337

chapter

17(3)

Process Cost Systems

______________________________________________

OPENING COMMENTS

In this chapter, you need to consider which method(s) of process costing you will choose to cover in your

class. When the FIFO method is presented in the chapter (Objectives 2 and 3), the manufacturing

department adds materials at the beginning of production and conversion costs evenly throughout

production. This requires two sets of equivalent unit calculations. When the average cost method is

computations related to process costing.

The average cost method will still allow you to communicate the concept of equivalent units. If you want

to take a more conceptual approach, you could choose to only cover the average cost method and keep the

calculations more streamlined. If you want to dig into process costing more fully, the FIFO method may

After studying the chapter, your students should be able to:

1. Describe process cost systems.

2. Prepare a cost of production report.

3. Journalize entries for transactions using a process cost system.

4. Describe and illustrate the analysis of unit cost changes between periods.

Chapter 17(3) Process Cost Systems 338

5. Compare lean manufacturing with traditional manufacturing processing.

ADM: Describe and illustrate the use of a cost of production report in evaluating a company’s

performance.

KEY TERMS

cost of production report

cost per equivalent unit

equivalent units of production

first-in, first-out (FIFO) method

lean manufacturing

manufacturing cells

process cost system

process manufacturer

whole units

STUDENT FAQS

Why is it necessary to know the four steps of producing a cost of production report?

What does equivalent units of production (EUP) mean, and why is it necessary for it to be correct?

Started and completed under “units to be assigned cost” gives me problems every time. Do you have

a suggestion to eliminate my problem?

Why does the complement of the percentage in beginning inventory have to be used to calculate EUP

when the percent of completed has to be used for the ending?

Why in lean manufacturing a more efficient approach to manufacturing?

Why do we do a material and conversion EUP only? Shouldn’t conversion be made into Direct Labor

and Factory Overhead to be more accurate?

OBJECTIVE 1

Describe process cost systems.

SYNOPSIS

A process manufacturer produces products that are homogeneous; they use a cost system called process

costing. This system records the costs of each department or process. Process costing is similar to job

costing in that each records and summarizes product costs, allocates overhead, uses perpetual inventory,

and provides useful information for decision making. The example in the chapter, using ice cream, adds

all materials at the beginning of the process. There are two departments: Mixing and Packaging. Labor

and overhead costs occur in each department. When the Mixing Department is done with the product, its

costs are transferred to the Packaging Department along with the product. When the Packaging

Department completes its process, the product costs are transferred to finished goods. The cost flows in

Chapter 17(3) Process Cost Systems 339

the process cost system are similar to the physical flow of goods. As shown in Exhibit 4, each department

has a separate overhead account. The overhead is applied to work in process by debiting each

department’s factory overhead account and crediting each department’s Work in Process. When the

product is transferred, Work in Process—Mixing Department is credited and Work in Process—

Packaging Department is debited. Lastly, the Packaging Department transfers the product to finished

goods. Finished Goods is debited for the amount transferred, and Work in Process—Packaging

Department is credited.

Key Terms and Definitions

Process Cost System—A type of cost system that accumulates costs for each of the various

departments within a manufacturing facility.

Process Manufacturer—A manufacturer that uses large machines to process a continuous flow

of raw materials through various stages of completion into a finished state.

Relevant Check Up Corner and Exhibits

Exhibit 1—Examples of Process Cost and Job Order Companies

Exhibit 2—Process Cost and Job Order Cost Systems

Exhibit 3—Physical Flows for a Process Manufacturer

Exhibit 4—Cost Flows for a Process Manufacturer—Frozen Delight

SUGGESTED APPROACH

Transparency Masters (TMs) 17(3)-1 through 17(3)-3 explain the types of manufacturers that use job

order and process costing, as well as the similarities and differences in these two systems. Ask your

students to give examples of companies that would use job order costing and companies that would use

process costing. As an alternative, ask your students whether a soft drink bottler would use a process or

job order system.

Because costs are accumulated by department in a process cost system, each department has its own work

in process account. Use TM 17(3)-4 to explain the flow of costs through the departmental work in process

accounts. Exhibit 4 in the text presents another illustration to reinforce the cost flows for a process

manufacturer.

