506

507

508

509

510

511

512

513

514

515

516

517

524

525

526

527

528

D1D0 (1 + g)

( rs – gL ) ( rs – gL )

=

534

535

536

537

538

539

Stock Price 1 year from now:

545

546

547

548

549

550

556

557

558

559

A B C D E F G H I

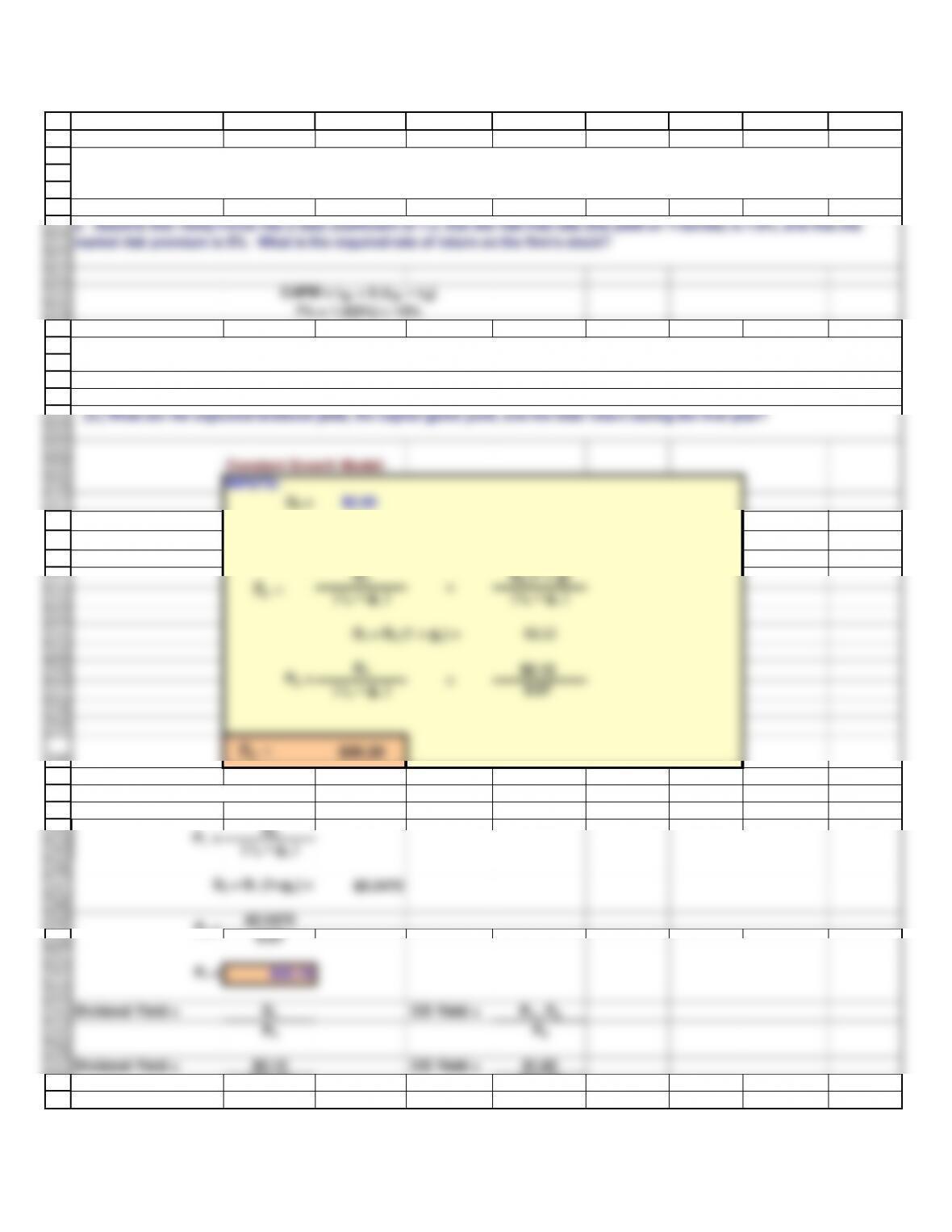

Constant Growth Model:

INPUTS:

D0 = $2.00

gL = 6%

D1 = D0 (1 + gL) = $2.12

D1$2.12

( rs – gL ) 0.07

( rs – gL )

D2 = D1 (1+gL) = $2.2472

$2.2472

0.07

Dividend Yield = $2.12 CG Yield = $1.82

$30.29 $30.29

o. Assume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 7.0%, and that the

market risk premium is 5%. What is the required rate of return on the firm’s stock?

