Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 11 Liabilities: Bonds Payable

Appendix 1 and 2 Prob. 11–4A

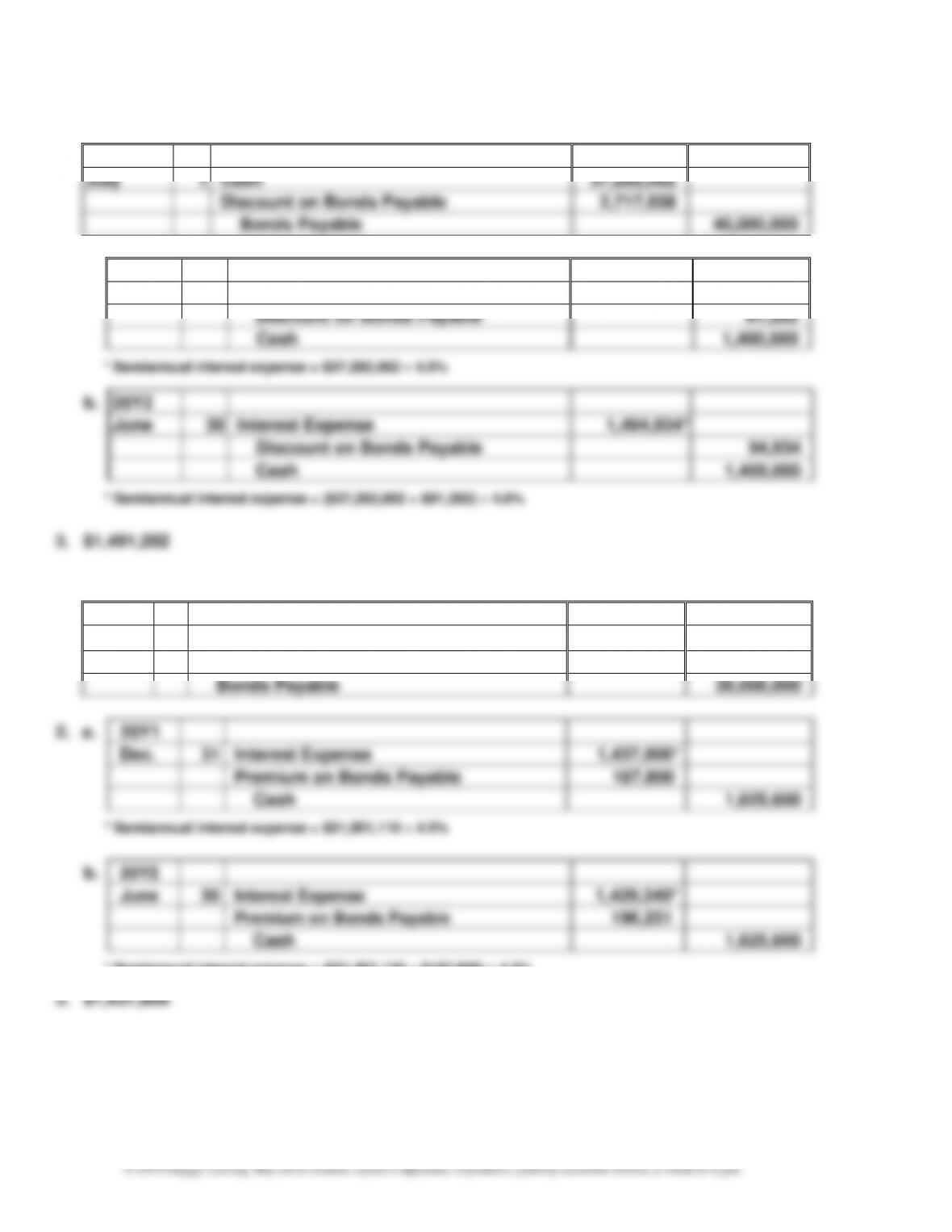

1.

20Y1

July

1

Cash

37,282,062

Discount on Bonds Payable

2,717,938

Bonds Payable

40,000,000

2. a.

20Y1

Dec.

