CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–33

Comp. Prob. 3 (Continued)

2.

Kornett Company

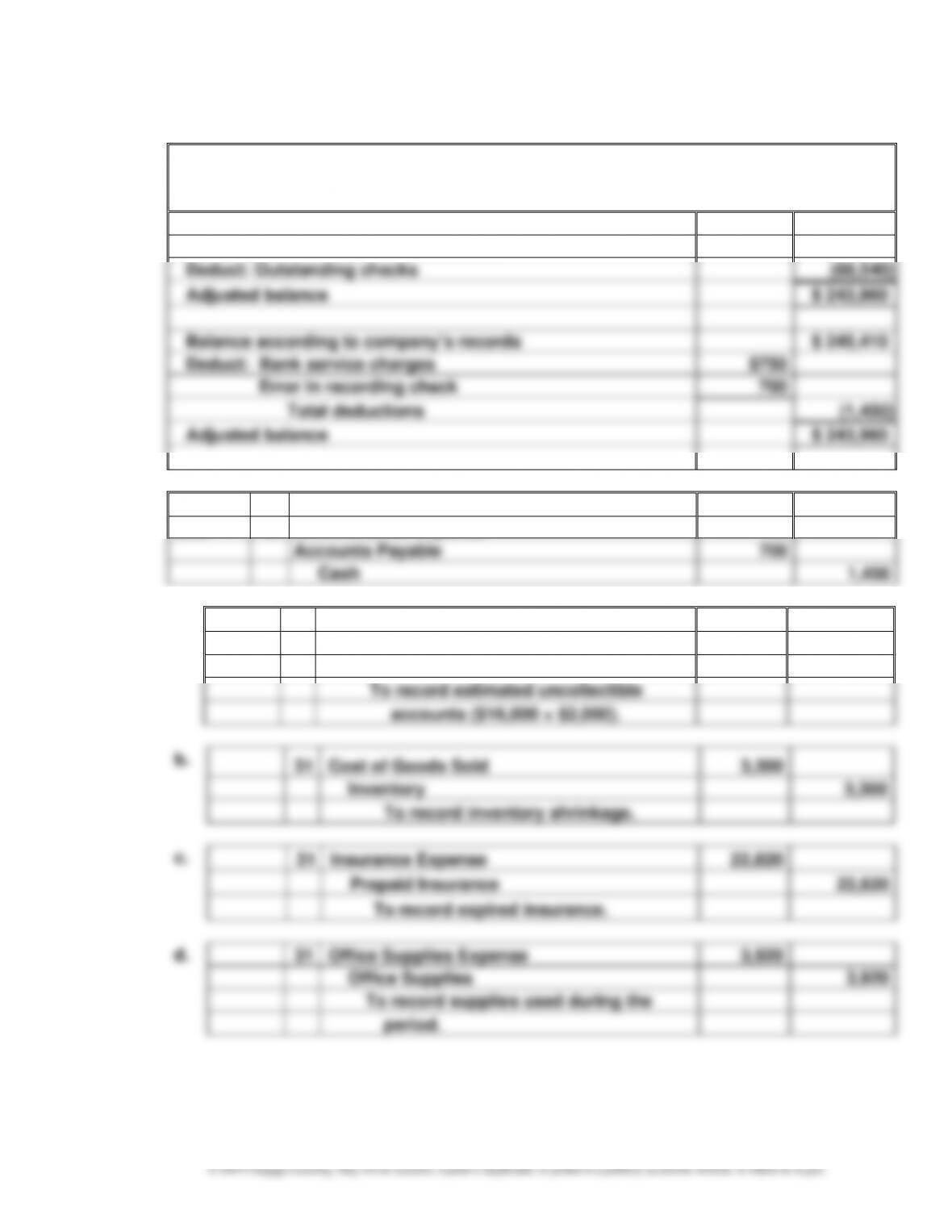

Bank Reconciliation

December 31, 20Y5

Balance according to bank statement

$ 283,000

Add: Deposit in transit on December 31

29,500

Deduct: Outstanding checks

(68,540)

Adjusted balance

$ 243,960

Balance according to company’s records

$ 245,410

Deduct: Bank service charges

$750

Error in recording check

700

Total deductions

(1,450)

Adjusted balance

$ 243,960

3.

20Y5

Dec.

31

Miscellaneous Expense

750

Accounts Payable

700

Cash

1,450

4.

a.

20Y5

Dec.

31

Bad Debt Expense

18,000

Allowance for Doubtful Accounts

18,000

To record estimated uncollectible

accounts ($16,000 + $2,000).

b.

