Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Mini Case: 7 - 21

or in part.

d. 1. Suppose the free cash flow at Time 1 is expected to grow at a constant rate of gL

forever. If gL < WACC, what is a formula for the present value of expected free

cash flows when discounted at the WACC?

Answer:

d. 2. If the most recent free cash flow is expected to grow at a constant rate of gL

forever (and gL < WACC), what is a formula for the present value of expected

free cash flows when discounted at the WACC?

Answer:

e. 1. Use B&M’s data and the free cash flow valuation model to answer the following

questions. What is its estimated value of operations?

Answer:

e. 2. What is its estimated total corporate value? (This is the entity value.)

e. 3. What is its estimated intrinsic value of equity?

420

05.011.0

)05.01(24

V

gWACC

)g1(FCF

V

op

L

L0

op

L

1

op gWACC

FCF

V

L

L0

op gWACC

)g1(FCF

V

f. 1. You have just learned that B&M has undertaken a major expansion that will

change its expected free cash flows to −$10 million in 1 year, $20 million in 2

years, and $35 million in 3 years. After 3 years, free cash flow will grow at a rate

of 5%. No new debt or preferred stock were added, the investment was financed

by equity from the owners. Assume the WACC is unchanged at 11% and that

there are still 10 million shares of stock outstanding. What is its horizon value

(i.e., its value of operations at year three)? What is its current value of

operations (i.e., at time zero)?

Answer:

Year

0

1

2

3

4

5

… t

FCF

−$

$20

$35

FCF3(1+0.05)

FCF4(1+ 0.05)

FCFt(1+ 0.05)

Mini Case: 7 - 23

or in part.

Year

0

1

2

3

4

5

… t

FCF

FCF1

FCF2

FCF3

PV of FCF in explicit forecast

←

←

←

FCF3(1+gL)

FCF4(1+gL)

FCFt(1+gL)

HV3

←

←

←

PV of HV is the PV of FCF beyond

the explicit forecast

←

←

←

0 WACC = 11% 1 2 3 gL = 5% 4 N

| | | | | |

-10 20 35

Answer:

Value of operations

$480.67

+ Value of nonoperating assets

100.00

Total estimated value of firm

$580.67

− Debt

200.00

− Preferred stock

50.00

Estimated value of equity

$330.67

÷ Number of shares

10.00

Estimated stock price per share =

$33.07

or in part.

g. If B&M undertakes the expansion, what percent of B&M’s value of operations

at Year 0 is due to cash flows from Years 4 and beyond? Hint: use the horizon

value at t = 3 to help answer this question.

Answer: First, calculate the present value of the horizon value. Then divide the present value

Percent of value due to cash flows from Year 4 and beyond:

h. Based on your answer to the previous question, what are two reasons why

managers often emphasize short-term earnings?

i. Your employer also is considering the acquistion of Hatfield Medical Supplies.

You have gathered the following data regarding Hatfield, with all dollars

reported in millions: (1) most recent sales of $2,000; (2) most recent total net

operating capital, OpCap = $1,120; (3) most recent operating profitability ratio,

OP = NOPAT/Sales = 4.5%; and (4) most recent capital requirement ratio, CR =

OpCap/Sales = 56%. You estimate that the growth rate in sales from Year 0 to

Year 1 will be 10%, from Year 1 to Year 2 will be 8%, from Year 2 to Year 3

will be 5%, and from Year 3 to Year 4 will be 5%. You also estimate that the

long-term growth rate beyond Year 4 will be 5%. Assume the operating

profitability and capital requirement ratios will not change. Use this information

