Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

D-1

APPENDIX D

INVESTMENTS

EXERCISES

Ex. D–1

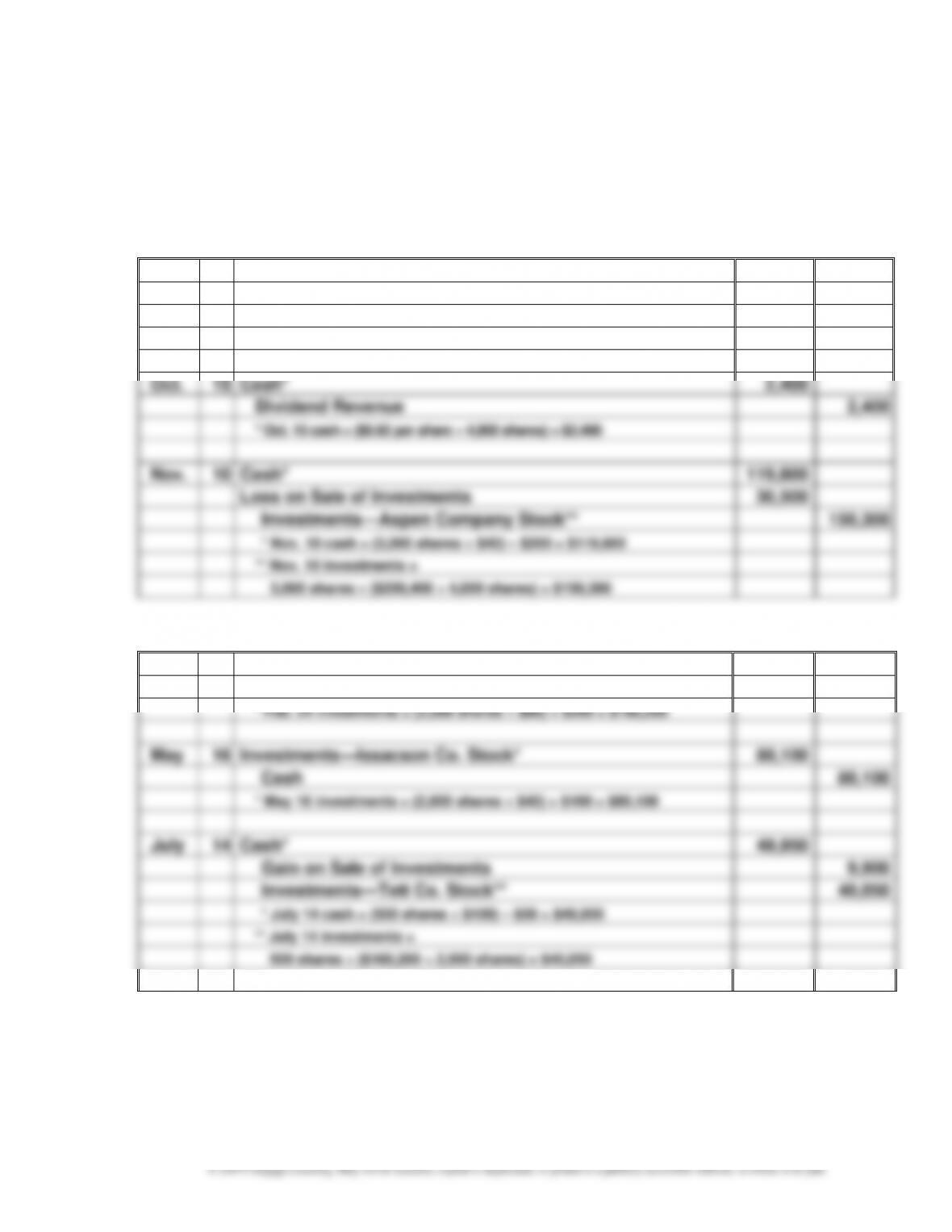

Sept.

12

Investments—Aspen Company Stock*

200,400

Cash

200,400

* Sept. 12 investments =

(4,000 shares $50 per share) + $400 = $200,400

Oct.

15

Cash*

2,400

Dividend Revenue

2,400

* Oct. 15 cash = ($0.60 per share 4,000 shares) = $2,400

Nov.

10

Cash*

119,800

Loss on Sale of Investments

30,500

Investments—Aspen Company Stock**

150,300

* Nov. 10 cash = (3,000 shares $40) – $200 = $119,800

** Nov. 10 investments =

3,000 shares ($200,400 ÷ 4,000 shares) = $150,300

Ex. D–2

Feb.