31

Interest Expense

1,491,282*

Discount on Bonds Payable

91,282

Cash

1,400,000

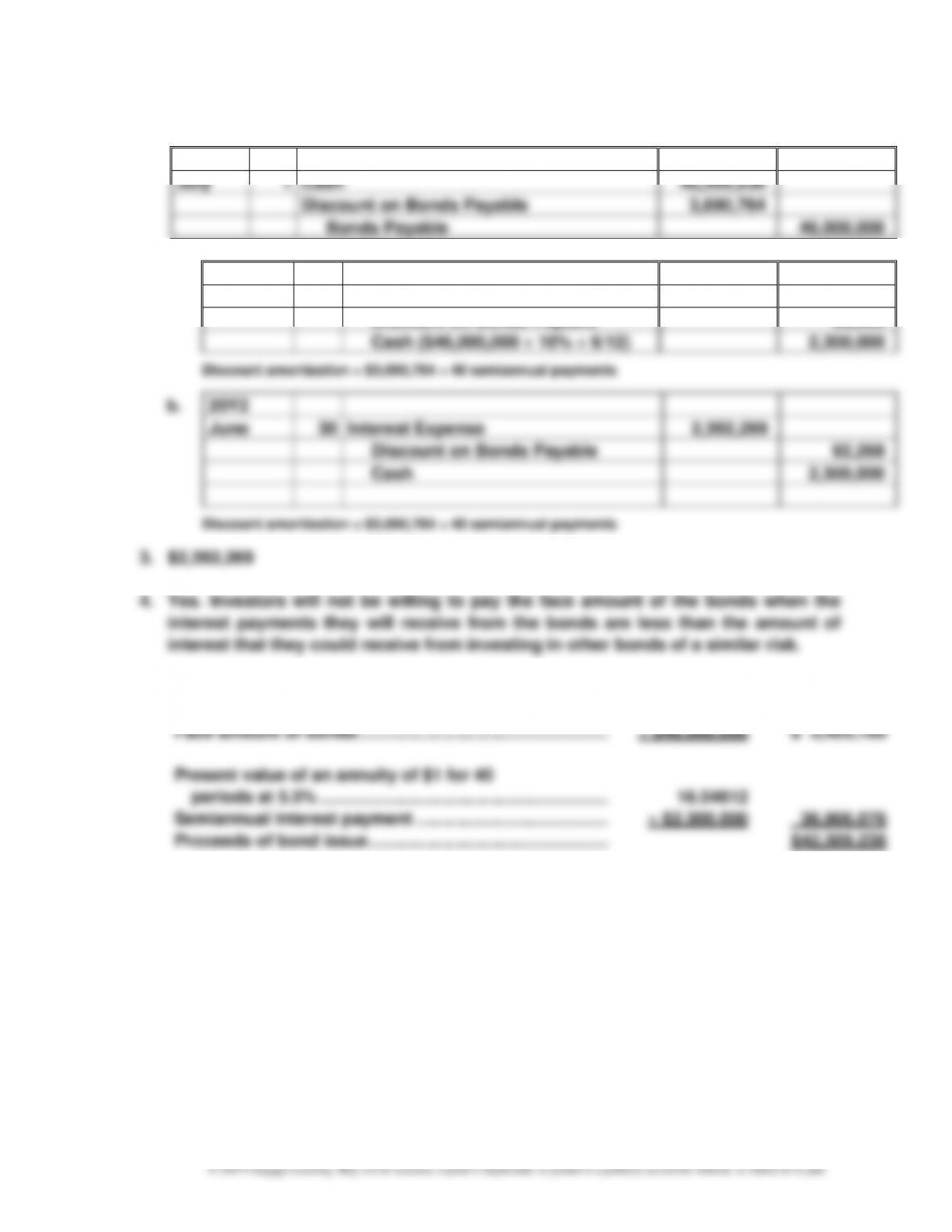

CHAPTER 11 Liabilities: Bonds Payable

Prob. 11–15B

1.

20Y1

July

1

Cash

42,309,236

Discount on Bonds Payable

3,690,764

Bonds Payable

46,000,000

2. a.

20Y1

Dec.

