1–1

CHAPTER 1

INTRODUCTION TO ACCOUNTING AND BUSINESS

DISCUSSION QUESTIONS

2. The role of accounting is to provide information for managers to use in operating the business. In addition,

3. The corporate form allows the company to obtain large amounts of resources by issuing stock. For this

4. No. The business entity assumption limits the recording of economic data to transactions directly affecting

5. The land should be recorded at its cost of $167,500 to Reliable Repair Service. This is consistent with the

cost principle.

6. a. No. The offer of $2,000,000 and the increase in the assessed value should not be recognized in the

7. An account receivable is a claim against a customer for goods or services sold. An account payable is an

9. (a) The business incurred a net loss of $75,000 ($640,000 – $715,000).

10. (a) Net income or net loss

CHAPTER 1 Introduction to Accounting and Business

BASIC EXERCISES

BE 1–1

BE 1–2

a.

A

=

L + SE

$395,000

=

$97,000

SE

=

$298,000

b.

A

=

L + SE

–$65,000

=

$36,000

SE

=

–$101,000

SE on December 31, 20Y2

=

$298,000

SE on December 31, 20Y3

=

$197,000

BE 1–3

(3) Asset (Supplies) increases by $2,100;

Liability (Accounts Payable) increases by $2,100.

BE 1–4

Paradise Travel Service

Income Statement

For the Year Ended May 31, 20Y6

Fees earned

$ 900,000

Expenses:

Wages expense

$450,000

Office expense

300,000

Miscellaneous expense

15,000

Total expenses

(765,000)

Net income

$ 135,000

1–3

BE 1–5

Paradise Travel Service

Statement of Stockholders’ Equity

For the Year Ended May 31, 20Y6

Common

Stock

Retained

Earnings

Total

Balances, June 1, 20Y5

$ 60,000

$300,000

$360,000

Issued common stock

40,000

40,000

Net income

135,000

135,000

Dividends

(10,000)

(10,000)

Balances, May 31, 20Y6

$100,000

$425,000

$525,000

BE 1–6

Paradise Travel Service

Balance Sheet

May 31, 20Y6

Assets

Cash

$ 52,000

Accounts receivable

38,000

Supplies

3,000

Land

450,000

Total assets

$ 543,000

Liabilities

Accounts payable

$ 18,000

Stockholders’ Equity

Common stock

$100,000

Retained earnings

425,000

Total stockholders’ equity

525,000

Total liabilities and stockholders’ equity

$ 543,000

CHAPTER 1 Introduction to Accounting and Business

1–4

BE 1–7

Paradise Travel Service

Statement of Cash Flows

For the Year Ended May 31, 20Y6

Cash flows from (used for) operating activities:

Cash received from customers

$ 880,000

Cash paid for operating expenses

(758,000)

Net cash flows from operating activities

$ 122,000

Cash flows from (used for) investing activities:

Cash paid for purchase of land

(150,000)

Cash flows from (used for) financing activities:

Cash received from issuing common stock

$ 40,000

Cash paid for dividends

(10,000)

Net cash flows from financing activities

30,000

Net increase in cash

$ 2,000

Cash balance, June 1, 20Y5

50,000

Cash balance, May 31, 20Y6

$ 52,000

BE 1–8

a.

Dec. 31,

20Y4

Dec. 31,

20Y3

Total liabilities …………………………………………………..

Total stockholders’ equity ………………………………….

Ratio of liabilities to stockholders’ equity ……………

$4,085,000

$4,300,000

0.95*

$2,880,000

$3,600,000

0.80**

* $4,085,000 ÷ $4,300,000

** $2,880,000 ÷ $3,600,000

b.

Increased

CHAPTER 1 Introduction to Accounting and Business

1–5

EXERCISES

Ex. 1–1

a.

1.

manufacturing

6.

manufacturing

11.

service

2.

manufacturing

7.

service

12.

service

3.

manufacturing

8.

service

13.

manufacturing

4.

service

9.

manufacturing

14.

service

5.

retail

10.

retail

15.

retail

accounting information system.

Ex. 1–2

As in many ethics issues, there is no one right answer. Oftentimes, disclosing only what is

Ex. 1–3

a.

1.

M

5.

O

9.

X

2.

L

6.

O

10.

O

3.

O

7.

X

4.

M

8.

L

financial condition or results of operations.

Ex. 1–4

Ex. 1–5

CHAPTER 1 Introduction to Accounting and Business

1–6

Ex. 1–6

Ex. 1–7

a. $3,650,000 ($5,250,000 – $1,600,000)

Ex. 1–8

a. (2) liability

f. (3) stockholders’ equity (expense)

Ex. 1–9

a. Increases assets and increases stockholders’ equity.

Ex. 1–10

a. (1) Total assets increased $183,000 ($298,000 – $115,000).

(3) Stockholders’ equity increased $183,000.

b. (1) Total assets decreased $80,000.

CHAPTER 1 Introduction to Accounting and Business

1–7

Ex. 1–11

1.

