Mini Case: 8 – 8

c. Consider Triple Play’s call option with a $25 strike price. The following table

contains historical values for this option at different stock prices:

Stock Price Call Option Price

$25 $ 3.00

30 7.50

35 12.00

40 16.50

45 21.00

50 25.50

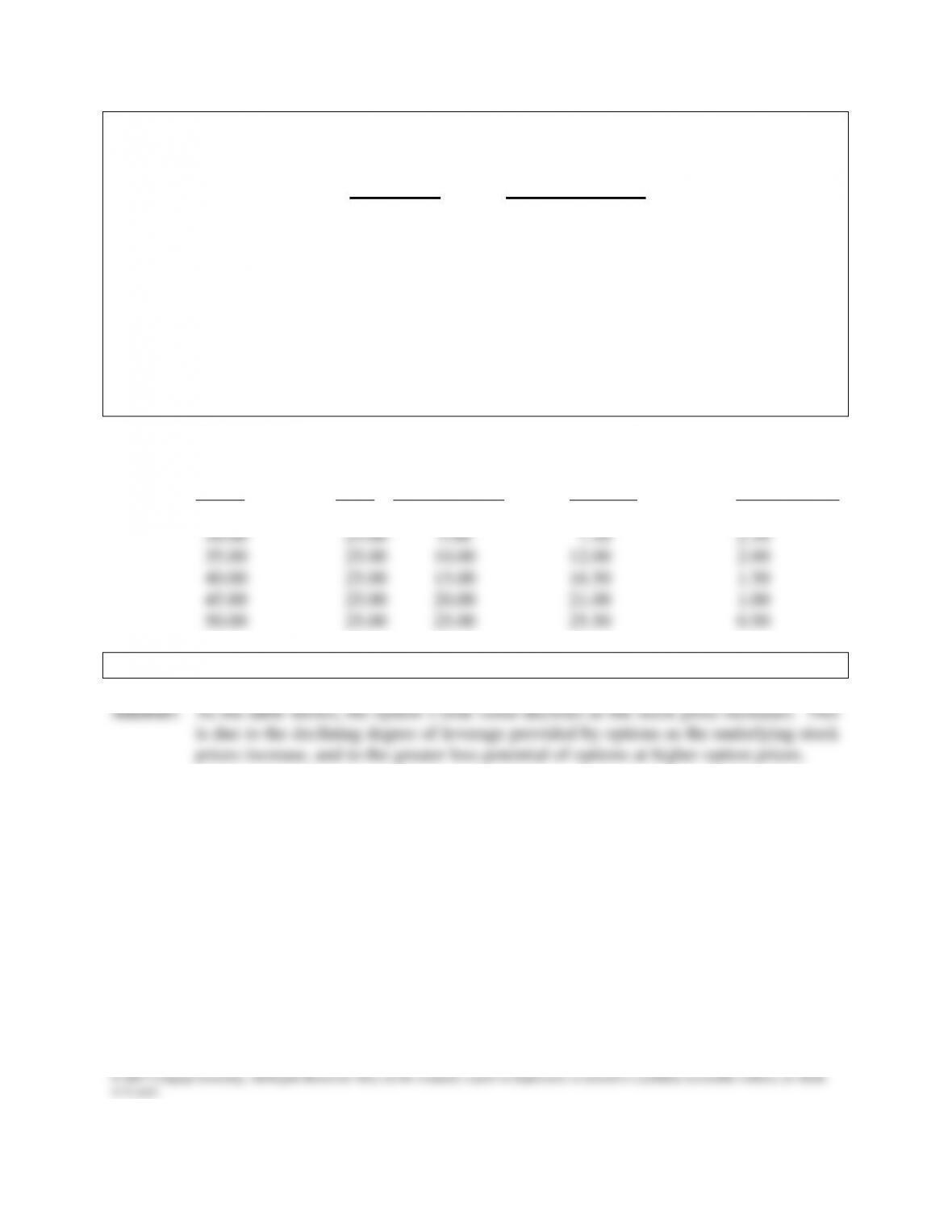

1. Create a table which shows (a) stock price, (b) strike price, (c) exercise value, (d)

option price, and (e) the time value, which is the option’s price less its exercise

value.

Answer: Price Of Strike Exercise Value Market Price Time Value

Stock Price Of Option Of Option (D) – (C) =

(A) (B) (A) – (B) = (C) (D) (E)

$25.00 $25.00 $ 0.00 $ 3.00 $3.00

c. 2. What happens to the option’s time value as the stock price rises? Why?

