Chapter 16(2) Job Order Costing 330

Point out that, unlike the situation in the banquet example, overhead costs usually are not divided evenly

manufacture than others.

Assume that MTM manufacturing estimates it will spend $1 million on overhead expenses. MTM is a

highly automated manufacturing plant; therefore, the majority of its overhead expenses relate to

machinery (depreciation, repairs and maintenance, electricity used). Machine hours used would be a

The formula to calculate MTM’s predetermined overhead rate is as follows:

Estimated Total Factory Overhead Costs $1,000,000 $25/hour

Estimated Activity Base (machine hours) 40,000 hours

Ask your students to calculate the overhead that would be allocated to a product that uses 3.5 hours of

machine time. (Answer: $87.50) Remind students that overhead costs are added to the product’s materials

and labor costs.

overhead costs.

In practice, more than one factory overhead rate may be used for applying overhead. Materials-related

overhead (such as purchasing, materials receiving or inspection, and materials storage costs) could be

allocated based on the direct materials cost of a product, with the remaining overhead allocated based on

illustrated in Chapter 23.

DEMONSTRATION PROBLEM—Overapplied and Underapplied Overhead

Ask your students to calculate the amount of overhead allocated to the products of a company that has a

predetermined overhead rate of $10 per machine hour if machines were used for 10,000 hours. (Answer:

$100,000)

Chapter 16(2) Job Order Costing 331

© 2018 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

1. Actual overhead costs do not equal the estimated costs used to compute the predetermined overhead

rate.

2. The actual activity base (machine hours) does not equal the estimated activity base used to compute

the predetermined overhead rate.

TM 16(2) -2 shows circumstances where over- and underapplied overhead occur and how they are treated

in the accounting records.

GROUP LEARNING ACTIVITY—Journal Entries in a Job Order System

Exhibit 2 in the text summarizes the flow of costs in a job order cost system (costs move from materials

inventory to work in process to finished goods to cost of goods sold). Exhibit 9 shows the entries needed

to record manufacturing costs in T accounts. Ask your students to record the journal entries listed on TM

16(2)-3, using Exhibits 2 and 9 as a guide. The correct entries are displayed on TM 16(2)-4. You may

want to have your students post these entries to T accounts and determine account balances.

Emphasize the following points as students record their entries:

process and factory overhead.

overhead.

4. Product sales serve as the basis for transferring jobs from finished goods to cost of goods sold.

OBJECTIVE 3

SYNOPSIS

A job order cost system can also be used for a professional service business. Customers can be viewed as

jobs for which costs are accumulated. The primary product costs for services are direct labor and

through a service business is shown in Exhibit 11.

Relevant Check Up Corner and Exhibits

Chapter 16(2) Job Order Costing 332

SUGGESTED APPROACH

Refer your students to Exhibit 11 in the text. While reviewing that diagram, stress the following points:

an overhead expense.

2. A cost of services account is used to record the cost of completed jobs.

GROUP LEARNING ACTIVITY—Job Order Costing in a Service Business

TM 16(2) -6 presents information about a CPA firm that does audit and tax work. Divide your class into

small groups and instruct students to determine the cost to prepare a tax return. The solution is shown on

TM 16(2) -7.

ADM OBJECTIVE

Describe the use of job order cost information for decision making.

SYNOPSIS

The job order cost system allows managers to compare the costs of similar jobs, compare overtime, and

compare actual costs to expected costs. Discrepancies can be investigated and future costs controlled.

Relevant Check Up Corner and Exhibits

Exhibit 12—Comparing Data from Job Cost Sheets

Make a Decision – Analyzing Job Costs

SUGGESTED APPROACH

The goal of this objective is to explore the ways in which job cost information is used in decision making.

To put your students in the role of decision maker, use the following Group Learning Activity.

GROUP LEARNING ACTIVITY—Decision Making

Handout 16(2) -1 is a brief problem asking students to interpret two job cost sheets. Ask your students to

work on this problem in groups. After providing sufficient time, ask some of the groups to report their

responses. TM 16(2) –5 provides the solution.

Chapter 16(2) Job Order Costing 333

Comparing the two job cost sheets shows that the improved price per pound of alloy does not offset the

increased costs associated with higher materials usage rates and reduced casting and machining

department efficiency. It is likely that the events are related. The lower alloy cost has probably resulted

from the purchase of sub-quality raw materials. As a result, more alloy is required per casting on Job 210

than on prior jobs. In addition, the casting and machining departments are having greater difficulty with

the castings, causing the efficiency of the departments to drop. Therefore, it appears that the new alloy

vendor is causing the company to experience more scrapped castings, which increases the materials cost

and conversion costs to produce product. Shipping costs are unaffected.

Job 210 also is allocated more overhead because it now consumes more labor hours. This allocation

Handout 16(2) -1

Decision Making Using Job Cost Data

Griffin Casting Company is a job shop that manufactures castings for a variety of purposes. The

following two job cost sheets relate to two different orders for an identical casting used to house

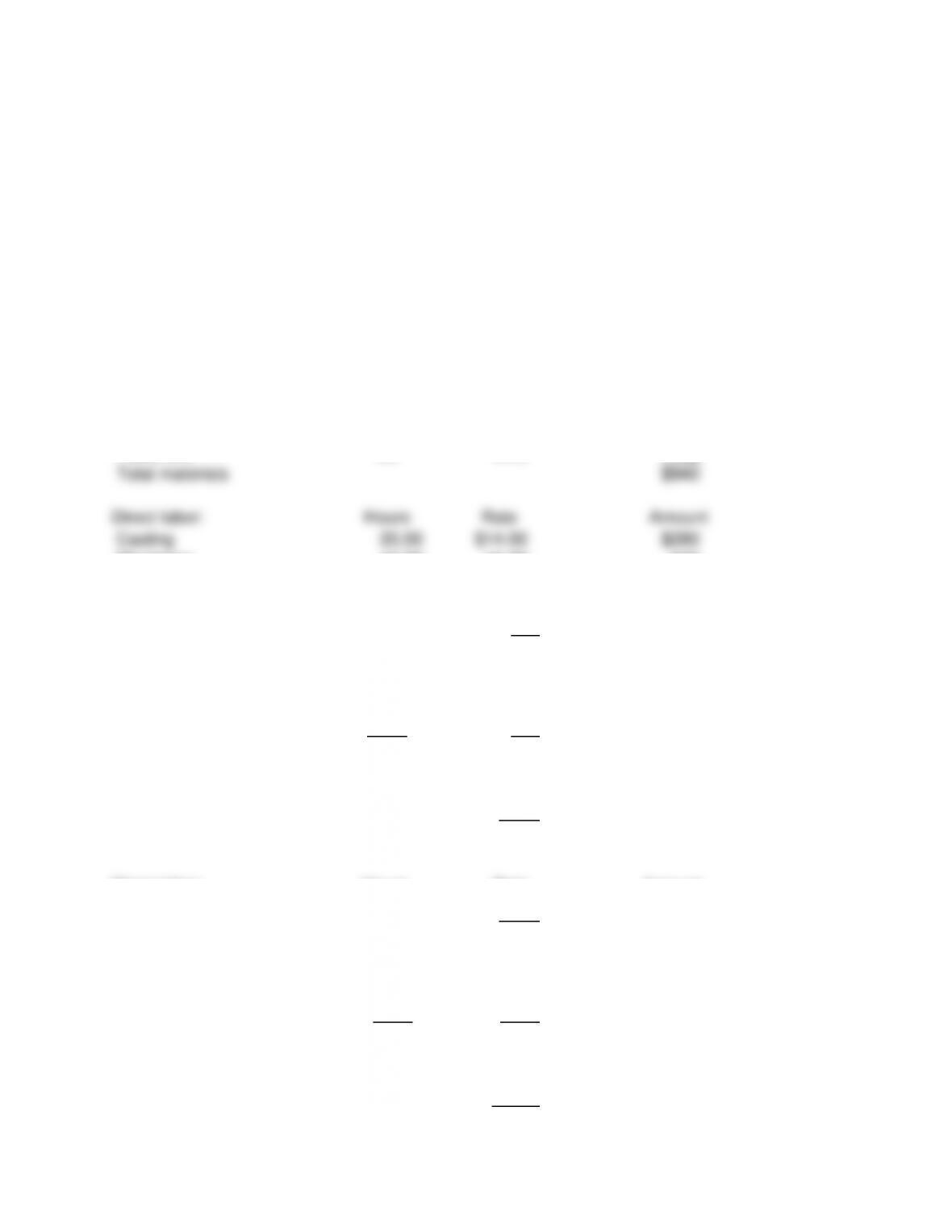

Job 100 Date Completed: March 30 Item: 40 automobile generator housings

Materials: Quantity Price Amount

Alloy (pounds) 60 $15.00 $900

Fasteners 160 0.25 40

Total materials $940

Direct labor: Hours Rate Amount

Casting 20.00 $14.00 $280

Machining 40.00 16.00 640

Shipping 4.00 10.00 40

Total direct labor 64.00 $960

Factory overhead

(200% of direct labor dollars) 960 200% $1,920

Total Cost $3,820

Total Units ÷ 40

Unit Cost $95.50

Materials: Quantity Price Amount

Alloy (pounds) 200 $12.00 $2,400

Fasteners 400 0.25 100

Total materials $2,500

Direct labor: Hours Rate Amount

Casting 60.00 $14.00 $2,840

Machining 120.00 16.00 1,920

Shipping 10.00 10.00 100

Total direct labor 190.00 $2,860

Factory overhead

(200% of direct labor dollars) 2,860 200% $5,720

Total Cost $11,080

Total Units ÷ 100

Unit Cost $110.80

Type Item Description Video Excel CLGL LO(s) Difficulty Time Est BUSPROG AICPA

ACBSP – Primary Bloom’s ADM Service Real World

Writing

Ethics

MC 1 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

MC 2 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

MC 3 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

MC 4 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

MC 5 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

LREX 1 Issuance of materials x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

LREX 2 Direct labor costs x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

LREX 3 Factory overhead costs x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

LREX 4 Applying factory overhead x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

LREX 5 Job costs x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

LREX 6 Cost of goods sold x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

DQ 6 n/a Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

DQ 7 n/a Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

DQ 8 n/a Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

DQ 9 n/a Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

BE 6 Cost of goods sold x 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Applying

EX 1 Transactions in a job order cost system 2 Easy 5 min. Analytic FN – Measurement Job Order Costing Remembering

EX 2 Cost flow relationships x 2 Easy 10 min. Analytic FN – Measurement Job Order Costing Applying

EX 3 Cost of materials issuances under the FIFO method x 2 Moderate 30 min. Analytic FN – Measurement Job Order Costing Applying x

EX 10 Predetermined factory overhead rate x 2 Moderate 15 min. Analytic FN – Measurement Job Order Costing Applying

EX 11 Predetermined factory overhead rate x 2 Moderate 15 min. Analytic FN – Measurement Job Order Costing Applying

EX 12 Entry for jobs completed; cost of unfinished jobs x 2 Moderate 15 min. Analytic FN – Measurement Job Order Costing Applying

EX 13 Entries for factory costs and jobs completed 2 Moderate 30 min. Analytic FN – Measurement Job Order Costing Applying

PR 4A Analyzing manufacturing cost accounts x 2 Challenging 1.5 hours Analytic FN – Measurement Job Order Costing Applying

PR 5A Flow of costs and income statement x 2 Challenging 1.5 hours Analytic FN – Measurement Job Order Costing Applying

PR 1B Entries for costs in a job order cost system x x 2 Moderate 45 min. Analytic FN – Measurement Job Order Costing Applying

PR 2B Entries and schedules for unfinished jobs and completed jobs x x 2 Challenging 1.5 hours Analytic FN – Measurement Job Order Costing Applying

TIF 1 Ethics in action n/a Moderate 15 min. Ethics FN – Measurement Job Order Costing Evaluating x x

TIF 2 Team activity n/a Moderate 45 min. Analytic FN – Measurement Job Order Costing Applying x

TIF 3 Communication n/a Easy 15 min. Analytic FN – Measurement Job Order Costing Evaluating x

Focus

Assoc Assets

Tagging