Most of the problems in this chapter focus on illustrating the concept of risk aversion. They

assume that individuals have concave utility of wealth functions and therefore dislike variance in

their wealth. For some of these problems (especially the later ones), students will need to review

the material on mathematical statistics in Chapter 2.

Comments on Problems

7.1 This problem reverses the risk-aversion logic to show that observed behavior can be used

to place bounds on subjective probability estimates.

presented here.

7.3 This is a nice, homey problem about diversification. The problem can be done

graphically, but instructors could introduce variances into the problem if desired.

7.4 This problem is a graphical introduction to the economics of health insurance that

examines cost-sharing provisions. Health insurance is discussed in more detail in Chapter

18.

7.5 This problem provides some simple numerical calculations involving risk aversion and

insurance when utility is logarithmic.

7.6 This is a rather difficult problem as written. It can be simplified by using a particular

utility function (e.g.,

( ) lnU W W

). With the logarithmic utility function, one cannot use

the Taylor approximation until after differentiation, however. If the approximation is

applied before differentiation, concavity (and risk aversion) is lost. This problem can,

with specific numbers, also be done graphically, if desired. The notion that fines are more

effective can be contrasted with the criminologist’s view that apprehension of law–

provisions can affect diversification.

CHAPTER 7:

Uncertainty

7.9 This is a new problem on diversification, here applied to investing in financial assets. The

problem illustrates a case in which it is optimal to diversify into an asset with obviously

lower expected returns. The problem shows that diversification can be beneficial with

Analytical Problems

special cases of the HARA function.

7.12 More on the CRRA function. This problem stresses the close connection between the

7.13 Graphing risky investments. This problem provides an illustration of investment theory

in the state preference framework.

7.14 The portfolio problem with a Normally distributed risky asset. This problem shows

how the portfolio problem can be solved explicitly if asset returns are Normal.

behavioral economics, which Kahneman (Nobel Prize winner) and Tversky applied to

explain the results of their lab experiments. Actual experimental results are cited in the

problem.

