Chapter 9 CFIN5

Chapter 9 Solutions

9-1

6

1

1(1.10)

Value PV of CFs 36,950 36,950(4.355261) 160,926.88

0.10

é ù

–

ê ú

ê ú

= = = =

ê ú

ê ú

ë û

9-2 a.

4

1

1(1.16)

Value PV of CFs 104,000 104,400(2.798181) 292,130.06

0.16

é ù

–

ê ú

ê ú

= = = =

ê ú

ê ú

ë û

b.

4

1

1(1.12)

Value PV of CFs 104,000 104,400(3.037349) 317,099.27

0.12

é ù

–

ê ú

ê ú

= = = =

ê ú

ê ú

ë û

9-3

10

1

1(1.11)

NPV 3,600,000 600,000 0.11

é ù

–

ê ú

ê ú

=- + ê ú

ê ú

ë û

3,600,000 600,000(5.889232) 3,600,000 3,533,539.21 66,460.79=- + =- + =-

Calculator solution: CF0 = -3,600,000, CF1 – CF10 =600,000, I = 11; compute NPV = -66,460.79; IRR =

10.56%

Alternative calculator solution using TVM keys: N = 10, PV = -3,600,000, PMT = 600,000, FV = 0;

compute I/Y = 10.56% = IRR

The investment is not acceptable, because NPV < 0 and IRR < r = 11%.

9-4

5

1

1(1.09)

NPV 42,000 11,000 0.09

é ù

–

ê ú

ê ú

=- + ê ú

ê ú

ë û

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 9 CFIN5

9-5

3

1

1(1 IRR)

20,070 8,500 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

9-6

6

1

1(1 IRR)

74,000 16,500 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

9-7 a.

4

1

1(1.14)

NPV 75,000 26,000 0.14

é ù

–

ê ú

ê ú

=- + ê ú

ê ú

ë û

b.

4

1

1(1 IRR)

75,000 26,000 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

c. Because IRR > r = 14% and NPV > 0, the project is acceptable.

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 9 CFIN5

9-8 a.

3

1

1(1.12)

NPV 34,000 14,150 0.12

é ù

–

ê ú

ê ú

=- + ê ú

ê ú

ë û

b.

3

1

1(1 IRR)

34,000 14,150 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

c. Because IRR < r = 12% and NPV < 0, the project is not acceptable; but, just barely.

9-9 Data for NPV profile: Cost = 64,000, CF = 18,200 for five years

r NPV

0.00 $27,000.00

0.01 24,332.45

0.02 21,784.96

0.03 19,350.67

0.04 17,023.17

0.05 14,796.48

0.06 12,665.02

0.07 10,623.59

0.08 8,667.32

0.09 6,791.65

0.10 4,992.32

0.11 3,265.33

0.12 1,606.93

0.13 13.61

0.14 (1,517.93)

0.15 (2,990.78)

0.16 (4,407.86)

0.17 (5,771.90)

0.18 (7,085.49)

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 9 CFIN5

9-10. MIRR:

PV of Cash FV in Year 3 of

Year

CF Outflows @ 12% Cash Inflows @ 12%

0 (82,000) (82,000.00)

1 35,000 43,904.00

2 70,000 78,400.00

The investment is not acceptable, because MIRR < r = 12%.

9-11 IRR:

4

1

1(1 IRR)

5,500 1,800 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

NPV ($)

Chapter 9 CFIN5

9-12 IRR:

2

1

1(1 IRR)

90,000 54,000 IRR

é ù

–

ê ú

+

ê ú

=ê ú

ê ú

ë û

9-13 Traditional payback:

Year

CF CF

0 -270,000 -270,000

1 75,000 -195,000

2 75,000 -120,000

3 75,000 -45,000

4 75,000 30,000

5 75,000 105,000

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 9 CFIN5

45,000

PB 3 3.6 years

75,000

= + =

Alternative solution: Because the future cash flows represent an annuity, PB can be computed as

follows:

270,000

PB 3.6 years

75,000

= =

Discounted payback:

Year

CF PV of CF @ 11% PV of CF

0 (270,000) (270,000.00) (270,000.00)

1 75,000 67,567.57 (202,432.43)

2 75,000 60,871.68 (141,560.75)

3 75,000 54,839.35 (86,721.40)

4 75,000 49,404.82 (37,316.57)

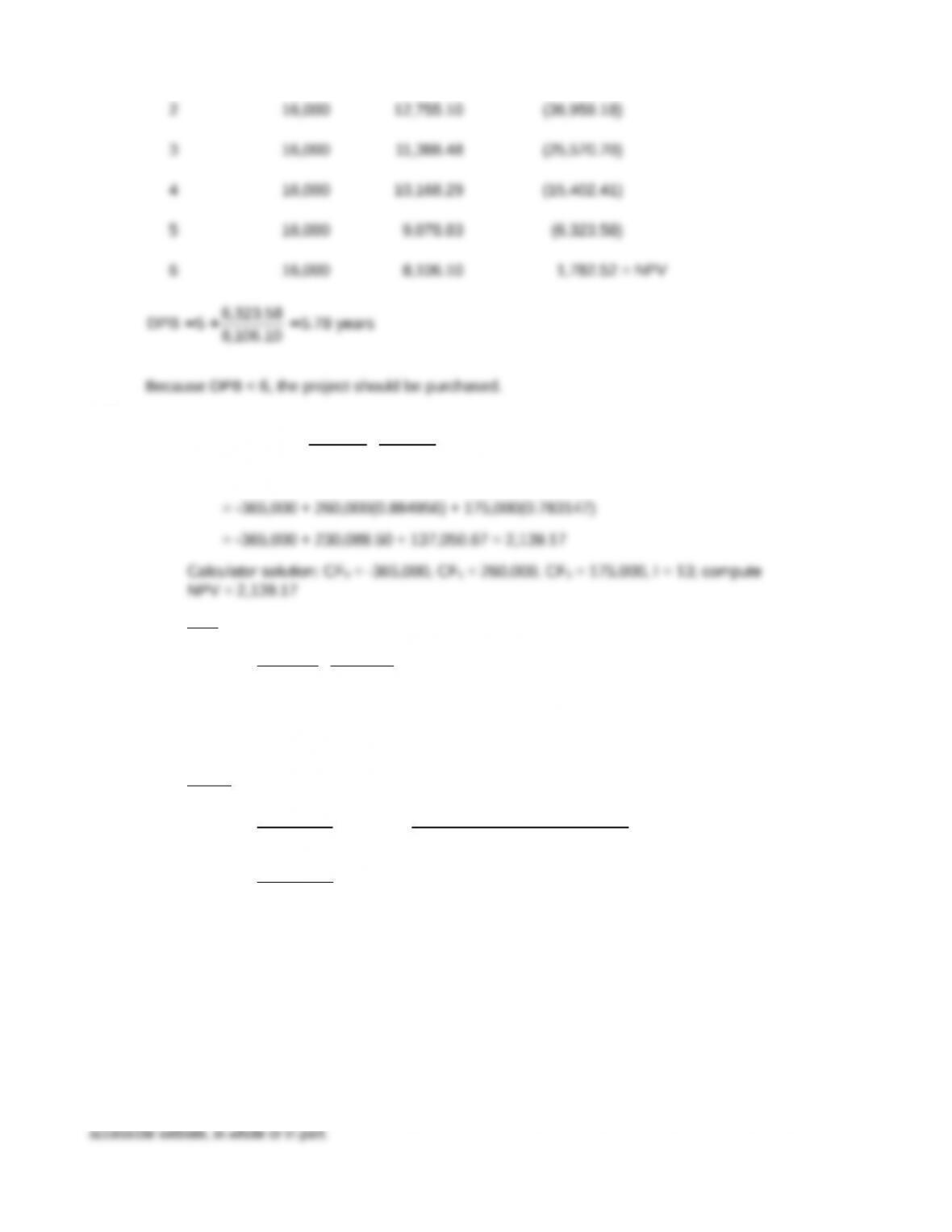

5 75,000 44,508.85 7,192.28 = NPV

37,316.57

DPB 4 4.84 years

44,508.58

= + =

Because DPB < 5, the project should be purchased.

9-14 Traditional payback:

Year

CF CF

0 -64,000 -64,000

1 16,000 -48,000

2 16,000 -32,000

3 16,000 -16,000

Chapter 9 CFIN5

9-15 a.

