1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

22

23

24

25

26

27

b. What is the market interest rate on Jana’s debt and what is the component cost of this debt for WACC purposes?

34

35

36

37

38

(5) Jana’s target capital structure is 30% long-term debt, 10% preferred stock, and 60% common equity.

expected to grow at a constant rate of 5.8% in the foreseeable future. Jana’s beta is 1.2, the yield on T-bonds is 5.6%,

and the market risk premium is estimated to be 6%. For the own-bond-yield-plus-judgmental-risk-premium approach,

the firm uses a 3.2% judgmental risk premium.

39

46

47

48

49

50

51

A B C D E F G H I

10/28/2015

Situation

COST OF DEBT, rd

N30

PV 1,153.72

PMT 60

B-T rd10%

Tax rate 40%

A-T rd =(1 – Tax rate) x (B-T rd)

A-T rd =60% x10%

Chapter 9. Mini Case

(1) The firm’s tax rate is 40%.

(2) The current price of Jana’s 12% coupon, semiannual payment, noncallable bonds with 15 years remaining to

maturity is $1,153.72. Jana does not use short-term interest-bearing debt on a permanent basis. New bonds would be

privately placed with no flotation cost.

To help you structure the task, Leigh Jones has asked you to answer the following questions.

During the last few years, Jana Industries has been too constrained by the high cost of capital to make many capital

investments. Recently, though, capital costs have been declining, and the company has decided to look seriously at a

major expansion program that has been proposed by the marketing department. Assume that you are an assistant to

Leigh Jones, the financial vice president. Your first task is to estimate Jana’s cost of capital. Jones has provided you

with the following data, which she believes may be relevant to your task:

a. (1.) What sources of capital should be included when you estimate Jana’s weighted average cost of capital

(WACC)? Answer: See Chapter 9 PowerPoint file.

(3) The current price of the firm’s 10%, $100 par value, quarterly dividend, perpetual preferred stock is $116.95. Jana

would incur flotation costs equal to 5% of the proceeds on a new issue.

(4) Jana’s common stock is currently selling at $50 per share. Its last dividend (D0) was $3.12, and dividends are

(2.) Should the component costs be figured on a before-tax or an after-tax basis? Answer: See Chapter 9

54

55

56

57

58

59

60

61

Flotation costs 5%

66

67

68

69

70

71

Preferred stock carries a higher risk to investors than debt. Companies are not required to pay preferred dividends

73

74

will be difficulty raising additional funds, and preferred stockholders may gain control of the firm.

