WHAT’S NEW IN THE EIGHTH EDITION:

There is a new In the News feature on “A Trip to Jekyll Island” and a new question in the

Problems and Applications section.

LEARNING OBJECTIVES:

By the end of this chapter, students should understand:

what money is and what functions money has in the economy.

what the Federal Reserve System is.

how the banking system helps determine the supply of money.

what tools the Federal Reserve uses to alter the supply of money.

468

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

29

THE MONETARY

SYSTEM

469 ❖ Chapter 29/The Monetary System

CONTEXT AND PURPOSE:

Chapter 29 is the <rst chapter in a two-chapter sequence dealing with money and prices in

the long run. Chapter 29 describes what money is and develops how the Federal Reserve

controls the quantity of money. Because the quantity of money in>uences the rate of

in>ation in the long run, the following chapter concentrates on the causes and costs of

in>ation.

The purpose of Chapter 29 is to help students develop an understanding of what money

is, what forms money takes, how the banking system helps create money, and how the

Federal Reserve controls the quantity of money. An understanding of money is important

because the quantity of money a?ects in>ation and interest rates in the long run, and

production and employment in the short run.

KEY POINTS:

The term money refers to assets that people regularly use to buy goods and services.

Money serves three functions. As a medium of exchange, it is the item used to make

transactions. As a unit of account, it provides the way to record prices and other

economic values. As a store of value, it o?ers a way to transfer purchasing power from

the present to the future.

Commodity money, such as gold, is money that has intrinsic value: It would be valued

even if it were not used as money. Fiat money, such as paper dollars, is money without

intrinsic value: It would be worthless if it were not used as money.

In the U.S. economy, money takes the form of currency and various types of bank

deposits, such as checking accounts.

The Federal Reserve, the central bank of the United States, is responsible for regulating

the U.S. monetary system. The Fed chair is appointed by the president and con<rmed by

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Chapter 29/The Monetary System ❖ 470

Congress every four years. The chair is the lead member of the Federal Open Market

Committee, which meets about every six weeks to consider changes in monetary policy.

Bank depositors provide resources to banks by depositing their funds into bank accounts.

These deposits are part of a bank’s liabilities. Bank owners also provide resources (called

bank capital) for the bank. Because of leverage (the use of borrowed funds for

investment), a small change in the value of a bank’s assets can lead to a large change in

the value of the bank’s capital. To protect depositors, bank regulators require banks to

hold a certain minimum amount of capital.

The Fed controls the money supply primarily through open-market operations. The

purchase of government bonds increases the money supply, and the sale of government

bonds decreases the money supply. The Fed also uses other tools to control the money

supply. It can expand the money supply by decreasing the discount rate, increasing its

lending to banks, lowering reserve requirements, or decreasing the interest rate on

reserves. It can contract the money supply by increasing the discount rate, decreasing

its lending to banks, raising reserve requirements or increasing the interest rate on

reserves.

When individuals deposit money in banks and banks loan out some of these deposits, the

quantity of money in the economy increases. Because the banking system in>uences the

money supply in this way, the Fed’s control of the money supply is imperfect.

The Federal Reserve has in recent years set monetary policy by choosing a target for the

federal funds rate, a short-term interest rate at which banks make loans to one another. As

the Fed achieves its target, it adjusts the money supply.

CHAPTER OUTLINE:

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

This is a good chapter to “win back” the students who were bored with

national income accounting. Students are generally interested in learning

more about the banking system and the Federal Reserve. The Federal

Reserve o?ers a free, 13-minute video entitled “The Fed Today” that

discusses the history and operations of the Fed.

471 ❖ Chapter 29/The Monetary System

I. The Meaning of Money

A. De<nition of money: the set of assets in an economy that people regularly

use to buy goods and services from other people.

B. The Functions of Money

1. Money serves three functions in our economy.

a. De<nition of medium of exchange: an item that buyers give to sellers

when they want to purchase goods and services.

b. De<nition of unit of account: the yardstick people use to post prices

and record debts.

c. De<nition of store of value: an item that people can use to transfer

purchasing power from the present to the future.