24

Investments—Tett Co. Stock*

160,200

Cash

160,200

* Feb. 24 investments = (2,000 shares $80) + $200 = $160,200

May

16

Investments—Issacson Co. Stock*

80,100

Cash

80,100

* May 16 investments = (2,000 shares $40) + $100 = $80,100

July

14

Cash*

49,950

Gain on Sale of Investments

9,900

Investments—Tett Co. Stock**

40,050

* July 14 cash = (500 shares $100) – $50 = $49,950

** July 14 investments =

500 shares ($160,200 ÷ 2,000 shares) = $40,050

APPENDIX D Investments

D-2

Ex. D–2 (Concluded)

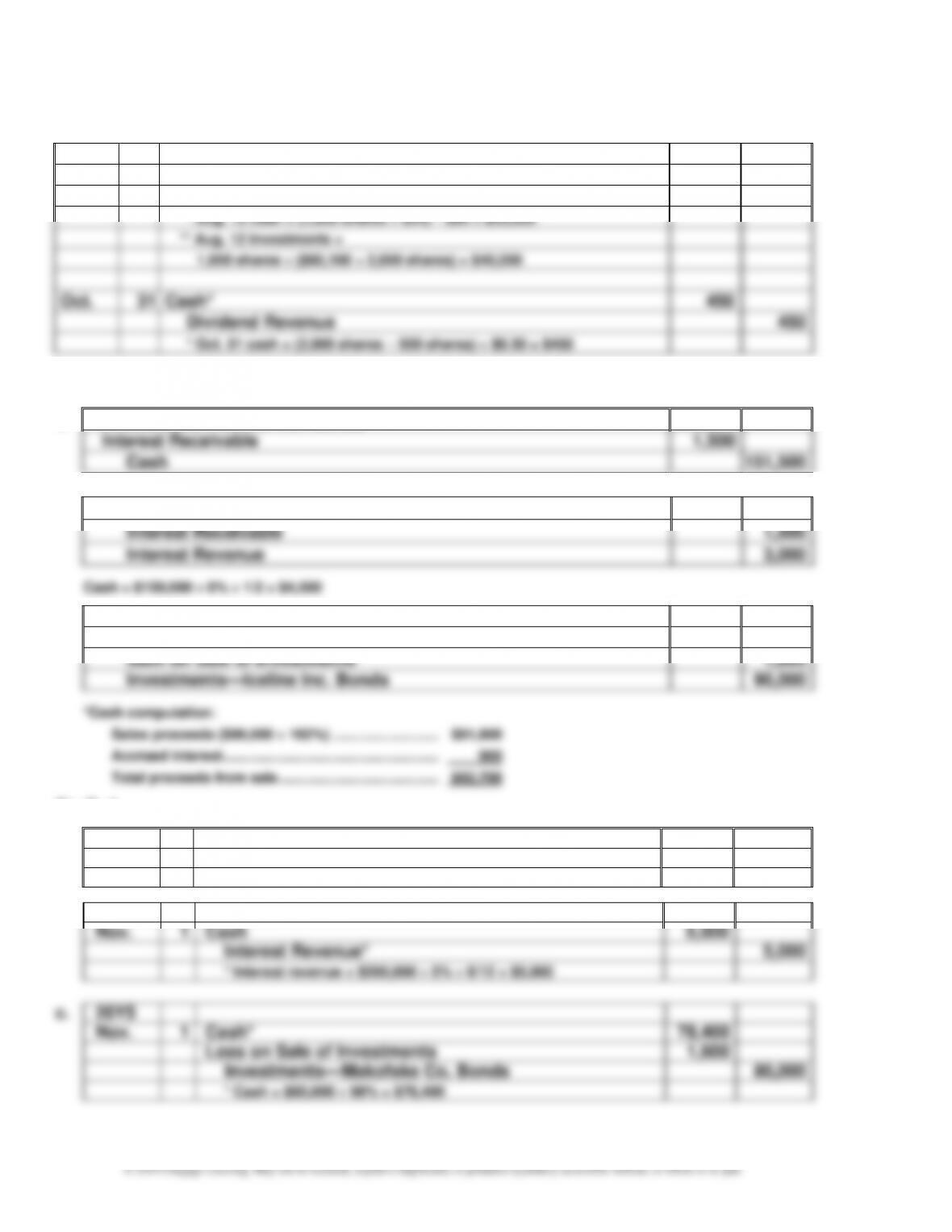

Aug.

