CHAPTER 1 Introduction to Accounting and Business

1–36

Prob. 1–5B (Continued)

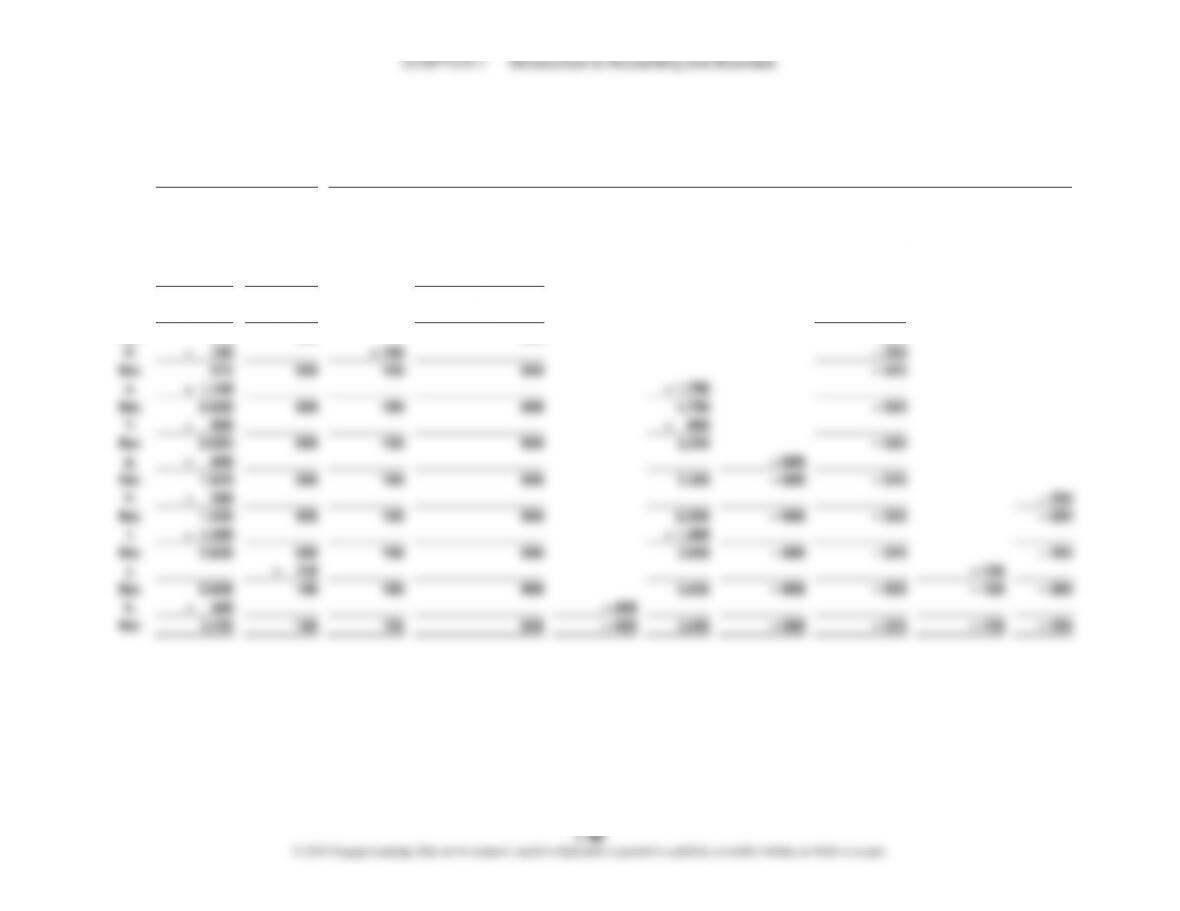

3.