2. De<nition of liquidity: the ease with which an asset can be converted into

the economy’s medium of exchange.

a. Money is the most liquid asset available.

b. Other assets (such as stocks, bonds, and real estate) vary in their liquidity.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Begin the analysis by asking students, “What is money?” Students will

likely want to start right in with a discussion of the functions that money

serves. Stop them. Ask them instead to describe money. Hold up a dollar

bill and a piece of paper cut to the same size. Ask the students which they

Chapter 29/The Monetary System ❖ 472

c. When people decide how to allocate their wealth, they must balance the

liquidity of each possible asset against the asset’s usefulness as a store of

value.

C. The Kinds of Money

1. De<nition of commodity money: money that takes the form of a

commodity with intrinsic value.

2. De<nition of 3at money: money without intrinsic value that is used as

money because of government decree.

D. Money in the U.S. Economy

1. The quantity of money circulating in the United States is sometimes called the

money stock.

2. Included in the measure of the money supply are currency, demand deposits, and

other monetary assets.

a. De<nition of currency: the paper bills and coins in the hands of the

public.

b. De<nition of demand deposits: balances in bank accounts that

depositors can access on demand by writing a check.

3. Figure 1 shows the monetary assets included in two important measures of the

money supply, M1 and M2.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Figure 1

Point out to students that currency only makes up about 30% of the value

of M1, with the remaining 70% in the form of checking deposits. Students

need to understand that the majority of the money in the economy is

actually made up of account balances rather than stacks of currency in a

473 ❖ Chapter 29/The Monetary System

4. FYI: Why Credit Cards Aren’t Money

a. Credit cards are not a form of money; when a person uses a credit card, he or

she is simply deferring payment for the item.

b. Because using a debit card is like writing a check, the account balances that

lie behind debit cards are included in the measures of money.

5. Case Study: Where Is All the Currency?

a. If we divide the amount of outstanding currency in the United States by the

adult population, we <nd that the average adult holds over $5,500 in currency.

b. Of course, most adults carry a much smaller amount.

c. One explanation is that a great deal of U.S. currency may be held in other

countries.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Students are quite curious about whether credit cards are considered

money. You can satisfy their curiosity in part by pointing out that credit

cards actually lead to a drop in the quantity of money people need to

carry because they allow households to consolidate bills for payment once

Make sure that students realize that the assets included in M1 and M2

di?er in terms of their liquidity. Also note that there are other measures of

the money supply (M3 and MZM), which include less liquid assets like time

Chapter 29/The Monetary System ❖ 474

d. Another explanation is that large amounts of currency may be held by

criminals because transactions that use currency leave no paper trail.

II. The Federal Reserve System

A. De<nition of Federal Reserve (Fed): the central bank of the United States.

B. De<nition of central bank: An institution designed to oversee the banking

system and regulate the quantity of money in the economy.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

475 ❖ Chapter 29/The Monetary System

Activity 1—What Can Be Learned from a Dollar?

Type: In-class demonstration

Topics: Money, Federal Reserve

Materials needed: None

Time: 5 minutes

Class limitations: Works in any size class

Purpose

This activity introduces the role of the Federal Reserve in controlling the money

supply.

Instructions

Ask the class to take a dollar bill from wallets (or a $5, $10, $20, or $100).

Students without any currency can share with someone who does. Ask the class to

read the bill.

After a minute, ask them what they have learned.

Common Answers and Points for Discussion

Most students focus on the statement “This note is legal tender for all debts,

public and private.” This statement is the only “backing” U.S. currency has—the

note is not convertible into gold or silver. This can be used to introduce the

di?erence between <at money and commodity money.