Solutions

ln 1,100,000 1 ln 900,000 ln 1,000,000 .pp

Solving,

13.9108 13.7102 1 13.8155,pp

implying

2006 0.1053,p

or

0.525.p

7.2 See graph.

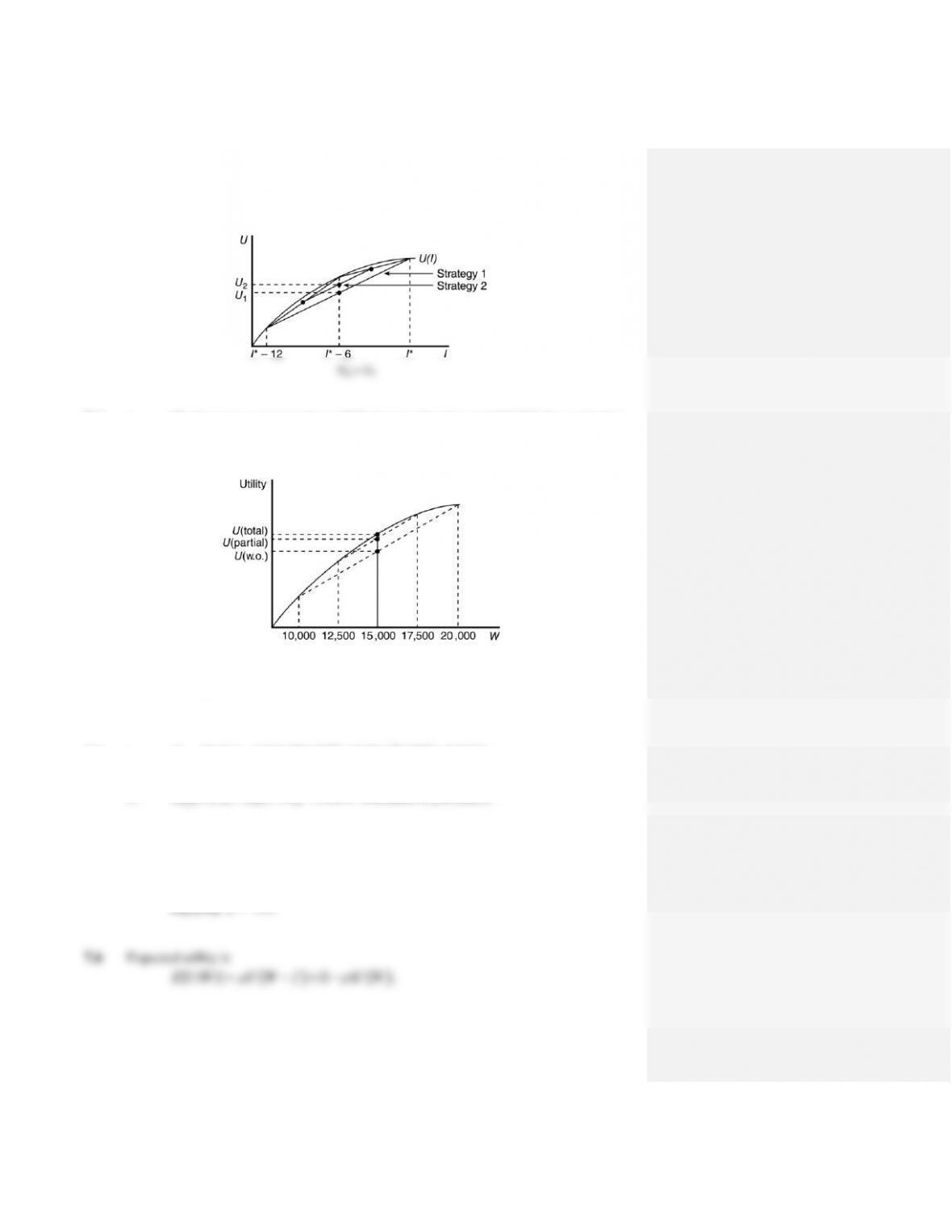

7.3 a.

Strategy 1

Outcome

Probability

12 Eggs

0.5

0 Eggs

0.5

Expected value =

0.5 (12) 0.5( 0) 6.

Strategy 2

Outcome

Probability

12 Eggs

0.25

6 Eggs

0.5

0 Eggs

0.25

Expected value =

0.25 (12) 0.5( 6) 0.25(0) 3 3 6.

b.

Commented [C1]: COMP: Please set h as h.