31

Interest Expense

2,392,269

Discount on Bonds Payable

92,269

Cash ($46,000,000 10% 6/12)

2,300,000

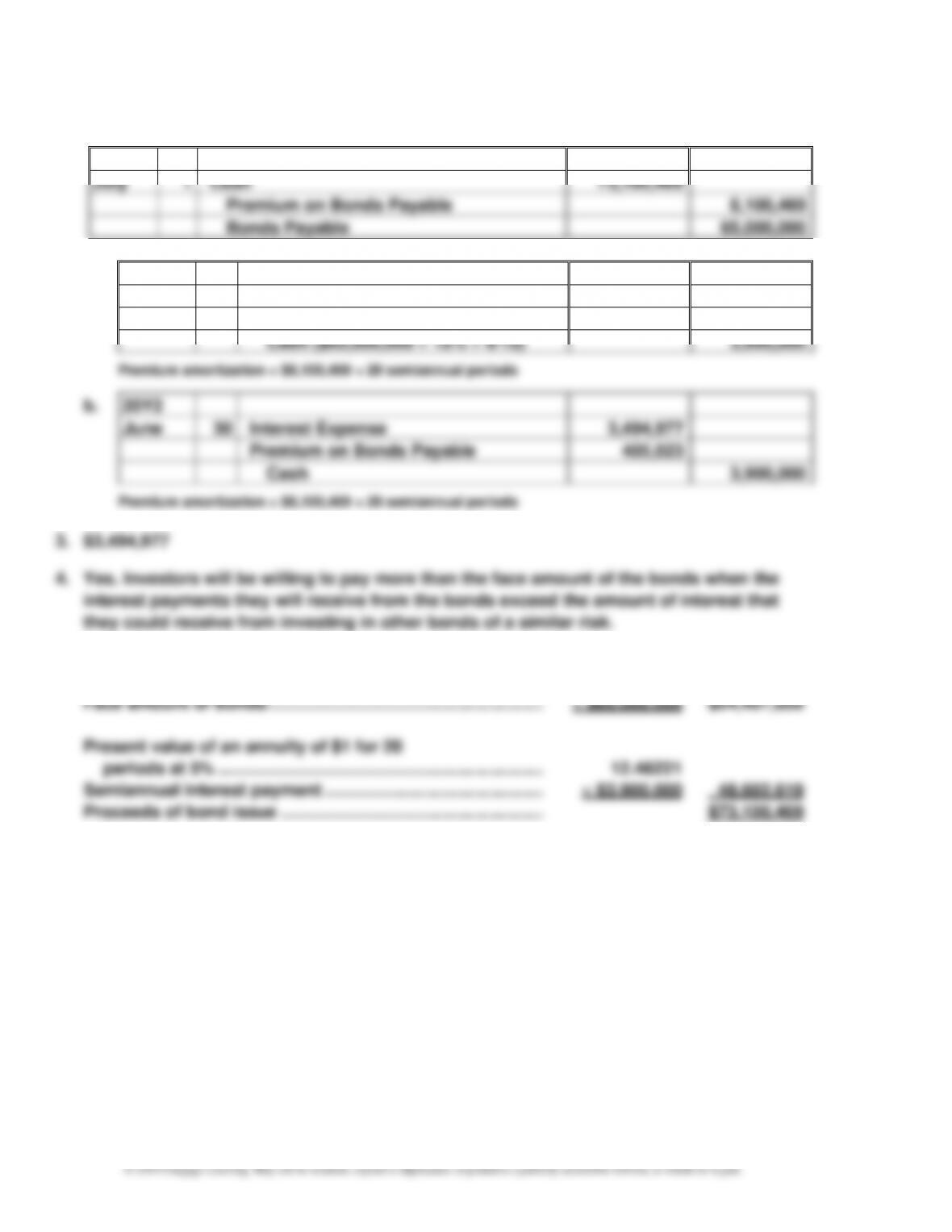

CHAPTER 11 Liabilities: Bonds Payable

Prob. 11–2B

1.

20Y1

July

1

Cash

73,100,469

Premium on Bonds Payable

8,100,469

Bonds Payable

65,000,000

2. a.

20Y1

Dec.