C. The Fed’s Organization

1. The Fed was created in 1913 after a series of bank failures.

1. The Fed is run by a Board of Governors with 7 members who serve 14-year terms.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Highlight the Federal Reserve’s independence from the federal

government. Students are surprised to <nd that the Fed actually earns

more than enough to <nance its operations without being funded by

Chapter 29/The Monetary System ❖ 476

a. The Board of Governors has a chair who is appointed for a four-year term.

b. The current chair is Janet Yellen.

2. The Federal Reserve System is made up of 12 regional Federal Reserve Banks

located in major cities around the country.

3. One job performed by the Fed is the regulation of banks to ensure the health of

the nation’s banking system.

a. The Fed monitors each bank’s <nancial condition and facilitates bank

transactions by clearing checks.

b. The Fed also makes loans to banks when they want to borrow.

4. The second job of the Fed is to control the quantity of money available in the

economy.

a. De<nition of money supply: the quantity of money available in the

economy.

b. De<nition of monetary policy: the setting of the money supply by

policymakers in the central bank.

D. The Federal Open Market Committee

1. The Federal Open Market Committee (FOMC) consists of the 7 members of the

Board of Governors and 5 of the 12 regional bank presidents.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Have students pull out dollar bills and read the name of the city of the

district bank on the bill. However, make sure that they are actually

reading o? dollar bills and not just guessing the names of large cities.

Introduce students to the idea of open market operations here, but do not

be surprised if they do not catch on quickly. You can return to this topic

later in the chapter.

477 ❖ Chapter 29/The Monetary System

2. The primary way in which the Fed increases or decreases the number of dollars in

the economy is through open market operations (which involve the purchase or

sale of U.S. government bonds).

a. If the Fed wants to increase the supply of money, it creates dollars and uses

them to purchase government bonds from the public through the nation’s

bond markets.

b. If the Fed wants to reduce the supply of money, it sells government bonds

from its portfolio to the public. Money is then taken out of the hands of the

public and the supply of money falls.

III. Banks and the Money Supply

A. The Simple Case of 100-Percent-Reserve Banking

1. Example: Suppose that currency is the only form of money and the total amount

of currency is $100.

2. A bank is created as a safe place to store currency; all deposits are kept in the

vault until the depositor withdraws them.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

The process of money creation in the banking system is one of the more

diUcult things to teach at the Principles level. Nearly every aspect of the

process will be new to students and nothing is obvious or intuitive.

Therefore, it is extremely important that each step in the process is shown

through T-accounts so that students can see how the banking system

creates money as banks carry out their normal functions of accepting

Chapter 29/The Monetary System ❖ 478

a. De<nition of reserves: deposits that banks have received but have not

loaned out.

b. Under the example described above, we have 100-percent-reserve banking.

