10/28/2015

SITUATION

LOOKING AT EXERCISE AND MARKET VALUE OF AN OPTION

Strike) price = $25

Price of Strike Exercise

the stock Price Value

$0 $20.00 $0.00

$5 $20.00 $0.00

$10 $20.00 $0.00

$15 $20.00 $0.00

$20 $20.00 $0.00

$25 $20.00 $5.00

$30 $20.00 $10.00

$35 $20.00 $15.00

$25

Chapter 8. Mini Case for Financial Options and Applications in Corporate Finance

$20.00

$25.00

$3.00

$1.00

$0.50

$15.00

To begin, you gathered some outside materials on the subject and used these materials to draft a list of

pertinent questions that need to be answered. In fact, one possible approach to the paper is to use a

Assume that you have just been hired as a financial analyst by Triple Play Inc., a mid-sized California

company that specializes in creating high-fashion clothing. Since no one at Triple Play is familiar with the

basics of financial options, you have been asked to prepare a brief report that the firm’s executives could

use to gain at least a cursory understanding of the topics.

$0.00

$50.00

$3.00

$7.50

$12.00

$16.50

$21.00

$25.50

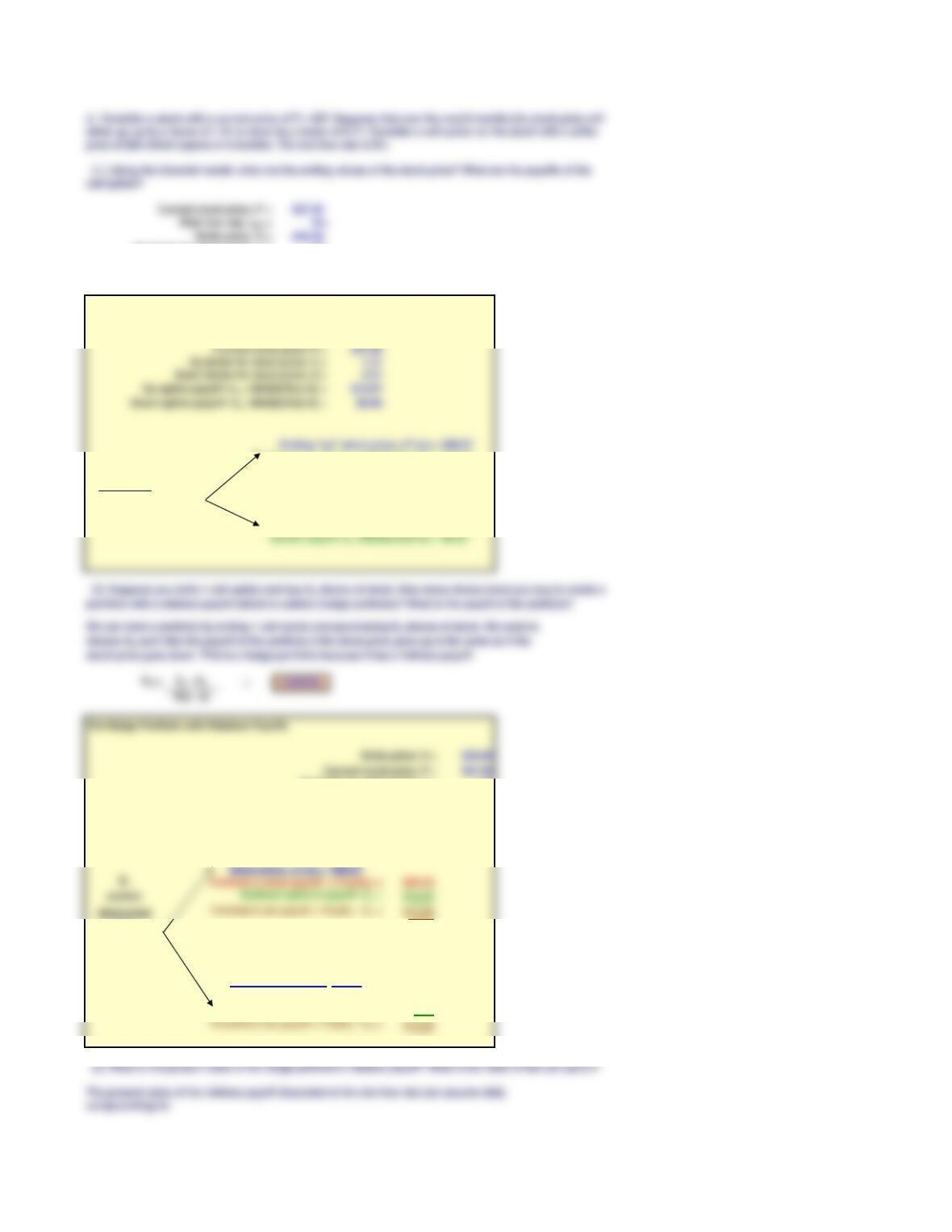

(1.) What are the corresponding exercise values and option time values?

Exercise Values

Option Time Values

Strike Price=

$35.00

$40.00

a. What is a financial option? What is the single most important characteristic of an option? Answer: See

Chapter 08 Mini Case Show

b. Options have a unique set of terminology. Define the following terms: (1) call option; (2) put option; (3)

exercise price; (4) striking, or strike price; (5) option price; (6) expiration date; (7) exercise value; (8) writing

an option; (9) covered option; (10) naked option; (11) in-the-money call; (12) out-of-the-money call; and (13)

LEAP. Answer: See Chapter 08 Mini Case Show

c. Consider Triple Play’s call option with a $25 strike price. The following table contains historical values

for this option at different stock prices:

Suppose a stock has the strike price shown below. The Exercise Value is the profit if you choose to exercise

the stock. If the current price of the stock is greater than the strike price, then the Exercise Value is the

current stock price minus the strike price; otherwise, it is zero (you would never exercise the option if the

stock price is less than the strike price.)

Stock Price