31

Interest Expense

3,494,977

Premium on Bonds Payable

405,023

Cash ($65,000,000 12% 6/12)

3,900,000

CHAPTER 11 Liabilities: Bonds Payable

11-17

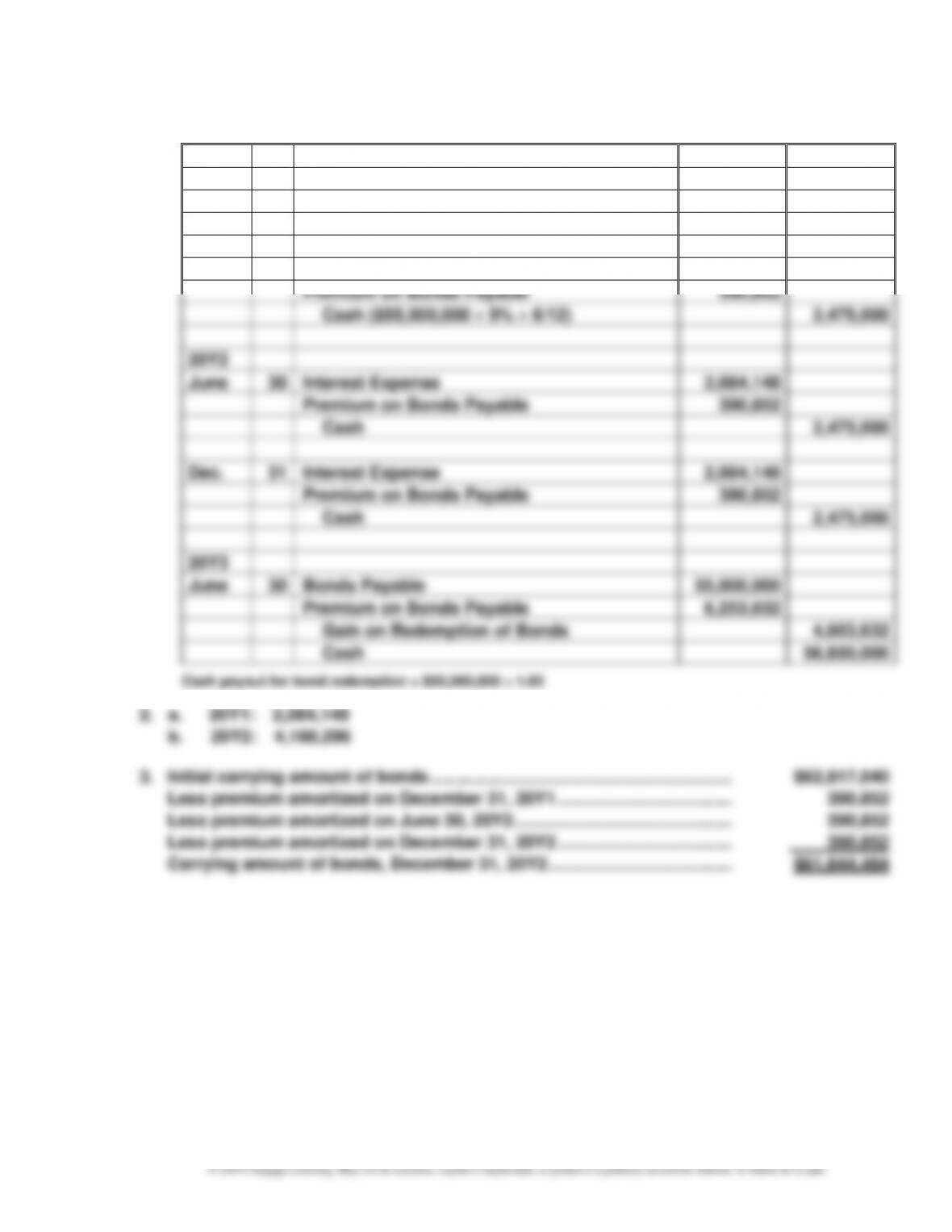

Prob. 11–3B

1.

20Y1

July

1

Cash

62,817,040

Premium on Bonds Payable

7,817,040

Bonds Payable

55,000,000

Dec.

31

Interest Expense

2,084,148

Premium on Bonds Payable

390,852

Cash ($55,000,000 9% 6/12)

2,475,000

20Y2

June

30

Interest Expense

2,084,148

Premium on Bonds Payable

390,852

Cash

2,475,000

Dec.