Bev’s Dry Cleaners

Income Statement

For the Month Ended November 30, 20Y3

Dry cleaning revenue

$110,000

Expenses:

Dry cleaning expense

$ 29,450

Wages expense

24,000

Supplies expense

7,200

Rent expense

4,000

Truck expense

2,100

Utilities expense

1,800

Miscellaneous expense

1,300

Total expenses

(69,850)

Net income

$ 40,150

Bev’s Dry Cleaners

Statement of Stockholders’ Equity

For the Month Ended November 30, 20Y3

Common

Stock

Retained

Earnings

Total

Balances, November 1, 20Y3

$ 50,000

$ 98,500

$ 148,500

Issued common stock

21,000

21,000

Net income

40,150

40,150

Dividends

(5,000)

(5,000)

Balances, November 30, 20Y3

$ 71,000

$133,650

$ 204,650

Bev’s Dry Cleaners

Balance Sheet

November 30, 20Y3

Assets

Cash

$ 81,800

Accounts receivable

75,000

Supplies

11,800

Land

85,000

Total assets

$ 253,600

Liabilities

Accounts payable

$ 48,950

Stockholders’ Equity

Common stock

$ 71,000

Retained earnings

133,650

Total stockholders’ equity

204,650

Total liabilities and stockholders’ equity

$ 253,600

CHAPTER 1 Introduction to Accounting and Business

1–37

Prob. 1–5B (Concluded)

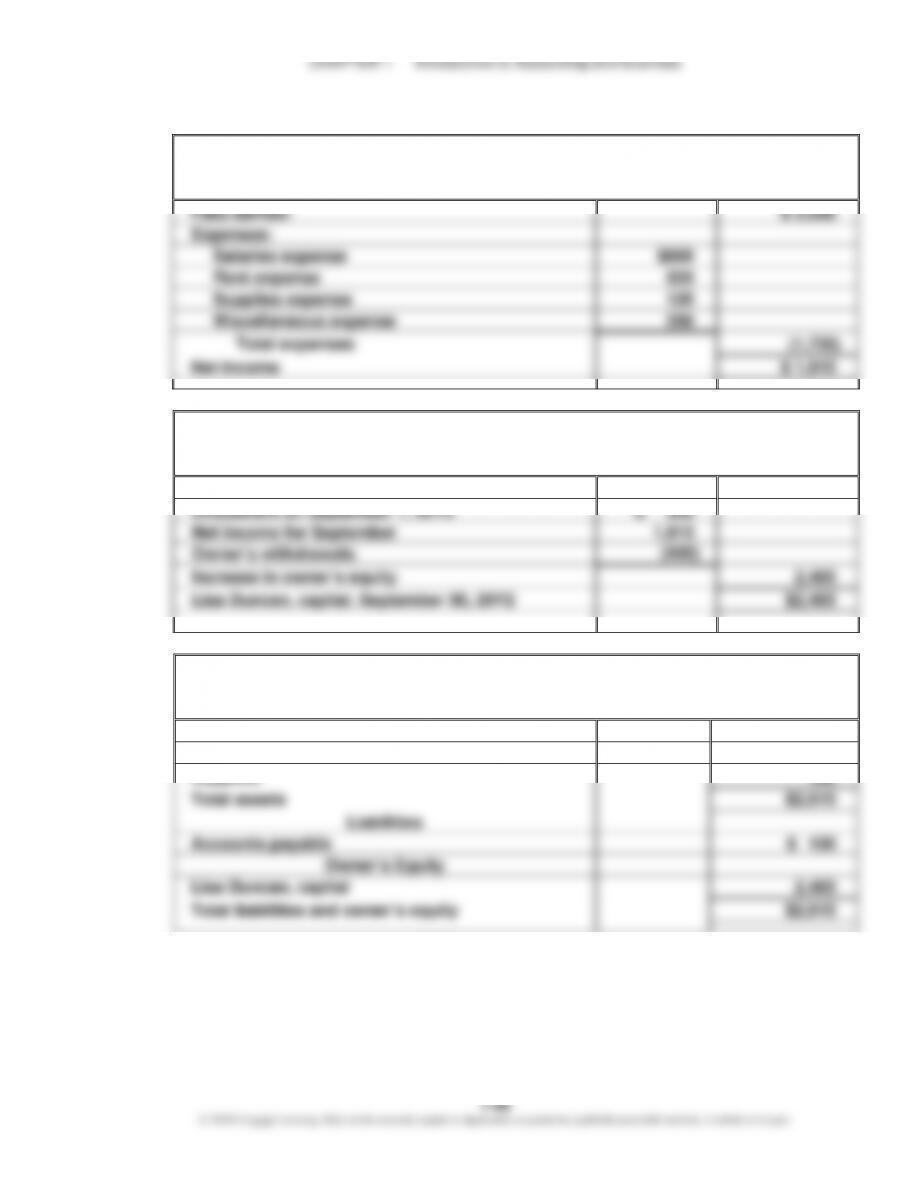

4. (Optional)