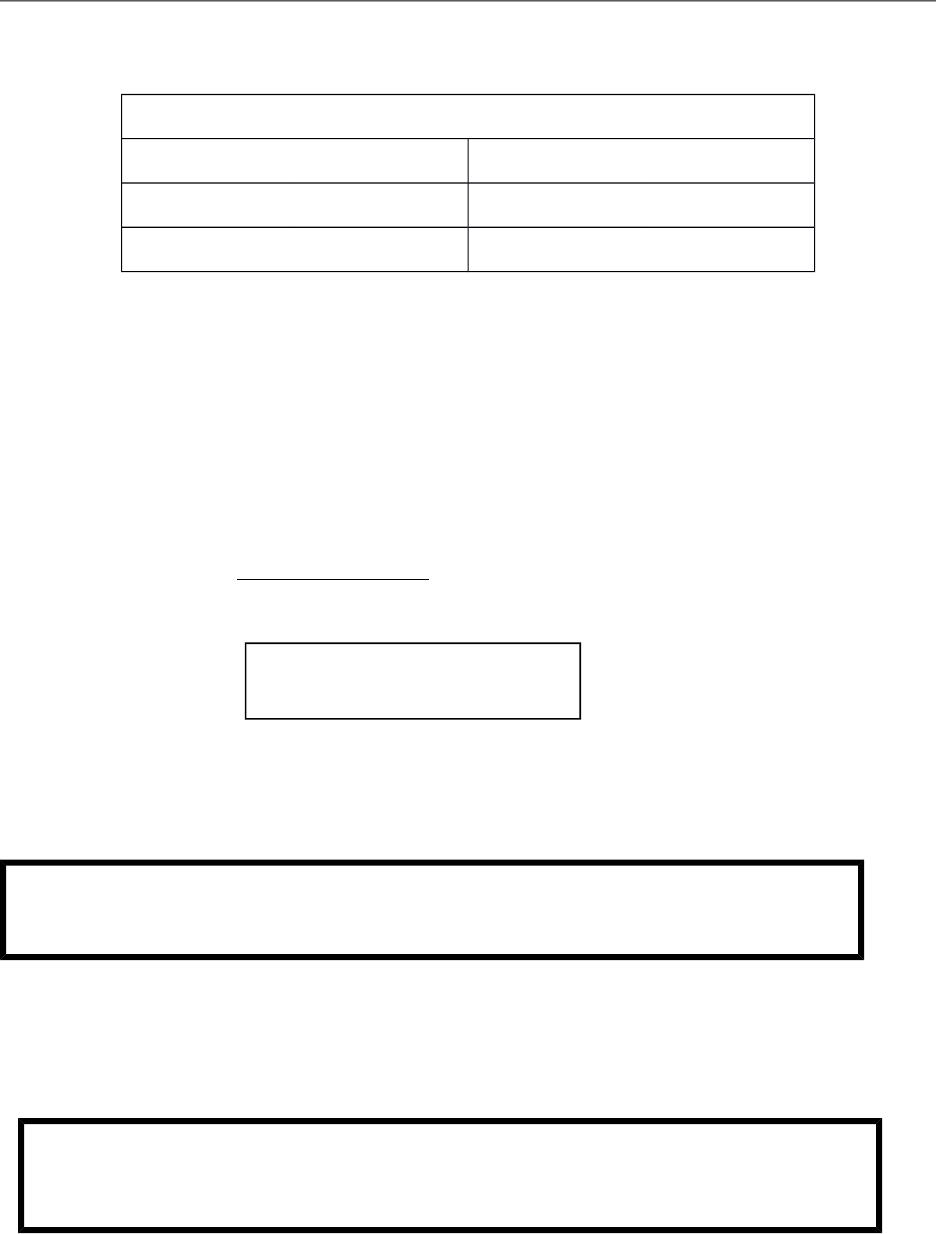

3. The <nancial position of the bank can be described with a T-account:

FIRST NATIONAL BANK

Assets Liabilities

Reserves $100.00 Deposits $100.00

4. The money supply in this economy is unchanged by the creation of a bank.

a. Before the bank was created, the money supply consisted of $100 worth of

currency.

b. Now, with the bank, the money supply consists of $100 worth of deposits.

5. This means that, if banks hold all deposits in reserve, banks do not in>uence the

supply of money.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Students will either catch on to T–accounts immediately or be completely

confused. It is a good idea to explain them and then let students work

together in small groups of two or three. You can check each group to

identify the students who will require individualized attention.

Make sure that you explain why bank reserves are an asset from the

bank’s perspective, but customer deposits are a liability.

479 ❖ Chapter 29/The Monetary System

B. Money Creation with Fractional-Reserve Banking

1. De<nition of fractional-reserve banking: a banking system in which banks

hold only a fraction of deposits as reserves.

2. De<nition of reserve ratio: the fraction of deposits that banks hold as

reserves.