(a) increase

2.

(a) increase

3.

(b) decrease

4.

(b) decrease

Ex. 1–12

1.

c

6.

c

2.

a

7.

d

3.

e

8.

a

4.

e

9.

e

5.

c

10.

e

Ex. 1–13

a. (1) Provided catering services for cash, $71,800.

b. $300 ($40,300 – $40,000)

Ex. 1–14

CHAPTER 1 Introduction to Accounting and Business

1–8

Ex. 1–15

Amber

Stockholders’ equity at end of year ($1,730,000 – $1,150,000) …………………….

$ 580,000

Deduct stockholders’ equity at beginning of year ($1,220,000 – $990,000) ……….

(230,000)

Net income (increase in stockholders’ equity) ……………………………………….

$ 350,000

Blue

Increase in stockholders’ equity (as determined for Amber) ………………………

$ 350,000

Add dividends …………………………………………………………………………………………

60,000

Net income ………………………………………………………………………………………….

$ 410,000

Coral

Increase in stockholders’ equity (as determined for Amber) ………………………

$ 350,000

Deduct additional issuance of common stock …………………………………………..

(140,000)

Net income ………………………………………………………………………………………….

$ 210,000

Daffodil

Increase in stockholders’ equity (as determined for Amber) ………………………

$ 350,000

Deduct additional issuance of common stock …………………………………………..

(140,000)

$ 210,000

Add dividends …………………………………………………………………………………………

60,000

Net income ………………………………………………………………………………………….

$ 270,000

Ex. 1–16

Ex. 1–17

CHAPTER 1 Introduction to Accounting and Business

1–9

Ex. 1–18

a.

Organic Products Company

Statement of Stockholders’ Equity

For the Month Ended June 30, 20Y9

Common

Stock

Retained

Earnings

Total

Balances, June 1, 20Y9

$180,000

$1,630,000

$1,810,000

Issued common stock

50,000

50,000

Net income

115,000

115,000

Dividends

(25,000)

(25,000)

Balances, June 30, 20Y9

$230,000

$1,720,000

$1,950,000

b. The statement of stockholders’ equity is prepared before the June 30, 20Y9, balance sheet

Ex. 1–19

Imaging Services

Income Statement

For the Month Ended March 31, 20Y5

Fees earned

$ 482,000

Expenses:

Wages expense

$300,000

Rent expense

41,500

Supplies expense

3,600

Miscellaneous expense

1,900

Total expenses

(347,000)

Net income

$ 135,000

CHAPTER 1 Introduction to Accounting and Business

1–10

Ex. 1–20

In each case, solve for a single unknown, using the following equation:

Stockholders’ Equity (beginning) + Additional Common Stock Issued – Dividends +

Revenues – Expenses = Stockholders’ Equity (ending)

Freeman

Stockholders’ equity at end of year ($1,260,000 – $330,000) ……………………..

$ 930,000

Stockholders’ equity at beginning of year ($900,000 – $360,000) ……………….

(540,000)

Increase in stockholders’ equity ……………………………………………………….

$ 390,000

Deduct increase due to net income ($570,000 – $240,000) …………………………

(330,000)

$ 60,000

Add dividends ……………………………………………………………………………………

75,000

Additional common stock issued ……………………………………………………….

(a)

$ 135,000

Heyward

Stockholders’ equity at end of year ($675,000 – $220,000) ………………………..

$ 455,000

Stockholders’ equity at beginning of year ($490,000 – $260,000) ……………….

(230,000)

Increase in stockholders’ equity ……………………………………………………….

$ 225,000

Add dividends ……………………………………………………………………………………

32,000

$ 257,000

Deduct additional common stock issued …………………………………………………

(150,000)

Increase due to net income …………………………………………………………………….

$ 107,000

Add expenses ……………………………………………………………………………………

128,000

Revenue …………………………………………………………………………………………….

(b)

$ 235,000

Jones

Stockholders’ equity at end of year ($100,000 – $80,000) ………………………….

$ 20,000

Stockholders’ equity at beginning of year ($115,000 – $81,000) …………………

(34,000)

Decrease in stockholders’ equity ……………………………………………………….

$ (14,000)

Decrease in stockholders’ equity due to net loss ……………………………………..

($115,000 – $122,500) …………………………..……………………………………………..

7,500

$ (6,500)

Deduct common stock issued …………………………………………………………………

(10,000)

Dividends ……………………………………………………………………………………

(c)

$ (16,500)

Ramirez

Stockholders’ equity at end of year ($270,000 – $136,000) ………………………..

$ 134,000

Add decrease due to net loss ($115,000 – $128,000) …………………………..

13,000

$ 147,000

Add dividends ……………………………………………………………………………………

39,000

Stockholders’ equity at beginning of year ……………………………………………….

$ 186,000

Deduct additional investment …………………………………………………………………

(55,000)

$ 131,000

Add liabilities at beginning of year ……………………………………………………….

120,000

Assets at beginning of year ………………………………………………………………..