78

79

80

81

82

88

89

90

91

92

93

94

96

97

99

100

101

102

103

104

105

110

111

112

113

A B C D E F G H I

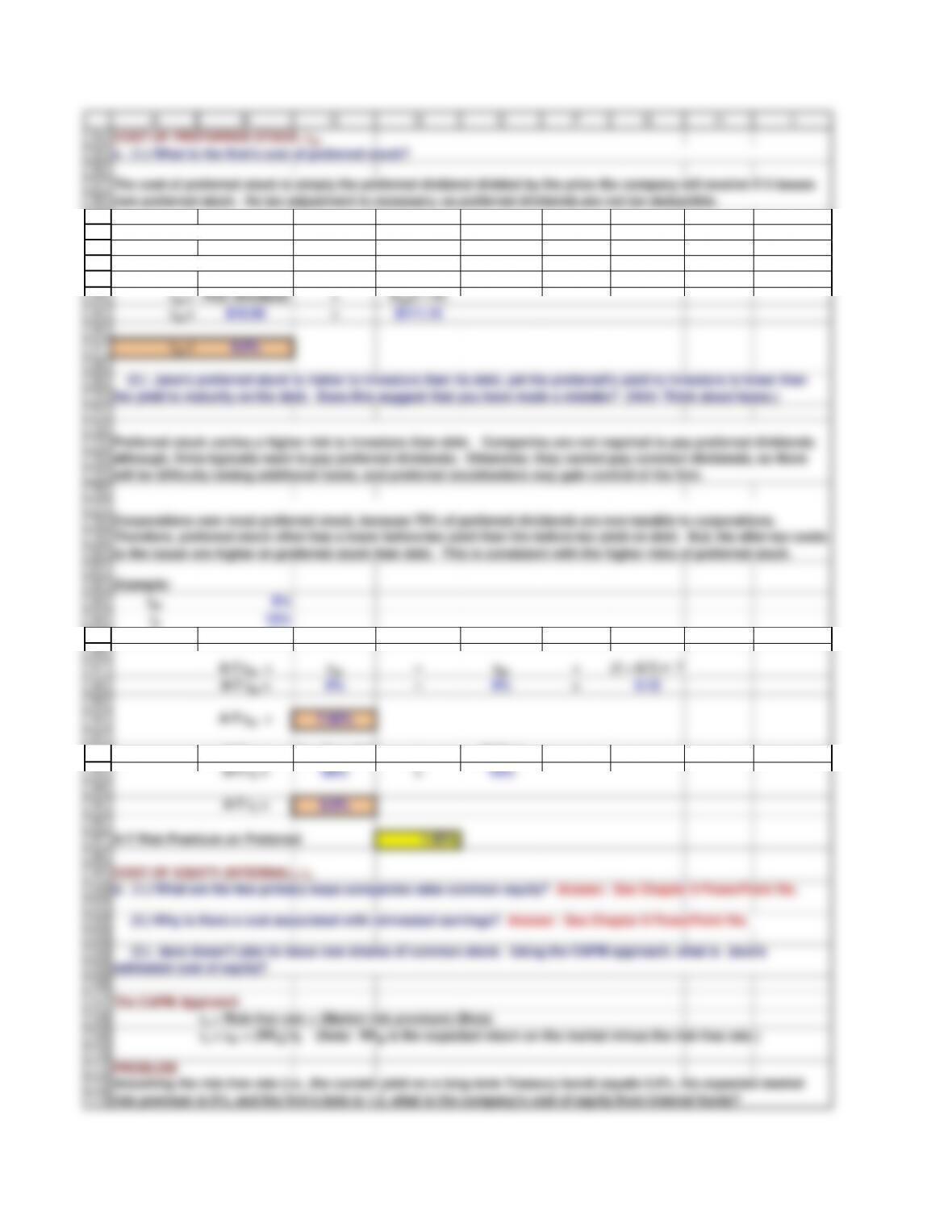

COST OF PREFERRED STOCK, rps

Pref. Dividend $10.00

Pref. Price $116.95

rps =9.0%

Example:

A-T rps = 9% –9% ×0.12

A-T rps = 7.92%

A-T rd = (1 – Tax rate) × (B-T rd)

A-T rd = 60% ×10%

A-T Risk Premium on Preferred 1.92%

COST OF EQUITY (INTERNAL), rs

PROBLEM

The cost of preferred stock is simply the preferred dividend divided by the price the company will receive if it issues

new preferred stock. No tax adjustment is necessary, as preferred dividends are not tax deductible.

Corporations own most preferred stock, because 70% of preferred dividends are non-taxable to corporations.

Therefore, preferred stock often has a lower before-tax yield than the before-tax yield on debt. But, the after-tax costs

to the issuer are higher on preferred stock than debt. This is consistent with the higher risks of preferred stock.

(2.) Jana’s preferred stock is riskier to investors than its debt, yet the preferred’s yield to investors is lower than

the yield to maturity on the debt. Does this suggest that you have made a mistake? (Hint: Think about taxes.)

although, firms typically want to pay preferred dividends. Otherwise, they cannot pay common dividends, so there

Assuming the risk-free rate (i.e., the current yield on a long-term Treasury bond) equals 5.6%, the expected market

risk premium is 6%, and the firm’s beta is 1.2, what is the company’s cost of equity from internal funds?

d. (1.) What are the two primary ways companies raise common equity? Answer: See Chapter 9 PowerPoint file.