3. Example: Same as before, but First National decides to set its reserve ratio equal

to 10% and lend the remainder of the deposits.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Chapter 29/The Monetary System ❖ 480

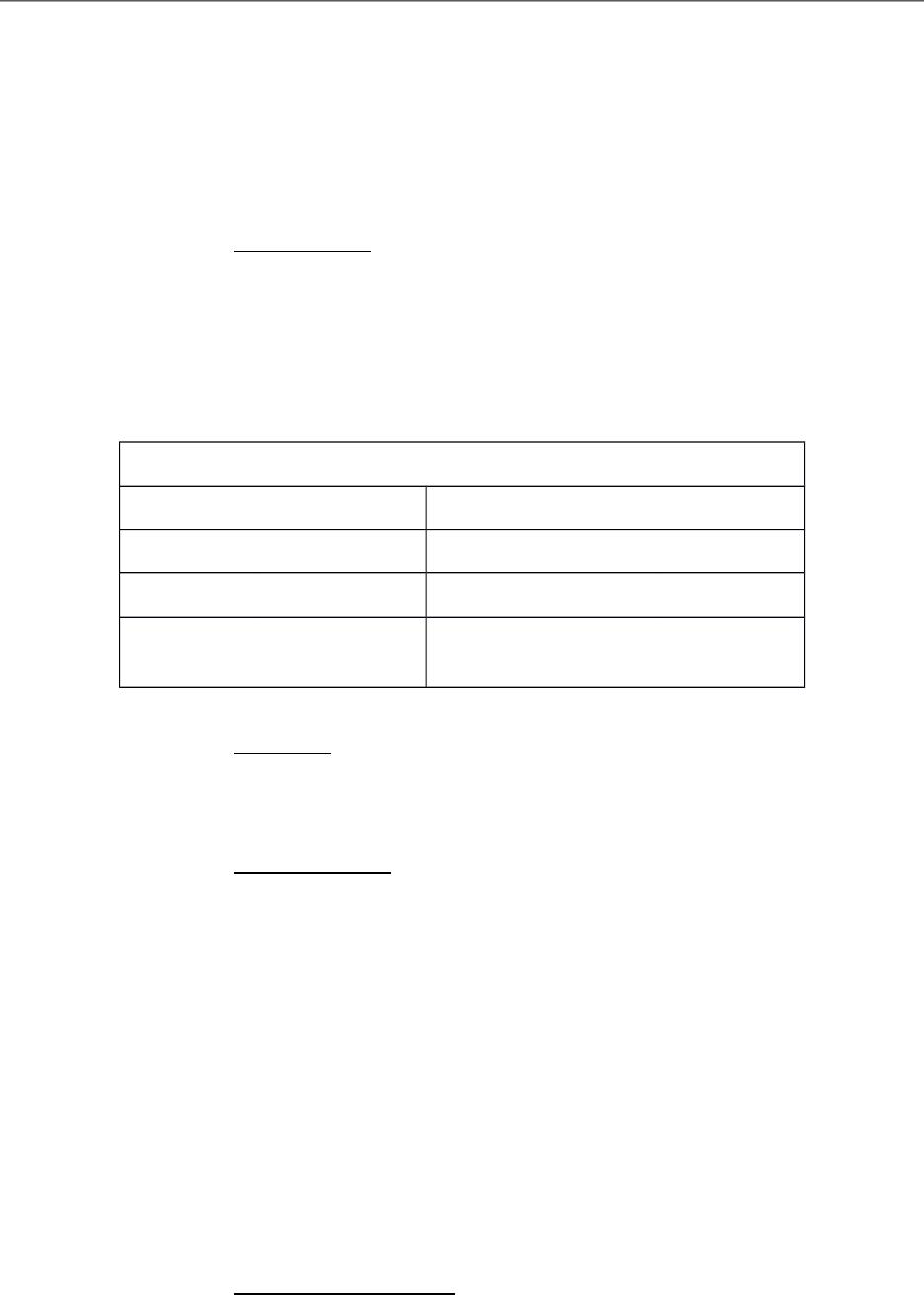

4. The bank’s T-account would look like this:

FIRST NATIONAL BANK

Assets Liabilities

Reserves $10.00 Deposits $100.00

Loans $90.00

5. When the bank makes these loans, the money supply changes.

a. Before the bank made any loans, the money supply was equal to the $100

worth of deposits.

b. Now, after the loans, deposits are still equal to $100, but borrowers now also

hold $90 worth of currency from the loans.

c. Therefore, when banks hold only a fraction of deposits in reserve, banks

create money.