(d)

$ 251,000

CHAPTER 1 Introduction to Accounting and Business

1–11

Ex. 1–21

a.

Ebony Interiors

Balance Sheet

February 28, 20Y3

Assets

Cash

$ 320,000

Accounts receivable

800,000

Supplies

30,000

Total assets

$1,150,000

Liabilities

Accounts payable

$ 310,000

Stockholders’ Equity

Common stock

$200,000

Retained earnings

640,000*

Total stockholders’ equity

840,000

Total liabilities and stockholders’ equity

$1,150,000

* $640,000 = $320,000 + $800,000 + $30,000 – $310,000 – $200,000

Ebony Interiors

Balance Sheet

March 31, 20Y3

Assets

Cash

$ 380,000

Accounts receivable

960,000

Supplies

35,000

Total assets

$1,375,000

Liabilities

Accounts payable

$ 400,000

Stockholders’ Equity

Common stock

$200,000

Retained earnings

775,000*

Total stockholders’ equity

975,000

Total liabilities and stockholders’ equity

$1,375,000

* $775,000 = $380,000 + $960,000 + $35,000 – $400,000 – $200,000

CHAPTER 1 Introduction to Accounting and Business

1–12

Ex. 1–21 (Concluded)

c. Stockholders’ equity, March 31 …………………………………………………………… $ 975,000

Stockholders’ equity, February 28 ……………………………………………………….. (840,000)

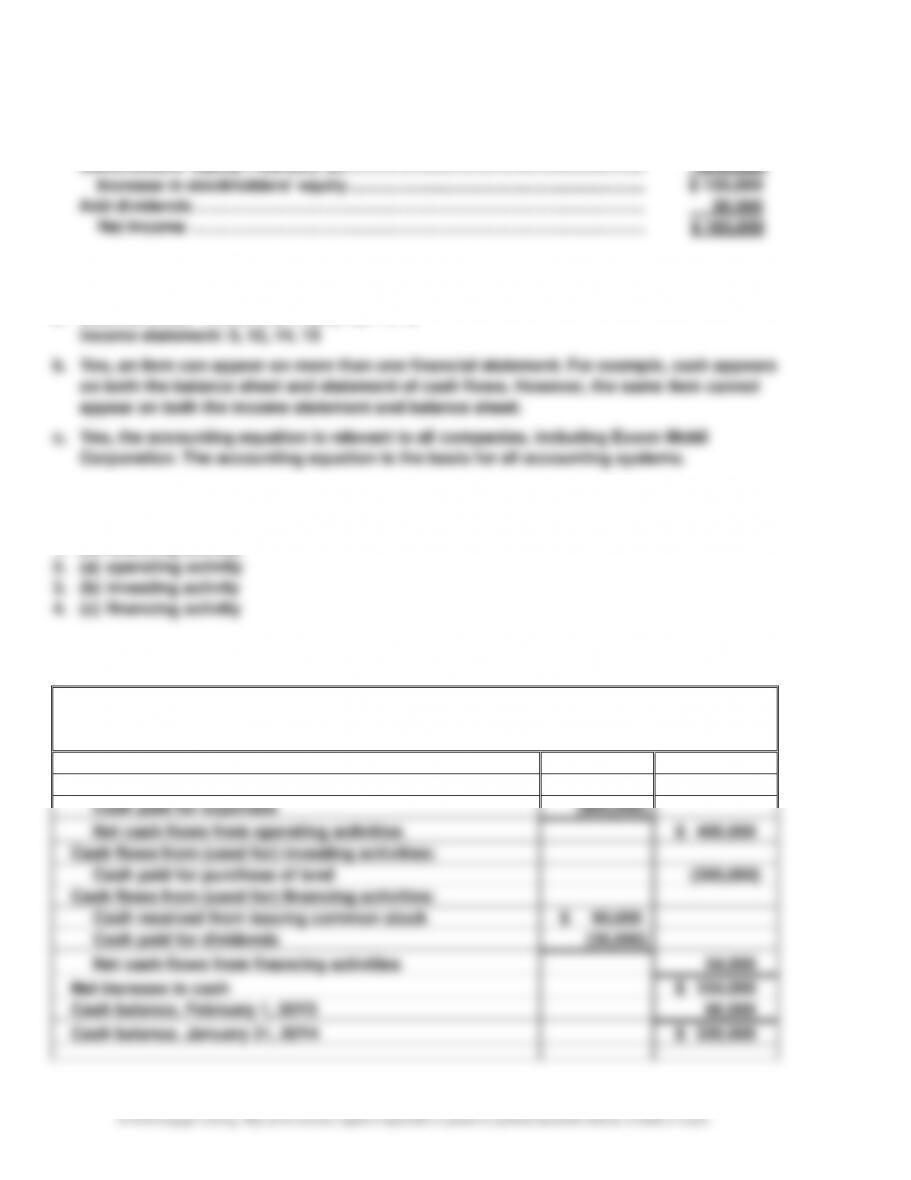

Ex. 1–22

a. Balance sheet: 1, 2, 3, 4, 6, 7, 8, 9, 10, 11, 13

Ex. 1–23

1. (c) financing activity

Ex. 1–24

Parker Consulting Group

Statement of Cash Flows

For the Year Ended January 31, 20Y4

Cash flows from (used for) operating activities:

Cash received from customers

$1,200,000

Cash paid for expenses

(800,000)

Net cash flows from operating activities

$ 400,000

Cash flows from (used for) investing activities:

Cash paid for purchase of land

(300,000)

Cash flows from (used for) financing activities:

Cash received from issuing common stock

$ 90,000

Cash paid for dividends

(36,000)

Net cash flows from financing activities

54,000

Net increase in cash

$ 154,000

Cash balance, February 1, 20Y3

66,000

Cash balance, January 31, 20Y4

$ 220,000

CHAPTER 1 Introduction to Accounting and Business

1–13

Ex. 1–25

a. 1. All financial statements should contain the name of the business in their heading. The

3. The year in the heading for the statement of stockholders’ equity should be 20Y7

rather than 20Y6.

5. On the income statement, the miscellaneous expense amount should be listed as the

last expense.

6. On the income statement, the total expenses are subtracted from the sales

8. Accounts payable should be listed as a liability on the balance sheet.

CHAPTER 1 Introduction to Accounting and Business

1–14

Ex. 1–25 (Concluded)

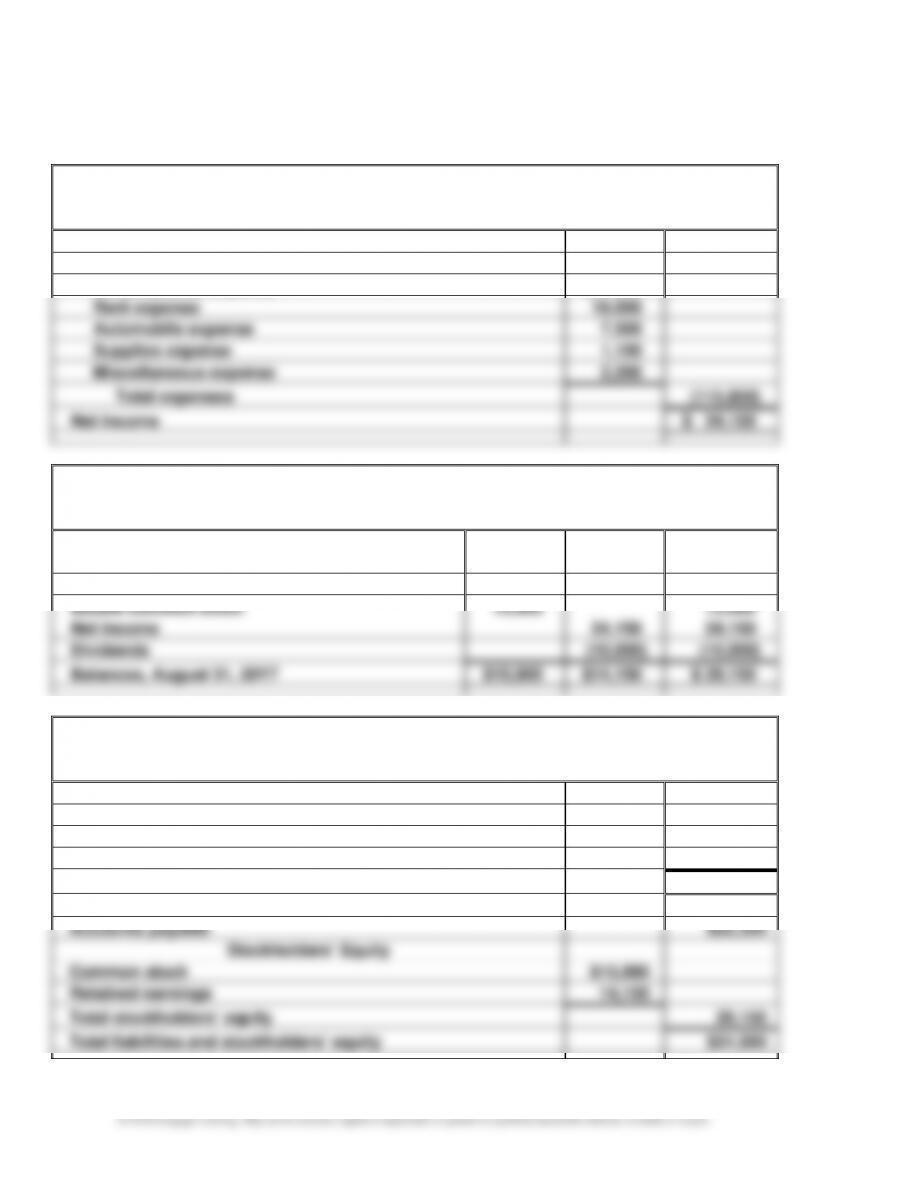

b. Corrected financial statements appear as follows:

We-Sell Realty

Income Statement

For the Month Ended August 31, 20Y7

Sales commissions

$ 140,000

Expenses:

Office salaries expense

$87,000

Rent expense

18,000

Automobile expense

7,500

Supplies expense

1,150

Miscellaneous expense

2,200

Total expenses

(115,850)

Net income

$ 24,150

We-Sell Realty

Statement of Stockholders’ Equity

For the Month Ended August 31, 20Y7

Common

Stock

Retained

Earnings

Total

Balances, August 1, 20Y7

$ 0

$ 0

$ 0

Issued common stock

15,000

15,000

Net income

24,150

24,150

Dividends

(10,000)

(10,000)

Balances, August 31, 20Y7

$15,000

$14,150

$ 29,150

We-Sell Realty

Balance Sheet

August 31, 20Y7

Assets

Cash

$ 8,900

Accounts receivable

38,600

Supplies

4,000

Total assets

$51,500

Liabilities

Accounts payable

$22,350

Stockholders’ Equity

Common stock

$15,000

Retained earnings

14,150

Total stockholders’ equity

29,150

Total liabilities and stockholders’ equity

$51,500

CHAPTER 1 Introduction to Accounting and Business

1–15

PROBLEMS

Prob. 1–1A

1.

Assets

=

Liabilities +

Stockholders’ Equity

Cash

+

Accts.

Rec.

+

Supplies

=

Accts.

Payable

+

Common

Stock

–

Dividends

+

Fees

Earned

–

Rent

Expense

–

Salaries

Expense

–

Supplies

Expense

–

Auto

Exp.

–

Misc.

Exp.

a.

b.

+ 60,000

+ 1,800

+ 1,800

+ 60,000

Bal.

c.

60,000

+ 22,300

1,800

1,800

60,000

+ 22,300

Bal.

d.

82,300

– 7,000

1,800

1,800

60,000

22,300

– 7,000

Bal.

e.

75,300

– 1,100

1,800

1,800

– 1,100

60,000

22,300

– 7,000

Bal.

f.

74,200

+ 3,600

1,800

700

60,000

22,300

+ 3,600

– 7,000

Bal.

g.

74,200

– 1,750

3,600

1,800

700

60,000

25,900

– 7,000

– 750

– 1,000

Bal.

h.

72,450

– 4,000

3,600

1,800

700

60,000

25,900

– 7,000

– 4,000

– 750

– 1,000

Bal.

i.

68,450

3,600

1,800

– 1,550

700

60,000

25,900

– 7,000

– 4,000

– 1,550

– 750

– 1,000

Bal.

j.

68,450

– 5,000

3,600

250

700

60,000

– 5,000

25,900

– 7,000

– 4,000

– 1,550

– 750

– 1,000

Bal.

63,450

3,600

250

700

60,000

– 5,000

25,900

– 7,000

– 4,000

– 1,550

– 750

– 1,000

2. Stockholders’ equity is the right of stockholders (owners) to the assets of the business. These rights are increased by issuing common stock and

revenues and decreased by dividends and expenses.