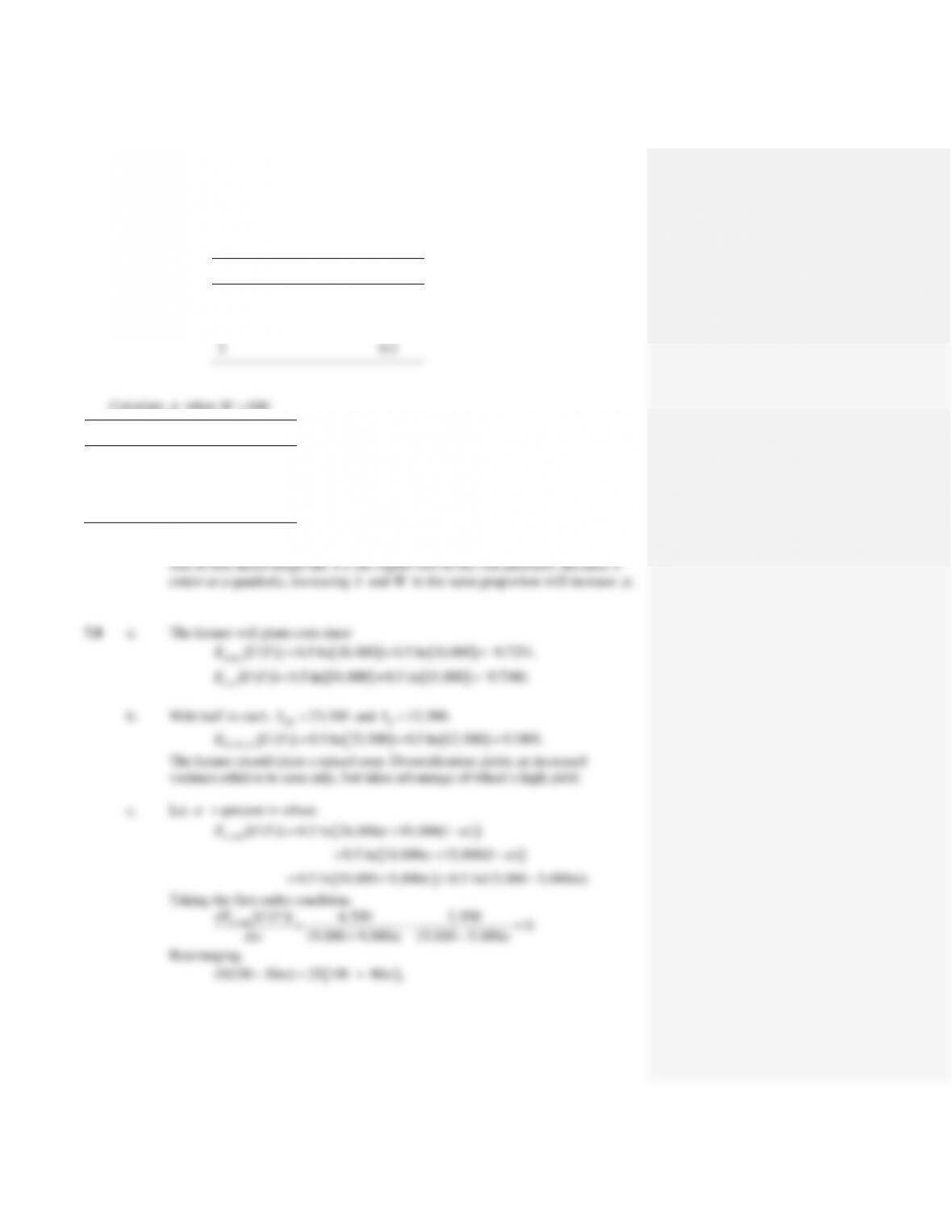

7.4 a. The insurance company has a 50% chance of paying out $10,000. Its cost is thus

$5,000. The consumer has a certain wealth of $15,000 with fair insurance

compared to a 50–50 chance of wealth of $10,000 or $20,000 without insurance.

b. Cost of the policy is

0.5 5,000 2,500

. Hence, wealth is 17,500 with no illness

and 12,500 with the illness.

7.5 a.

no ins[ ( )] 0.75ln 10,000 0.25ln 9,000 9.1840.E U Y

b.

ins[ ( )] ln 9,750 9.1850.E U Y

Insurance is preferable.

c. We have

ln(10,000 ) 9.1840.p

Exponentiating,

9.1840

10,000 9,740,pe

implying

260.p

Calculate

p

when

10W

k

p

0.5

0.0125

1

0.05

2

0.2

Risk premium is higher when the level of initial wealth is lower. The greater the

Calculate

p

when

100W

k

p

0.5

0.00125

1

0.005

2

0.02

implying

0.444.

Plugging

into the utility function yields

*mix[ ( )] 0.5 ln 22,996 0.5 ln 12,780 9.7494.E U Y

This is a slight improvement over the 50–50 mix.

d. If the farmer plants only wheat,

24,000

NR

Y

and

14,000.