12

Cash*

33,920

Loss on Sale of Investments

6,130

Investments—Issacson Co. Stock**

40,050

* Aug. 12 cash = (1,000 shares $34) – $80 = $33,920

** Aug. 12 investments =

1,000 shares ($80,100 ÷ 2,000 shares) = $40,050

Oct.

31

Cash*

450

Dividend Revenue

450

* Oct. 31 cash = (2,000 shares – 500 shares) $0.30 = $450

Ex. D–3

a.

Investments—Iceline Inc. Bonds

150,000

Interest Receivable

1,500

Cash

151,500

b.

Cash

4,500

Interest Receivable

1,500

Interest Revenue

3,000

c.

Cash*

92,700

Interest Revenue

900

Gain on Sale of Investments

1,800

Investments—Iceline Inc. Bonds

90,000

Ex. D–4

a.

20Y5

May

1

Investments—Makofske Co. Bonds

200,000

Cash

200,000

b.

20Y5

Nov.

1

Cash

5,000

Interest Revenue*

5,000

* Interest revenue = $200,000 5% 6/12 = $5,000

c.

20Y5

Nov.

1

Cash*

78,400

Loss on Sale of Investments

1,600

Investments—Makofske Co. Bonds

80,000

* Cash = $80,000 98% = $78,400

APPENDIX D Investments

D-3

Ex. D–4 (Concluded)

