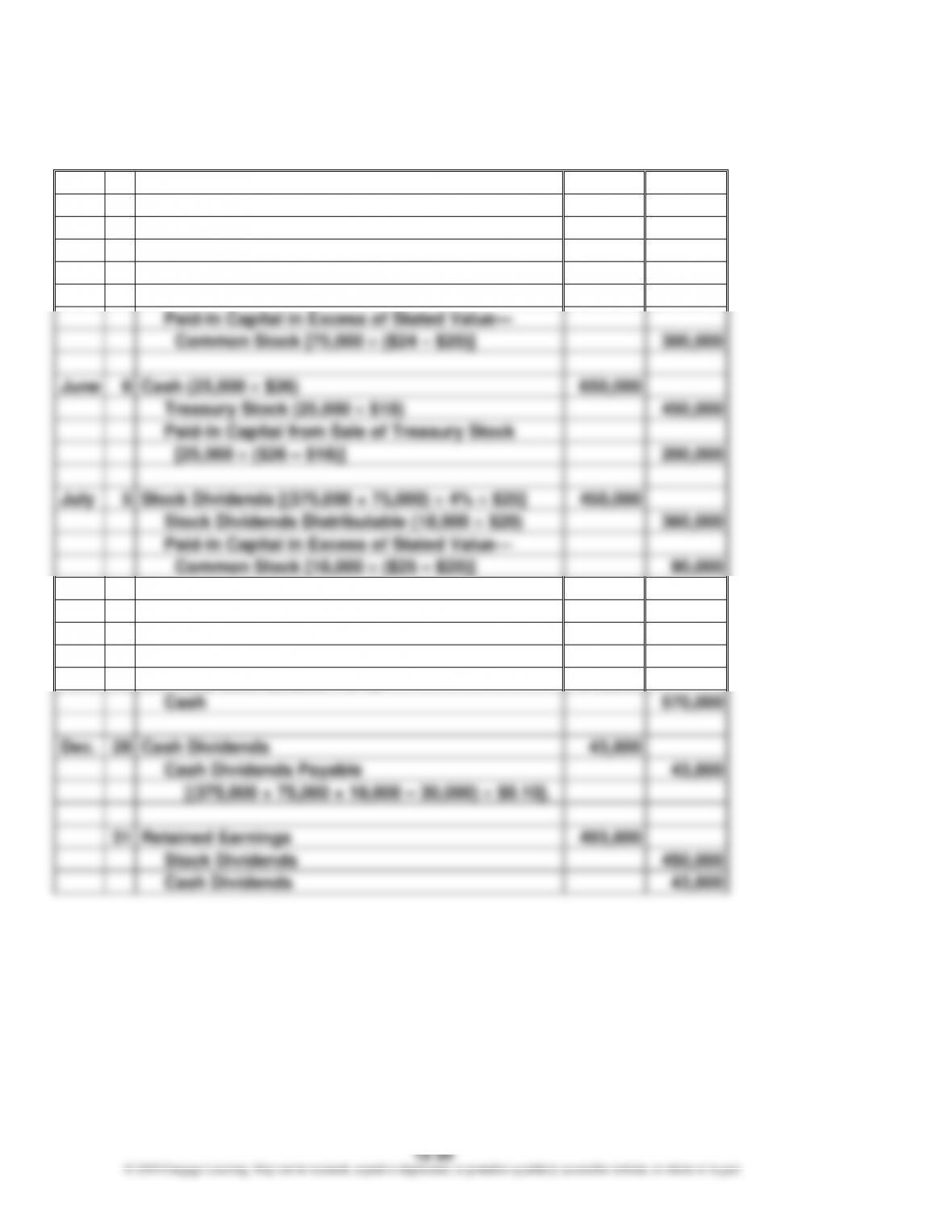

Prob. 12–4A (Continued)

2.

20Y6

Jan.

22

Cash Dividends Payable [(375,000 – 25,000) $0.08]

28,000

Cash

28,000

Apr.

10

Cash (75,000 shares $24)

1,800,000

Common Stock (75,000 $20)

1,500,000

Paid-In Capital in Excess of Stated Value—

Common Stock [75,000 ($24 – $20)]

300,000

June

6

Cash (25,000 $26)

650,000

Treasury Stock (25,000 $18)

450,000

Paid-In Capital from Sale of Treasury Stock

[25,000 ($26 – $18)]

200,000

July

5

Stock Dividends [(375,000 + 75,000) 4% $25]

450,000

Stock Dividends Distributable (18,000 $20)

360,000

Paid-In Capital in Excess of Stated Value—

Common Stock [18,000 ($25 – $20)]

90,000

Aug.

15

Stock Dividends Distributable

360,000

Common Stock

360,000

Nov.

23

Treasury Stock (30,000 $19)

570,000

Cash

570,000

Dec.

28

Cash Dividends

43,800

Cash Dividends Payable

43,800

[(375,000 + 75,000 + 18,000 – 30,000) $0.10].

31

Retained Earnings

493,800

Stock Dividends

450,000

Cash Dividends

43,800