31

Interest Expense

2,084,148

Premium on Bonds Payable

390,852

Cash

2,475,000

20Y3

June

30

Bonds Payable

55,000,000

Premium on Bonds Payable

6,253,632

Gain on Redemption of Bonds

4,603,632

Cash

56,650,000

CHAPTER 11 Liabilities: Bonds Payable

Appendix 1 and 2 Prob. 11–4B

1.

20Y1

July

1

Cash

42,309,236

Discount on Bonds Payable

3,690,764

Bonds Payable

46,000,000

2. a.

20Y1

Dec.

31

Interest Expense

2,327,008

Premium on Bonds Payable

27,008

Cash

2,300,000

CHAPTER 11 Liabilities: Bonds Payable

MAKE A DECISION

MAD 11–1

a.

Expense Interest

ExpenseInterest Expense Tax Income Before Income

EarnedInterest Times +

=

9.0

$484

$484 $3,892

:2 Year

4.4

$459

$459 $1,568

:1 Year

:Amazon

=

+

=

+

11-20

MAD 11–2

a.

ExpenseInterest

ExpenseInterest Expense Tax Income Before Income

EarnedInterest Times +

=

12.2

$88

$88 $983

:Clorox =

+

24.1

$579

$579 $13,369

:Gamble & Procter =

+

b. Procter & Gamble has a times interest earned ratio of 24.1, which is almost twice as large