(2.) Why is there a cost associated with reinvested earnings? Answer: See Chapter 9 PowerPoint file.

(3.) Jana doesn’t plan to issue new shares of common stock. Using the CAPM approach, what is Jana’s

estimated cost of equity?

c. (1.) What is the firm’s cost of preferred stock?

114

115

116

117

118

119

120

123

124

125

126

127

128

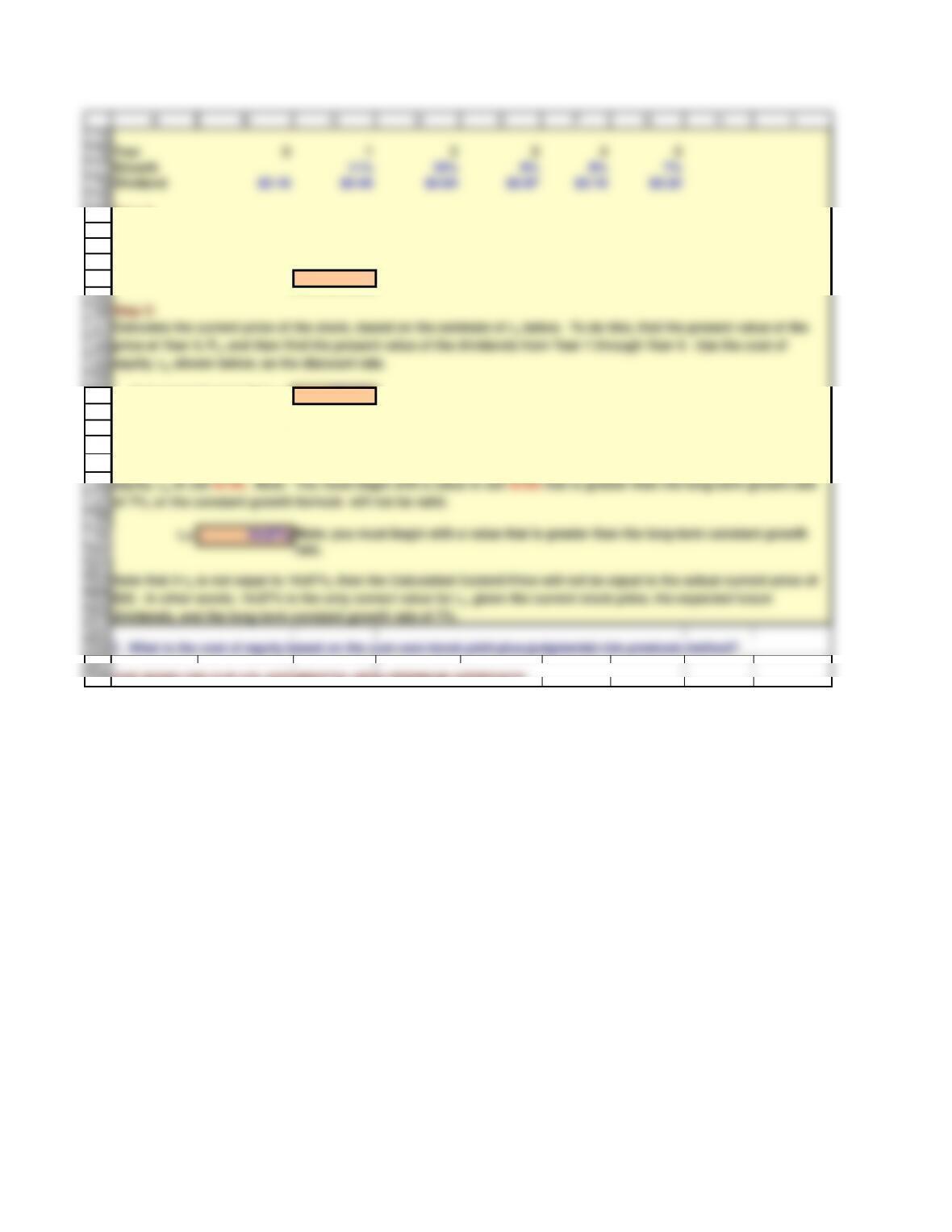

The next expected dividend is easy to estimate, and the stock price can be determined readily. However, it is not easy

to determine the marginal investor’s expected future growth rate. Three approaches are commonly used: (1)

historical growth rates, (2) retention growth model, and (3) analysts’ forecasts.

Suppose a firm’s stock trades at $50 and its most recent dividend was $3.12. If the expected constant growth rate is

5.8%, what is the firm’s cost of equity?

135

136

137

138

139

145

146

147

148

149

150

Find g:

growth rate, and what growth rate would you get? Is this consistent with the 5% growth rate given earlier?

157

158

159

160

161

162

BONUS: APPLICATION OF THE DISCOUNTED CASH FLOW APPROACH WHEN GROWTH IS NOT CONSTANT

165

the discounted cash flow valuation procedure for non-constant growth from Chapter 7 to estimate the cost of equity.

168

169

170

171

172

estimated growth rates.

A B C D E F G H I

Risk-free rate 5.6%

Expected market risk premium

6%

Beta 1.2

rs = rRF + (RPM)(bi)

rs = 5.6% +6.0% 1.2

THE DISCOUNTED CASH FLOW APPROACH

e. (1.) What is the estimated cost of equity using the dividend growth approach?

P0 =$50.00

D0 =$3.12

g = 5.8%

D1 =$3.30

2. Retention Growth Model

g =

(1 – Payout rate)

(ROE)

g = 38% 15.00%

g = 5.70%

Step 1:

Create a time line showing the expected future dividend payments. These are based on the current dividend and the

(3.) Could the dividend growth approach be applied if the growth rate was not constant? How?

Suppose the current dividend is $2.16 per share and the current actual price that we observe is $32.00 per share.

Analysts forecast growth of 11% the first year, 10% the second year, 9% the third year, 8% the fourth year, and 7%

thereafter. Estimate the cost of equity.

As we noted earlier, analysts often provide non-constant estimates of future growth. We can use a modification of

e. (2.) Suppose the firm has historically earned 15% on equity (ROE) and retained 35% of earnings, and investors

expect this situation to continue in the future. How could you use this information to estimate the future dividend

The simplest dividend growth approach assumes that growth is expected to remain constant, and in this case: rs =

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

A B C D E F G H I

THE BOND-YIELD-PLUS-JUDGMENTAL-RISK-PREMIUM APPROACH

Year 0 1 2 3 4 5

Growth 11% 10% 9% 8% 7%

Dividend $2.16 $2.40 $2.64 $2.87 $3.10 $3.32

Step 2:

Price at Year 4 = $42.20

Step 3:

Calculated Current Price = $32.00

Step 4:

rs=14.87%

Note: you must begin with a value that is greater than the long-term constant growth

rate.

Using the constant growth formula from Chapter 7 to estimate the price at Year 4: P4 = D5 / (rs – g). Notice that D5 and

g are given in the time line above, but the estimate for rs is shown below.

Calculate the current price of the stock, based on the estimate of rs below. To do this, find the present value of the

price at Year 4, P4, and then find the present value of the dividends from Year 1 through Year 4. Use the cost of

equity, rs, shown below, as the discount rate.

Use Goal Seek to determine the cost of equity, rs, shown below. Click Tools (What-If Analysis), Goal Seek and set the

value of the Calculated Current Price, cell C191, equal to the actual current stock price of $32 by changing the cost of

equity, rs, in cell B199. Note: You must begin with a value in cell B199 that is greater than the long-term growth rate

of 7%, or the constant growth formula will not be valid.

Note that if rs is not equal to 14.87%, then the Calculated Current Price will not be equal to the actual current price of

$32. In other words, 14.87% is the only correct value for rs, given the current stock price, the expected future

dividends, and the long-term constant growth rate of 7%.

f. What is the cost of equity based on the over-own-bond-yield-plus-judgmental-risk-premium method?

209

210

211

212

213

214

after-tax cost of debt, cost of preferred stock, and cost of common equity.

It is common to use several methods to estimate the cost of equity, and then find the average of these methods.

The weighted average cost of capital (WACC) is calculated using the firm’s target capital structure together with its

A B C D E F G H I

This approach consists of adding a judgmental risk premium to the yield on the firm’s own long-term debt. It is

logical that a firm with risky, low-rated debt would also have risky, high-cost equity. Historically, we have observed

that the risk premium for equity is in the range of 3 to 5 percentage points. This method provides a ballpark estimate,

and it is generally used as a check on the CAPM and dividend growth estimates. This method is used primarily in

utility rate case hearings.

269

270

271

272

273

274

275

276

277

278

279

284

285

286

287

288

289

D0 =$3.12

the issuance of new securities. A company cannot use the entire proceeds of a new security issuance, because it

must use some of the proceeds to pay the flotation costs.

295

296

297

298

299

306

n. Explain in words why new common stock that is raised externally has a higher percentage cost than equity that is

raised internally as retained earnings. Answer: See Chapter 9 PowerPoint file.

307

308

309

310

rs = D1÷

314

316

317

318

319

320

321

322

PROBLEM: Flotation Costs and the Cost of Debt

A B C D E F G H I

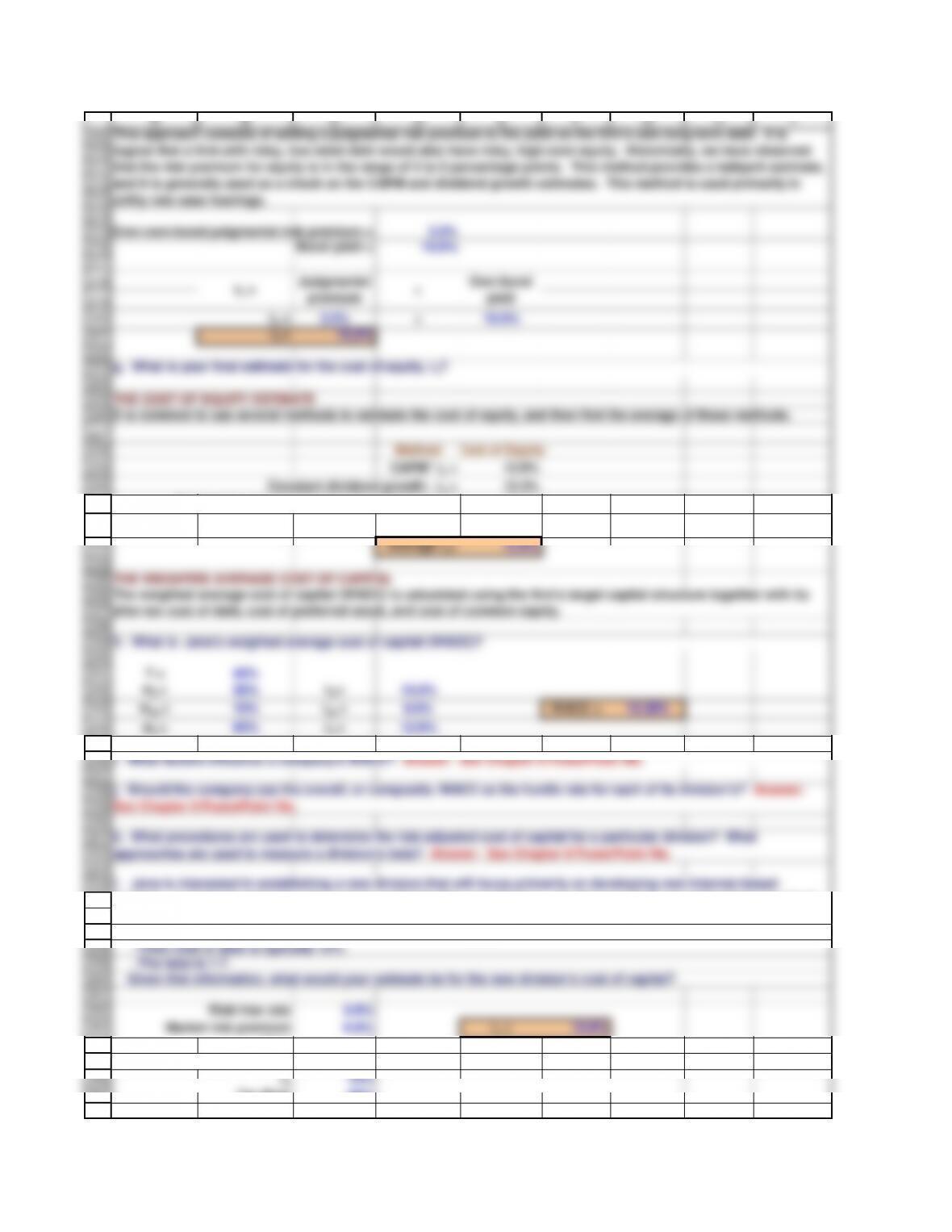

WACC =

(wd × rd) ×(1 – T) + (ws × rs)

