[Key code here]

An asterisk (*) will appear to the right of an incorrect entry.

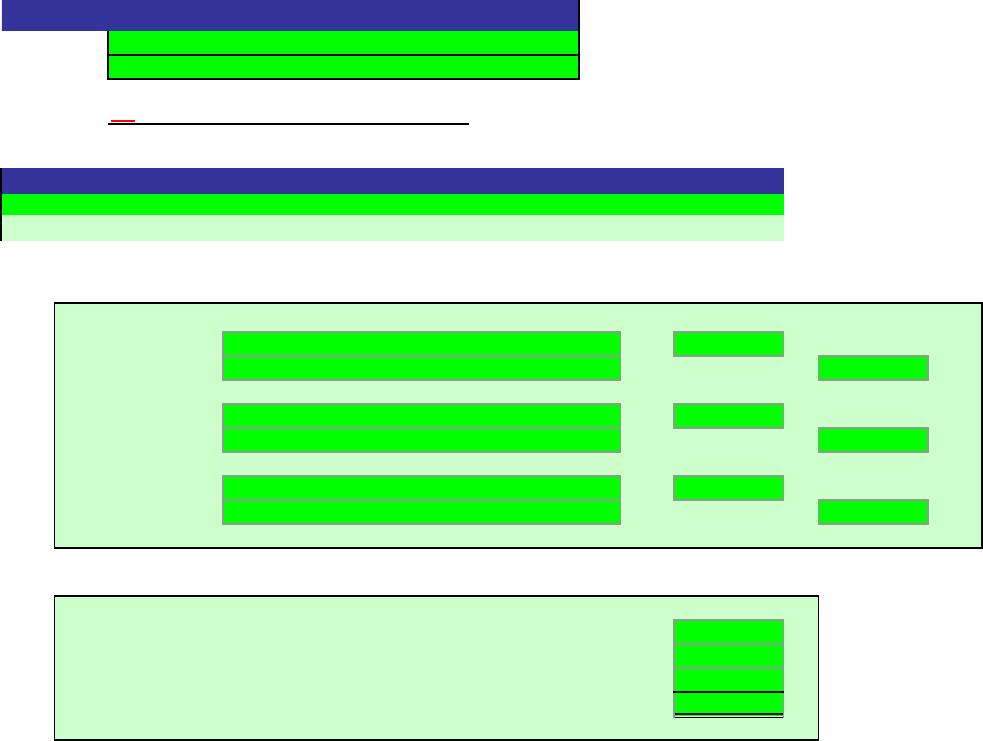

a. 20Y6

Jan. 4

July 2

Dec. 31

b.

Initial acquisition cost

Equity earnings for 20Y6

Cash dividends received

Investment in Filington Co. stock balance, Dec. 31, 20Y6

Exercise D-7

Name:

Section:

Score:

0%

Key Code:

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

An asterisk (*) will appear to the right of an incorrect entry.

a. 20Y6

Jan. 4 4,800,000

4,800,000

July 2 240,000

240,000

Dec. 31 480,000

480,000

b.

Initial acquisition cost 4,800,000$

Equity earnings for 20Y6 480,000

Cash dividends received (240,000)

Investment in Filington Co. stock balance, Dec. 31, 20Y6 5,040,000$

Score:

ON

Exercise D-7

Name:

Solution

Section:

Cash

Investment in Filington Co. Stock

Investment in Filington Co. Stock

Income of Filington Co.

Key Code:

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Investment in Filington Co. Stock

Cash

[Key code here]

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

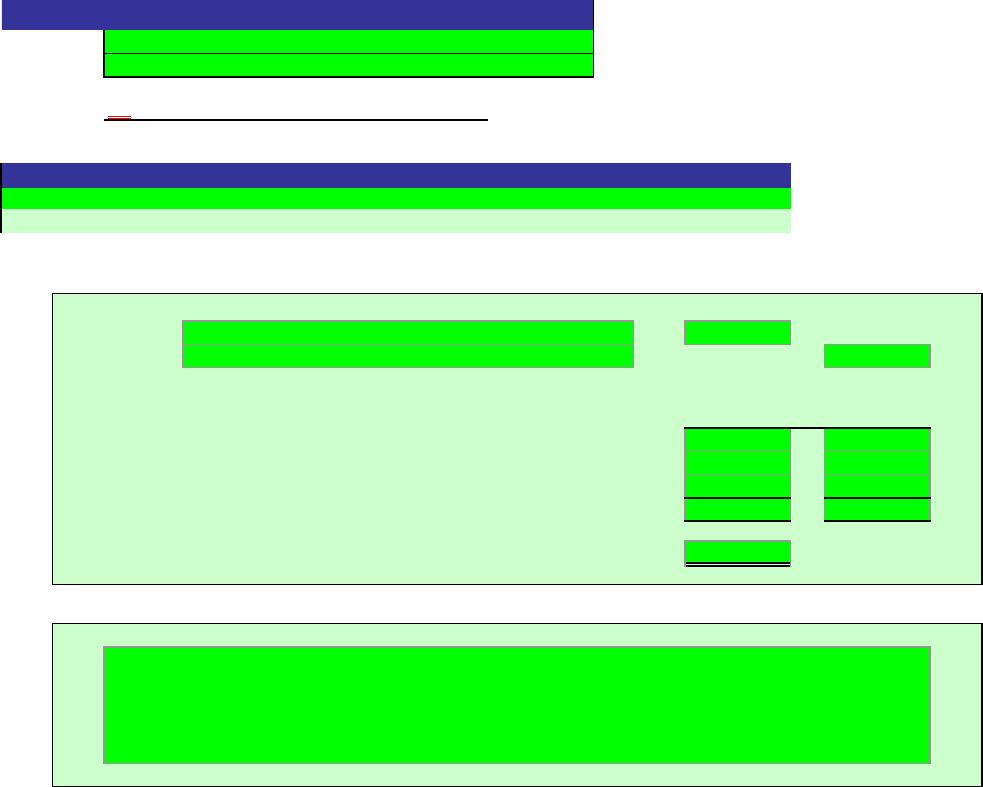

a. 20Y9

Dec. 31

Fair Value

Cost (Dec 31, 20Y9)

Dust Devil, Inc.

Gale Co.

Whirlwind Co.

Total

Increase (decrease) in fair value

b.

Exercise D-11

Name:

Section:

(Key essay answer here)

Score:

0%

Key Code:

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

An asterisk (*) will appear to the right of an incorrect entry. The essay answer will not be graded.

a. 20Y9

Dec. 31 4,250

4,250

Fair Value

Cost (Dec 31, 20Y9)

Dust Devil, Inc. 81,700$ 76,000$

Gale Co. 68,000 63,750

Whirlwind Co. 114,000 119,700

Total 263,700$ 259,450$

Increase (decrease) in fair value (4,250)$

b.

Score:

ON

Exercise D-11

Name:

Solution

Section:

The unrealized loss on trading investments is reported on the income statement as “Other revenue and expense”

(or a separate item if significant). The unrealized loss is deducted in determining net income.

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Unrealized Gain (Loss) on Trading Investments

Valuation Allowance for Trading Investments