6. Note that, while new money has been created, so has debt. There is no new

wealth created by this process.

C. The Money Multiplier

1. The creation of money does not stop at this point.

2. Borrowers usually borrow money to purchase something and then the money

likely becomes redeposited at a bank.

3. Suppose a person borrowed the $90 to purchase something and the funds then

get redeposited in Second National Bank. Here is this bank’s T-account (assuming

that it also sets its reserve ratio to 10%):

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

481 ❖ Chapter 29/The Monetary System

SECOND NATIONAL BANK

Assets Liabilities

Reserves $9.00 Deposits $90.00

Loans $81.00

4. If the $81 in loans becomes redeposited in another bank, this process will go on

and on.

5. Each time the money is deposited and a bank loan is created, more money is

created.

6. De<nition of money multiplier: the amount of money the banking system

generates with each dollar of reserves.

7. In our example, the money supply increased from $100 to $1,000 after the

establishment of fractional-reserve banking.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

ALTERNATIVE CLASSROOM EXAMPLE:

Reserve ratio = 12.5%

Spend some time showing students how the multiplier changes as reserve

requirements change. Make sure that you explain why the multiplier

changes when the reserve ratio changes. Students will catch on to the

math fairly quickly; it is the intuition that is most diUcult for them.

money multiplier 1/reserve ratio=

Chapter 29/The Monetary System ❖ 482

D. Bank Capital, Leverage, and the Financial Crisis of 2008–2009

1. In reality, banks also get funds from issuing debt and equity.

2. De<nition of bank capital: the resources a bank’s owners have put into

the institution.

3. A more realistic balance sheet for a bank:

MORE REALISTIC NATIONAL BANK

Assets Liabilities and Owners’ Equity

Reserves $200.00 Deposits $800.00

Loans $700.00 Debt $150.00

Securities $100.00 Capital (owner’s

equity)

$50.00

4. De<nition of leverage: the use of borrowed money to supplement existing

funds for purposes of investment.

5. De<nition of leverage ratio: the ratio of assets to bank capital.

a. The leverage ratio is $1,000/$50 = 20.

b. A leverage ratio of 20 means that, for every dollar of capital that has been

contributed by the owners, the bank has $20 of assets.

c. Because of leverage, a small change in assets can lead to a large change in

owner’s equity.

6. De<nition of capital requirement: a government regulation specifying a

minimum amount of bank capital.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

483 ❖ Chapter 29/The Monetary System

7. In 2008 and 2009, many banks realized they had incurred sizable losses on some

of their assets.

IV. The Fed’s Tools of Monetary Control

A. How the Fed In>uences the Quantity of Reserves

1. Open-Market Operations

a. De<nition of open-market operations: the purchase and sale of U.S.

government bonds by the Fed.

b. If the Fed wants to increase the supply of money, it creates dollars and uses

them to purchase government bonds from the public in the nation’s bond

markets.

c. If the Fed wants to lower the supply of money, it sells government bonds from

its portfolio to the public in the nation’s bond markets. Money is then taken

out of the hands of the public and the supply of money falls.

d. If the sale or purchase of government bonds a?ects the amount of deposits in

the banking system, the e?ect will be made larger by the money multiplier.

e. Open market operations are easy for the Fed to conduct and are therefore the

tool of monetary policy that the Fed uses most often.

2. Fed Lending to Banks

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

You may wish to use T-accounts to show the e?ects of an open market

purchase or sale. This way, students can see that the e?ect of an open

market operation can be quite large because of the money multiplier.

Chapter 29/The Monetary System ❖ 484

a. The Fed can also lend reserves to banks.

b. De<nition of discount rate: the interest rate on the loans that the Fed

makes to banks.

c. A higher discount rate discourages banks from borrowing from the Fed and

likely encourages banks to hold onto larger amounts of reserves. This in turn

lowers the money supply.

d. A lower discount rate encourages banks to lend their reserves (and borrow

from the Fed). This will increase the money supply.

e. In recent years, the Fed has set up new mechanisms for banks to borrow from

the Fed.