CHAPTER 1 Introduction to Accounting and Business

1–16

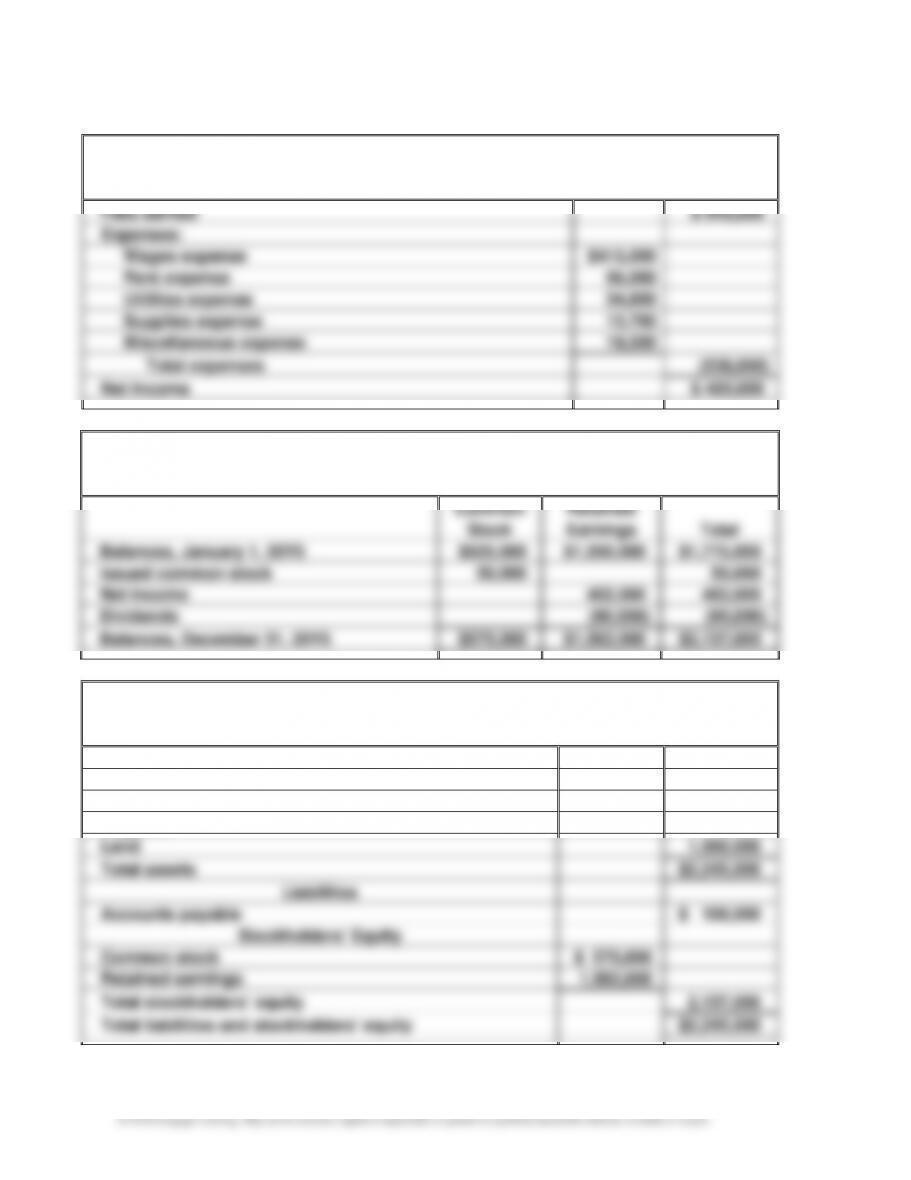

Prob. 1–2A

1.

Global Travel Agency

Income Statement

For the Year Ended December 31, 20Y5

Fees earned

$ 940,000

Expenses:

Wages expense

$415,000

Rent expense

56,000

Utilities expense

34,800

Supplies expense

12,700

Miscellaneous expense

19,500

Total expenses

(538,000)

Net income

$ 402,000

2.

Global Travel Agency

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y5

Common

Stock

Retained

Earnings

Total

Balances, January 1, 20Y5

$525,000

$1,250,000

$1,775,000

Issued common stock

50,000

50,000

Net income

402,000

402,000

Dividends

(90,000)

(90,000)

Balances, December 31, 20Y5

$575,000

$1,562,000

$2,137,000

3.

Global Travel Agency

Balance Sheet

December 31, 20Y5

Assets

Cash

$ 200,000

Accounts receivable

539,000

Supplies

6,000

Land

1,500,000

Total assets

$2,245,000

Liabilities

Accounts payable

$ 108,000

Stockholders’ Equity

Common stock

$ 575,000

Retained earnings

1,562,000

Total stockholders’ equity

2,137,000

Total liabilities and stockholders’ equity

$2,245,000

CHAPTER 1 Introduction to Accounting and Business

1–17

Prob. 1–2A (Concluded)

4. Ending common stock and retained earnings appear on both the statement of stockholders’

Prob. 1–3A

1.

Reliance Financial Services

Income Statement

For the Month Ended July 31, 20Y2

Fees earned

$144,500

Expenses:

Salaries expense

$55,000

Rent expense

33,000

Auto expense

16,000

Supplies expense

4,500

Miscellaneous expense

4,800

Total expenses

(113,300)

Net income

$ 31,200

2.

Reliance Financial Services

Statement of Stockholders’ Equity

For the Month Ended July 31, 20Y2

Common

Stock

Retained

Earnings

Total

Balances, July 1, 20Y2

$ 0

$ 0

$ 0

Issued common stock

50,000

50,000

Net income

31,200

31,200

Dividends

(15,000)

(15,000)

Balances, July 31, 20Y2

$50,000

$ 16,200

$ 66,200

CHAPTER 1 Introduction to Accounting and Business

1–18

Prob. 1–3A (Concluded)

3.

Reliance Financial Services

Balance Sheet

July 31, 20Y2

Assets

Cash

$32,600

Accounts receivable

34,500

Supplies

2,500

Total assets

$69,600

Liabilities

Accounts payable

$ 3,400

Stockholders’ Equity

Common stock

$50,000

Retained earnings

16,200

Total stockholders’ equity

66,200

Total liabilities and stockholders’ equity

$69,600

4. (Optional)

Reliance Financial Services

Statement of Cash Flows

For the Month Ended July 31, 20Y2

Cash flows from (used for) operating activities:

Cash received from customers

$ 110,000

Cash paid for expenses

and to creditors*

(112,400)

Net cash flows used for operating activities

$ (2,400)

Cash flows from (used for) investing activities

0

Cash flows from (used for) financing activities:

Cash received from issuing common stock

$ 50,000

Cash paid for dividends

(15,000)

Net cash flows from financing activities

35,000

Net increase in cash

$32,600

Cash balance, July 1, 20Y2

0

Cash balance, July 31, 20Y2

$32,600

* $3,600 + $33,000 + $20,800 + $55,000; these amounts are taken from the Cash column

shown in the problem.

CHAPTER 1 Introduction to Accounting and Business

1–19

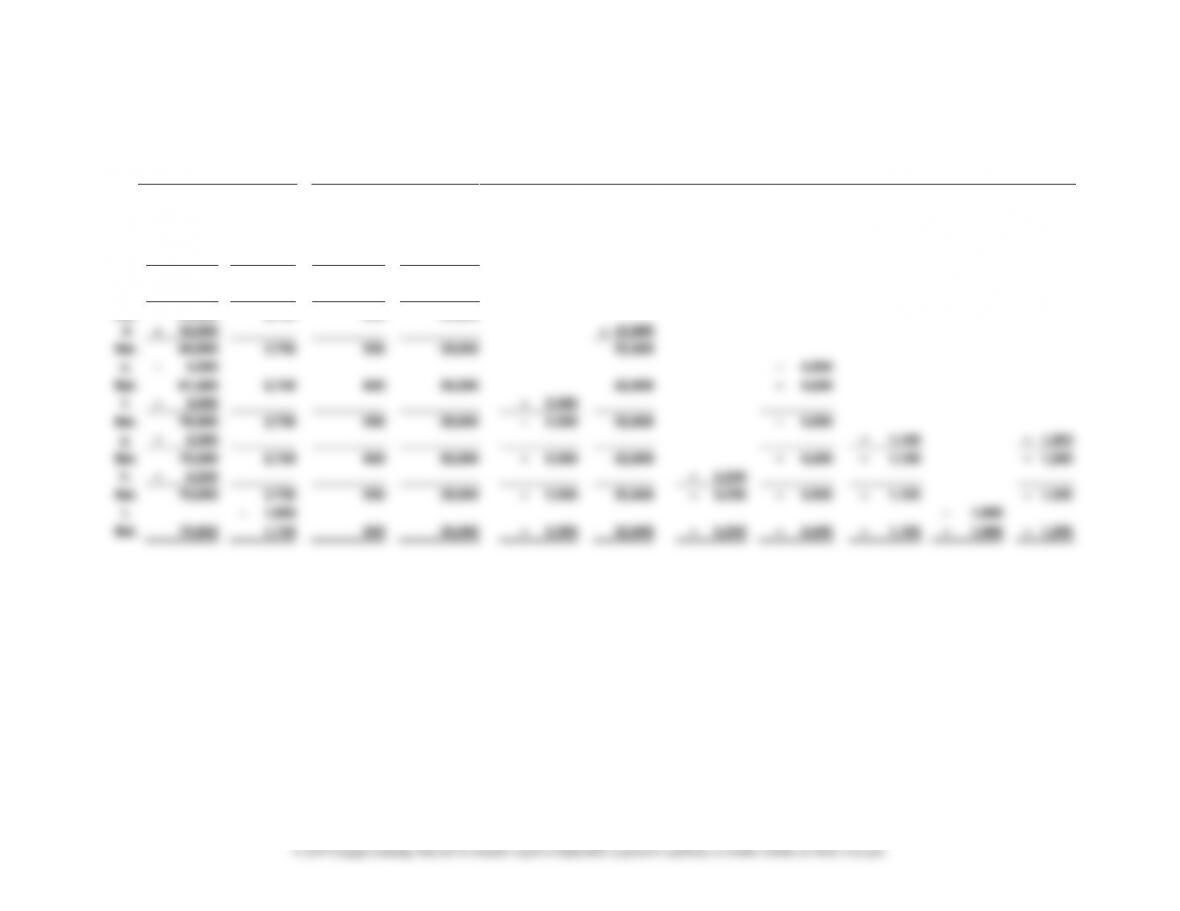

Prob. 1–4A

1.

Assets

=

Liabilities +

Stockholders’ Equity

Cash

+

Supplies

=

Accts.

Payable

+

Common

Stock

–

Dividends

+

Sales

Comm.

–

Salaries

Exp.

–

Rent

Exp.

–

Auto

Exp.

–

Supplies

Exp.

–

Misc.

Exp.

a.

b.

+ 35,000

+ 2,750

+ 2,750

+ 35,000

Bal.

c.

35,000

– 1,800

2,750

2,750

– 1,800

35,000

Bal.

d.

33,200

+ 52,800

2,750

950

35,000

+ 52,800

Bal.

e.

86,000

– 4,500

2,750

950

35,000

52,800

– 4,500

Bal.

f.

81,500

– 3,000

2,750

950

35,000

– 3,000

52,800

– 4,500

Bal.

g.

78,500

– 2,300

2,750

950

35,000

– 3,000

52,800

– 4,500

– 1,100

– 1,200

Bal.

h.

76,200

– 5,250

2,750

950

35,000

– 3,000

52,800

– 5,250

– 4,500

– 1,100

– 1,200

Bal.

i.

70,950

2,750

– 1,000

950

35,000

– 3,000

52,800

– 5,250

– 4,500

– 1,100

– 1,000

– 1,200

Bal.

70,950

1,750

950

35,000

– 3,000

52,800

– 5,250

– 4,500

– 1,100

– 1,000

– 1,200

CHAPTER 1 Introduction to Accounting and Business

1–20

Prob. 1–4A (Concluded)

2.

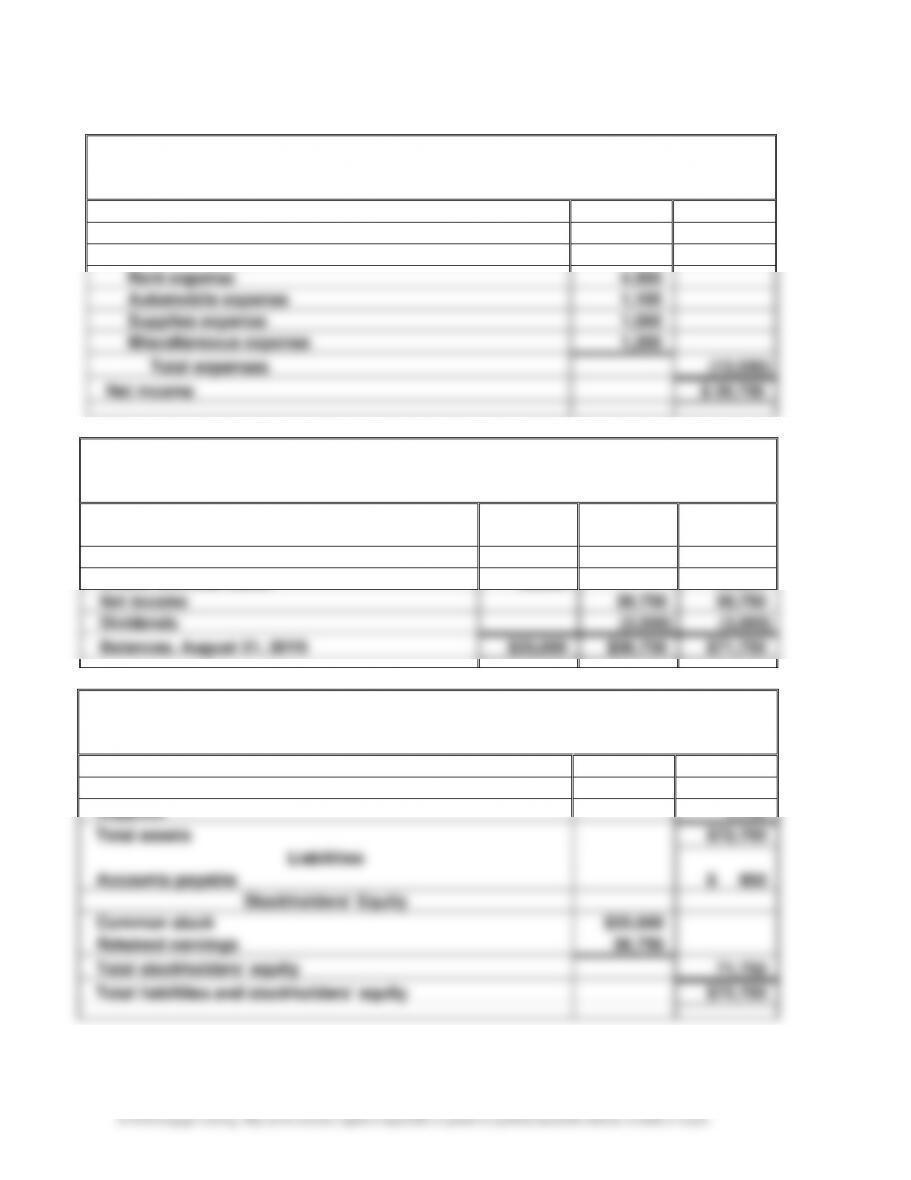

Western Realty

Income Statement

For the Month Ended August 31, 20Y9

Sales commissions

$ 52,800

Expenses:

Salaries expense

$5,250

Rent expense

4,500

Automobile expense

1,100

Supplies expense

1,000

Miscellaneous expense

1,200

Total expenses

(13,050)

Net income

$ 39,750

Western Realty

Statement of Stockholders’ Equity

For the Month Ended August 31, 20Y9

Common

Stock

Retained

Earnings

Total

Balances, August 1, 20Y9

$ 0

$ 0

$ 0

Issued common stock

35,000

35,000

Net income

39,750

39,750

Dividends

(3,000)

(3,000)

Balances, August 31, 20Y9

$35,000

$36,750

$71,750

Western Realty

Balance Sheet

August 31, 20Y9

Assets

Cash

$70,950

Supplies

1,750

Total assets

$72,700

Liabilities

Accounts payable

$ 950

Stockholders’ Equity

Common stock

$35,000

Retained earnings

36,750

Total stockholders’ equity

71,750

Total liabilities and stockholders’ equity

$72,700