13 112

0 2 3

1

32

23

32

32

1

2

3

22

1.

33

F

F

rF

rF

x F dx r dr

r

FF

Analytical Problems

12

1

()

() ()

1

(1 )( )

(1 )

.

Uw

rw Uw

w

w

w

The reciprocal,

1 ( ),rw

is linear in

w

since it is of the form

,a bw

and

1.

()

w

rw

b. When

0

and

1

1,

0

1

( ) .

w

w

rw

Thus,

()rw

is a constant as required if

.

d. Let

1

( ) .r w A

Then

( ) ( ).U w AU w

Solving this differential equation demonstrates

( ) .

Aw

U w ke

2

2

22

() 1

()

( 2 ).

w

Uw

w

ww

Thus, we have a quadratic utility function.

a. A high value for

1R

implies a low elasticity of substitution between states of

the world. A very risk-averse individual is not willing to make trades away from

the certainty line except at very favorable terms.

b.

1R

implies the individual is risk-neutral. The elasticity of substitution between

wealth in various states of the world is infinite. Indifference curves are linear with

slopes of

1.

If

,R

the individual has an infinite relative risk-aversion

parameter. His or her indifference curves are L-shaped implying an unwillingness

to trade away from the certainty line at any price.

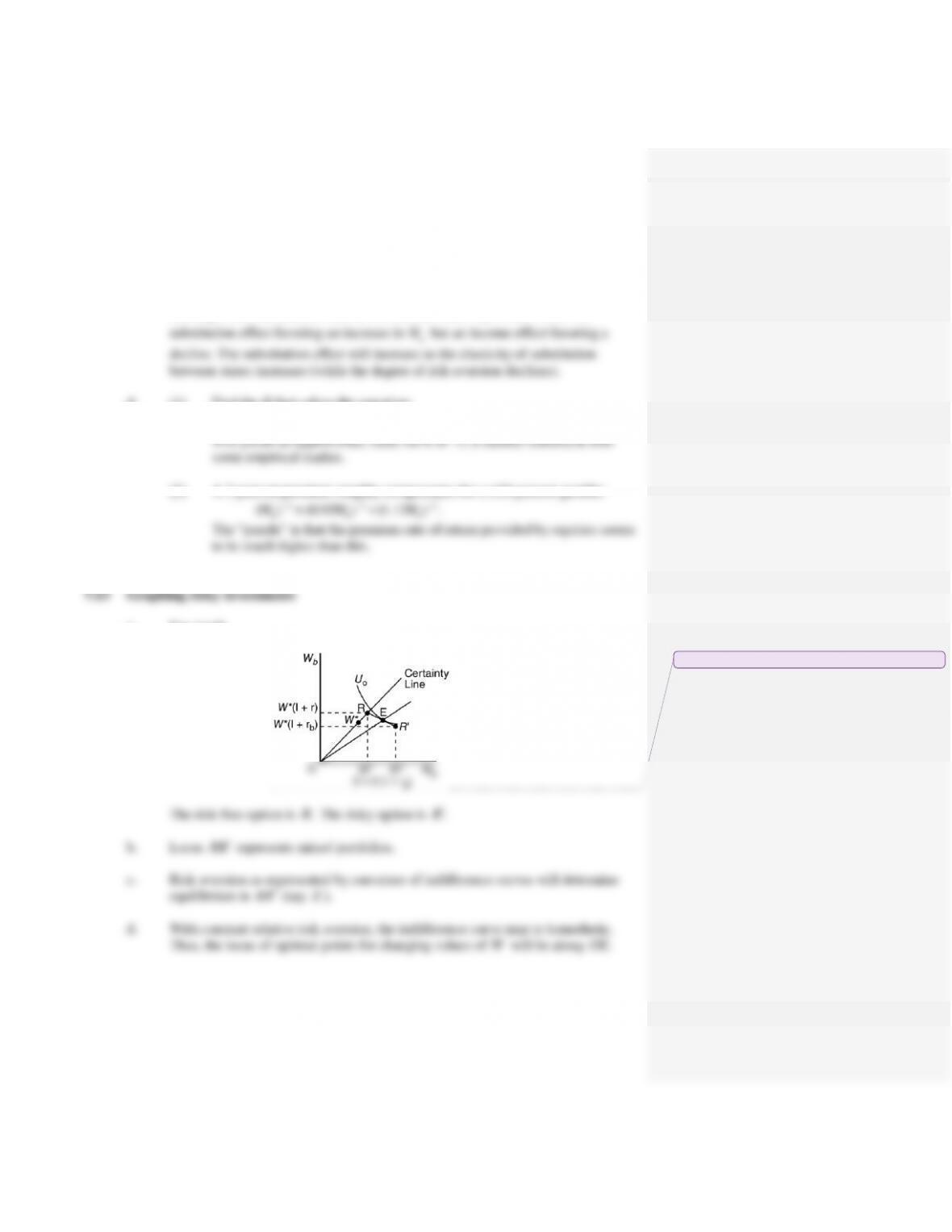

c. A rise in

b

p

rotates the budget constraint counterclockwise about the

g

W

intercept. Both substitution and income effects cause

b

W

to fall. There is a

d. (1) Find the R that solves the equation:

0 0 0

( ) 0.5(1.055 ) 0.5(0.955 ) .