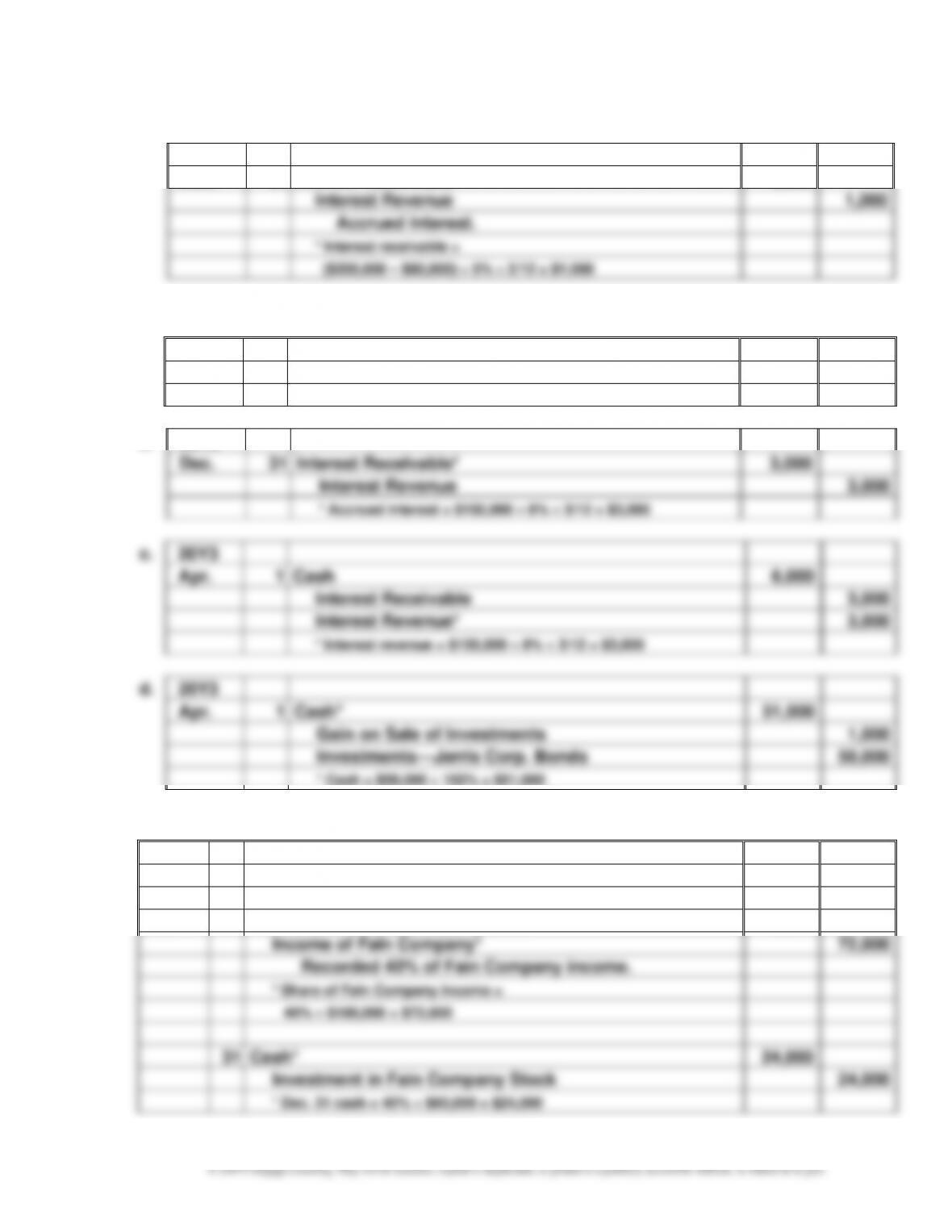

d.

20Y5

Dec.

31

Interest Receivable*

1,000

Interest Revenue

1,000

Accrued interest.

* Interest receivable =

($200,000 – $80,000) 5% 2/12 = $1,000

Ex. D–5

a.

20Y2

Oct.

1

Investments—Jerris Corp. Bonds

150,000

Cash

150,000

b.

20Y2

Dec.

31

Interest Receivable*

3,000

Interest Revenue

3,000

* Accrued interest = $150,000 8% 3/12 = $3,000

c.

20Y3

Apr.

1

Cash

6,000

Interest Receivable

3,000

Interest Revenue*

3,000

* Interest revenue = $150,000 8% 3/12 = $3,000

d.

20Y3

Apr.

1

Cash*

51,000

Gain on Sale of Investments

1,000

Investments—Jerris Corp. Bonds

50,000

* Cash = $50,000 102% = $51,000

Ex. D–6

Jan.

2

Investment in Fain Company Stock

800,000

Cash

800,000

Dec.

31

Investment in Fain Company Stock

72,000

Income of Fain Company*

72,000

Recorded 40% of Fain Company income.

* Share of Fain Company income =

40% $180,000 = $72,000

31

Cash*

24,000

Investment in Fain Company Stock

24,000

* Dec. 31 cash = 40% $60,000 = $24,000

APPENDIX D Investments

D-4

Ex. D–7

a.

20Y6

Jan.

4

Investment in Filington Co. Stock*

4,800,000

Cash

4,800,000

* Jan. 14 investment =

160,000 shares $30 per share = $4,800,000

July

2

Cash*

240,000

Investment in Filington Co. Stock

240,000

* Dividend =

$600,000 ($160,000 ÷ 400,000 shares) = $240,000

Dec.

31

Investment in Filington Co. Stock

480,000

Income of Filington Co.*

480,000

Record 40% share of Filington

Co. net income.

* Income = $1,200,000

(160,000 shares ÷ 400,000 shares) = $480,000

b. Initial acquisition cost ....................................................................................... $4,800,000

Equity earnings for 20Y6 ................................................................................... 480,000

