10–1

CHAPTER 10

LIABILITIES: CURRENT, INSTALLMENT NOTES,

AND CONTINGENCIES

DISCUSSION QUESTIONS

1. No. A discounted note payable has no stated interest rate, but provides interest by discounting the note

3. The deductions from employees’ earnings are for amounts owed (liabilities) to others for such items as

federal taxes, state and local income taxes, and contributions to pension plans.

4. 1. a

5. An advantage of using a separate payroll bank account is that reconciling the bank statements is

6. The vacation pay expense should be recorded during the period in which the vacation privilege is earned.

7. In a defined contribution plan, the company invests contributions on behalf of the employee during the

8. a. Each periodic payment includes (1) a repayment of the principal amount of the note and (2) a payment

of interest on the outstanding balance.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

BASIC EXERCISES

BE 10–1

BE 10–2

Total wage payment ………………………………………………… $ 800.00

BE 10–3

Salaries Expense

70,000

Social Security Tax Payable

4,200

Medicare Tax Payable

1,050

Employees Federal Income Tax Payable

15,350

Retirement Savings Deductions Payable

2,800

Salaries Payable

46,600

BE 10–4

Payroll Tax Expense

5,994

Social Security Tax Payable

4,200

Medicare Tax Payable

1,050

State Unemployment Tax Payable

648

Federal Unemployment Tax Payable

96

State Unemployment Tax Payable = $12,000 5.4% = $648

Federal Unemployment Tax Payable = $12,000 0.8% = $96

BE 10–5

a.

Vacation Pay Expense

40,000

Vacation Pay Payable

40,000

Vacation pay accrued for the period.

b.

Pension Expense

222,750

Cash

185,000

Unfunded Pension Liability

37,750

To record pension cost and funding.

10–3

BE 10–6

a.

Cash

45,000

Notes Payable

45,000

Issued installment notes for cash.

b.

Interest Expense

3,600

Notes Payable

6,134

Cash

9,734

Paid principal and interest on installment notes.

BE 10–7

a.

July

31

Product Warranty Expense

14,625

Product Warranty Payable

14,625

To record warranty expense for

July (4.5% $325,000).

b.

Nov.

11

Product Warranty Payable

220

Cash

220

BE 10–8

a.

sLiabilitieCurrent

AssetsQuick

Ratio Quick =

1.6

$1,875

$800 $1,200 $1,000

:20Y4

1.5

$2,300

$910 $1,400 $1,140

:20Y3

=

++

=

++

b. The quick ratio of Adieu Company has improved from 1.5 in 20Y3 to 1.6 in 20Y4. This

increase is the result of small decreases in the three types of quick assets (cash,

temporary investments, and accounts receivable) compared to the larger decrease in the

current liability, accounts payable. The increase shows Adieu to be in a better position to

pay current liabilities within a short period of time.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–4

EXERCISES

Ex. 10–1

Current liabilities as of March 31st, 2016:

Ex. 10–2

a. 1. Bennett Enterprises:

Inventory

400,000

Notes Payable

400,000

2.

Notes Payable

400,000

Interest Expense

5,000

Cash

405,000

b. 1. Spectrum Industries:

Notes Receivable

400,000

Sales

400,000

2.