1 2

260,000 175,000

NPV 365,000 (1.13) (1.13)

=- + +

b. IRR:

1 2

260,000 175,000

365,000 (1 IRR) (1 IRR)

= +

+ +

Calculator solution: CF0 = -365,000, CF1 = 260,000, CF2 = 175,000, I = 13; compute

IRR = 13.48%

c. MIRR:

1 0

n 2

2

TV 260,000(1.13) 175,000(1.13)

Cost 365,000

(1 MIRR) (1 MIRR)

468,800

365,000 (1 MIRR)

+

= = =

+ +

=+

Calculator solution: N =2, PV = -365,000, PMT = 0, FV = 468,800; compute I/Y = 13.33% = MIRR

The investment is acceptable, because MIRR > r = 13%.

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 9 CFIN5

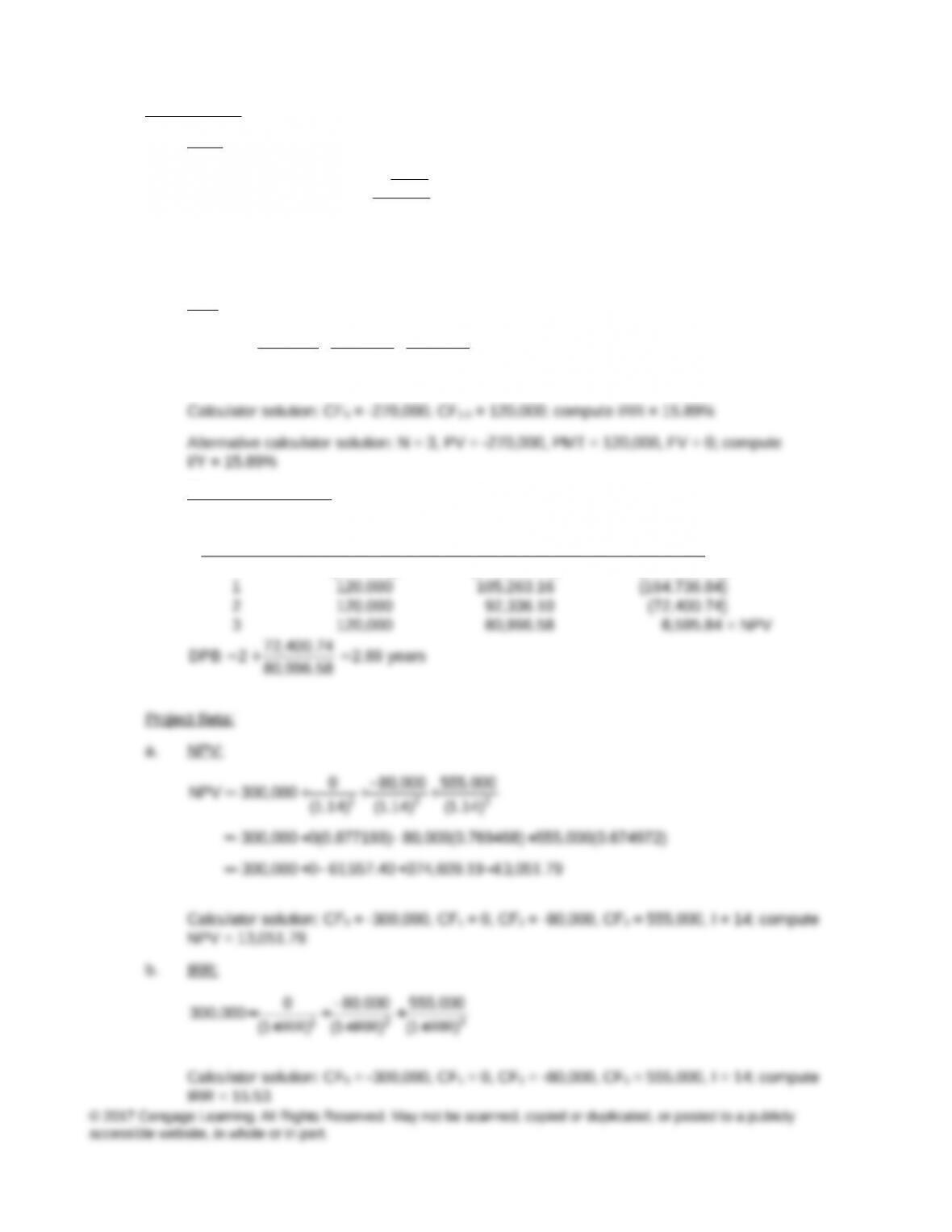

9-16 Project Alpha:

a. NPV:

1

3

(1.14)

1

NPV 270,000 120,000 270,000 120,000(2.321632) 8,595.84

0.14

é ù

–

ê ú

=- + =- + =

ê ú

ê ú

ë û

Calculator solution: CF0 = -270,000, CF1-3 = 120,000, I = 14; compute NPV = 8,595.84

b. IRR:

1 2 3

120,000 120,000 120,000

270,000 (1 IRR) (1 IRR) (1 IRR)

= + +

+ + +

c. Discounted payback:

Year CF PV of CF @ 12% PV of C

0 (270,000) (270,000.00) (270,000.00)

Chapter 9 CFIN5

c. Discounted payback:

Year CF PV of CF @ 12% PV of C

0 (300,000) (300,000.00) (300,000.00)

1 0 0.00 (300,000.00)

9-17 Project AB:

a. NPV:

é ù

–

ê ú

=- + =- + =

ê ú

ê ú

ë û

1

3

(1.13)

1

NPV 90,000 39,000 90,000 39,000(2.361153) 2,084.95

0.13

b. IRR:

= + +

+ + +

1 2 3

39,000 39,000 39,000

90,000 (1 IRR) (1 IRR) (1 IRR)

c. MIRR:

é ù

–

ê ú

ê ú

+ + ë û

= = = =

+ + +

= =

+ +

3

2 1 0

n 3 3

3 3

(1.13) 1

39,000 0.13

TV 39,000(1.13) 39,000(1.13) 39,000(1.13)

Cost 90,000

(1 MIRR) (1 MIRR) (1 MIRR)

39,000(3.4069) 132,869.10

90,000 (1 MIRR) (1 MIRR)