Option Price

$45.00

$25.00

$30.00

$5.00

$10.00

$2.50

$2.00

$1.50

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

Exercise Value vs. Stock Price

Current stock price, P = $27.00

Risk-free rate, rRF = 6%

Strike price, X = $25.00

Up factor for stock price, u = 1.41

Down factor for stock price, d = 0.71

Years to expiration, t = 0.50

Binomial Payoffs

Up factor for stock price: u = 1.41

Down factor for stock price: d = 0.71

Up option payoff: Cu = MAX[0,P(u)-X] = $13.07

Down option payoff: Cd =MAX[0,P(d)-X] = $0.00

Ending “up” stock price = P (u) = $38.07

Option payoff: Cu = MAX[0,P(u)-X] = $13.07

Ns = Cu – Cd=0.69153

P(u – d)

The Hedge Portfolio with Riskless Payoffs

Strike price: X = $25.00

Current stock price: P = $27.00

Up factor for stock price: u = 1.41

Down factor for stock price: d = 0.71

Up option payoff: Cu = MAX[0,P(u)-X] = $13.07

Down option payoff: Cd =MAX[0,P(d)-X] = $0.00

Number of shares of stock in portfolio: Ns = (Cu – Cd) / P(u-d) = 0.69153

Stock price = P (u) = $38.07

P,

Portfolio’s stock payoff: = P(u)(Ns) = $26.33

current

Subtract option’s payoff: Cu = $13.07

stock price

Portfolio’s net payoff = P(u)Ns – Cu = $13.26

$27

Stock price = P (d) = $19.17

Portoflio’s stock payoff: = P(d)(Ns) = $13.26

Subtract option’s payoff: Cd = $0.00

We can form a portfolio by writing 1 call option and purchasing Ns shares of stock. We want to

choose Ns such that the payoff of the portfolio if the stock price goes up is the same as if the

stock price goes down. This is a hedge portfolio because it has a riskless payoff.

d. Consider a stock with a current price of P = $27. Suppose that over the next 6 months the stock price will

either go up by a factor of 1.41 or down by a factor of 0.71. Consider a call option on the stock with a strike

price of $25 which expires in 6 months. The risk-free rate is 6%.

(1.) Using the binomial model, what are the ending values of the stock price? What are the payoffs of the

call option?

(2.) Suppose you write 1 call option and buy Ns shares of stock. How many shares must you buy to create a

portfolio with a riskless payoff (which is called a hedge portfolio)? What is the payoff of the portfolio?

(3.) What is the present value of the hedge portfolio’s riskless payoff? What is the value of the call option?

The present value of the riskless payoff disounted at the risk-free rate (we assume daily

compounding) is:

N = 182.5

I/YR = 0.0164%

PMT = 0

FV = ($13.26)

PV = $12.865 Using the PV function.

Alternatively, use the present value equation:

Pv of payoff = = $13.2567 =$12.865

1.03045

VC = Ns (P) – Present value of riskless payoff

VC = $5.81

Ns = 0.69153

Amount borrowed = PV of riskless payoff = $12.86

Repayment of riskless payoff = $13.26

Payoff if stock is up:

Stock price = $38.07

Value of stock in portfolio = $26.33

Less repayment of borrowing = $13.26

Net payoff of portfolio = $13.07

Payoff if stock is down:

Stock price = $19.17

Value of stock in portfolio = $13.26

Less repayment of borrowing = $13.26

Net payoff of portfolio = $0.00

Notice that these are the same payoffs of the option.

The current value of the hedge portolio is the the stock value (Ns x P) less the call value (VC). But

the hedge portfolio has a riskless payoff, so the hedge portfolio’s value must also be equal to the

present value of the riskless payoff disounted at the risk-free rate (we assume daily

compounding). With a little algebra, we get:

If you borrow an amount equal to the present value of the riskless payoff and buy Ns shares of

stock, the payoffs of this portfolio replicate the payoffs of the call option.

(4.) What is a replicating portfolio? What is arbitrage?

Payoff

(1 + rRF/365)365*(t)

BLACK-SCHOLES OPTION PRICING MODEL

The derivation of the Black-Scholes model rests on the concept of a riskless hedge. By buying shares of a

position, where gains on the stock are exactly offset by losses on the option. Ultimately, the Black-Scholes

model utilizes these three formulas:

price for a security sold short.

6. The call option can be exercised only on its expiration date.

7. Trading in all securities takes place continuously, and the stock price moves randomly.

e. (2.) Write out the three equations that constitute the model.

interest rate.

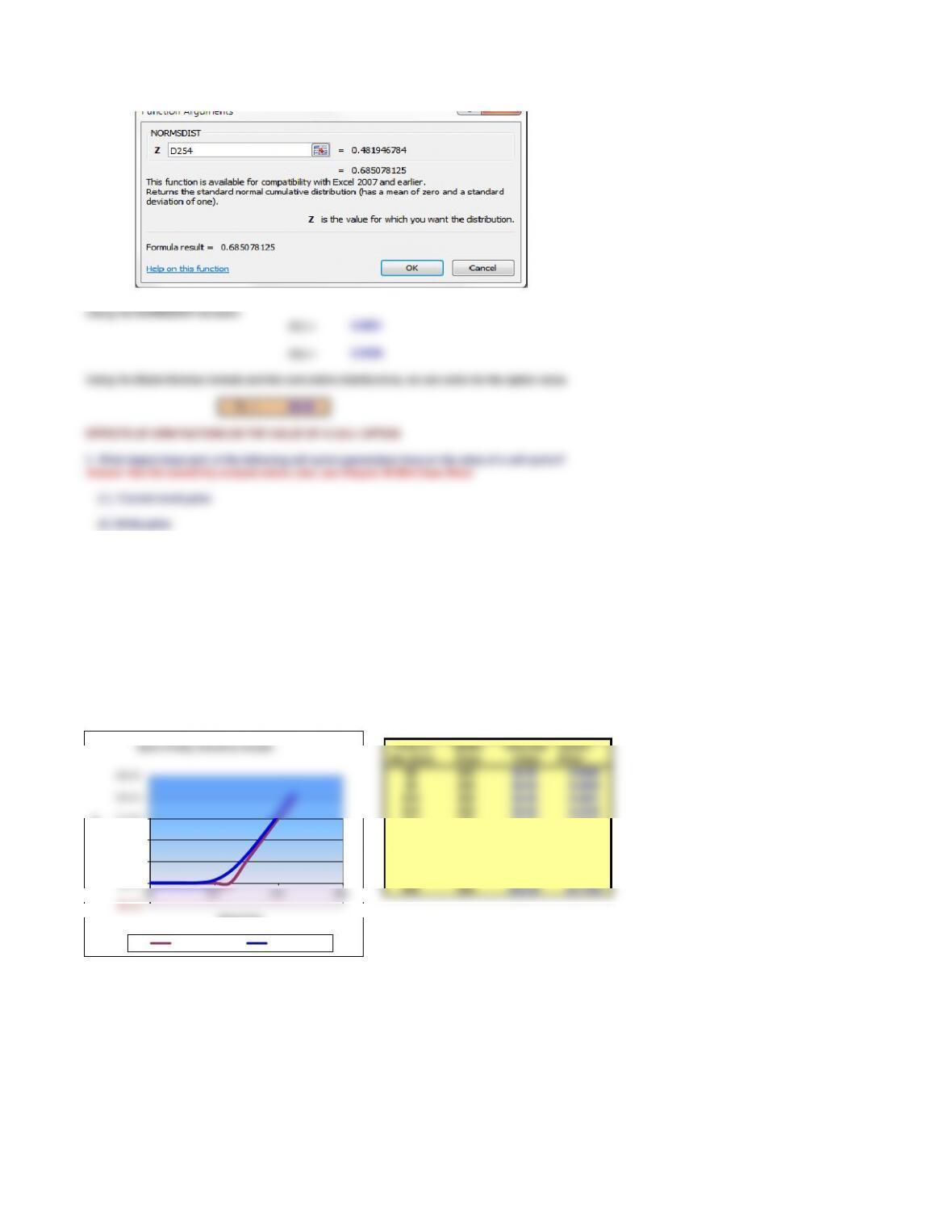

d1 = { ln (P/X) + [rRF + s2 /2) ] t } / (s t1/2)

d2 = d1 – s (t 1 / 2)

Key Inputs: Key output:

P$27 VC = $5.059

X$25

rRF 6%

t (in years) 0.5

s0.49

Now, we will use the formula from above to solve for d1.

(d1)=0.4819

Having solved for d1, we will now use this value to find d2.

(d2)=0.1355

e. In 1973, Fischer Black and Myron Scholes developed the Black-Scholes Option Pricing Model (OPM).

In deriving this option pricing model, Black and Scholes made the following assumptions:

e. (1.) What assumptions underlie the OPM?

In these equations, V is the value of the option. P is the current price of the stock. N(d1) is the area beneath

the standard normal distribution corresponding to (d1). X is the strike price. rRF is the risk-free rate. t is the

time to maturity. N(d2) is the area beneath the standard normal distribution corresponding to (d2). s, or

sigma, is the volatility of the stock price, as measured by the standard deviation.

1. The stock underlying the call option provides no dividends or other distributions during the life of the

option.

2. There are no transaction costs for buying or selling either the stock or the option.

3. The short-term, risk-free interest rate is known and is constant during the life of the option.

4. Any purchaser of a security may borrow any fraction of the purchase price at the short-term, risk-free

At this point, we have all of the necessary inputs for solving for the value of the call option. We will use the

formula for V from above to find the value. The only complication arises when entering N(d1) and N(d2).

Remember, these are the areas under the standard normal distribution. Luckily, Excel is equipped with a

function that can determine cumulative probabilities of the normal distribution. This function is located in

the list of statistical functions, as “NORMSDIST”. For both N(d1) and N(d2), we will follow the same

procedure of using this function in the value formula.

e. (3.) What is the value of the following call option according to the OPM?

Looking at these equations we see that you must first solve d1 and d2 before you can proceed to value the

option.

This model is widely used by options traders and is generally considered to be the standard for option

pricing. Many hand-held calculators and computer programs have this formula permanently stored in. We

now use Excel to write a “program”, if you will, for the Black-Scholes pricing model in Excel.

First, we will lay out the input data given to us in the setup of the problem.

Using the NORMSDIST function:

(d1) = 0.6851

(d2) = 0.5539

VC = $5.06

(1.) Current stock price

(2.) Strike price

(3.) Option’s term to maturity

(4.) Risk-free rate

(5.) Variability of the stock price

Change the inputs below to see the impact on the option’s price (X=25 for all cases).

Using the Black-Scholes formula and the cumulative distributions, we can solve for the option value.

EFFECTS OF OPM FACTORS ON THE VALUE OF A CALL OPTION

f. What impact does each of the following call option parameters have on the value of a call option?

Answer: See the sensitivity analysis below; also, see Chapter 08 Mini Case Show