Bev’s Dry Cleaners

Statement of Cash Flows

For the Month Ended November 30, 20Y3

Cash flows from (used for) operating activities:

Cash received from customers*

$ 115,000

Cash paid for expenses and to creditors**

(53,200)

Net cash flows from operating activities

$ 61,800

Cash flows from (used for) investing activities:

Cash paid for acquisition of land

(35,000)

Cash flows from (used for) financing activities:

Cash received from issuing common stock

$ 21,000

Cash paid for dividends

(5,000)

Net cash flows from financing activities

16,000

Net increase in cash

$ 42,800

Cash balance, November 1, 20Y3

39,000

Cash balance, November 30, 20Y3

$ 81,800

* $38,000 + $77,000; these amounts are taken from the Cash column of the spreadsheet in Part 2.

** $4,000 + $20,000 + $29,200; these amounts are taken from the Cash column of the spreadsheet in

Part 2.

CHAPTER 1 Introduction to Accounting and Business

1–38

Prob. 1–6B

a. Wages expense, $203,200 ($288,000 – $48,000 – $17,600 – $14,400 – $4,800)

b. Net income, $112,000 ($400,000 – $288,000)

CHAPTER 1 Introduction to Accounting and Business

1–39

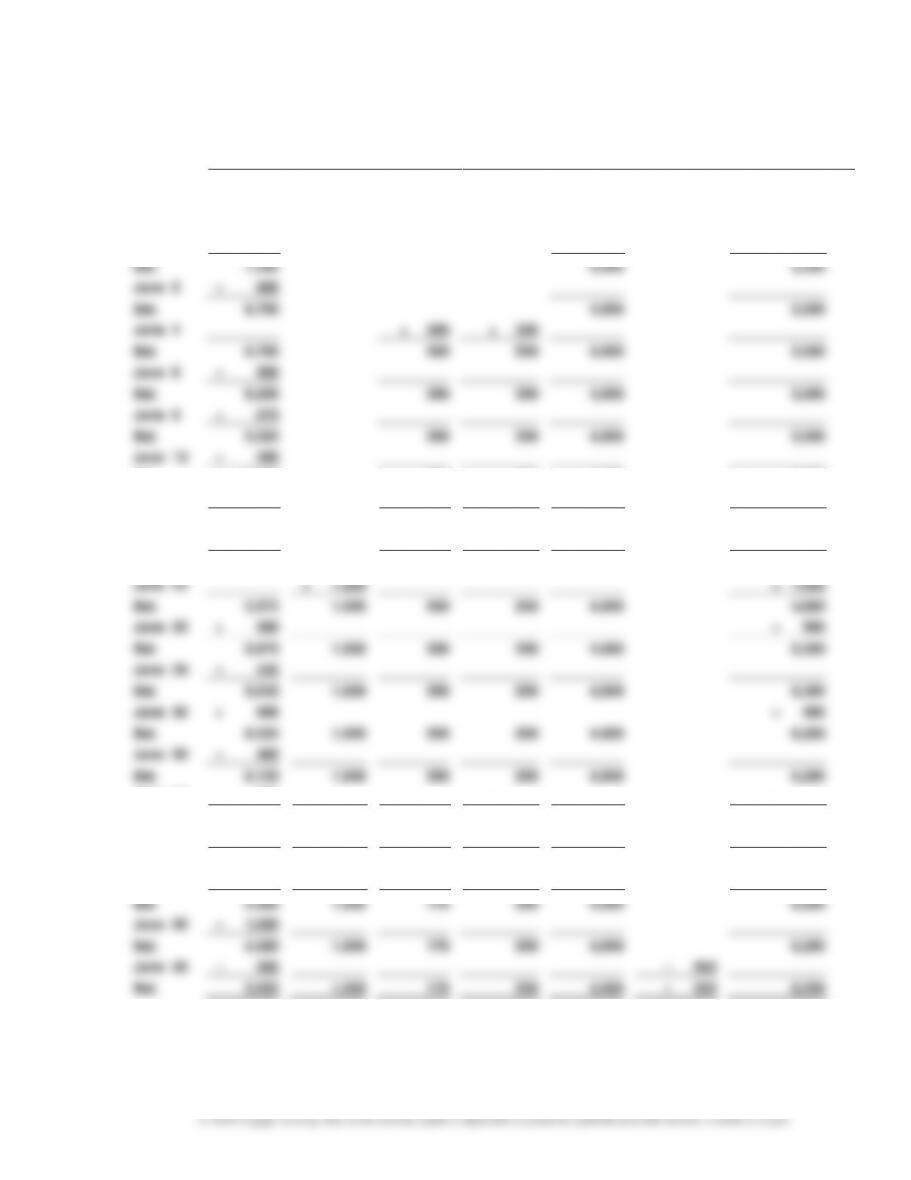

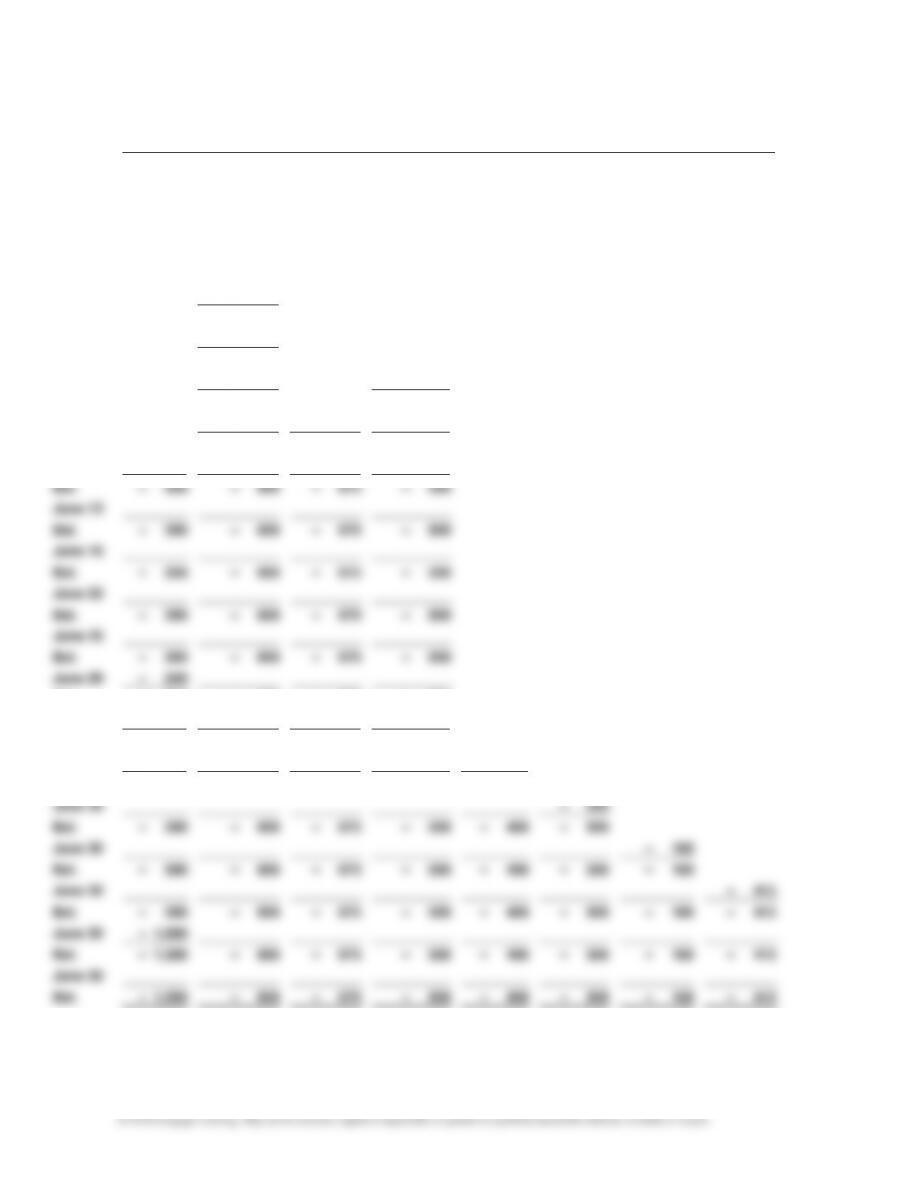

CONTINUING PROBLEM

1.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

+

Accts. Rec.