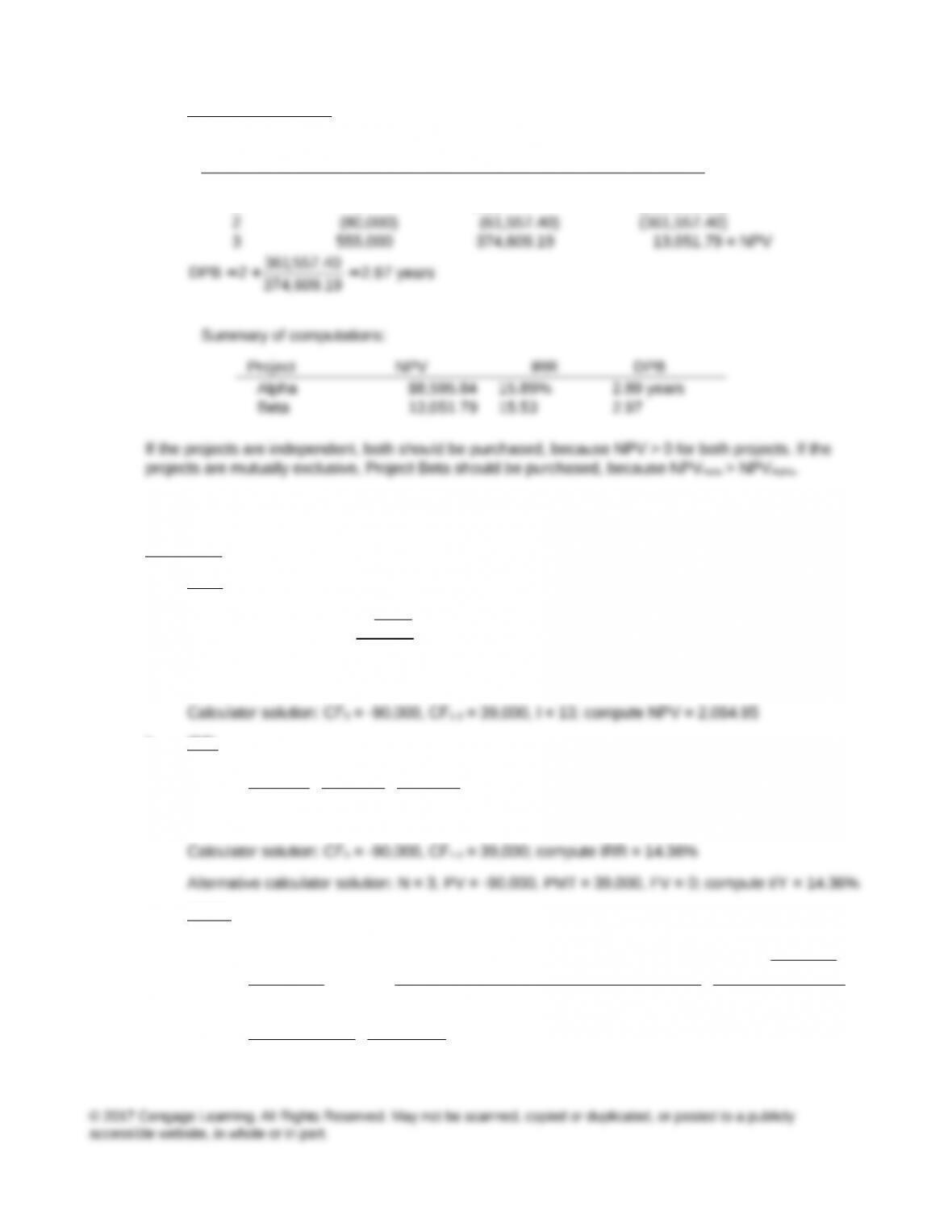

Chapter 9 CFIN5

d. Discounted payback:

Year CF PV of CF @ 13% PV of C

0 (90,000) (90,000.00) (90,000.00)

1 39,000 34,513.27 (55,486.73)

Chapter 9 CFIN5

Year CF PV of CF @ 13% PV of C

0 (100,000) (100,000.00) (100,000.00)

1 0 0.00 (100,000.00)

Chapter 9 CFIN5

= + =

66,857.90

DPB 2 2.96 years

69,305.02

Summary of computations:

Project NPV IRR MIRR DPB

AB $2,084.95 14.36% 13.87% 2.92 years

LM 2,224.90 13.83 13.83 2.98

UV 2,447.12 13.89 13.63 2.96

If the projects are independent, all should be purchased, because NPV > 0 for all of the projects. If the

projects are mutually exclusive, Project UV should be purchased, because NPVUV > NPVLM > NPVAB.

9-18 NPV:

=- + + =- + +

=- + + =

S1 2

14,000 6,000

NPV 16,000 16,000 14,000(0.862069) 6,000(0.743163)

(1.16) (1.16)

16,000 12,068.97 4,458.98 527.95

Calculator solution: CF0 = -16,000, CF1 = 14,000, CF2 = 6,000, I = 16; compute NPV = 527.94

=- + + =- + +

=- + + =

T1 2

2,000 18,600

NPV 15,000 15,000 2,000(0.862069) 18,600(0.743163)

(1.16) (1.16)

15,000 1,724.14 13,822.83 546.97

Calculator solution: CF0 = -15,000, CF1 = 2,000, CF2 = 18,600, I = 16; compute NPV = 546.97 NPVT =

546.97 > NPVS = 527.94, thus Project T is the project that should be purchased.

IRR:

= +

+ +

1 2

2,000 18,600

15,000 (1 IRR) (1 IRR)

Calculator solution: CF0 = -15,000, CF1 = 2,000, CF2 = 18,600, compute IRR = 18.22%

Note: Students who use the projects’ IRRs to determine which project should be purchased would

choose Project S, because its IRR is 19.01 percent (Calculator solution: CF0 = -16,000, CF1 = 14,000,

CF2 = 6,000, compute IRR = 19.01%); thus, IRRS > IRRT. But, Project S should not be purchased

because its NPV is lower than Project T’s NPV; that is NPVS < NPVT.

9-19 a. Because they are independent and both projects have positive NPVs, both projects are

b. When a project has a positive NPV, we know that it is acceptable using both the NPV technique

9-20 a. Because all of the capital budgeting techniques listed in the table are based on time value of

money (TVM) concepts, they all must agree with respect to the accept/reject decision. The

Chapter 9 CFIN5

b. Because IRR > r when a project is acceptable and IRR < r when a project is not acceptable, the

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.