R

Y

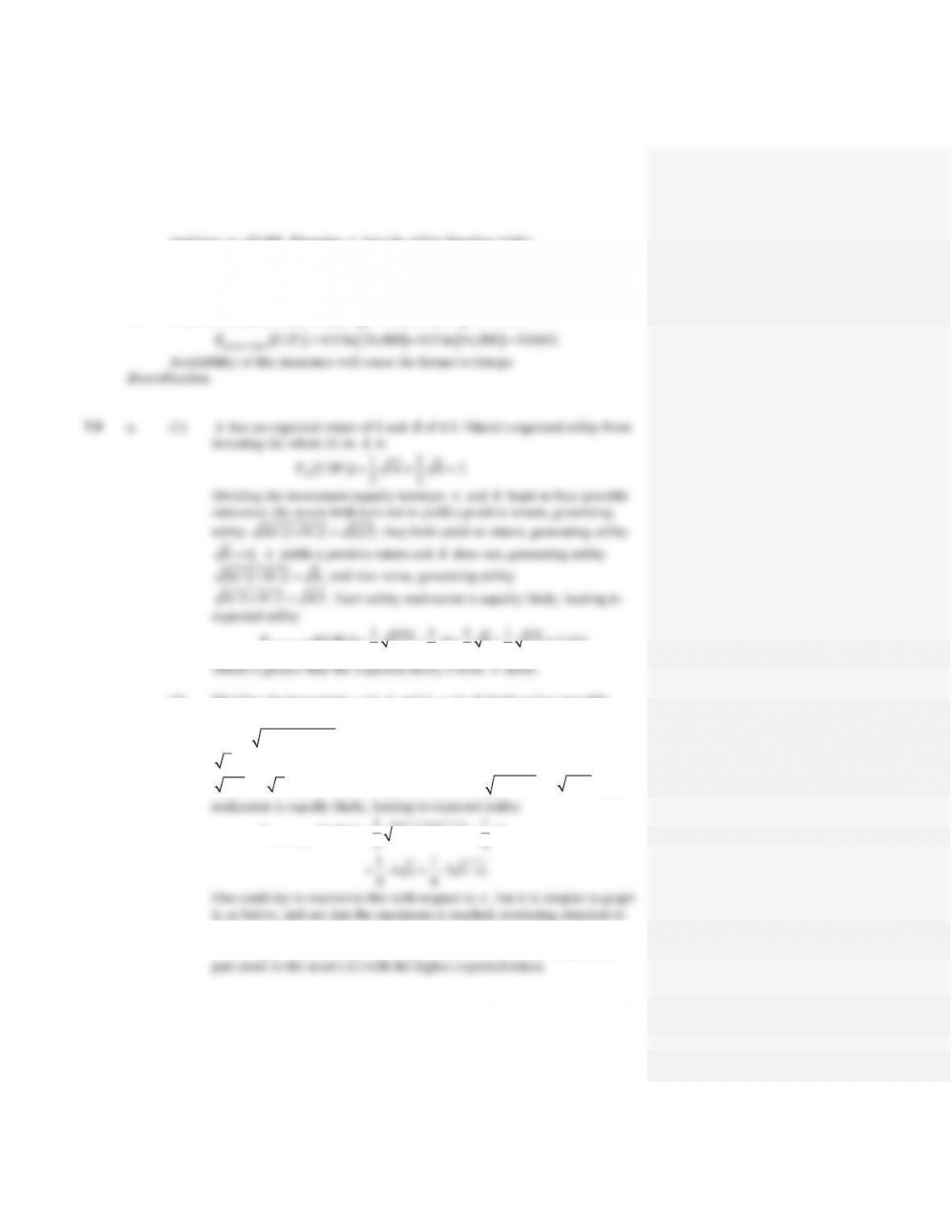

equal split 1 1 1 1

[ ( )] 12.5 0 8 4.5 2.121,

4 4 4 4

E U W

a

in

A

and

1a

in

B

leads to four possible

outcomes: the assets both turn out to yield a positive return, generating

utility

16 9(1 );aa

they both yield no return, generating utility

0 0;

A

yields a positive return and

B

does not, generating utility

16 4 ;aa

and vice versa, generating utility

9(1 ) 3 1 .aa

Each

11

4 3 1 .