Cash

405,000

Notes Receivable

400,000

Interest Revenue

5,000

Interest Expense/Revenue = $400,000 5% 90 360 = $5,000

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

Ex. 10–3

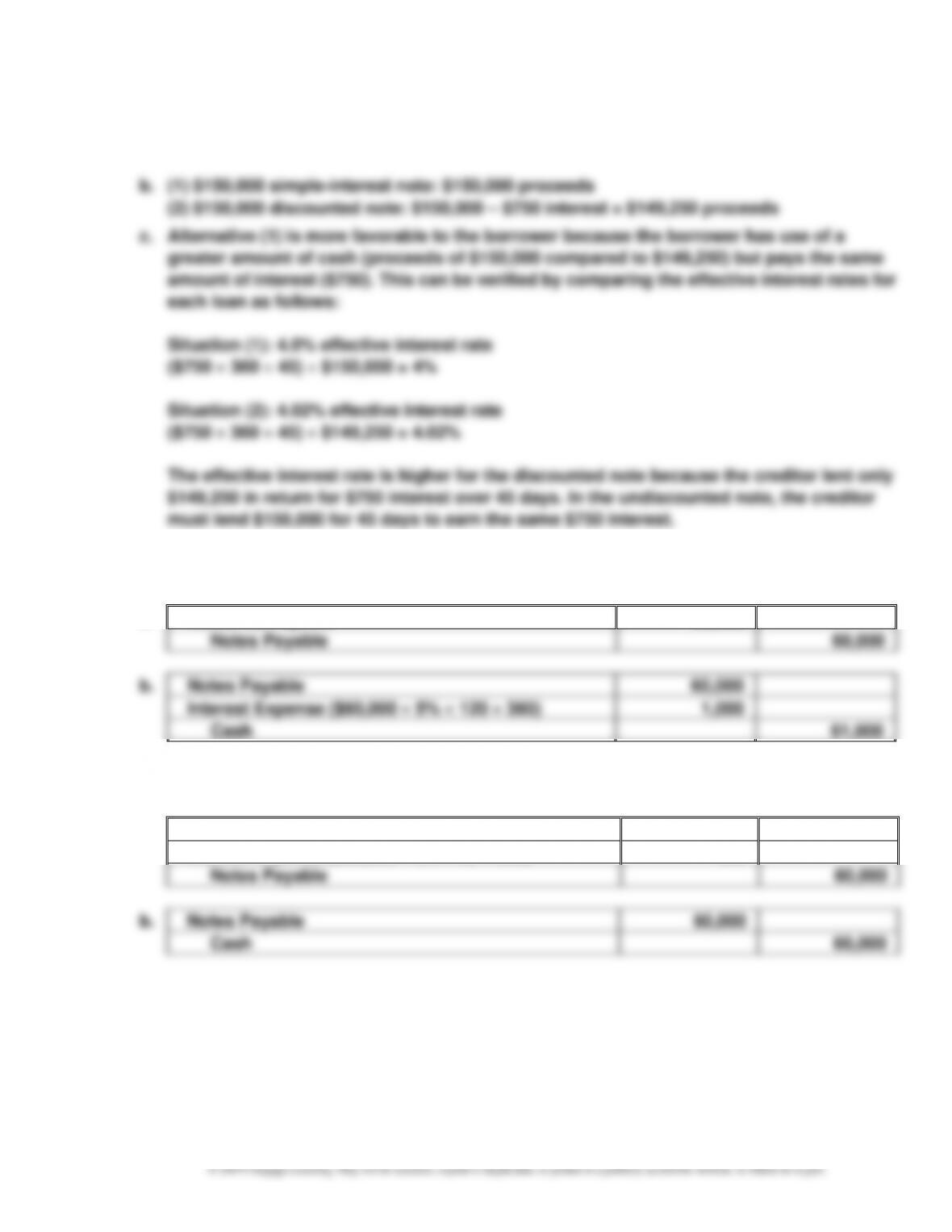

a. $150,000 4% 45 360 = $750 for each alternative.

Ex. 10–4

a.

Accounts Payable

60,000

Notes Payable

60,000

60,000

Cash

61,000

a.

Notes Payable

60,000

Cash

60,000

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

Ex. 10–6

a.

June

30

Building

560,000

Land

400,000

Notes Payable

600,000

Cash

360,000

b.

Dec.

31

Notes Payable

30,000

Interest Expense

15,000

Cash

45,000

(First installment interest =

$600,000 5% 6/12)