As you cover these illustrations, emphasize that there are separate work in process and factory overhead

accounts for each department. This allows the manufacturer to accumulate product costs by department.

Also stress that costs transferred out of one department become the costs transferred in to the next

department.

Chapter 17(3) Process Cost Systems 340

OBJECTIVE 2

Prepare a cost of production report.

SYNOPSIS

In a process system, the cost of units transferred out of each department must be determined along with

the cost of any partially completed units remaining in the department. These costs are reported in a cost of

are complete. Equivalent units of production are the portion of whole units that are complete with respect

to materials or conversion. The materials costs are 100% complete because all the materials are added at

the beginning. The conversion cost are 40% complete, and the equivalent units are all units in process

multiplied by 40%. The equivalent units are computed in Exhibit 7. Cost must be converted for both

for the Mixing Department.

Key Terms and Definitions

Cost of Production Report—A report prepared periodically by a processing department,

summarizing (1) the units for which the department is accountable and the disposition of those

units and (2) the costs incurred by the department and the allocation of those costs between

completed and partially completed units.

completed production.

Equivalent Units of Production—The portion of whole units that are complete with respect to

materials or conversion costs.

First-In, First-Out (FIFO) Method—The method of inventory costing based on the assumption

that the costs of merchandise sold should be charged against revenue in the order in which the

costs were incurred.

Relevant Check Up Corner and Exhibits

Exhibit 5—July Units to Be Costed—Mixing Department

Exhibit 6—Direct Materials Equivalent Units

Exhibit 7—Conversion Equivalent Units

Check Up Corner 17(3)-1 – Equivalent Units

Check Up Corner 17(3)-2 – Cost per Equivalent Unit

Chapter 17(3) Process Cost Systems 341

SUGGESTED APPROACH

one unit of product as follows:

Cost to Make One Unit in One Department = Department’s Cost for the Month

Number of Units Produced During the Month

demonstration problem in TM 17(3)-5 to prepare a cost of production report for Advanced Technologies’

assembly department. Refer your students to Exhibit 8 in the text as a model for this report. You may

want to review the major sections of the cost of production report prior to assigning this activity.

LECTURE AID—Equivalent Units

The following scenario relates equivalent units to a common student dilemma.

Assume that you are taking four classes this term, and all four classes require a five-page paper. Of

course, when will these papers be due? (I’ve never had a class that didn’t immediately respond with the

Assume that you write four pages on the first paper and run out of information. Then you write three

pages on the next paper and stop to watch a TV show. Next, you write two pages on the third paper before

you get too bored to continue. So you switch to the last paper and write one page before you fall asleep at

the keyboard. If you worked on one paper until it was finished and then started another paper, how many

Emphasize that there are two equivalent units in this example. Two finished papers could have been

written with the same effort used to do partial work on four papers.

DEMONSTRATION PROBLEM—Process Costing, FIFO Method

The text presents the calculation of product costs under FIFO process costing as a four-step process. Use

Chapter 17(3) Process Cost Systems 342

Advanced Technologies produces notebook computers in three departments: assembly, testing, and

assembly process.

Assume that the assembly department of Advanced Technologies began April with 800 units in its work

in process inventory. Assembly on these units was three-fourths complete at the beginning of the month.

During the month, 3,000 units were started in the assembly department. At the end of the month, 300 of

The costs associated with production in assembly during April were as follows:

Cost of units in beginning work in process inventory $228,000

Cost of materials used in April 630,000

STEP 1: Determine the units to be assigned costs. Instruct students to begin by determining the total

number of units worked on in the assembly department during April plus the number of units in each of

the following three categories:

Beginning Work in Process Inventory

Units Started and Completed During the Month

Ending Work in Process Inventory

process inventory.

STEP 2: Calculate equivalent units of production. Since all materials are added by the assembly

department at the beginning of production, and conversion costs are added evenly throughout production,

equivalent units must be calculated separately for materials and conversion costs. Remind students that

Chapter 17(3) Process Cost Systems 343

© 2018 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

No. of Whole Units Amount of Work Put into the Units during the Month

(expressed as a fraction or a percentage)

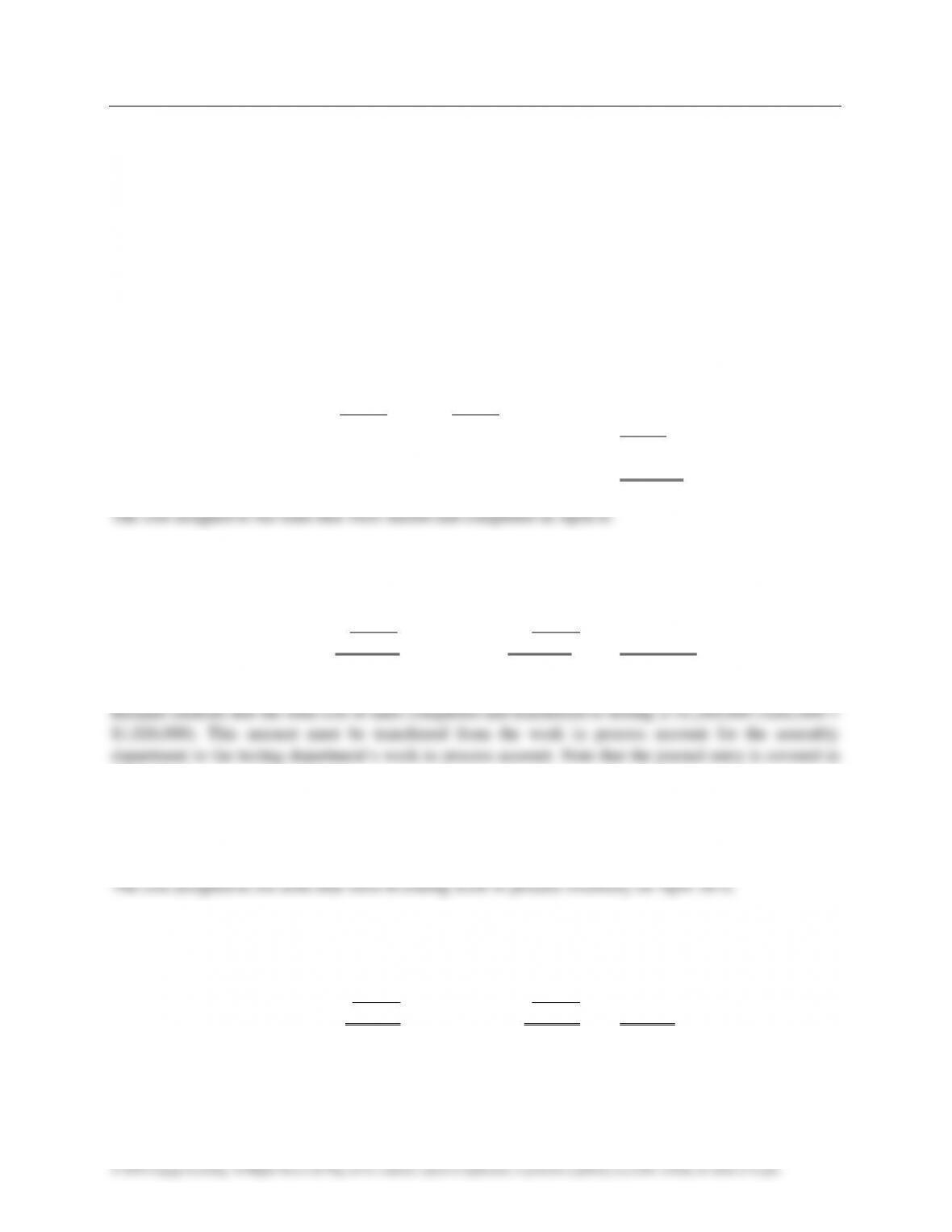

Material equivalent units for Advanced Technologies’ assembly department would be calculated as

follows:

% Materials

Whole Units Added in April Equivalent Units

Beginning WIP Inventory 800 0 0

Units Started and Completed 2,700 100% 2,700

Ending WIP Inventory 300 100% 300

3,000

Conversion equivalent units for Advanced Technologies’ assembly department would be calculated as

follows:

% Conversion

Whole Units Added in April Equivalent Units

Beginning WIP Inventory 800 1/4 200

Units Started and Completed 2,700 100% 2,700

Ending WIP Inventory 300 2/3 200

3,100

STEP 3: Determine the cost per equivalent unit. In order to determine the total cost to produce a unit, a

manufacturer must compute the materials cost and the conversion cost (labor and overhead) in a

completed unit. This amount is the cost per equivalent unit. The formula for this calculation is:

Costs Incurred During the Month

Cost per Equivalent Unit Equivalent Units Produced During the Month

For Advanced Technologies, cost per equivalent unit must be calculated separately for materials and

conversion costs since these resources are added at different rates in the manufacturing process (materials

Materials and conversion costs per equivalent unit are calculated as follows:

$630,000

Materials Cost/Equivalent Unit = $210

3,000 equiv. units

$527,000

Conversion Cost/Equivalent Unit $170

3,100 equiv. units

Chapter 17(3) Process Cost Systems 344

© 2018 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

STEP 4: Allocate costs to transferred and partially completed units. After calculating the cost per

equivalent unit for materials and conversion costs, the cost of units completed and those still in process

must be determined. Stress that students will have the most success if they calculate the cost separately

for each category of units on the equivalent units’ schedule. The beginning work in process and started

and completed categories represent units that have been completed in assembly and transferred on to the

testing department. The ending work in process represents the units that have not been completed.

The cost assigned to the units that were in beginning work in process is:

Direct Materials Conversion Cost Total Cost

Beginning WIP Balance $228,000

Cost to Complete:

Equivalent Units for April 0 200

Cost per Equivalent Unit $210 $170

0 34,000 34,000

Cost of April 1 WIP

transferred to testing $262,000

Direct Materials Conversion Cost Total Cost

Started and Completed:

Equivalent Units 2,700 2,700

Cost per Equivalent Unit $210 $170

Cost of Units Started & $567,000 $459,000 $1,026,000

Completed in April

Objective 3.

WIP Inventory—Testing Department 1,288,000

WIP Inventory—Assembly Department 1,288,000

Direct Materials Conversion Cost Total Cost

Ending WIP Inventory:

Equivalent Units 300 200

Cost per Equivalent Unit $210 $170

Total Cost of Ending WIP $63,000 $34,000 $97,000

Chapter 17(3) Process Cost Systems 345

CLASS DISCUSSION—Process Costing

In the previous Demonstration Problem, all materials were introduced at the beginning of the production

process. Ask your students for other examples of materials that would be added at the start of production.

Additional ideas include soup broth for soup making, alumina for aluminum smelting, crude oil for

gasoline refining, or pulp for papermaking. Next ask your students for materials that would not be added

In the Advanced Technologies problem, all conversion costs were incurred evenly throughout the

production process. Ask your students for an example of an overhead cost that would not be incurred

evenly. One example would be energy costs. Frequently, the energy component is not used at exactly the

same rate throughout processing. Therefore, some companies separate the energy cost from conversion

costs and account for it separately.

FIFO Method

The textbook illustrates process costing for the first department in a manufacturing process. End of

chapter problems also ask students to calculate product costs for departments that are second or third in

the manufacturing flow. Emphasize that all departments that receive units from prior departments also

receive costs that are “transferred in” from those departments. Transferred in costs can be treated in the

TM 17(3)-6 presents information to calculate and assign costs to units in Advanced Technology’s testing

department for the month of April. The four-step solution to this problem is provided on TMs 17(3)-7

through 17(3)-11. Allow your students the opportunity to practice FIFO process costing by working in

groups. Since most students struggle with this topic, the time for group work is well spent.

OBJECTIVE 3

SYNOPSIS

Next, journal transactions are discussed as these product transfers need to be journalized. Materials are

purchased and the materials account is debited and Accounts Payable is credited. As the direct materials

are requisitioned, work in process accounts are debited and Materials is credited. When indirect materials

are requisitioned or other indirect expenses are recognized, factory overhead accounts are debited and