31

Cost of Goods Sold

3,300

Inventory

3,300

To record inventory shrinkage.

c.

31

Insurance Expense

22,820

Prepaid Insurance

22,820

To record expired insurance.

d.

31

Office Supplies Expense

3,920

Office Supplies

3,920

To record supplies used during the

period.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

Comp. Prob. 3 (Continued)

e.

20Y5

Dec.

31

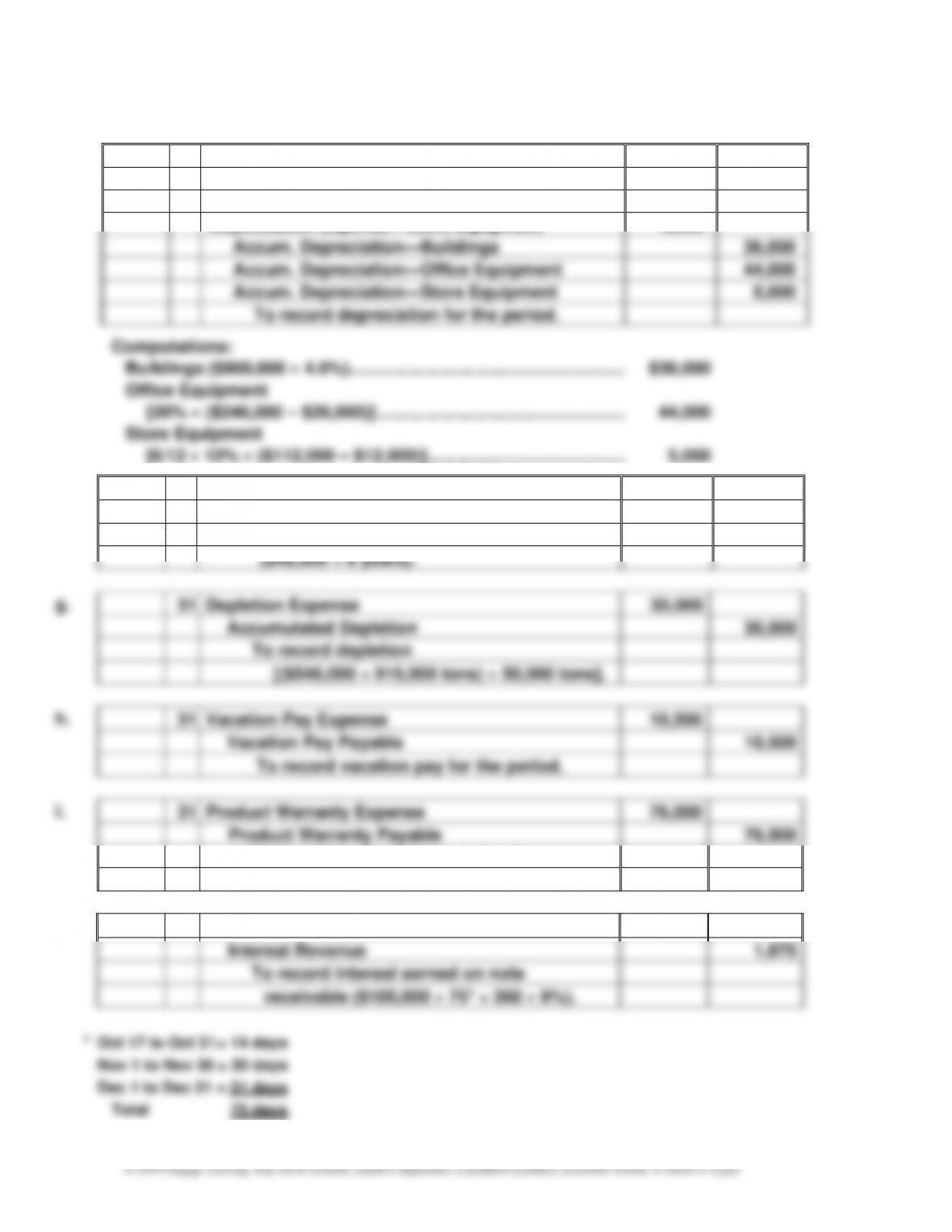

Depreciation Expense—Buildings

36,000

Depreciation Expense—Office Equipment

44,000

Depreciation Expense—Store Equipment

5,000

Accum. Depreciation—Buildings

36,000

Accum. Depreciation—Office Equipment

44,000

Accum. Depreciation—Store Equipment

5,000

To record depreciation for the period.

f.

20Y5

Amortization Expense—Patents

6,000

Dec.

31

Patents

6,000

To record patent amortization

($48,000 ÷ 8 years).