44

aa

One could try to maximize this with respect to

a

, but it is simpler to graph

it, as below, and see that the maximum is reached, restricting attention to

decimal values of

,a

for

0.8,a

at which point the expected utility is

2.185, higher than from an equal split. While Maria still diversifies, she

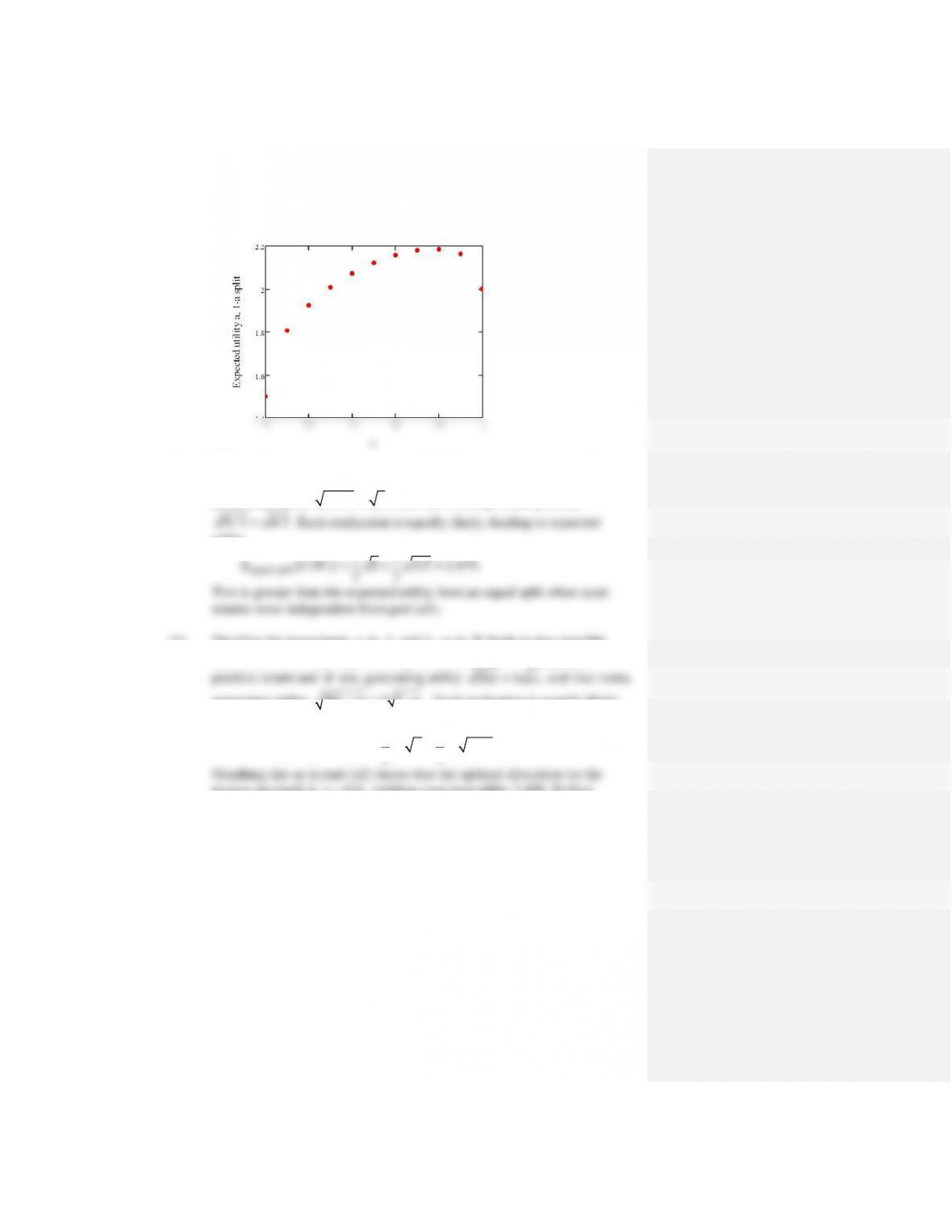

b. (1) With perfect negative correlation, and half invested in each asset, there are

only two possible outcomes:

A

has a positive return and

B

nothing,

generating utility

16/ 2 8;

and vice versa, generating utility

9 / 2 4.5.

Each realization is equally likely, leading to expected

utility

equal split 11

[ ( )] 8 4.5 2.475.

22

E U W

This is greater than the expected utility from an equal split when asset

returns were independent from part (a1).

(2) Dividing the investment

a

in

A

and

1a

in

B

leads to two possible

outcomes when there is perfect negative correlation:

A

can yield a

generating utility

9(1 ) 3 1 .aa

Each realization is equally likely,

leading to expected utility

,1 split 11

[ ( )] 4 3 1 .

22

aa

E U W a a

nearest decimal) is

0.6,a

yielding expected utility 2.498. Perfect

negative correlation makes diversification even more appealing.