B. How the Fed In>uences the Reserve Ratio

1. Reserve Requirements

a. De<nition of reserve requirements: regulations on the minimum

amount of reserves that banks must hold against deposits.

b. This can a?ect the size of the money supply through changes in the money

multiplier.

c. The Fed rarely uses this tool because of the disruptions in the banking

industry that would be caused by frequent alterations of reserve

requirements. (It is also not e?ective when banks hold a lot of excess

reserves.)

2. Paying Interest on Reserves

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

485 ❖ Chapter 29/The Monetary System

a. In October of 2008, the Fed began paying banks interest on reserves.

b. The higher the interest rate, the more reserves a bank will want to hold. This

will reduce the money multiplier and the money supply.

C. Problems in Controlling the Money Supply

1. The Fed does not control the amount of money that consumers choose to deposit

in banks.

a. The more money that households deposit, the more reserves the banks have,

and the more money the banking system can create.

b. The less money that households deposit, the less reserves banks have, and

the less money the banking system can create.

2. The Fed does not control the amount that bankers choose to lend.

a. The amount of money created by the banking system depends on loans being

made.

b. If banks choose to hold onto a greater level of reserves than required by the

Fed (called excess reserves), the money supply will fall.

3. Therefore, in a system of fractional-reserve banking, the amount of money in the

economy depends in part on the behavior of depositors and bankers.

4. Because the Fed cannot control or perfectly predict this behavior, it cannot

perfectly control the money supply.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Chapter 29/The Monetary System ❖ 486

D. Case Study: Bank Runs and the Money Supply

1. Bank runs create a large problem under fractional-reserve banking.

2. Because the bank only holds a fraction of its deposits in reserve, it will not have

the funds to satisfy all of the withdrawal requests from its depositors.

3. Today, deposits are guaranteed through the Federal Depository Insurance

Corporation (FDIC).

Activity 2—Money Creation

Type: In-class demonstration

Topics: The banking system and deposit expansion

Materials needed: two volunteers, a paper with “$1,000” written on it

Time: 25 minutes

Class limitations: Works in any size class

Purpose:

This activity demonstrates the role of the banking system in expanding the money

supply.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

487 ❖ Chapter 29/The Monetary System

The Federal Reserve also conducts open-market operations. Use the $1,000 paper

to buy a baseball cap from a student. (Explain that the Fed actually buys

government bonds from the public because the market for used baseball caps is

small.)

The capless student now has $1,000 to spend with any other member of the class.

This student receives $1,000 and puts it in the bank of his or her choice.

The bank now has $1,000 in deposits (a liability) and $1,000 in cash (an asset).

The bank needs to keep $200 in reserve (20%) but can loan the other $800. Have

the banker tear o? 20% of the bill and give the rest to another student.

Revise the banks’ balance sheets.

Now the borrower spends the $800 and the recipient deposits it in a bank. This

bank now has $800 in deposits and $800 in cash. Of that, $160 needs to be kept

in reserve and $640 can be lent. Have the banker save 20% of the paper and give

the rest to another eager borrower.

Revise the banks’ balance sheets.

E. The Federal Funds Rate

1. De<nition of federal funds rate: the short-term interest rate that banks

charge one another for loans.

2. When the federal funds rate rises or falls, other interest rates often move in the

same direction.

3. In recent years, the Fed has set a target for the federal funds rate.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.

Chapter 29/The Monetary System ❖ 488

F. In the News: A Trip to Jekyll Island

1. In spite of many examples of its positive e?ects on the economy, the Fed still

faces public scorn and mistrust.

2. This Los Angeles Times article describes the story of the creation of the Fed and

the public’s paranoia associated with the central bank.

© 2018 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise

on a password-protected website or school-approved learning management system for classroom use.