June

30

Notes Payable

30,000

Cash

44,250

[Second installment interest =

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–7

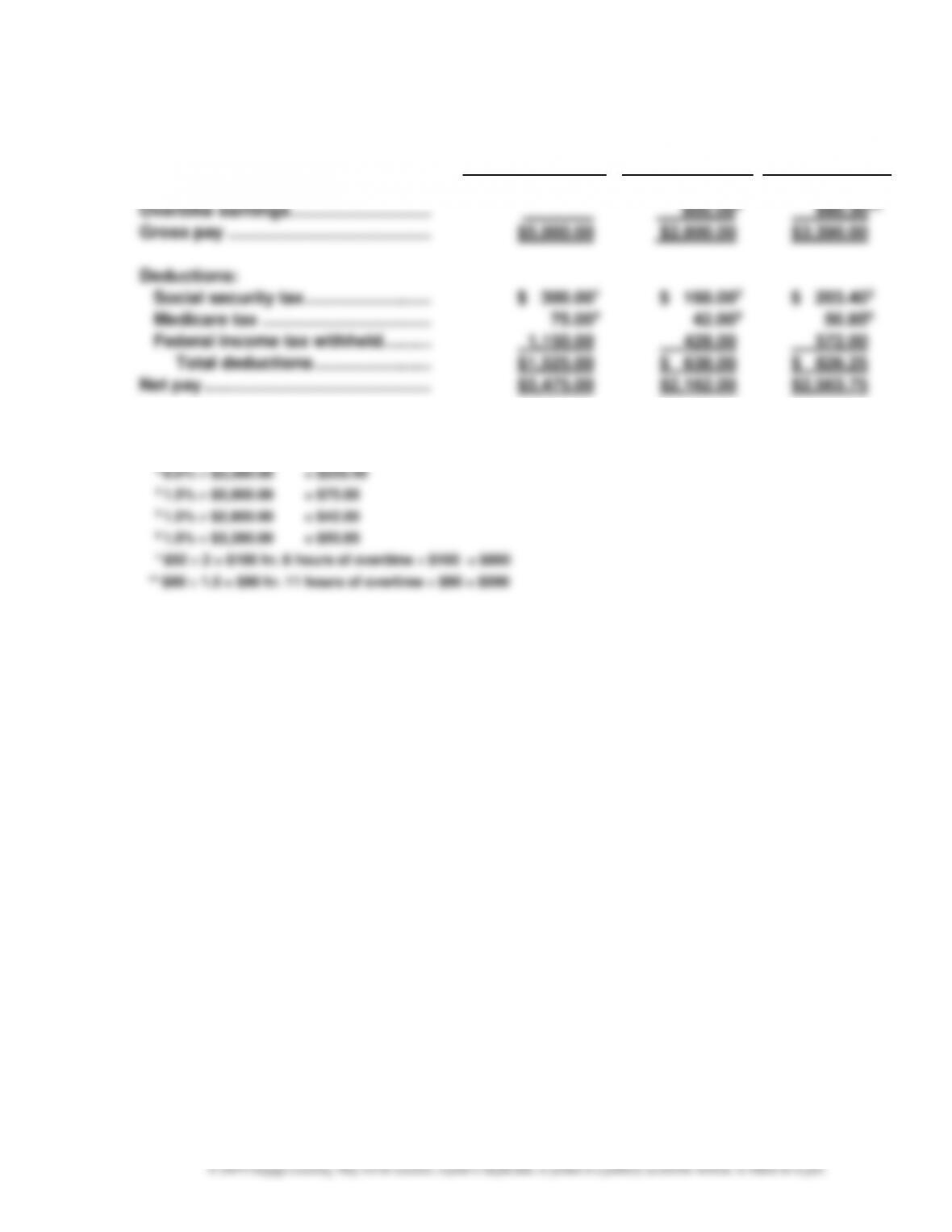

Ex. 10–9

Consultant

Computer

Programmer

Administrator

Regular earnings ………………………….

$5,000.00

$2,000.00

$2,400.00

Overtime earnings ………………………..

800.00*

990.00**

Gross pay ……………………………………

$5,000.00

$2,800.00

$3,390.00

Deductions:

Social security tax ……………………..

$ 300.001

$ 168.002

$ 203.403

Medicare tax ……………………………..

75.004

42.005

50.856

Federal income tax withheld ……….

1,150.00

428.00

572.00

Total deductions ……………………

$1,525.00

$ 638.00

$ 826.25

Net pay …………………………..……………

$3,475.00

$2,162.00

$2,563.75

1 6.0% $5,000.00 = $300.00

2 6.0% $2,800.00 = $168.00

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–8

Ex. 10–10

a. Summary: (1) $460,000; (3) $540,000; (8) $6,750; (12) $135,000

Net amount paid ………………………………………………………… $ 338,850

Total earnings …………………………..……………………………… $ 540,000

b.

Factory Wages Expense

285,000

Sales Salaries Expense

135,000

Office Salaries Expense

120,000

Social Security Tax Payable

32,400

Medicare Tax Payable

8,100

Employees Income Tax Payable

135,000

Medical Insurance Payable

18,900

Union Dues Payable

6,750

Salaries Payable

338,850

c.