WACC = 1.2% x60% + 14.2%

WACC = 14.9%

14.94%

10.38%

ADJUSTING THE COST OF CAPITAL FOR FLOTATION COSTS

g = 5.8%

D1 =$3.30

rs = D1÷P0+ g

rs = $3.30 ÷$50.00 +5.8%

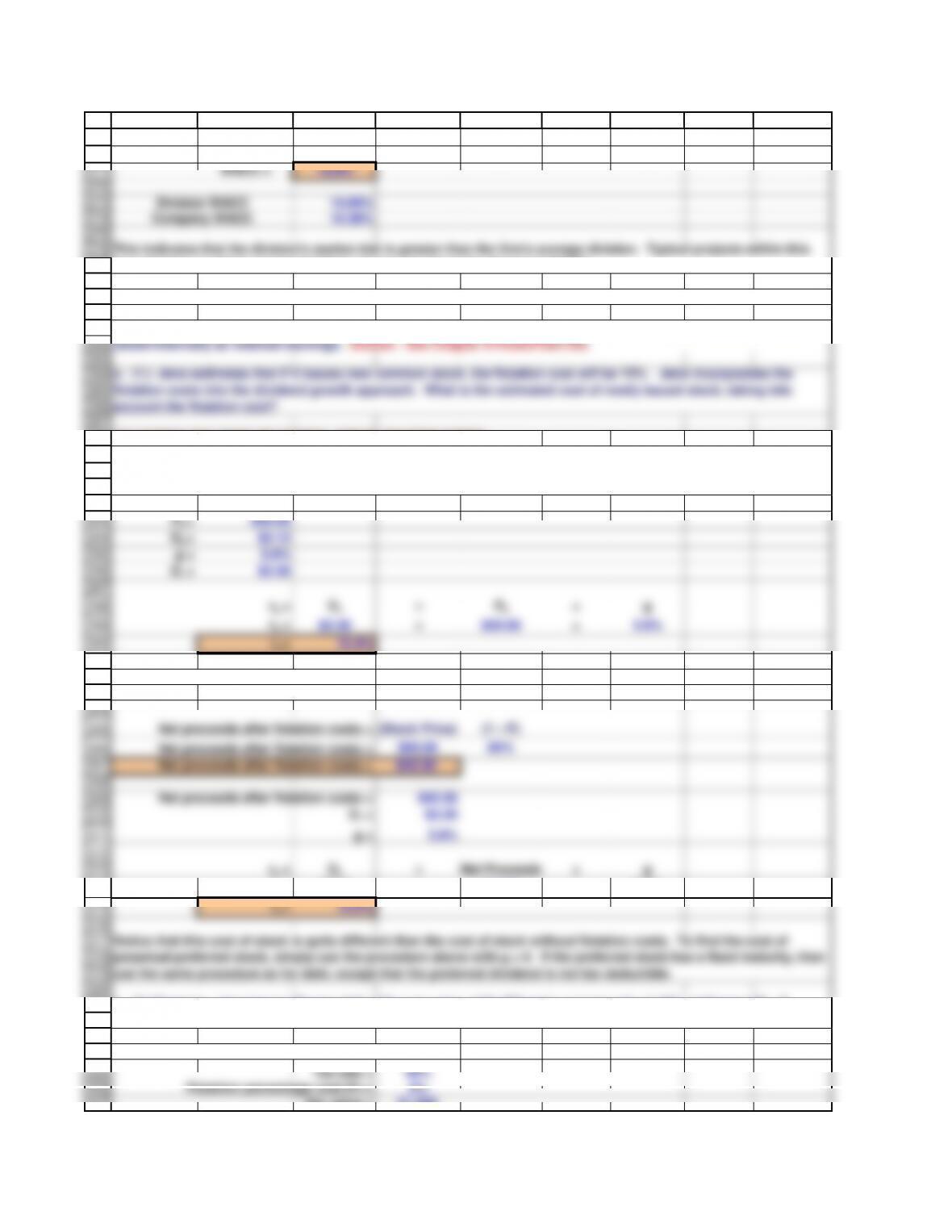

Net proceeds after flotation costs =

$50.00 85%

Net proceeds after flotation costs = $42.50

Net proceeds after flotation costs = $42.50

D1 =$3.30

rs = $3.30 ÷$42.50 +5.8%

Division WACC

m. What are three types of project risk? How is each type of risk used? Answer: See Chapter 9 PowerPoint file.

This indicates that the division’s market risk is greater than the firm’s average division. Typical projects within this

new division would be accepted if their returns are above the divisional WACC.

Company WACC

Notice that this cost of stock is quite different than the cost of stock without flotation costs. To find the cost of

perpetual preferred stock, simply use the procedure above with g = 0. If the preferred stock has a fixed maturity, then

use the same procedure as for debt, except that the preferred dividend is not tax deductible.

o. (2.) Suppose Jana issues 30-year debt with a par value of $1,000 and a coupon rate of 10%, paid annually. If

flotation costs are 2%, what is the after-tax cost of debt for the new bond issue?

flotation costs into the dividend growth approach. What is the estimated cost of newly issued stock, taking into

account the flotation cost?

Flotation costs are the fees charged by investment bankers plus the accounting and legal expenses associated with

328

329

330

331

332

333

334

335

336

337

338

339

340

341

342

343

344

345

346

347

348

349

350

351

352

353

354

355

A B C D E F G H I

Maturity payment = $1,000

Pre-tax coupon payment = $100

After-tax coupon payment =

(Coupon

pmt.)

(1 – Tax

rate)

After-tax coupon payment = $100 60%

After-tax coupon payment = $60

Net proceeds after flotation costs = (Par value) (1 – F)

Net proceeds after flotation costs = $1,000 98%

Net proceeds after flotation costs = $980

Number of coupon payments = N = 30

After-tax coupon payment = PMT = 60

Net proceeds after flotation costs = PV = 980

Payment of face value at maturity = FV = 1000

After tax cost of debt = Rate = 6.15% Note: use the Rate function.

Now find the rate that the company pays, based on its net proceeds after flotation costs and its after-tax payments.

p. What four common mistakes in estimating the WACC should Jana avoid?

Answer: See Chapter 9 PowerPoint file.

First, calculate the after-tax coupon payments and the net proceeds after the flotation costs.

Notice that this after-tax cost of debt is only slightly higher than the after-tax cost of debt for which flotation costs are

ignored. Therefore, analysts often ignore the flotation costs of debt.