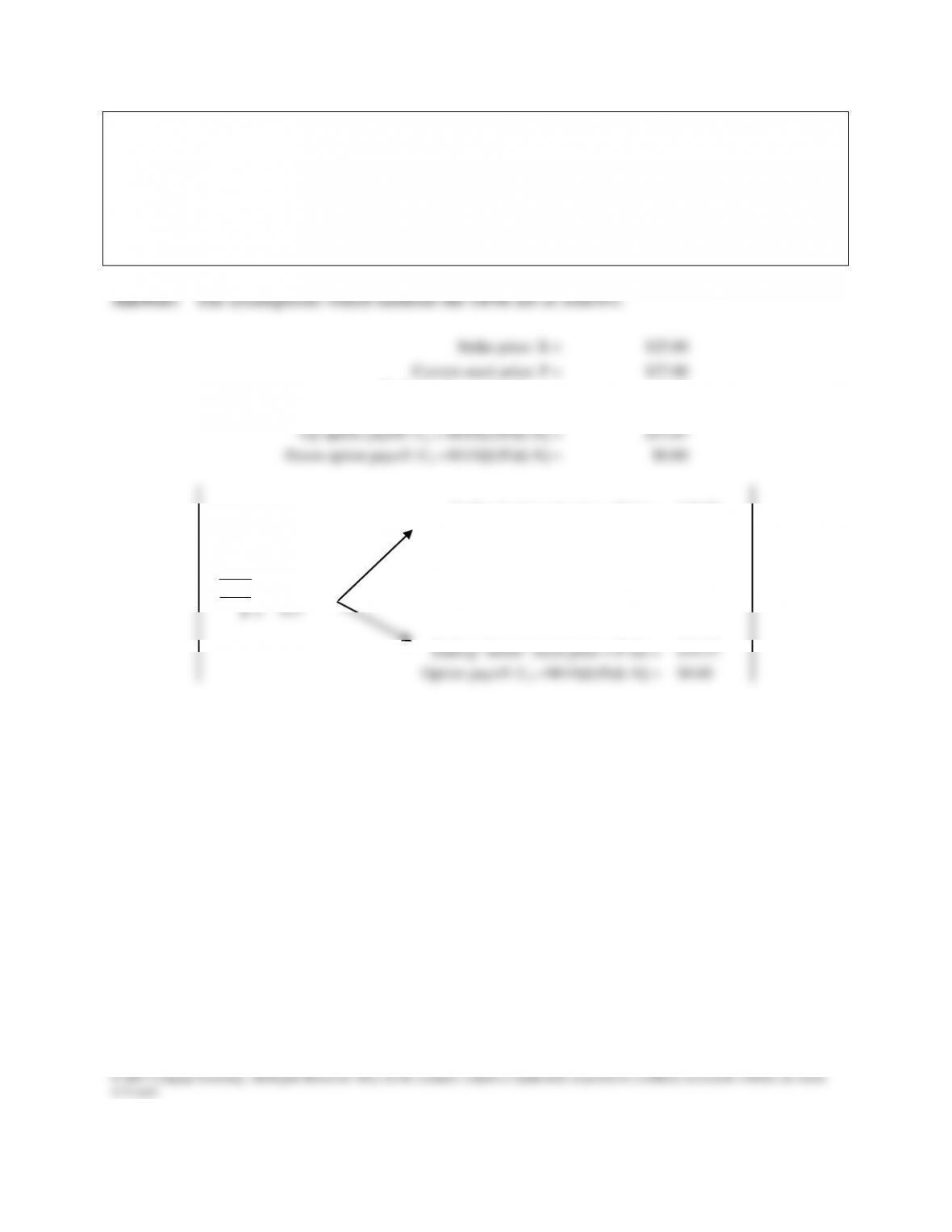

d. Consider a stock with a current price of P = $27. Suppose that over the next 6

months the stock price will either go up by a factor of 1.41 or down by a factor of

0.71. Consider a call option on the stock with a strike price of $25 which expires

in 6 months. The risk-free rate is 6%.

1. Using the binomial model, what are the ending values of the stock price? What

are the payoffs of the call option?

d. 2. Suppose you write 1 call option and buy Ns shares of stock. How many shares

must you buy to create a portfolio with a riskless payoff (which is called a hedge

portfolio)? What is the payoff of the portfolio?

Answer:

Ns =

Cu – Cd

=

0.69153

P(u – d)

$38.07

$26.33

$13.07

$19.17

$13.26

=

$12.865

1.03045

$5.81

Mini Case: 8 – 11

d. 4. What is a replicating portfolio? What is arbitrage?

e. In 1973, Fischer Black and Myron Scholes developed the Black-Scholes Option

Pricing Model (OPM).

1. What assumptions underlie the OPM?

the option.

e. 2. Write out the three equations that constitute the model.

