11–1

CHAPTER 11

LIABILITIES: BONDS PAYABLE

DISCUSSION QUESTIONS

1. (1) To pay the face (maturity) amount of the bonds at a specified date. (2) To pay periodic interest at a

specified percentage of the face amount.

3. Less than face amount. Because comparable bonds provide a market interest rate (12%) that is greater than

4. a. Greater than $26,000,000

6. a. Premium

(1) interest payments made periodically over the life of the bond and (2) the face amount that must be repaid

at maturity. The periodic payments consist entirely of interest, and the final payment at maturity consists

9. a. As a current liability on the balance sheet.

b. As a long-term liability on the balance sheet.

CHAPTER 11 Liabilities: Bonds Payable

BASIC EXERCISES

BE 11–1

a.

Cash

3,000,000

Bonds Payable

3,000,000

b.

Interest Expense

120,000

Cash

120,000

c.

Bonds Payable

3,000,000

Cash

3,000,000

BE 11–2

Cash

3,350,000

Discount on Bonds Payable

150,000

Bonds Payable

3,500,000

BE 11–3

Interest Expense

120,000

Discount on Bonds Payable

15,000

Cash

105,000

Discount on bonds payable = $150,000 ÷ 10 semiannual payments

BE 11–4

Cash

5,400,000

Premium on Bonds Payable

400,000

Bonds Payable

5,000,000

BE 11–5

Interest Expense

135,000

Premium on Bonds Payable

40,000

Cash

175,000

Premium on bonds payable = $400,000 ÷ 10 semiannual payments

BE 11–6

Bonds Payable

800,000

Premium on Bonds Payable

57,000

Gain on Redemption of Bonds

72,000

Cash

785,000

11–3

BE 11–7

a.

ExpenseInterest

ExpenseInterest Expense Tax Income Before Income

EarnedInterest Times +

=

12.0

$400,000

$400,000 $4,400,000

:20Y8 =

+

13.6

$440,000

$440,000 $5,544,000

:20Y9 =

+

b. The times interest earned ratio has increased from 12.0 in 20Y8 to 13.6 in 20Y9. The

CHAPTER 11 Liabilities: Bonds Payable

EXERCISES

Ex. 11–1

The bonds were selling at a premium. This is indicated by the selling price of 103.2, which is

Ex. 11–2

May

1

Cash

800,000

Bonds Payable

800,000

Nov.

1

Interest Expense ($800,000 6% 6/12)

24,000

Cash

24,000

Dec.

31

Interest Expense ($800,000 6% 2/12)

8,000

Interest Payable

8,000

Ex. 11–3

a. 1.

Cash

9,594,415

Discount on Bonds Payable

405,585

Bonds Payable

10,000,000

2.

Interest Expense

390,559

Discount on Bonds Payable

40,559

Cash

350,000

3.

Interest Expense

390,559

Discount on Bonds Payable

40,559

Cash

350,000

CHAPTER 11 Liabilities: Bonds Payable

Ex.11–3 (Concluded)

b. Annual interest paid ($10,000,000 7%) ………………………………………. $700,000

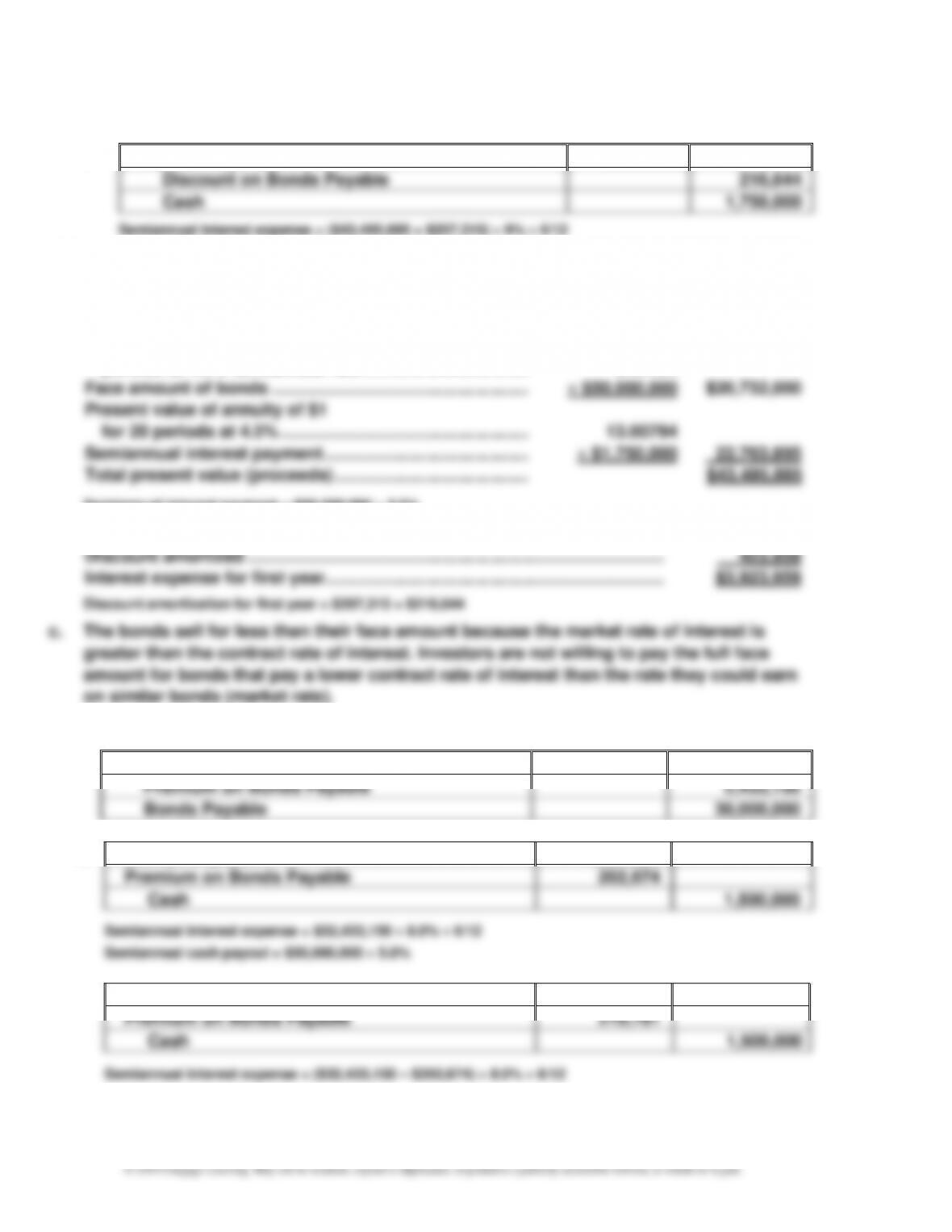

Ex. 11–4

a.

20Y1

Apr.

1

Cash

20,811,010

Premium on Bonds Payable

811,010

Bonds Payable

20,000,000

Oct.

1

Interest Expense

818,899

Premium on Bonds Payable

Cash

900,000

CHAPTER 11 Liabilities: Bonds Payable

11–6

Ex. 11–6

20Y5

May

1

Cash

22,000,000

Bonds Payable

22,000,000

Nov.

1

Interest Expense ($22,000,000 4% 6/12)

440,000

Cash

440,000

20Y9

Nov.

1

Bonds Payable

22,000,000

Gain on Redemption of Bonds

660,000

Cash

21,340,000

Ex. 11–7

1. The significant loss on redemption of the Simmons Industries bonds should be reported

Appendix 1 Ex. 11–8

Appendix 1 Ex. 11–9

a. First Year:

$200,000 0.93458 =

$186,916

Second Year:

$200,000 0.87344 =

174,688

Third Year:

$200,000 0.81630 =

163,260

Fourth Year:

$200,000 0.76290 =

52,580

Total present value

$677,444

b. $200,000 3.38721 = $677,442*

*$2 difference between (a) and (b) is due to rounding.

c. Cash on hand today can be invested to earn income. If each of the $200,000 of cash

receipts is invested at 7%, it will be worth $800,000 at the end of four years.

CHAPTER 11 Liabilities: Bonds Payable

11–7

Appendix 1 Ex. 11–10

Appendix 1 Ex. 11–11

No. The present value of your winnings using an interest rate of 12% is $31,047,750

higher interest rate.

Appendix 1 Ex. 11–12

Present value of $1 for 10 semiannual

periods at 4.5% semiannual rate………………………

0.64393

Face amount of bonds ……………………………………….

$25,000,000

$16,098,250

Present value of an annuity of $1

for 10 periods at 4.5% ……………………………………..

7.91272

Semiannual interest payment ……………………………..

$875,000

6,923,630

Total present value (proceeds) …………………………...

$23,021,880

Semiannual interest payment = $25,000,000 7% ÷ 2

Appendix 1 Ex. 11–13

Present value of $1 for 10 semiannual

periods at 4.5% semiannual rate………………………

0.64393

Face amount of bonds ……………………………………….

$42,000,000

$27,045,060

Present value of an annuity of $1

for 10 periods at 4.5% ……………………………………..

7.91272

Semiannual interest payment ……………………………..

$2,310,000

18,278,383

Total present value (proceeds) …………………………..

$45,323,443

Semiannual interest payment = $42,000,000 5.5%

Appendix 2 Ex. 11–14

a. 1.

Cash

43,495,895

Discount on Bonds Payable

6,504,105

Bonds Payable

50,000,000

2.

Interest Expense

1,957,315

Discount on Bonds Payable

207,315

Cash

1,750,000

Semiannual interest expense = $43,495,895 9% 6/12

Semiannual cash payout = $50,000,000 3.5%

CHAPTER 11 Liabilities: Bonds Payable

11–8

Appendix 2 Ex. 11–14 (Concluded)

3.

Interest Expense

1,966,644

Discount on Bonds Payable

216,644

Cash

1,750,000

Semiannual interest expense = ($43,495,895 + $207,315) 9% 6/12

Note: The following data in support of the proceeds of the bond issue stated in the

exercise are presented for the instructor’s information. Students are not required to make

the computations.

Present value of $1 for 20 semiannual

periods at 4.5% semiannual rate …………………………….

0.41464

Face amount of bonds ……………………………………………..

$50,000,000

$20,732,000

Present value of annuity of $1

for 20 periods at 4.5% ……………………………………………

13.00794

Semiannual interest payment ……………………………………

$1,750,000

22,763,895

Total present value (proceeds) ………………………………….

$43,495,895

Semiannual interest payment = $50,000,000 3.5%

b.

Annual interest paid ………………………………………………………………………….

$3,500,000

Discount amortized …………………………………………………………………………..

423,959

Interest expense for first year…………………………………………………………….

$3,923,959

Appendix 2 Ex. 11–15

a. 1.

Cash

32,433,150

Premium on Bonds Payable

2,433,150

Bonds Payable

30,000,000

2.

Interest Expense

1,297,326

Premium on Bonds Payable

202,674

Cash

1,500,000

Semiannual interest expense = $32,433,150 8.0% 6/12

Semiannual cash payout = $30,000,000 5.0%

3.

Interest Expense

1,289,219

Premium on Bonds Payable

210,781

Cash

1,500,000

Semiannual interest expense = ($32,433,150 – $202,674) 8.0% 6/12

CHAPTER 11 Liabilities: Bonds Payable

11–9

Appendix 2 Ex. 11–15 (Concluded)

b. Annual interest paid ($1,500,000 + $1,500,000) …………………………………. $3,000,000

Appendix 1 and 2 Ex. 11–16

a.

Present value of $1 for 10 semiannual

periods at 5% semiannual rate ………………………………

0.61391

Face amount of bonds ………………………………………………

$35,000,000

$21,486,850

Present value of an annuity of $1 for 10

periods at 5% ……………………………………………………….

7.72173

Semiannual interest payment …………………………………….

$2,100,000

16,215,633

Proceeds of bond sale ………………………………………………

$37,702,483

b. First semiannual interest payment ……………………………………………………. $ 2,100,000

Less 5% of carrying amount of $37,702,483 ………………………………………. (1,885,124)

Premium amortized …………………………………………………………………………. $ 214,876

c. Second semiannual interest payment ……………………………………………….. $ 2,100,000

CHAPTER 11 Liabilities: Bonds Payable

11–10

Appendix 1 and 2 Ex. 11–17

a.

Present value of $1 for 10 semiannual

periods at 6.0% semiannual rate ……………………………..

0.55839

Face amount of bonds ………………………………………………..

$80,000,000

$44,671,200

Present value of an annuity of $1 for 10

periods at 6.0% ………………………………………………………

7.36009

Semiannual interest payment …………………………………….

$3,600,000

26,496,324

Proceeds of bond sale ………………………………………………..

$71,167,524

First semiannual interest payment = $80,000,000 4.5%

b. 6.0% of carrying amount of $71,167,524 ……………………………………………… $ 4,270,051

c. 6.0% of carrying amount of $71,837,575 ……………………………………………… $ 4,310,255

CHAPTER 11 Liabilities: Bonds Payable

PROBLEMS

Prob. 11–1A

1.

20Y1

July

1

Cash

43,768,920

Discount on Bonds Payable

6,231,080

Bonds Payable

50,000,000

2. a.

20Y1

Dec.

31

Interest Expense

2,311,554

Discount on Bonds Payable

311,554

Cash

2,000,000

20Y2

Interest Expense

2,311,554

Discount on Bonds Payable

311,554

Cash

2,000,000

CHAPTER 11 Liabilities: Bonds Payable

11–12

Prob. 11–2A

1.

20Y1

July

1

Cash

31,951,110

Premium on Bonds Payable

1,951,110

Bonds Payable

30,000,000

2. a.

20Y1

Dec.

31

Interest Expense

1,402,444

Premium on Bonds Payable

97,556

Cash ($30,000,000 10% 6/12)

1,500,000

Premium amortization = $1,951,110 ÷ 20 seminannual payments (rounded)

b.

20Y2

June

30

Interest Expense

1,402,444

Premium on Bonds Payable

97,556

Cash

1,500,000

Premium amortization = $1,951,110 ÷ 20 semiannual payments (rounded)

3. $1,402,444

4. Yes. Investors will be willing to pay more than the face amount of the bonds when the

5.

Present value of $1 for 20 semiannual

periods at 4.5% semiannual rate ……………………………..

0.41464

Face amount of bonds ………………………………………………

$30,000,000

$12,439,200

Present value of annuity of $1

for 20 periods at 4.5% …………………………………………….

13.00794

Semiannual interest payment …………………………………….

$1,500,000

19,511,910

Proceeds of bond issue …………………………………………….