Salaries Payable

338,850

cash

338,850

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–9

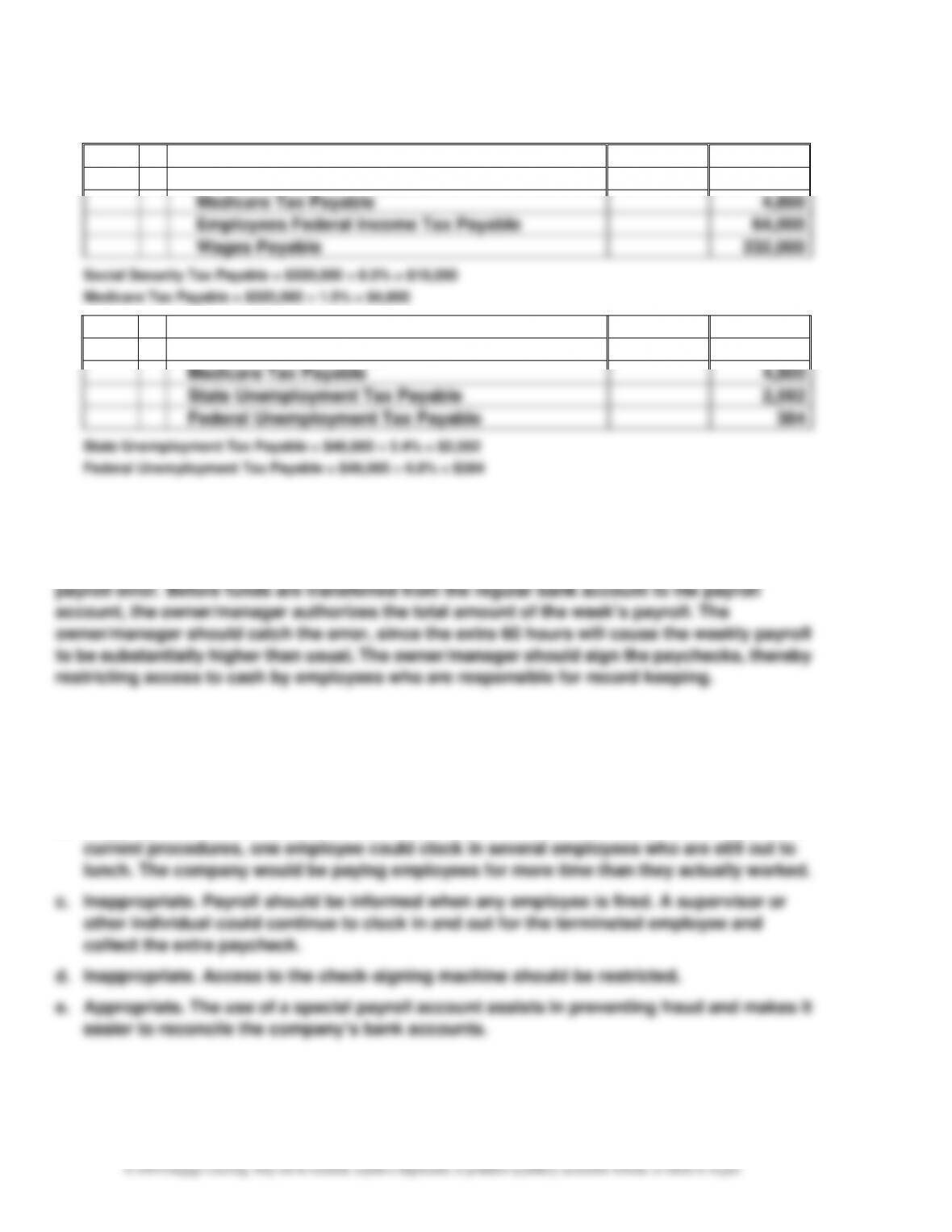

Ex. 10–11

a. Social security tax (6% $110,000) …………………………………………………………. $6,600

$9,800

b.

Payroll Tax Expense

9,800

Social Security Tax Payable

6,600

Medicare Tax Payable

1,650

State Unemployment Tax Payable

1,350

Federal Unemployment Tax Payable

200

Ex. 10–12

a.

May

18

Salaries Expense

615,000

Social Security Tax Payable ($615,000 6%)

36,900

Medicare Tax Payable ($615,000 1.5%)

9,225

Employees Federal Income Tax Payable

165,000

Salaries Payable

403,875

b.

May

18

Payroll Tax Expense

48,915

Social Security Tax Payable

36,900

Medicare Tax Payable

9,225

State Unemployment Tax Payable

2,430

Federal Unemployment Tax Payable

360

State Unemployment Tax Payable = $45,000 5.4% = $2,430

Federal Unemployment Tax Payable = $45,000 0.8% = $360

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–10

Ex. 10–13

a.

June

17

Wages Expense

320,000

Social Security Tax Payable

19,200

Medicare Tax Payable

4,800

Employees Federal Income Tax Payable

64,000

Wages Payable

232,000

b.

June

17

Payroll Tax Expense

26,976

Social Security Tax Payable

19,200

Medicare Tax Payable

4,800

State Unemployment Tax Payable

2,592

Federal Unemployment Tax Payable

384

State Unemployment Tax Payable = $48,000 5.4% = $2,592

Federal Unemployment Tax Payable = $48,000 0.8% = $384

Ex. 10–14

Big Howie’s Hot Dog Stand does have an internal control procedure that should detect the

Ex. 10–15

a. Appropriate. All changes to the payroll system, including wage rate increases, should be

authorized by someone outside the Payroll Department.

b. Inappropriate. Each employee should record his or her own time out for lunch. Under the

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–11

Ex. 10–16

a.

Jan.

31

Vacation Pay Expense

3,500

Vacation Pay Payable

3,500

Vacation pay accrued for January

($42,000 1/12).

b. Vacation pay is reported as a current liability on the balance sheet. If employees are

Ex. 10–17

a.

Dec.

31

Pension Expense

365,000

Unfunded Pension Liability

365,000

To record quarterly pension cost.

Jan.

15

Unfunded Pension Liability

365,000

Cash

365,000

b. In a defined contribution plan, the company invests contributions on behalf of the

employee during the employee’s working years. Normally, the employee and employer

contribute to the plan. The employee’s pension depends on the total contributions and the

Ex. 10–18

The $5,955 million unfunded pension liability is the approximate amount of the pension

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–12

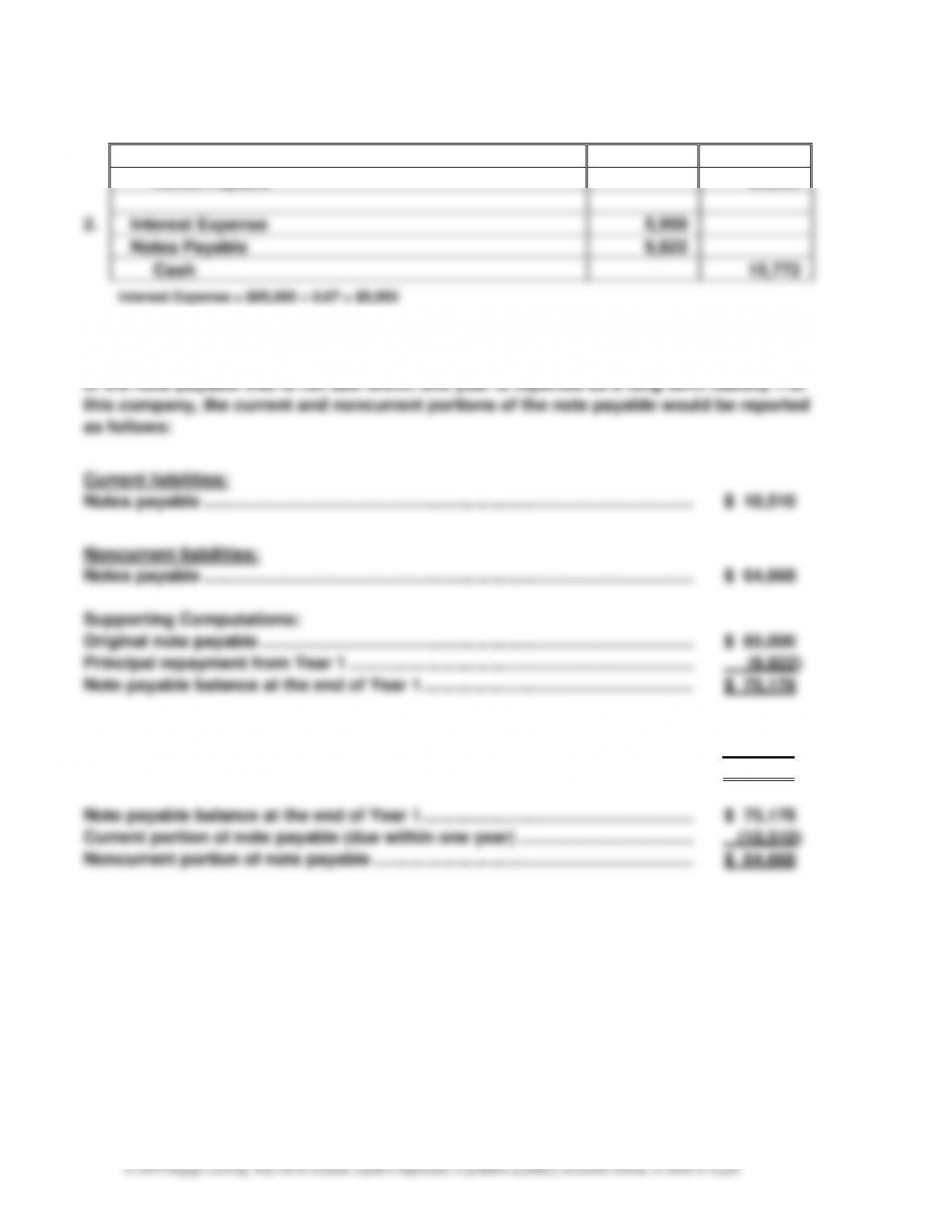

Ex. 10–19

a.

1.

Cash

85,000

Notes Payable

85,000

2.

Interest Expense

5,950

Notes Payable

9,822

Cash

15,772

b. Notes payable are reported as liabilities on the balance sheet. The portion of the note

payable that is due within one year is reported as a current liability. The remaining portion

Annual payment on note ………………………………………………………………………… $ 15,772

Second year interest payment ($75,178 0.07) …………………………..……………. (5,262)

Principal repayment portion of next installment ………………………………………. $ 10,510

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–13

Ex. 10–20

20Y2

Jan.

1

Cash

175,000

Notes Payable

175,000

Dec.

31

Interest Expense

14,000

Notes Payable

29,830

Cash

43,830

20Y5

Dec.

31

Interest Expense

6,253

Notes Payable

37,577*

Cash

43,830

Ex. 10–21

a.

A

B

C

D

E

For the

Year Ending

Dec. 31

January 1

Carrying

Amount

Note

Payment

(Cash Paid)

Interest Expense

(7% of January 1

Note Carrying Amount)

Decrease in

Notes

Payable

(B – C)

Dec. 31

Carrying

Amount

(A – D)

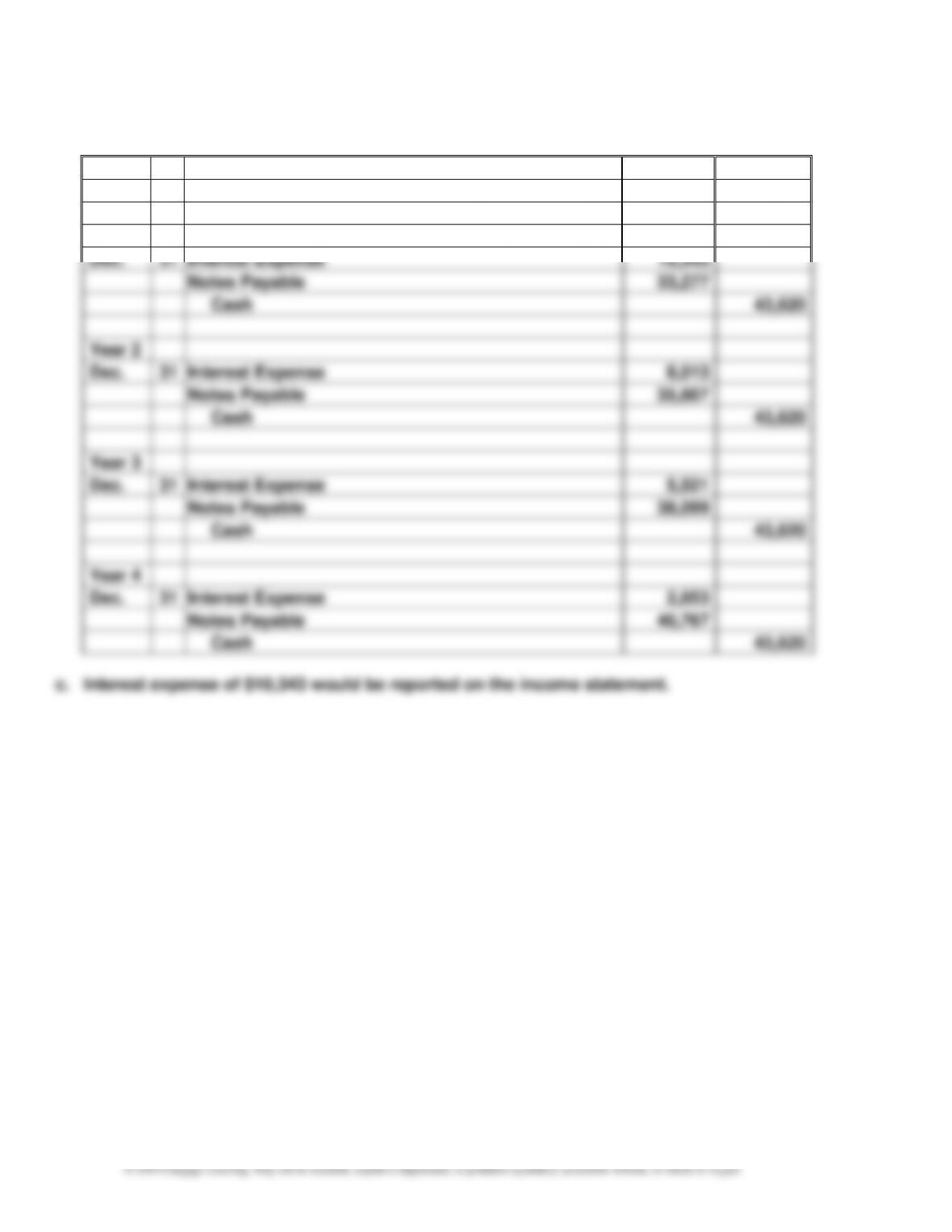

Year 1

$147,750

$ 43,620

$10,343 (7% of $147,750)

$ 33,277

$114,473

Year 2

114,473

43,620

8,013 (7% of $114,473)

35,607

78,866

Year 3

78,866

43,620

5,521 (7% of $78,866)

38,099

40,767

Year 4

40,767

43,620

2,853*

40,767

0

$174,480

$26,730

$147,750

* The interest expense in Year 4 is rounded to $2,853.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–14

Ex. 10–21 (Concluded)

b.

Year 1

Jan.

1

Cash

147,750

Notes Payable

147,750

Dec.

31

Interest Expense

10,343

Notes Payable

33,277

Cash

43,620

Year 2

Dec.

31

Interest Expense

8,013

Notes Payable

35,607

Cash

43,620

Year 3

Dec.

31

Interest Expense

5,521

Notes Payable

38,099

Cash

43,620

Year 4

Dec.

31

Interest Expense

2,853

Notes Payable

40,767

Cash

43,620

c. Interest expense of $10,343 would be reported on the income statement.

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–15

Ex. 10–22

a.

Jan.

31

Product Warranty Expense

30,000

Product Warranty Payable

30,000

To record warranty expense for January

($1,500,000 2%).

b.

Feb.

7

Product Warranty Payable

445

Supplies

325

Wages Payable

120

Ex. 10–23

a. The warranty liability represents estimated outstanding automobile warranty claims. Of

b.

Product Warranty Expense

4,132,000,000

Product Warranty Payable

4,132,000,000

c. In order for a product warranty to be reported as a liability in the financial statements, it

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–16

Ex. 10–24

a.

Damage Awards and Fines

365,000

EPA Fines Payable

240,000

Litigation Claims Payable

125,000

Note to Instructors: The “Damage Awards and Fines” would be disclosed on the income

statement under “Other expenses.”

b. The company experienced a hazardous materials spill at one of its plants during the

previous period. This spill has resulted in a number of lawsuits to which the company is a