Depletion Expense

30,000

To record depletion

Vacation Pay Expense

10,500

10,500

Product Warranty Expense

76,000

Product Warranty Payable

76,000

Interest Receivable

Interest Revenue

To record interest earned on note

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–35

Comp. Prob. 3 (Continued)

5.

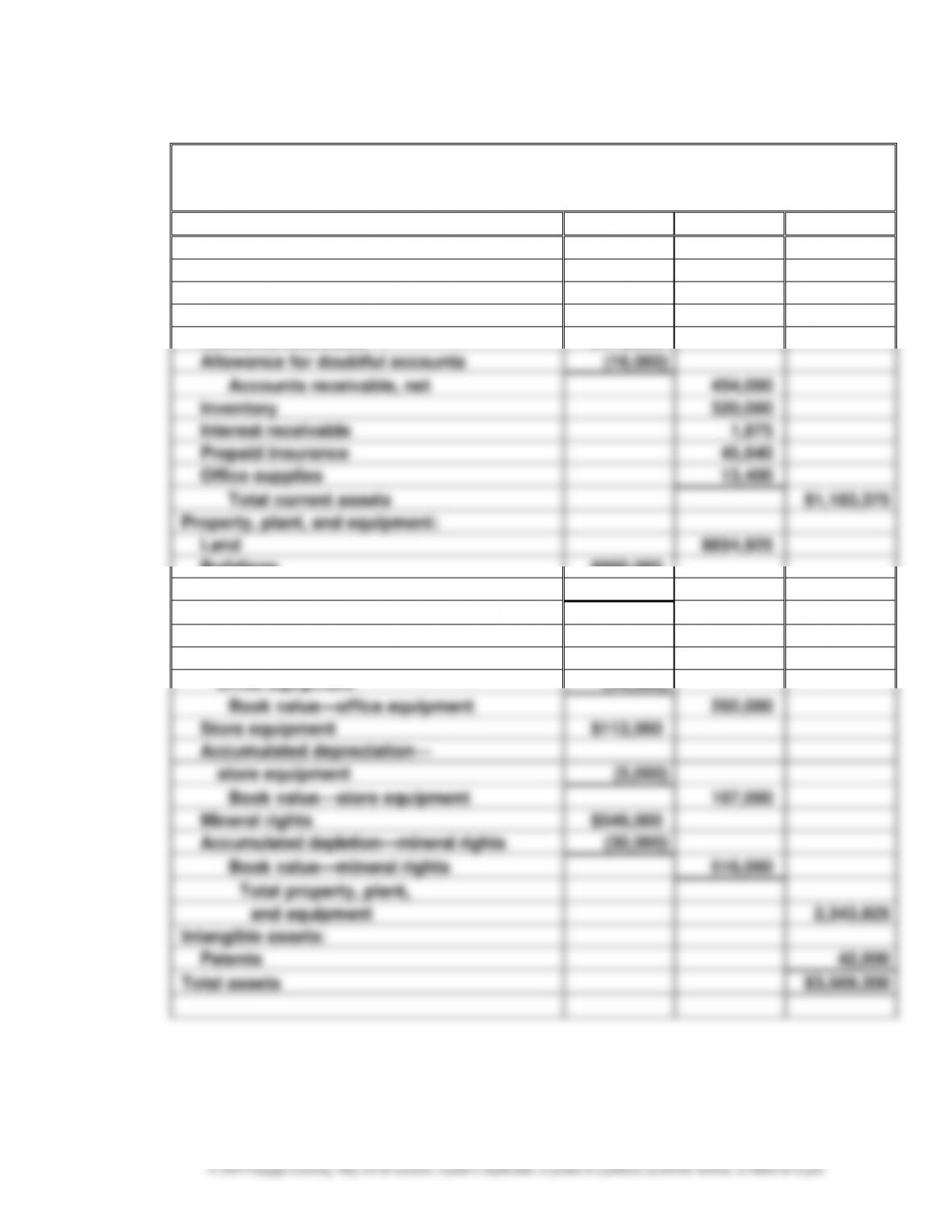

Kornett Company

Balance Sheet

December 31, 20Y5

Assets

Current assets:

Petty cash

$ 4,500

Cash

243,960

Notes receivable

100,000

Accounts receivable

$470,000

Allowance for doubtful accounts

(16,000)

Accounts receivable, net

454,000

Inventory

320,000

Interest receivable

1,875

Prepaid insurance

45,640

Office supplies

13,400

Total current assets

$1,183,375

Property, plant, and equipment:

Land

$654,925

Buildings

$900,000

Accumulated depreciation—buildings

(36,000)