Ex. D–8

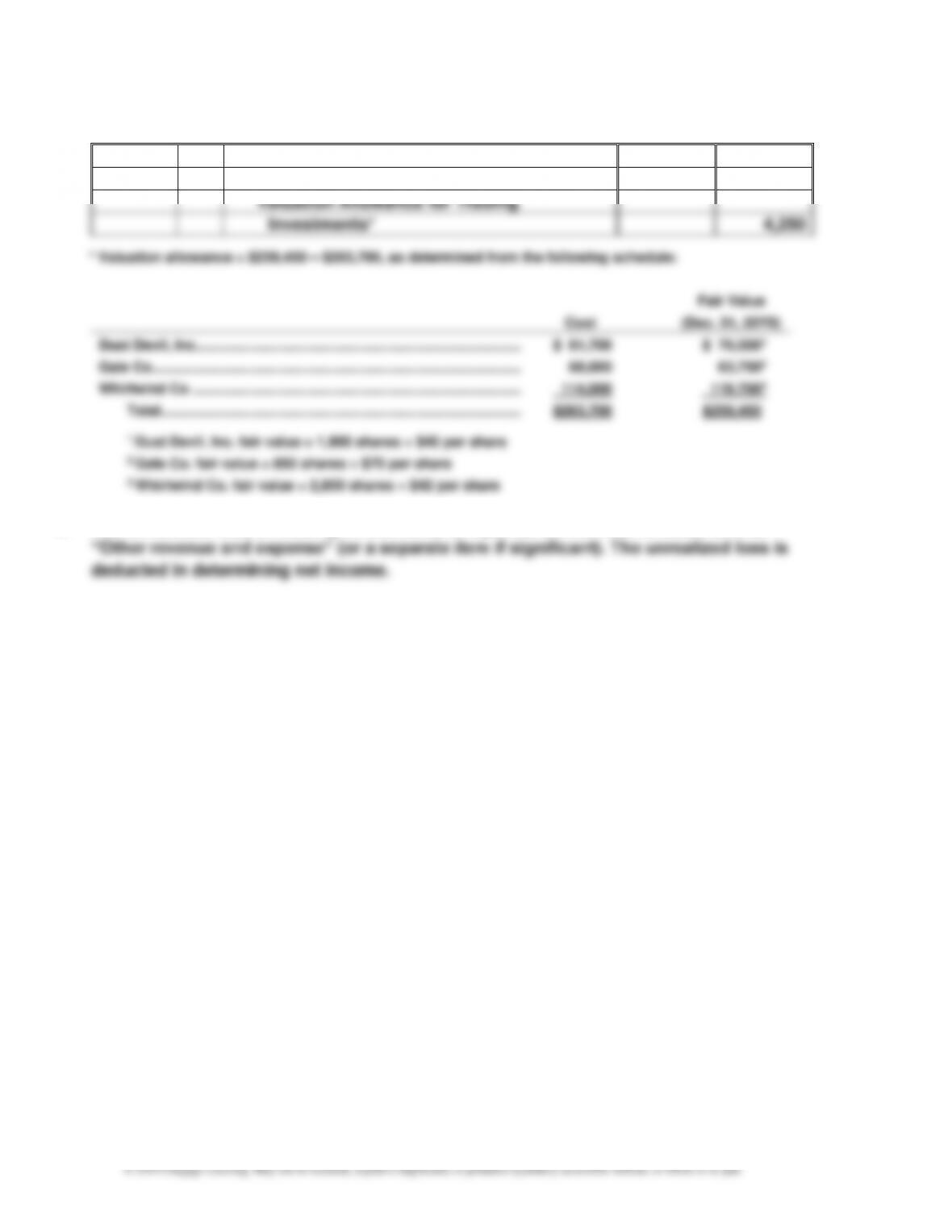

20Y9

Dec.

31

Valuation Allowance for Trading Investments*

5,900

Unrealized Gain on Trading Investments

5,900

To record increase in fair value of

trading investments.

APPENDIX D Investments

D-5

Ex. D–9

a.

20Y1

Feb.

24

Investments—Raiders Inc. Stock

851,000

Cash (18,500 shares $46 per share)

851,000

Dec.

31

Valuation Allowance for Trading Investments

111,000

Unrealized Gain on Trading Investments*

111,000

To record increase in fair value

of trading investments

* Unrealized gain = 18,500 shares

($52 per share – $46 per share) = $111,000

b. The unrealized gain or unrealized loss for trading investments is reported on the income

Ex. D–10

20Y3

Dec.

31

Unrealized Loss on Trading Investments

2,200

Valuation Allowance for Trading Investments

2,200

To record decrease in fair value

of trading investments.

APPENDIX D Investments

D-6

Ex. D–11

a.

20Y9

Dec.

31

Unrealized Loss on Trading Investments

4,250

Valuation Allowance for Trading

Investments*

4,250

b. The unrealized loss on trading investments is reported on the income statement as

APPENDIX D Investments

D-7

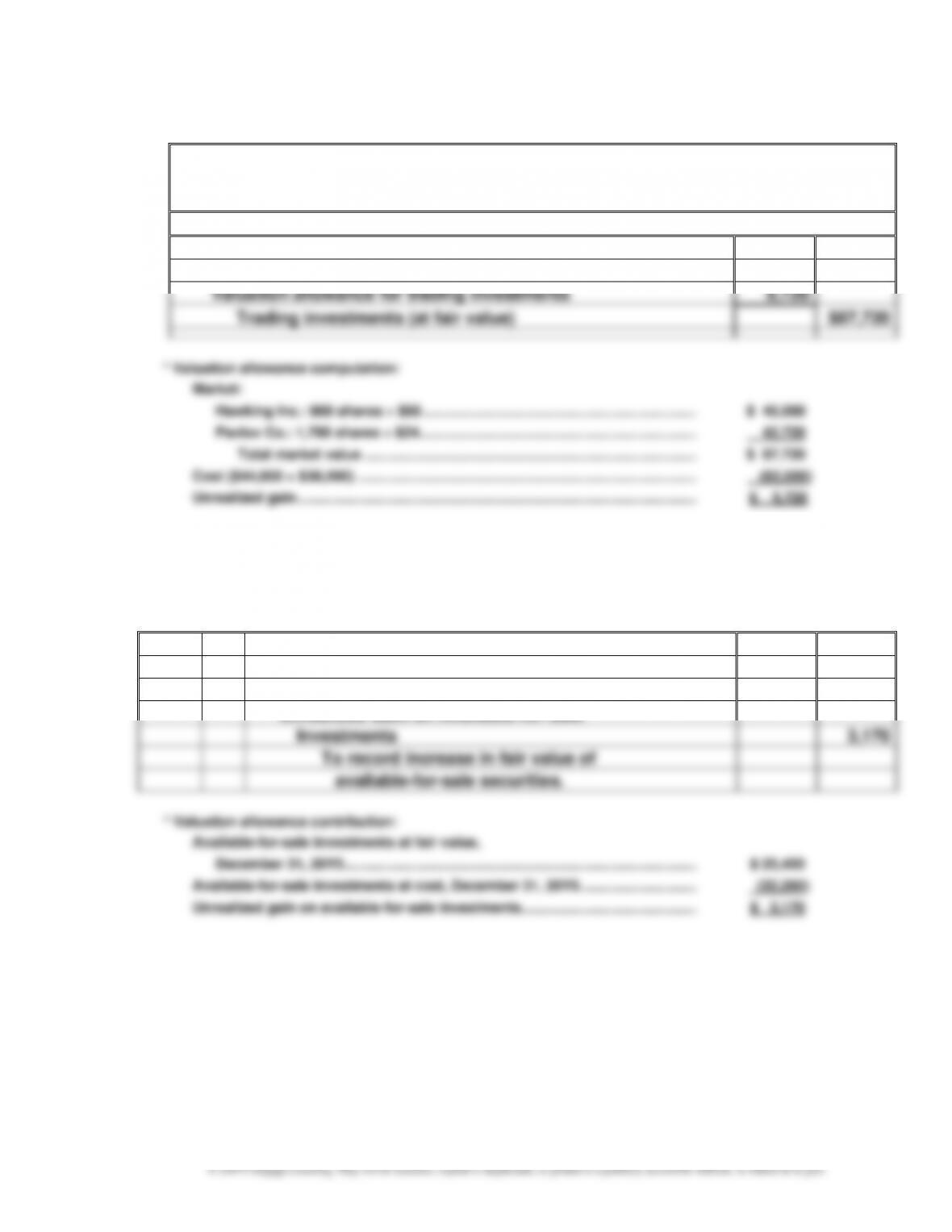

Ex. D–12

a.

Galileo Company

Balance Sheet (selected items)

December 31, 20Y8

Assets

Current assets:

Trading investments (at cost)

$82,000

Valuation allowance for trading investments

5,720

Trading investments (at fair value)

$87,720

* Valuation allowance computation:

Market:

Hawking Inc.: 900 shares $50 ...................................................................... $ 45,000

Pavlov Co.: 1,780 shares $24 ....................................................................... 42,720

Total market value ..................................................................................... $ 87,720

Cost ($44,000 + $38,000) ....................................................................................... (82,000)

Unrealized gain ...................................................................................................... $ 5,720

b. The unrealized gain on trading investments is reported on the income statement and

added in determining net income. Because net income is closed to Retained Earnings, the

unrealized gain will increase retained earnings and stockholders’ equity.

Ex. D–13

20Y5

Dec.

31

Valuation Allowance for Available-for-Sale

Investments*

3,170

Unrealized Gain on Available-for-Sale

Investments

3,170

To record increase in fair value of

available-for-sale securities.

APPENDIX D Investments

Ex. D–14

a.

20Y7

Jan.

1

Investments—Bengals Inc. Bonds

400,000

Cash

400,000

Dec.

31

Unrealized Loss on Available-for-Sale

Investments*

7,200

Valuation Allowance for Available-for-Sale

Investments

7,200

* $392,800 – $400,000

b. Unrealized Loss on Available-for-Sale Investments is reported in the “Stockholders’

Equity” section of the balance sheet, separately from the retained earnings or paid-in