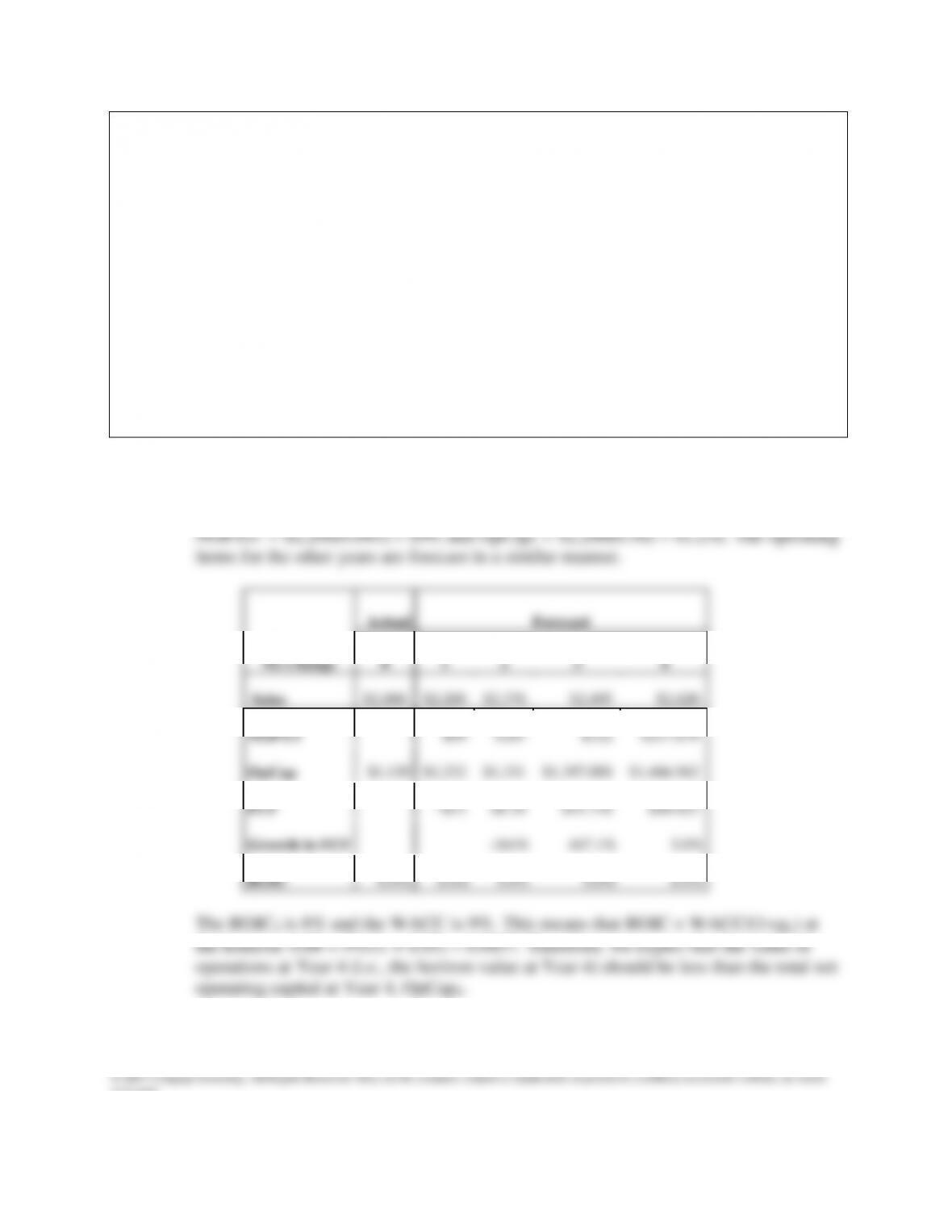

to forecast Hatfield's sales, net operating profit after taxes (NOPAT), OpCap,

free cash flow, and return on invested capital (ROIC) for Years 1 through 4.

Also estimate the annual growth in free cash flow for Years 2 through 4. The

weighted average cost of capital (WACC) is 9%. How does the ROIC in Year 4

compare with the WACC?

Answer:

The operating items are forecast as follows: Sales1 = $2,000(1+0.10) = $2,200;

or in part.

j. What is the horizon value at Year 4? What is the value of operations at Year 0?

How does the value of operations compare with the current total net operating

capital?

Answer:

PV of FCF = FCF

PV of FCF = $64.45

The value of operations is the sum of the PV of the horizon value plus the PVs of the

FCFs:

Value of Operations:

Present value of HV

$893.08

+ Present value of FCF

$64.45

Value of operations ≈

$958

Notice that the value of operations at Year 4 (i.e., the horizon value, HV4) is

$1,260.65 and that the total net operation capital at Year 4 (OpCap4 from Part i) is

the low ROIC relative to the WACC causes the value of operations to be less than the

total net operating capital.