Book value—buildings

864,000

Office equipment

$246,000

Accumulated depreciation—

office equipment

(44,000)

Book value—office equipment

202,000

Store equipment

$112,000

Accumulated depreciation—

store equipment

(5,000)

Book value—store equipment

107,000

Mineral rights

$546,000

Accumulated depletion—mineral rights

(30,000)

Book value—mineral rights

516,000

Total property, plant,

and equipment

2,343,925

Intangible assets:

Patents

42,000

Total assets

$3,569,300

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–36

Comp. Prob. 3 (Continued)

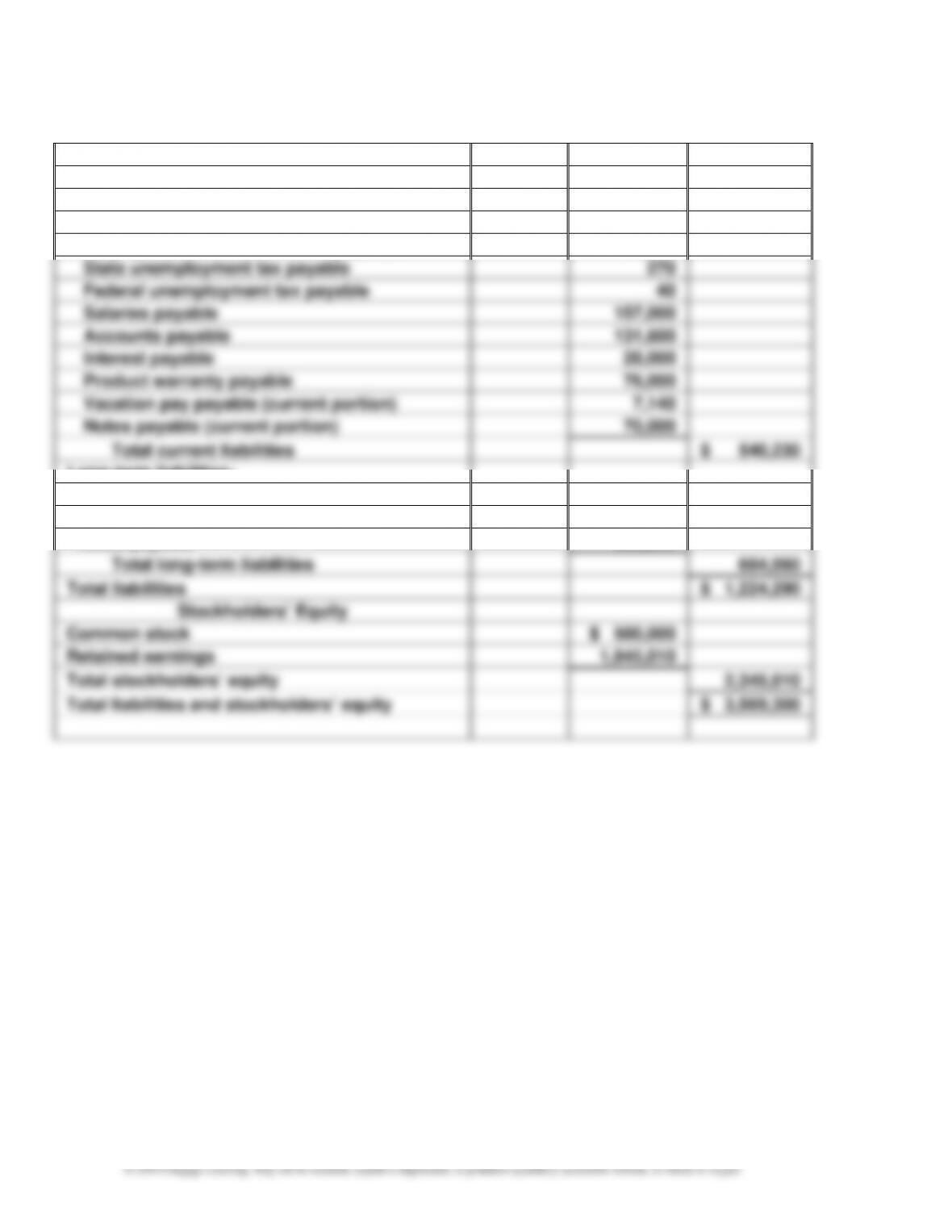

Liabilities

Current liabilities:

Social security tax payable

$ 25,470

Medicare tax payable

4,710

Employees federal income tax payable

40,000

State unemployment tax payable

270

Federal unemployment tax payable

40

Salaries payable

157,000

Accounts payable

131,600

Interest payable

28,000

Product warranty payable

76,000

Vacation pay payable (current portion)

7,140

Notes payable (current portion)

70,000

Total current liabilities

$ 540,230

Long-term liabilities:

Vacation pay payable

$ 3,360

Unfunded pension liability

50,700

Notes payable

630,000

Total long-term liabilities

684,060

Total liabilities

$ 1,224,290

Stockholders’ Equity

Common stock

$ 500,000

Retained earnings

1,845,010

Total stockholders’ equity

2,345,010

Total liabilities and stockholders’ equity

$ 3,569,300

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

MAKE A DECISION

MAD 10–1

a. Working Capital = Current Assets – Current Liabilities

10–38

MAD 10–1 (Concluded)

Amazon has 56.7% (42.2% + 14.5%) of its current assets consisting of cash and short-term

MAD 10–2

a. Working Capital = Current Assets – Current Liabilities

(in thousands)

b. Current Ratio =

sLiabilitieCurrent

setsCurrent As

$1,139,300 =

sLiabilitieCurrent

Abercrombie:

1.3

$486,000

$93,384 $547,189 =

+

The Gap:

0.7

$2,453,000

$1,783,000 =

d. Working capital is not a good measure for comparing the liquidity of two companies of

different sizes. In this case, The Gap’s current assets are nearly four times larger than

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

MAD 10–3

a. Working Capital = Current Assets – Current Liabilities

b.

sLiabilitieCurrent

setsCurrent As

RatioCurrent =

1.0

$1,909,443

$1,816,778

:3 Year

0.8

$2,217,912

$1,848,598

:2 Year

1.2

$1,935,647

$2,247,047

:1 Year

=

=

=

c.

sLiabilitieCurrent

AssetsQuick

Ratio Quick =

0.5

$1,909,443

$581,381 $296,967

:3 Year

0.4

$2,217,912

$599,073 $346,529

:2 Year

0.6

$1,935,647

$596,940 $97,131 $374,854

:1 Year

=

+

=

+

=

++

d. The quick ratio at the end of Year 1 was 0.6, indicating a tight short-term coverage of

current liabilities with quick assets. This is less of a concern because inventory turns into

10–40

MAD 10–4

a. Kohl’s has over four times the current assets of Neiman Marcus. Thus, using working

sLiabilitieCurrent

Neiman Marcus:

0.1

$840

$62 =

Kohl’s:

0.4

$2,974

$1,074 =

c. Kohl’s quick ratio of 0.4 is four times that of Neiman Marcus’s 0.1. Both companies have a

quick ratio less than 1.0. The small quick ratios can be partially explained by both

MAD 10–5

a. The gift cards represent unearned revenue (a liability). The gift cards have been

b. The credit card loans to the credit card customers do appear to represent mostly

short-term receivables based on the credit card data provided. The average account

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

MAD 10–5 (Concluded)

c.

sLiabilitieCurrent

setsCurrent As

RatioCurrent =

$7,037 =

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

TAKE IT FURTHER

TIF 10–1

1. Cannally and Kennedy is not obligated to pay a bonus to its employees under any

circumstances. The decision to pay a bonus is entirely discretionary. Companies

2. Tonya Latirno, on the other hand, is behaving unethically. Feeling that she is being

cheated, Tonya is attempting to replace the bonus by working overtime that is not

TIF 10–2

1. The so-called “underground economy” hides transactions from IRS scrutiny by

conducting business with cash (not check or credit card, which leaves an audit trail). The

intent in many such transactions is to evade income tax illegally. However, just because a

2. Marvin should respond that he would rather receive a payroll check as a normal employee.

As an employee, receiving cash rather than a payroll check subverts the U.S. tax system.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

TIF 10–3

A sample solution based on Starbucks’ Form 10-K for the fiscal year ended October 2, 2016,

follows:

1. $4,546.9 million. The company’s current liabilities include accounts payable, accrued

2. The company’s current liabilities have increased from $3,648.1 million to $4,546.9 million.

4. $400 million (balance sheet)

TIF 10–4

Memo

To: U. D. Mach III

From: A+ Student

Re: Financial Reporting of Series 3 Shock Absorber Lawsuit

10–44

TIF 10–4 (Concluded)

An alternative argument could be made that the uncertainty surrounding the connection

between the manufacturing defect and the cracked shock absorber is too uncertain to

TIF 10–5

Sumana’s interpretation of the pension issue is correct. The employee earns the pension

during the working years. The pension is part of the employee’s compensation that is

deferred until retirement. Thus, Felton should record an expense equal to the amount of