+

Supplies

=

Accts.

Payable

+

Common

Stock

–

Dividends

+

Fees

Earned

June 1

June 2

+ 4,000

+ 3,500

+ 4,000

+ 3,500

Bal.

7,500

4,000

3,500

June 2

– 800

Bal.

6,700

4,000

3,500

June 4

+ 350

+ 350

Bal.

6,700

350

350

4,000

3,500

June 6

– 500

Bal.

6,200

350

350

4,000

3,500

June 8

– 675

Bal.

5,525

350

350

4,000

3,500

June 12

– 350

Bal.

5,175

350

350

4,000

3,500

June 13

– 100

– 100

Bal.

5,075

350

250

4,000

3,500

June 16

+ 300

+ 300

Bal.

5,375

350

250

4,000

3,800

June 22

+ 1,000

+ 1,000

Bal.

5,375

1,000

350

250

4,000

4,800

June 25

+ 500

+ 500

Bal.

5,875

1,000

350

250

4,000

5,300

June 29

– 240

Bal.

5,635

1,000

350

250

4,000

5,300

June 30

+ 900

+ 900

Bal.

6,535

1,000

350

250

4,000

6,200

June 30

– 400

Bal.

6,135

1,000

350

250

4,000

6,200

June 30

– 300

Bal.

5,835

1,000

350

250

4,000

6,200

June 30

– 180

Bal.

5,835

1,000

170

250

4,000

6,200

June 30

– 415

Bal.

5,420

1,000

170

250

4,000

6,200

June 30

– 1,000

Bal.

4,420

1,000

170

250

4,000

6,200

June 30

– 500

– 500

Bal.

3,920

1,000

170

250

4,000

– 500

6,200

CHAPTER 1 Introduction to Accounting and Business

1–40

Continuing Problem (Continued)

Stockholders’ Equity (Continued)

–

Music

Exp.

–

Office Rent

Exp.

–

Equip.

Rent Exp.

–

Adver-

tising Exp.

–

Wages

Exp.

–

Utilities

Exp.

–

Supplies

Exp.

–

Misc. Exp.

June 1

June 2

Bal.

June 2

– 800

Bal.

June 4

– 800

Bal.

June 6

– 800

– 500

Bal.

June 8

– 800

– 675

– 500

Bal.

June 12

– 350

– 800

– 675

– 500

Bal.

June 13

– 350

– 800

– 675

– 500

Bal.

June 16

– 350

– 800

– 675

– 500

Bal.

June 22

– 350

– 800

– 675

– 500

Bal.

June 25

– 350

– 800

– 675

– 500

Bal.

June 29

– 350

– 240

– 800

– 675

– 500

Bal.

June 30

– 590

– 800

– 675

– 500

Bal.

June 30

– 590

– 800

– 675

– 500

– 400

Bal.

June 30

– 590

– 800

– 675

– 500

– 400

– 300

Bal.

June 30

– 590

– 800

– 675

– 500

– 400

– 300

– 180

Bal.

June 30

– 590

– 800

– 675

– 500

– 400

– 300

– 180

– 415

Bal.

June 30

– 590

– 1,000

– 800

– 675

– 500

– 400

– 300

– 180

– 415

Bal.

June 30

– 1,590

– 800

– 675

– 500

– 400

– 300

– 180

– 415

Bal.