Answer: The OPM consists of the following three equations:

V = P[N(d1) –

trRF

Xe

[N(d2)].

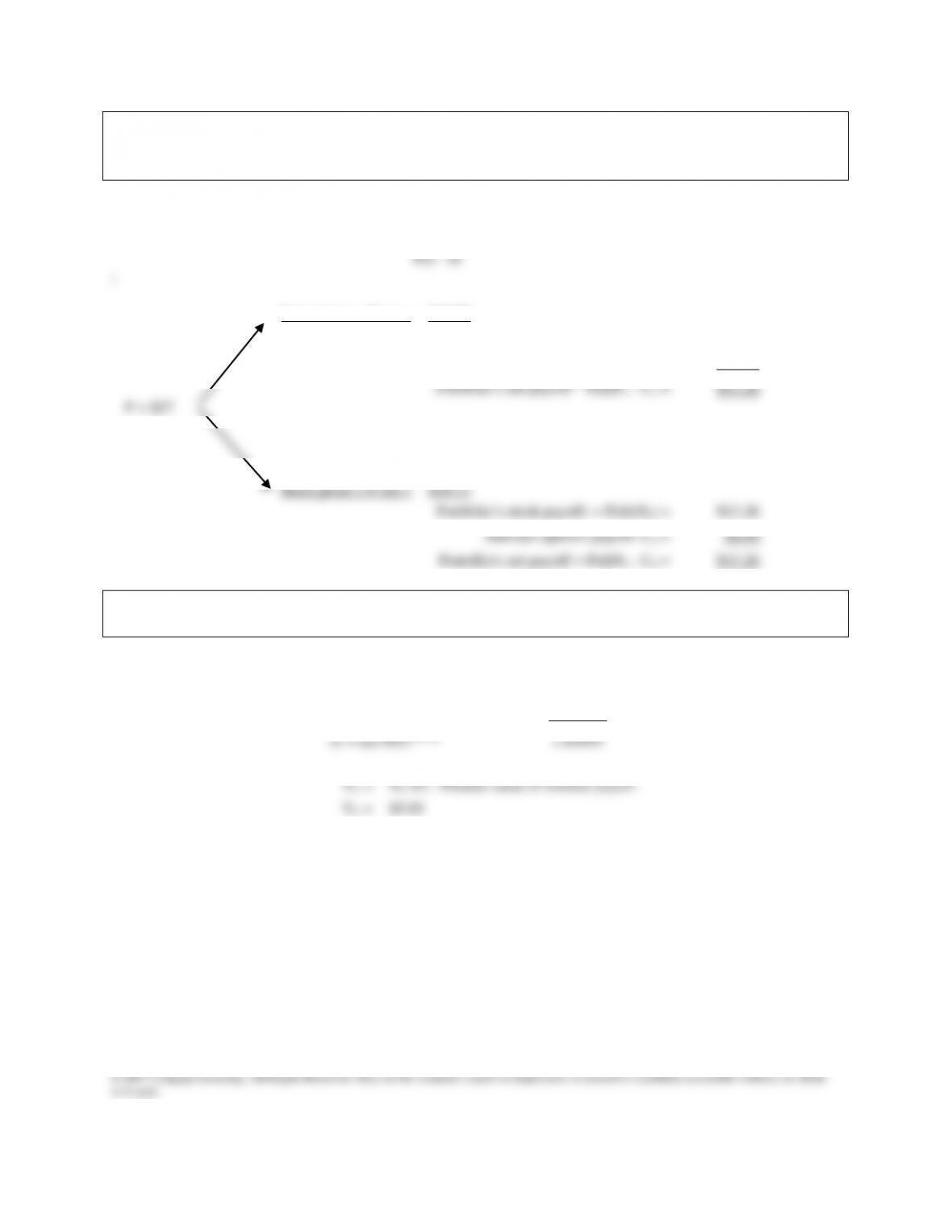

e. 3. What is the value of the following call option according to the OPM?

Stock Price = $27.00.

Strike Price = $25.00

Time To Expiration = 6 Months = 0.5 years.

Risk-Free Rate = 6.0%.

Stock Return Standard Deviation = 0.49.

Answer: The input variables are:

Mini Case: 8 – 14

f. What impact does each of the following call option parameters have on the value

of a call option?

1. Current Stock Price

2. Strike Price

3. Option’s Term To Maturity

4. Risk-Free Rate

5. Variability Of The Stock Price

Answer: 1. The value of a call option increases (decreases) as the current stock price

increases (decreases).

can climb.

g. What is put-call parity?

Answer: Put-call parity specifies the relationship between puts, calls, and the underlying stock

price that must hold to prevent arbitrage: