Chapter 16 CFIN5

Chapter 16 Solutions

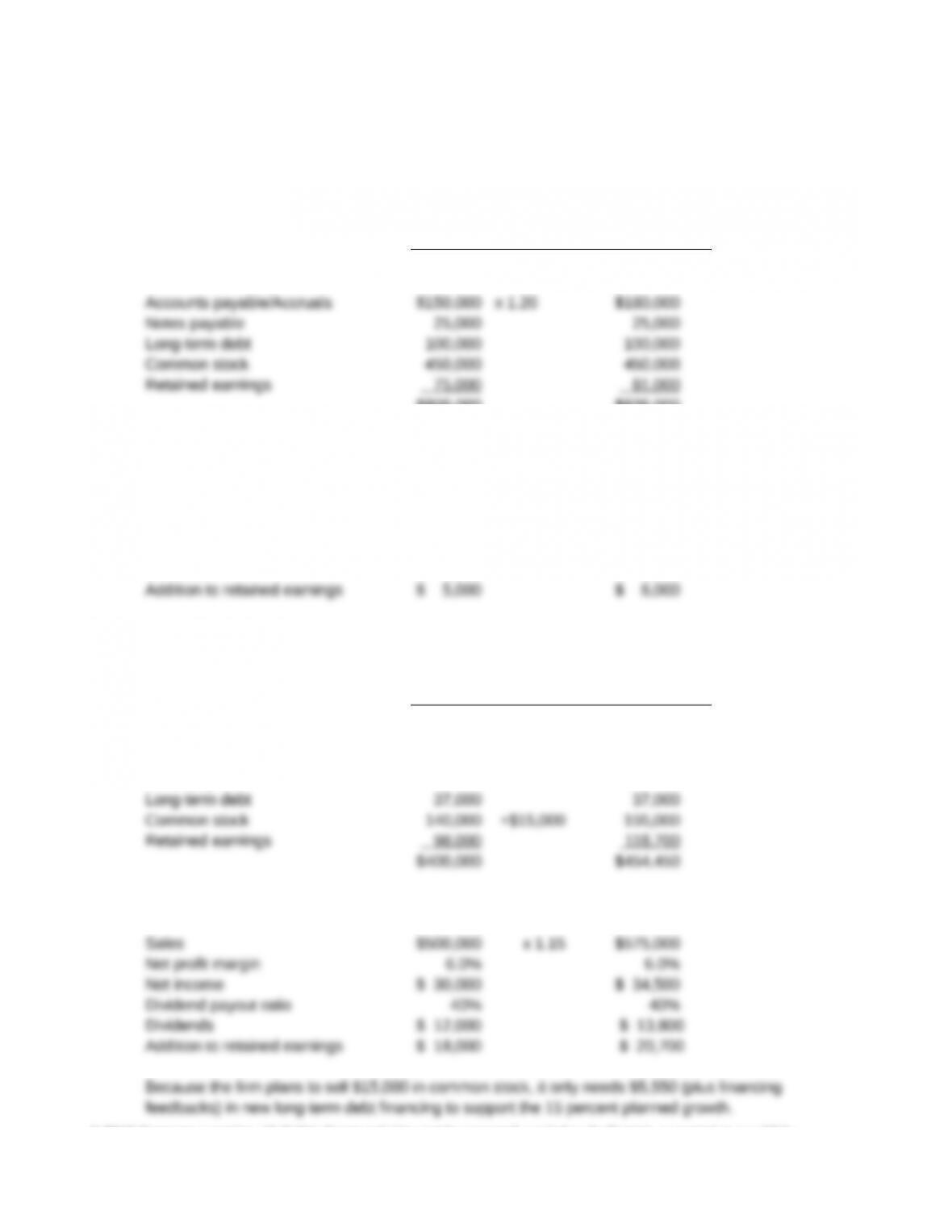

16-1 The following table shows the initial forecast and the AFN:

Current Growth Initial Forecast

Total assets $800,000 x 1.20 $960,000

$800,000 $836,000

AFN $124,000

Sales $250,000 x 1.20 $300,000

Net profit margin 5.0% 5.0%

Net income $ 12,500 $ 15,000

Dividend payout ratio 60% 60%

Dividends $ 7,500 $ 9,000

16-2 The following table shows the initial forecast and the AFN:

Current Growth Initial Forecast

Total assets $400,000 x 1.15 $460,000

Accounts payable $125,000 x 1.15 $143,750

Notes payable 0 0

AFN $ 5,550

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 16 CFIN5

16-3

$810,000

Full capacity sales $900,000

0.90

= =

16-4

$5,400,000

Full capacity sales $9,000,000

0.60

= =

% increase in sales = ($9,000,000 – $5,400,000)/$5,400,000 = 0.66667 = 66.67%

16-5

OpBE

F $1,500

= = = 200 units

QP – V $25.00 $17.50–

SOpBE = 200 x $25 = $5,000 =

( )

()

F $1,500 $1,500

= =

$17.50

V0.30

1 – 1

P$25.00

–

16-6 a.

OpBE

F $600,000

= = = 6,000 units

QP – V $250 $150–

Chapter 16 CFIN5

b.

OpBE

F $900,000

= = = 45,000 units

QP – V $45 $25–

SOpBE = 45,000 x $45 = $2,025,000 =

( )

()

F $900,000 $900,000

= =

$25

V0.444444

1 – 1

P$45

–

16-8 Selling price = $575

Fixed operating costs = $690,000

Variable operating costs = 70% x Sales

a. Sales = 6,000 machines:

Gross profit 6,000[$575 $575(0.7)] $1,035,000

DOL 3.0

EBIT 6,000[$575 $575(0.7)] $690,000 $345,000

–

= = = =

– –

b. Sales = 9,000 machines:

Gross profit 9,000[$575 $575(0.7)] $1,552,500

DOL 1.8

EBIT 9,000[$575 $575(0.7)] $690,000 $862,500

–

= = = =

– –

c. Sales = 12,000 machines:

Gross profit 12,000[$575 $575(0.7)] $2,070,000

DOL 1.5

EBIT 12,000[$575 $575(0.7)] $690,000 $1,380,000

–

= = = =

– –

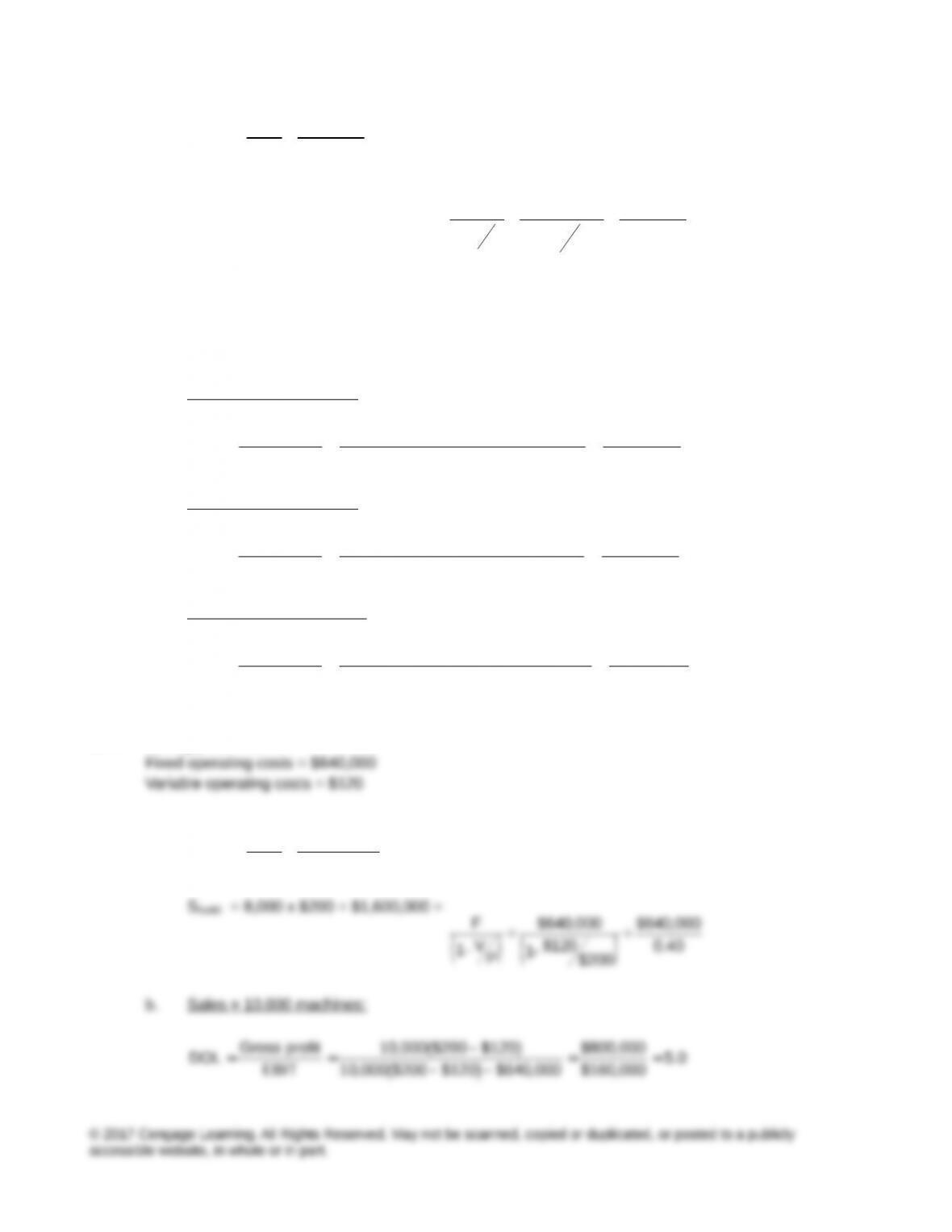

16-9 Selling price = $200

a.

OpBE

F $640,000

= = = 8,000 units

QP – V $200 $120–

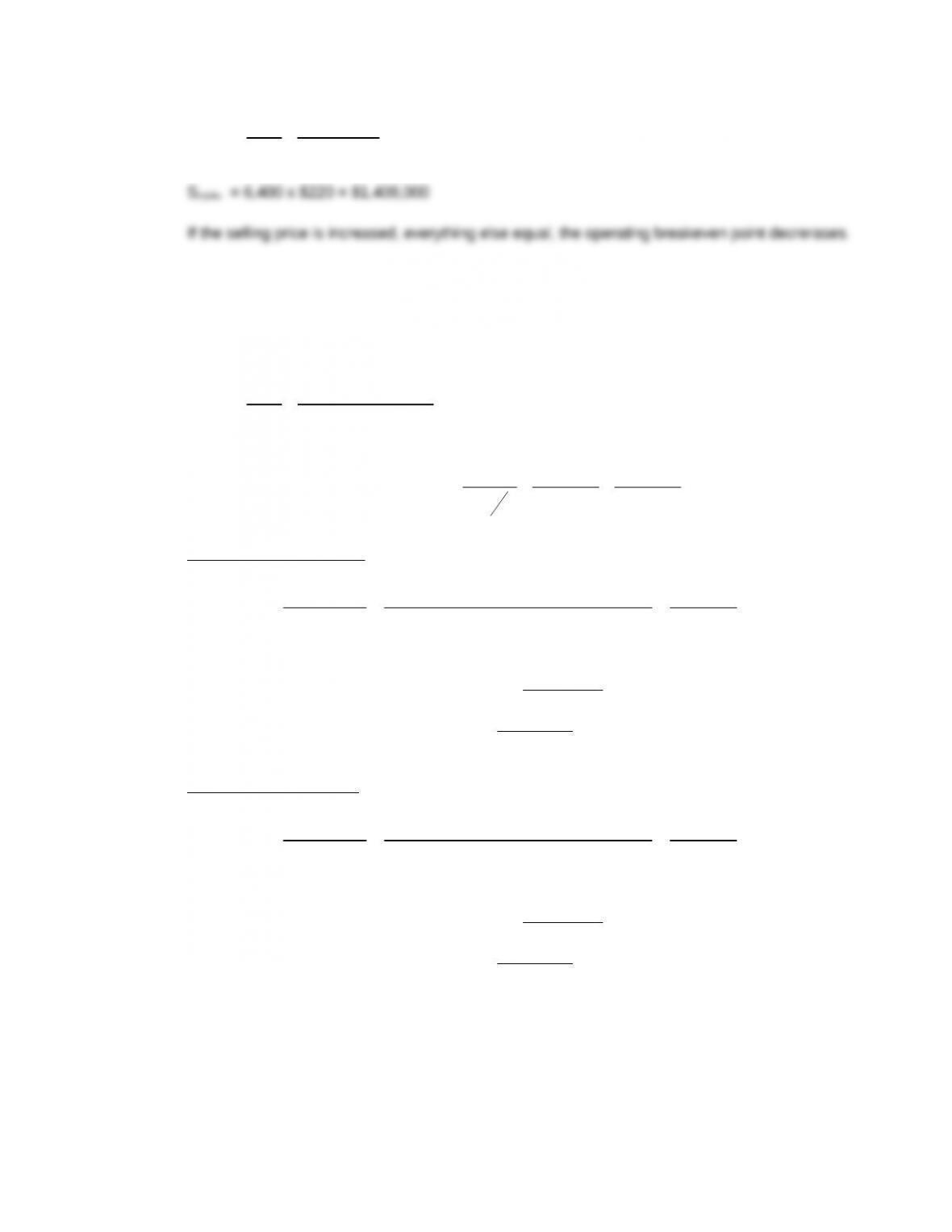

Chapter 16 CFIN5

c.

OpBE

F $640,000

= = = 6,400 units

QP – V $220 $120–

16-10 Selling price = $1,400

Fixed operating costs = $420,000

Variable operating costs = 80% of sales

a.

OpBE

F $420,000

= = = 1,500 units

QP – V $1,400 $1,400(0.8)–

SOpBE = 1,500 x $1,400 = $2,100,000 =

( )

( )

F $420,000 $420,000

= =

V 1 0.80 0.20

1 – P–

b. ODM: Sales = 2,000 units

=

–

= = = =

– –

Q 2,000

Gross profit 2,000[$1,400 $1,400(0.8)] $560,000

DOL 4.0

EBIT 2,000[$1,400 $1,400(0.8)] $420,000 $140,000

Sales = 2,000 x $1,400 $2,800,000

Variable CGS = 2,000 x ($1,400)(0.8) (2 ,240,000)

Gross profit $ 560,000

Fixed operating costs ( 420 ,000)

EBIT = NOI $ 140,000

CWI: Sales = 2,500 units

=

–

= = = =

– –

Q 2,500

Gross profit 2,500[$1,400 $1,400(0.8)] $700,000

DOL 2.5

EBIT 2,500[$1,400 $1,400(0.8)] $420,000 $280,000

Sales = 2,500 x $1,400 $3,500,000

Variable CGS = 2,500 x ($1,400)(0.8) (2 ,800,000)

Gross profit $ 700,000

Fixed operating costs ( 420 ,000)

EBIT = NOI $ 280,000

NOICWI > NOIODM, which shows that ODM is operating closer to its operating breakeven point.

ODM’s higher DOL indicates that it is operating closer to its operating breakeven point.

16-11 EBITFinBE = $100,000(0.10) + $240,000(0.08) = $10,000 + $19,200 = $29,200

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 16 CFIN5

16-12 Interest = $15,000(0.09) + $48,000(0.06) = $1,350 + $2,880 = $4,230

16-13 a. EBIT $99,000

Interest (33 ,000)

Chapter 16 CFIN5

a.

(EBIT I)(1 T) ($2,250 $1,000)(1 0.4) $750

EPS $1.50

# common shares 500 500

– – – –

= = = =

b.

EBIT $2,250

DFL 1.8

EBT $2,250 $1,000

= = =

–

16-16 DOL = 3.5

DFL = 2.0

a. DTL = DOL x DFL = 3.5 x 2.0 = 7.0

b. If sales are 5 percent lower than expected,

16-17 DFL = 4.0

DTL = 10.0

Sales = $600,000

Profit margin = 8%

a. DTL = DOL x DFL

b. Forecasted net = $600,000 x 0.08 = $48,000

16-18 Sales = $400,000

EBIT = $125,000

DOL = 2.0

DFL = 4.0

EPS = $2.50

If sales turn out to be $360,000 rather than $400,000, actual sales will be 10 percent lower than

expected:

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.

Chapter 16 CFIN5

16-19 Selling price = $180

Variable cost per unit = $135

Fixed operating costs = $371,250

Chapter 16 CFIN5

Gross profit 65,000($10.00 $7.50) $162,500

DTL 6.5 2.6 2.5

EBT 65,000($10.00 $7.50) $100,000 $37,500 $25,000

–

= = = = = ´

– – –

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly

accessible website, in whole or in part.