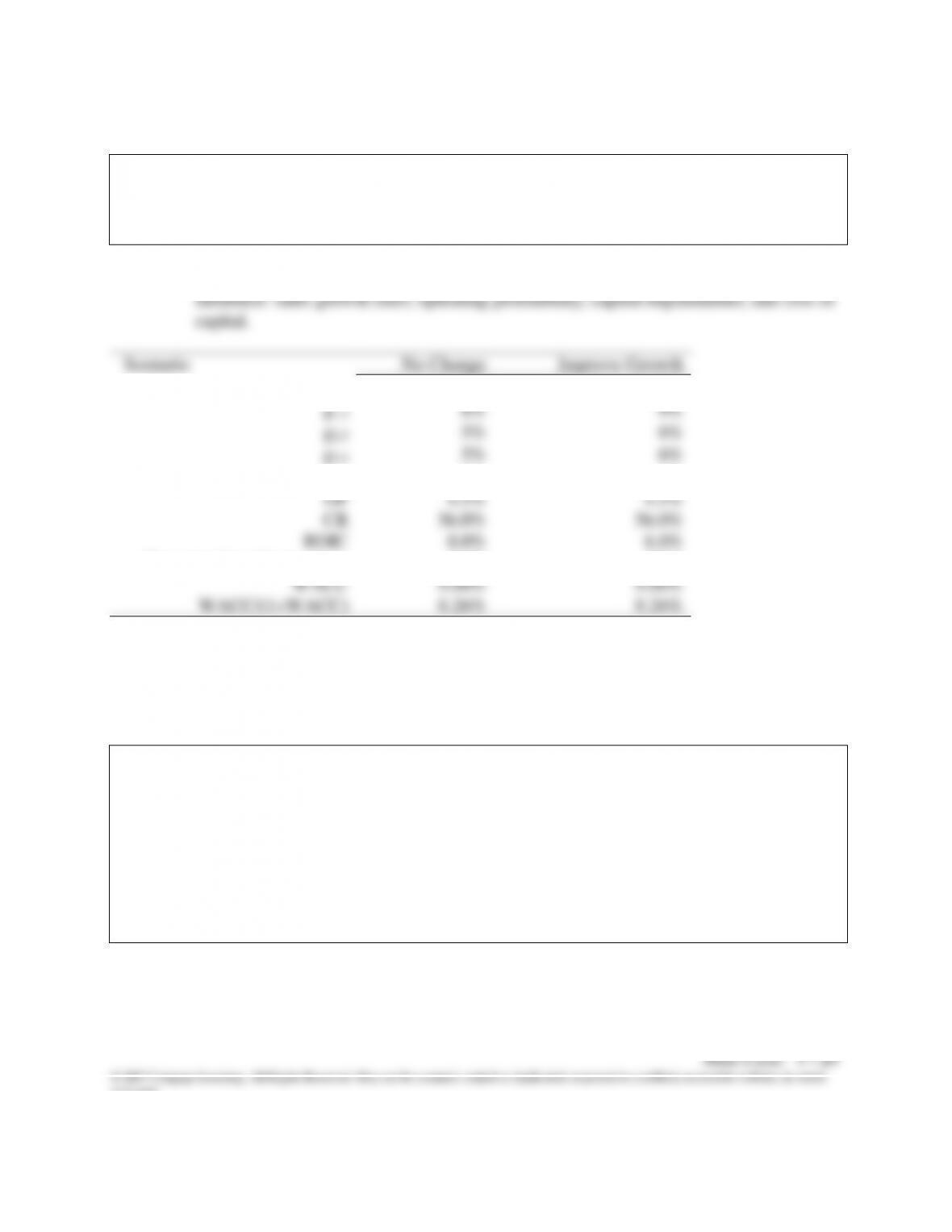

operations if expected growth increases by 1 percentage point relative to the

original growth rates (including the long-term growth rate)? What can explain

this? Hint: Use Scenario Manager.

Answer: Value drivers are the inputs to the FCF valuation model that managers are able to

Answer: .

Scenario

No Change

Improve OP

g0,1

10%

10%

g1,2

8%

8%

g2,3

5%

5%

g3,4

5%

5%

gL

5%

5%

OP

4.5%

5.5%

CR

56.0%

56.0%

ROIC

8.0%

9.8%

Current value of operations

$958

$1,523

WACC

9.00%

9.00%

WACC/(1+WACC)

8.26%

8.26%

The improvement in operating profitability increases the ROIC, which increases the value of

operations.

Scenario

No Change

Improve OP and CR

g0,1

10%

10%

g1,2

8%

8%

g2,3

5%

5%

g3,4

5%

5%

gL

5%

5%

OP

4.5%

5.5%

CR

56.0%

51.0%

ROIC

8.0%

10.8%

Current value of operations

$958

$1,756

WACC

9.00%

9.00%

WACC/(1+WACC)

8.26%

8.26%

The improvements in operating profitability and capital requirements increased the ROIC, so

growth now adds substantial value.