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–17

PROBLEMS

Prob. 10–1A

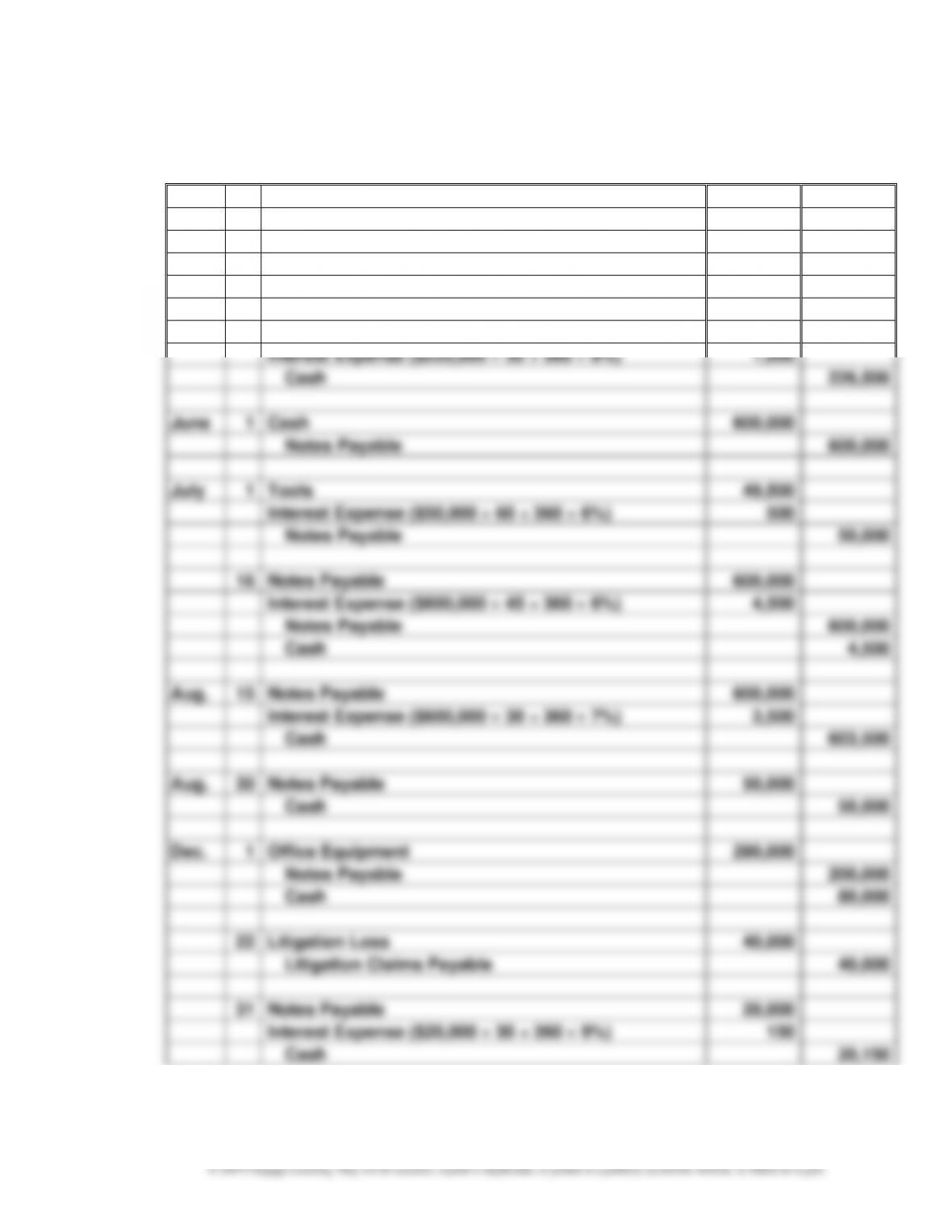

1.

Mar.

1

Inventory

225,000

Accounts Payable—Kirkwood Co.

225,000

31

Accounts Payable—Kirkwood Co.

225,000

Notes Payable

225,000

Apr.

30

Notes Payable

225,000

Interest Expense ($225,000 30 ÷ 360 8%)

1,500

Cash

226,500

June

1

Cash

600,000

Notes Payable

600,000

July

1

Tools

49,500

Interest Expense ($50,000 60 ÷ 360 6%)

500

Notes Payable

50,000

16

Notes Payable

600,000

Interest Expense ($600,000 45 ÷ 360 6%)

4,500

Notes Payable

600,000

Cash

4,500

Aug.

15

Notes Payable

600,000

Interest Expense ($600,000 30 ÷ 360 7%)

3,500

Cash

603,500

Aug.

30

Notes Payable

50,000

Cash

50,000

Dec.

1

Office Equipment

280,000

Notes Payable

200,000

Cash

80,000

22

Litigation Loss

40,000

Litigation Claims Payable

40,000

31

Notes Payable

20,000

Interest Expense ($20,000 30 ÷ 360 9%)

150

Cash

20,150

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–18

Prob. 10–1A (Concluded)

2.

a.

Product Warranty Expense

65,000

Product Warranty Payable

65,000

Warranty expense for the current year.

b.

Interest Expense

1,350

Interest Payable

1,350

Interest on notes payable.

Interest Expense = ($280,000 – $80,000 – $20,000) 9% 30 ÷ 360, or $20,000 9 9% 30 ÷ 360

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

10–19

Prob. 10–2A

1.

a.