R R R

W W W

(2) A 2 percent premium roughly compensates for a 10 percent gamble:

3 3 3

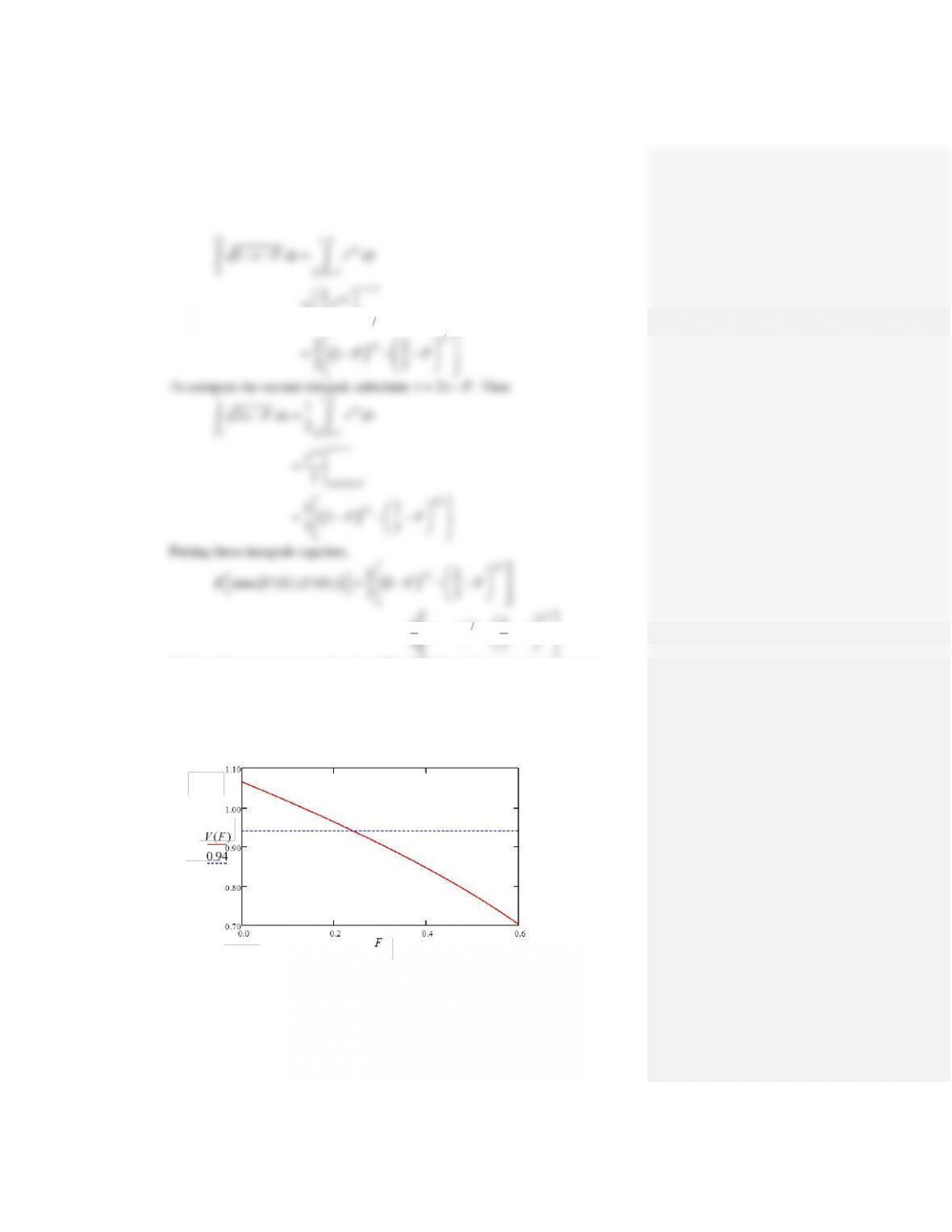

a. See graph.

Commented [C1]: COMP: Please change r, rb, I, rg to r, rb, I, rg.

7.14 The portfolio problem with a Normally distributed asset

From Example 7.3,

2

( ) .

2

Ww

A

E U W

For the portfolio allocation, we are looking to allocate

k

to the risky asset and

0–Wk

to

the risk-free one. Since the risky asset

r

is normally distributed with the distribution

( , )

rr

N

and final wealth is given by

0(1 ) ( )

ff

W W r k r r

(see Equation 7.48), final wealth is distributed as

0

( ) (1 ) ( )

f r f

E W W r k r

Expected utility is given by

22

0

( ) (1 ) ( ) .

2

f r f r

A

E U W W r k r k

Hence,

rf

ur

0,

r

k

20,

r

k

0.

k

A

less to be invested in it.

Behavioral Problem

Scenario 2

Gamble

Expected wealth

C

2,000 1 2 (1,000 0) 1,500

D

2,000 500 1,500

a. Scenarios (

A

)–(

D

) provide the same expected wealth—$1,500—so a risk-

neutral Stan should be indifferent among them.

the safe option

B

in Scenario 1 and

D

in Scenario 2.

c. It is natural to suppose subjects are risk averse, so more should choose option

D

subjects. Scenario 1 involves gains, so Pete behaves as predicted by

may be preferred.

The utility curve has to shift because of the kink at the anchor point.

Prospect Pete’s curve changes from convex to concave at the anchor point;

Standard Stan’s is linear or concave everywhere, so doesn’t have to shift.

Utility

Scenario 1

•

Wealth

1,000

Scenario 2

•

2,000