$31,951,110

CHAPTER 11 Liabilities: Bonds Payable

11–13

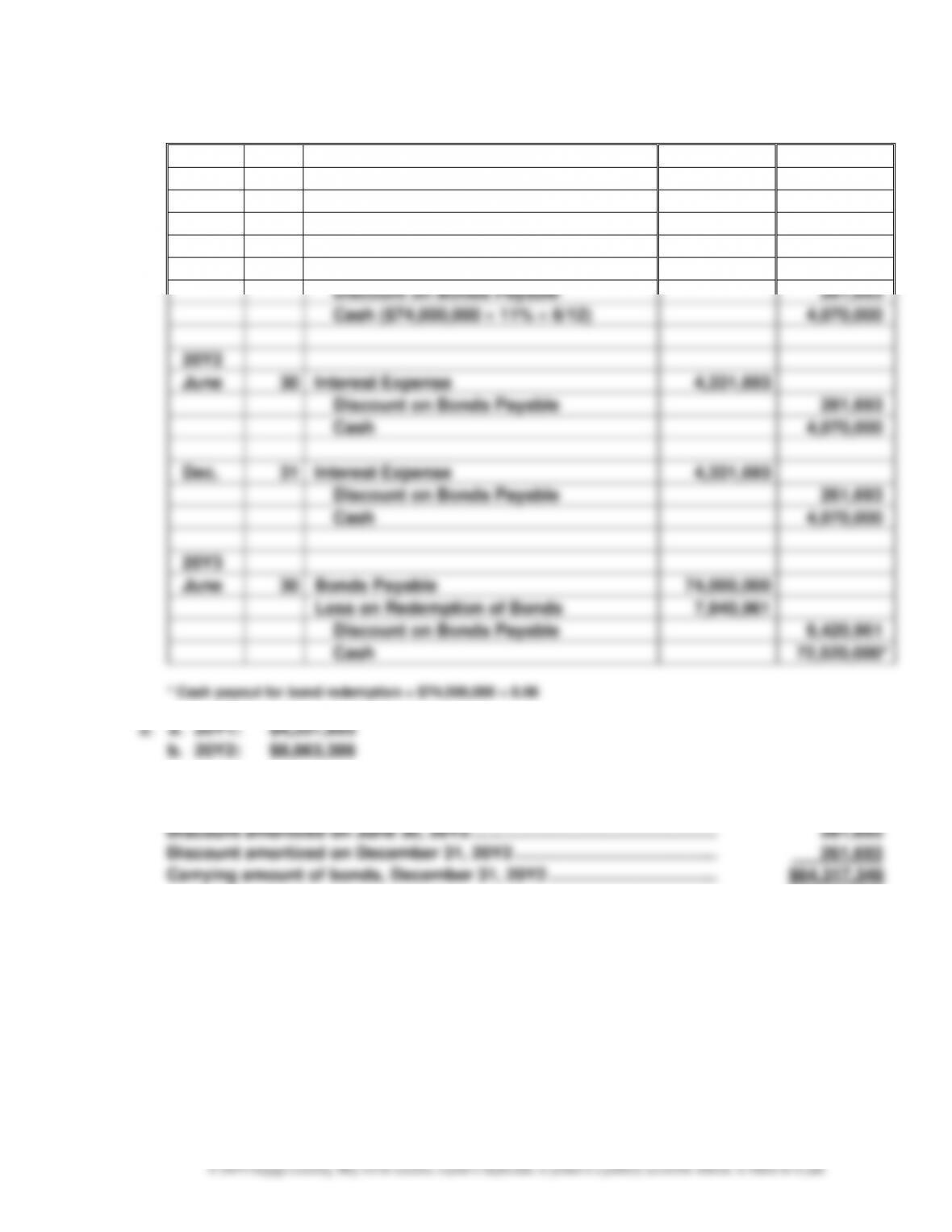

Prob. 11–3A

1.

20Y1

July

1

Cash

63,532,267

Discount on Bonds Payable

10,467,733

Bonds Payable

74,000,000

Dec.

31

Interest Expense

4,331,693

Discount on Bonds Payable

261,693

Cash ($74,000,000 11% 6/12)

4,070,000

20Y2

June

30

Interest Expense

4,331,693

Discount on Bonds Payable

261,693

Cash

4,070,000

Dec.

31

Interest Expense

4,331,693

Discount on Bonds Payable

261,693

Cash

4,070,000

20Y3

June

30

Bonds Payable

74,000,000

Loss on Redemption of Bonds

7,940,961

Discount on Bonds Payable

9,420,961

Cash

72,520,000*

* Cash payout for bond redemption = $74,000,000 0.98

2. a. 20Y1: $4,331,693

b. 20Y2: $8,663,386

3. Initial carrying amount of bonds ………………………………………………….. $63,532,267

Discount amortized on December 31, 20Y1 …………………………………… 261,693