– 1,590

– 800

– 675

– 500

– 400

– 300

– 180

– 415

CHAPTER 1 Introduction to Accounting and Business

1–41

Continuing Problem (Concluded)

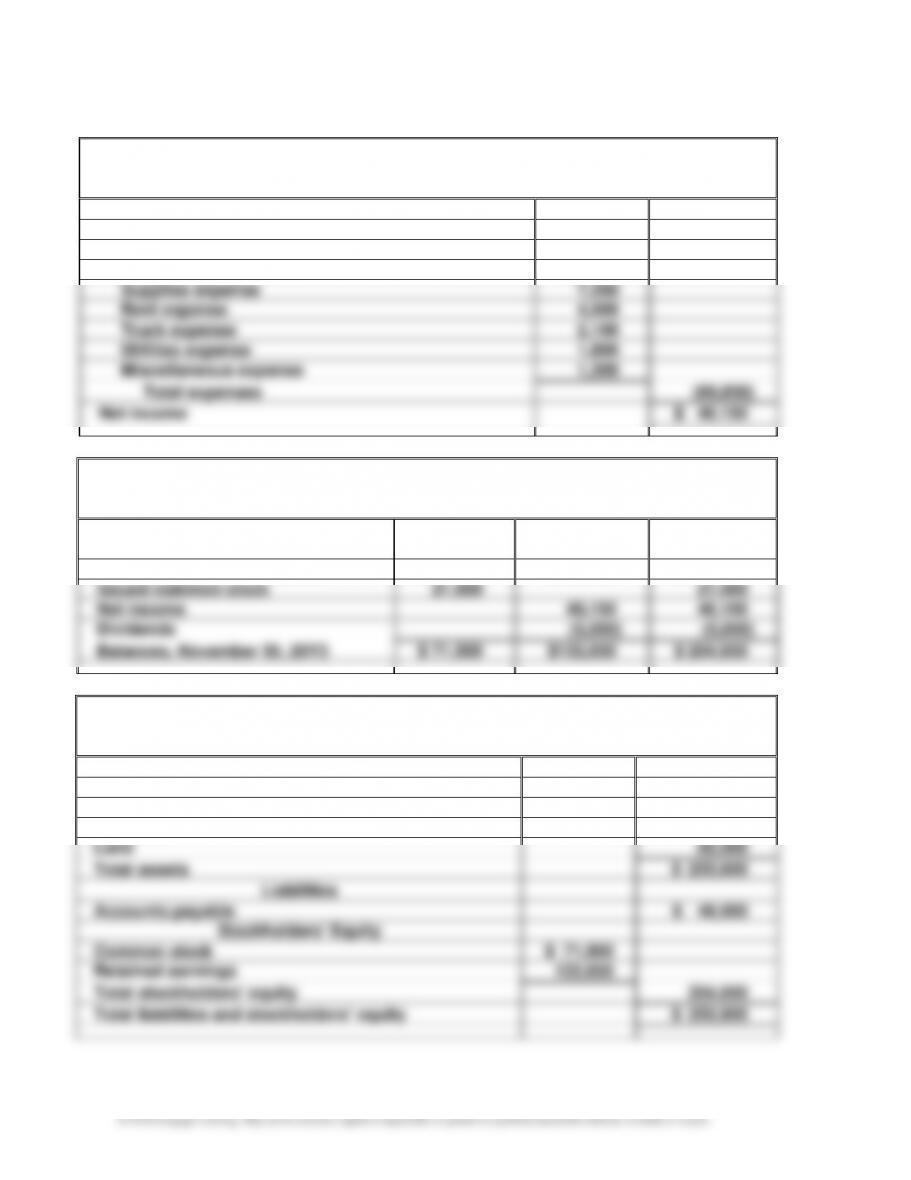

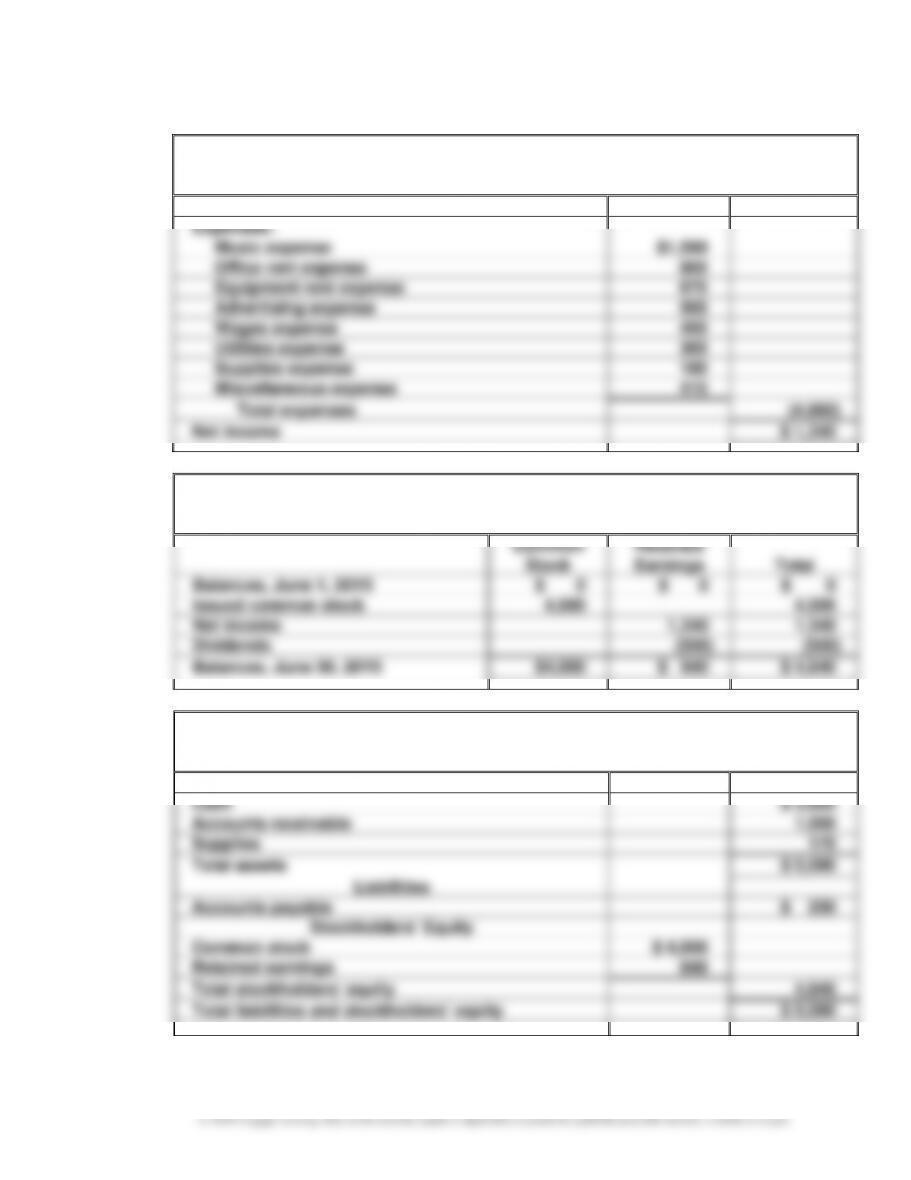

2.

PS Music

Income Statement

For the Month Ended June 30, 20Y5

Fees earned:

$ 6,200

Expenses:

Music expense

$1,590

Office rent expense

800

Equipment rent expense

675

Advertising expense

500

Wages expense

400

Utilities expense

300

Supplies expense

180

Miscellaneous expense

415

Total expenses

(4,860)

Net income

$ 1,340

3.

PS Music

Statement of Stockholders’ Equity

For the Month Ended June 30, 20Y5

Common

Stock

Retained

Earnings

Total

Balances, June 1, 20Y5

$ 0

$ 0

$ 0

Issued common stock

4,000

4,000

Net income

1,340

1,340

Dividends

(500)

(500)

Balances, June 30, 20Y5

$4,000

$ 840

$ 4,840

4.

PS Music

Balance Sheet

June 30, 20Y5

Assets

Cash

$ 3,920

Accounts receivable

1,000

Supplies

170

Total assets

$ 5,090

Liabilities

Accounts payable

$ 250

Stockholders’ Equity

Common stock

$ 4,000

Retained earnings

840

Total stockholders’ equity

4,840

Total liabilities and stockholders’ equity

$ 5,090

CHAPTER 1 Introduction to Accounting and Business

MAKE A DECISION

MAD 1–1

a.