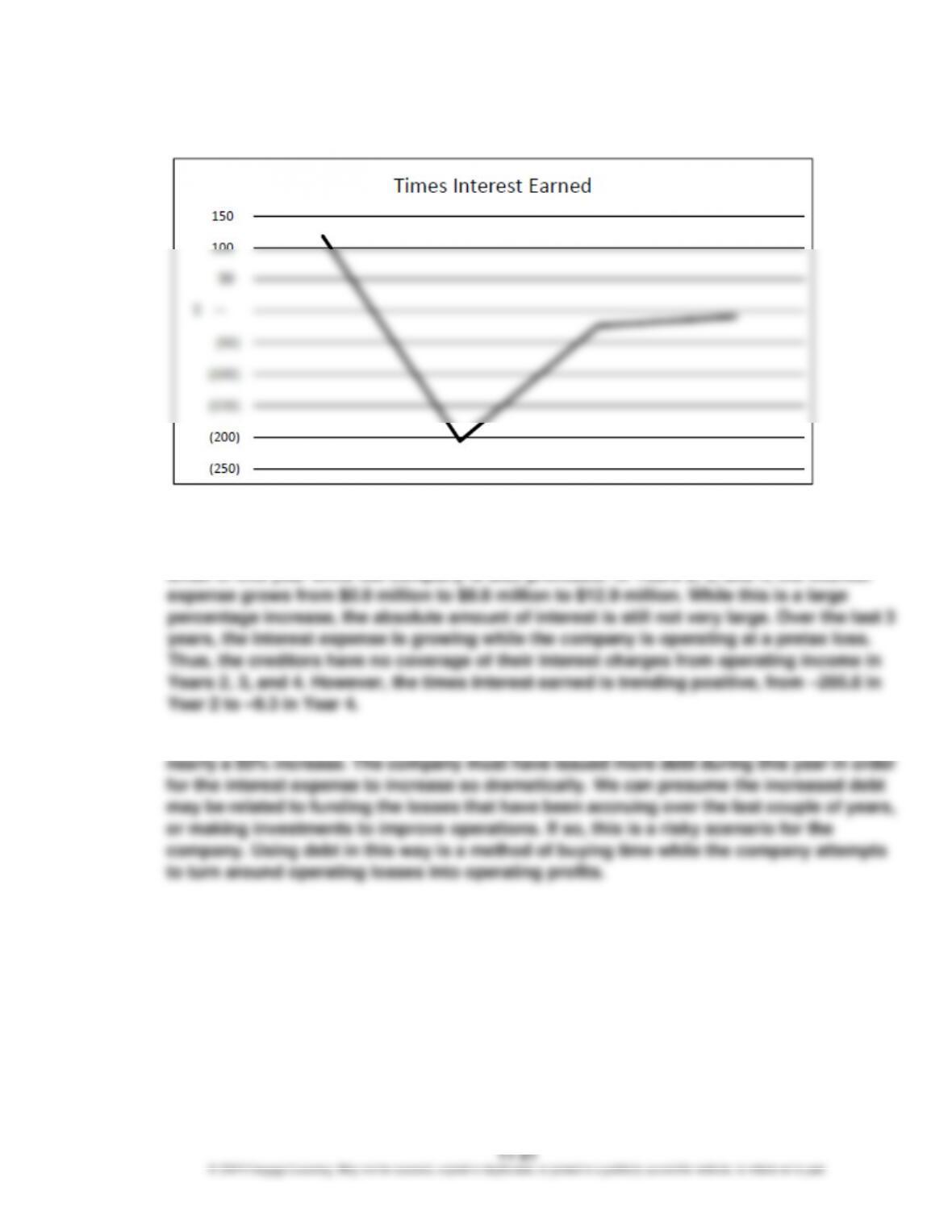

MAD 11–3

a.

ExpenseInterest

ExpenseInterest Expense Tax Income Before Income

EarnedInterest Times +

=

(9.3)

$12.9

$12.9 $(132.3)

:4 Year

(24.2)

$8.8

$8.8 $(221.9)

:3 Year

(205.8)

$0.9

$0.9 $(186.1)

:2 Year

119.0

$0.5

$0.5 $59.0

:1 Year

=

+

=

+

=

+

=

+

CHAPTER 11 Liabilities: Bonds Payable

MAD 11–3 (Concluded)

b.

c. While the times interest earned ratio is unfavorable, there is a positive trend. In Year 1, the

ratio is over 100 and indicates exceptional interest coverage. Interest expense is very

small in this year while the company is also profitable. In Years 2, 3, and 4, the interest

d. The interest expense increased from $8.8 million in Year 3 to $12.9 million in Year 4. This is

11-22

MAD 11–4

a.

ExpenseInterest

Expense Interest Expense Tax Income Before Income

EarnedInterest Times +

=

6.1

$234

$234 $1,184

:Marriott

3.1

$587

$587 $1,255

:Hilton

=

+

=

+

b. The times interest earned ratio is 3.1 for Hilton and 6.1 for Marriott. Using this ratio, we can

conclude that Marriott’s earnings provide its creditors greater protection of their interest

CHAPTER 11 Liabilities: Bonds Payable

TAKE IT FURTHER

TIF 11–1

CEG’s actions were technically legal; it did not violate any laws. However, this action could

damage the company’s reputation. If investors perceive that the company is not acting fairly

in its dealings with them, then the company may find it difficult to issue additional debt in the

future.

This case is based on a real-world situation, where GE Capital, a division of General Electric,

announced a follow-up long-term bond issue within days of an initial debt issue. The

actions.

TIF 11–2

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2016,

follows:

1. a. $2,010 million (balance sheet)

11-24

TIF 11–3

To: Liz Nolan

From: A+ Student

Re: Bond Redemption

I have reviewed the proposed redemption of the company’s 7% bonds and the subsequent

7% Bonds

5% Bonds

Interest

Savings

Face amount ........................................................

$1,000,000

$1,000,000

Contract rate of interest ...................................

7.0%

5.0%

Term ..................................................................

0.5

0.5

Semiannual interest payment .............................

$ 35,000

$ 25,000

$ 10,000

Number of interest periods remaining ...................................................................

10

Total interest savings .................................................................................................

$100,000

The interest savings of $100,000 are significantly larger than the $30,000 redemption

premium, resulting in a $70,000 savings to the company. However, the company must also

consider the impact of the time value of money on these savings. The $70,000 in interest

savings occurs over the next five years, with the company saving $10,000 on every

semiannual interest payment. Because these savings are in the future, they must be

discounted back to today to determine their present value. Using the market rate of interest of

5%, the present value of these savings is calculated as follows:

Semiannual interest savings .................................................................................... $10,000.00

CHAPTER 11 Liabilities: Bonds Payable

TIF 11–4

Receive $100,000,000 today:

Present value of $100,000,000 today = $100,000,000

Receive $25,000,000 today, plus $9,000,000 per year for 8 years:

Present value of $25,000,000 today ................................................................... $25,000,000