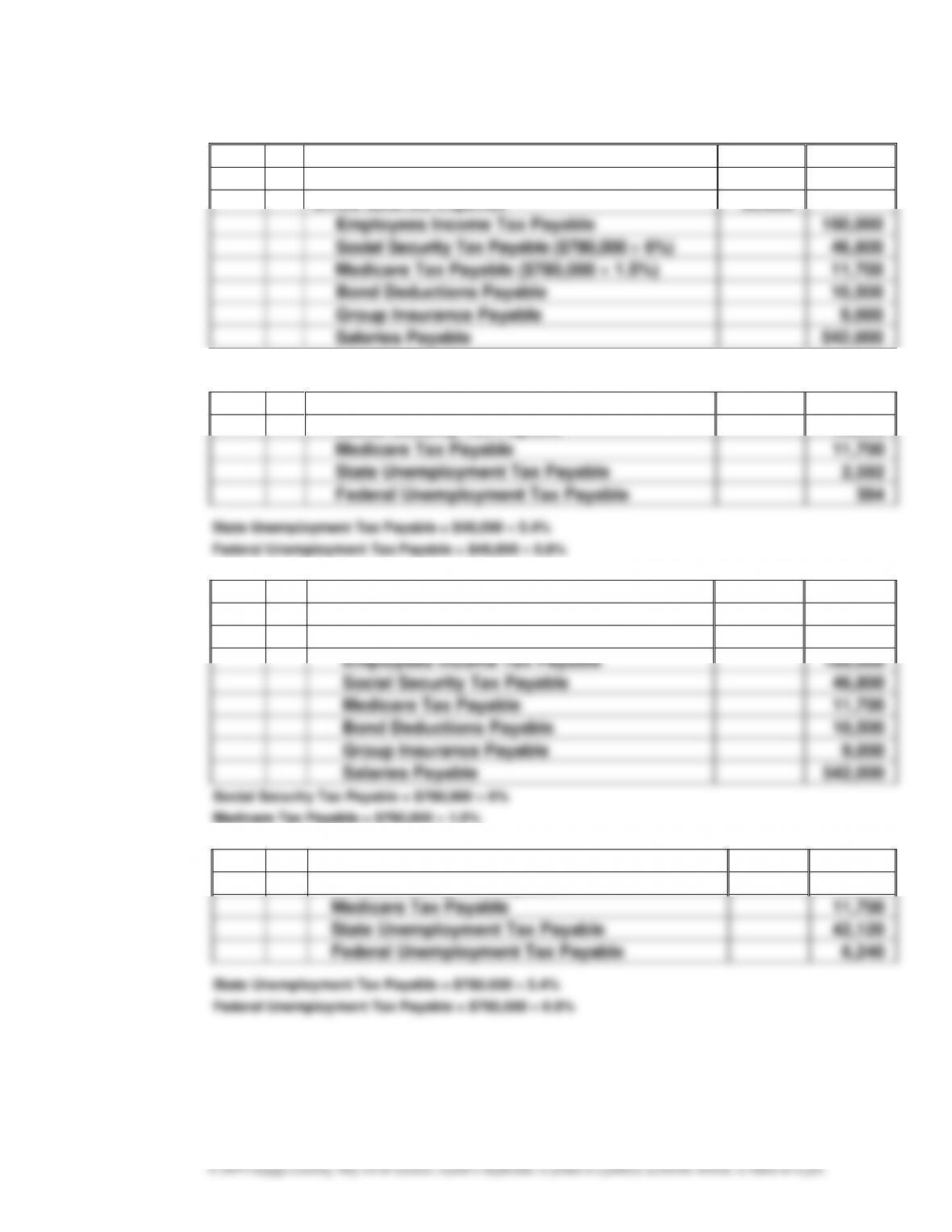

Dec.

30

Sales Salaries Expense

540,000

Warehouse Salaries Expense

155,000

Office Salaries Expense

85,000

Employees Income Tax Payable

160,000

Social Security Tax Payable ($780,000 6%)

46,800

Medicare Tax Payable ($780,000 1.5%)

11,700

Bond Deductions Payable

10,500

Group Insurance Payable

9,000

Salaries Payable

542,000

b.

Dec.

30

Payroll Tax Expense

61,476

Social Security Tax Payable

46,800

Medicare Tax Payable

11,700

State Unemployment Tax Payable

2,592

Federal Unemployment Tax Payable

384

State Unemployment Tax Payable = $48,000 5.4%

Federal Unemployment Tax Payable = $48,000 0.8%

2.

a.

Dec.

30

Sales Salaries Expense

540,000

Warehouse Salaries Expense

155,000

Office Salaries Expense

85,000

Employees Income Tax Payable

160,000

Social Security Tax Payable

46,800

Medicare Tax Payable

11,700

Bond Deductions Payable

10,500

Group Insurance Payable

9,000

Salaries Payable

542,000

Social Security Tax Payable = $780,000 6%

Medicare Tax Payable = $780,000 1.5%

b.

Jan.

5

Payroll Tax Expense

106,860

Social Security Tax Payable

46,800

Medicare Tax Payable

11,700

State Unemployment Tax Payable

42,120

Federal Unemployment Tax Payable

6,240

CHAPTER 10 Liabilities: Current, Installment Notes, and Contingencies

Prob. 10–3A

1.

Employee

Gross

Earnings

Federal Income

Tax Withheld

Social Security

Tax Withheld

Medicare

Tax Withheld

Arnett …………

$ 9,000.00

$ 1,698.00

$ 540.00

$ 135.00

Cruz …………..

55,200.00

9,576.00

3,312.00

828.00

Edwards …….

24,600.00

4,896.00

1,476.00

369.00

Harvin ………..

5,900.00

1,052.00

354.00

88.50

Nicks ………….

132,000.00

31,020.00

7,920.00

1,980.00

Shiancoe ……

113,000.00

25,330.00

6,780.00

1,695.00

Ward ………….

7,050.00

1,182.00

423.00

105.75

$346,750.00

$ 74,754.00

$ 20,805.00

$ 5,201.25

2. a. Social security tax paid by employer ……………………………………………… $20,805.00