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde to sLiabilitie of Ratio =

3.84

$13,384

$51,363

:Amazon =

2.09

$4,378

$9,141

:BuyBest =

b. Amazon’s ratio is 3.84, which means the total liabilities are almost four times as great as

MAD 1–2

a.

Equityrs’Stockholde Total

sLiabilitie Total

Equityrs’Stockholde to sLiabilitie of Ratio =

5.74

$6,316

$36,233

:3 Year

3.29

$9,322

$30,624

:2 Year

2.24

$12,522

$27,996

:1 Year

=

=

=

b. The ratio of liabilities to stockholders’ equity for Home Depot increased from 2.24 in Year 1

1–43

MAD 1–3

a.

Equityrs’Stockholde Total

sLiabilitie Total

Equityrs’Stockholde to sLiabilitie of Ratio =

3.08

$7,654

$23,612

:3 Year

2.18

$9,968

$21,753

:2 Year

1.76

$11,853

$20,879

:1 Year

=

=

=

b. The ratio of liabilities to stockholders’ equity for Lowe’s increased from 1.76 in Year 1 to

3.08 in Year 3, causing the margin of protection to creditors to decrease. This is a

significant increase in this ratio for the three-year period.

MAD 1–4

The ratios of liabilities to stockholders’ equity are summarized below for Home Depot (MAD 1–2)

and Lowe’s (MAD 1–3).

Year 3

Year 2

Year 1

Home Depot

5.74

3.29

2.24

Lowe’s

3.08

2.18

1.76

Lowe’s ratio of liabilities to stockholders’ equity is less than that of Home Depot for all three

years. Thus, the risk to Lowe’s creditors is less than that of Home Depot’s creditors. The

three-year trend for both companies shows that the size of this ratio is increasing. However,

Home Depot appears to be more aggressive than Lowe’s in its use of debt.

CHAPTER 1 Introduction to Accounting and Business

1–44

MAD 1–5

a. Ratio of Liabilities to Stockholders’ Equity =

Equityrs’Stockholde Total

sLiabilitie Total

8.7

$51

$444

:sJohn‘ Papa =

7.9

$911

$7,164

:Brands Yum! =

b. The ratio of liabilities to stockholders’ equity is 8.7 for Papa John’s and 7.9 for Yum!

c. Papa John’s ratio of liabilities to stockholders’ equity of 8.7 is higher than that of Yum!

CHAPTER 1 Introduction to Accounting and Business

1–45

TAKE IT FURTHER

TIF 1–1

1. The car repair is a personal expense and is Marco’s personal responsibility. By

using partnership funds to pay for the repair, Marco is behaving unethically because

CHAPTER 1 Introduction to Accounting and Business

1–46

TIF 1–2

1. Acceptable professional conduct requires that Colleen Fernandez supply First Federal

Bank with all the relevant financial statements necessary for the bank to make an

2. a. Owners are generally willing to provide bankers with information about the operating

and financial condition of the business, such as the following:

• Operating Information:

• Description of business operations

• Financial Condition:

• List of assets and liabilities (balance sheet)

Owners are normally reluctant to provide the following types of information to

bankers:

• Proprietary Operating Information. Such information, which might hurt the

significantly affect the owner’s personal wealth.

b. Bankers typically want as much information as possible about the ability of the

business and the owner to repay the loan with interest. Examples of such information

are described above.

c. Both bankers and business owners share the common interest of the business doing

CHAPTER 1 Introduction to Accounting and Business

TIF 1–3

A sample solution based on Twitter’s Form 10-K for the fiscal year ended

December 31, 2016, follows:

2. San Francisco, CA

4. Service

5. Twitter is a global platform for public self-expression and conversation in real time.

6. Balance sheet, statement of operations (income statement), statement of comprehensive

TIF 1–4

Example Memo

To: Teacher

From: Student

TIF 1–5

The difference in the two bank balances, $55,000 ($80,000 – $25,000), may not be pure profit from

an accounting perspective. To determine the accounting profit for the six-month period, the

revenues for the period would need to be matched with the related expenses. The revenues