P1 =

P1 =

CAPM = rRF + b (rRF – rM)

7% + 1.2(5%) = 13%

n. (3.) What happens if a company has a constant gL which exceeds rs? Will many stocks have expected growth greater than

the required rate of return in the short run (i.e., for the next few years)? In the long run (i.e., forever)? Answer: See Chapter 7

Mini Case Show.

P0 =

=

560

561

562

563

564

565

566

567

568

569

570

571

577

578

579

580

581

582

589

590

591

592

593

600

601

602

603

604

g0,1 = 30% Growth rate for Year 1 only.

g1,2 = 25% Growth rate for Year 2 only.

609

610

611

612

A B C D E F G H I

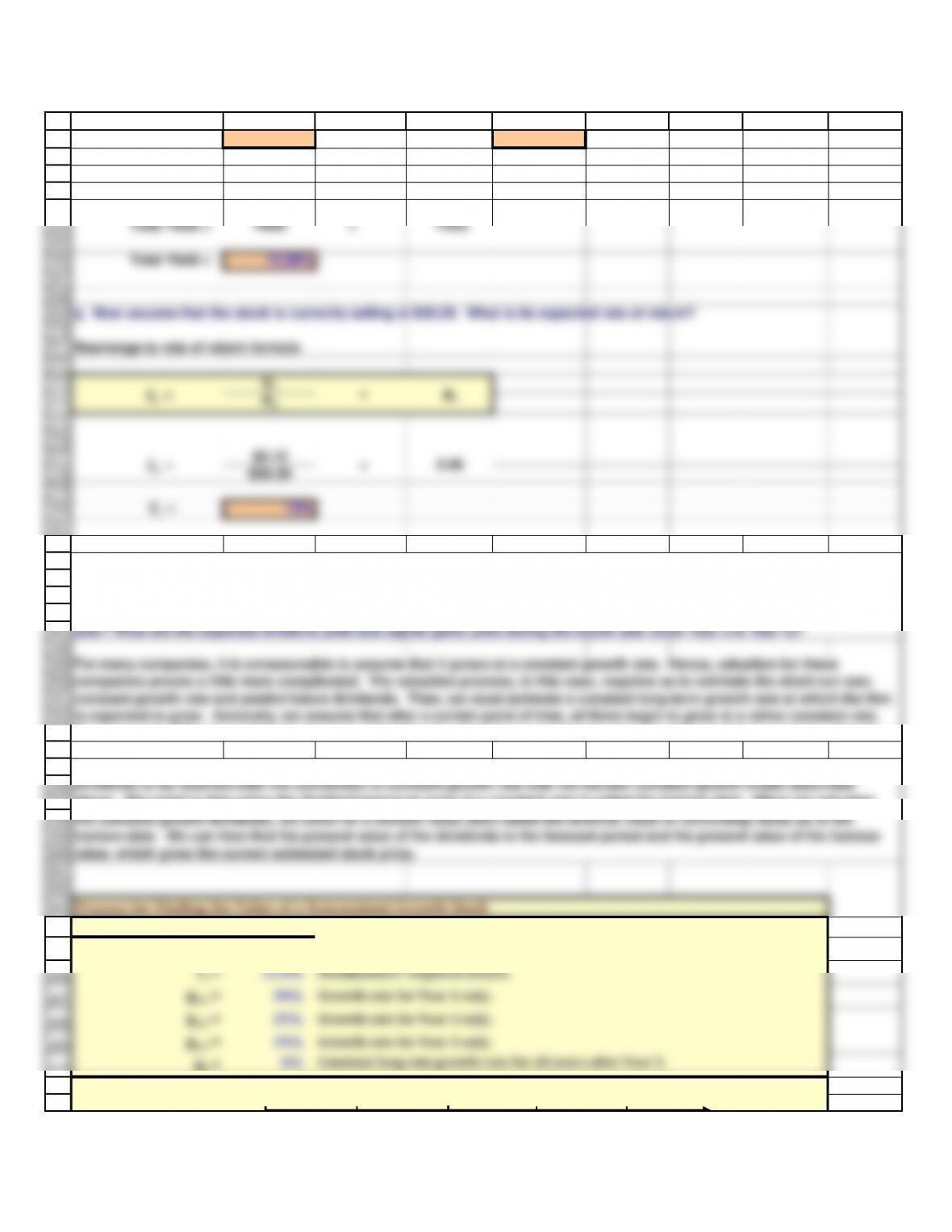

Dividend Yield = 7.00% CG Yield = 6.00%

Total Yield =

Dividend

Yield

+

CG

Yield

Total Yield = 13.00%

Rearrange to rate of return formula

$2.12

$30.29

13%

Process for Finding the Value of a Nonconstant Growth Stock

INPUTS:

g2,3 = 15% Growth rate for Year 3 only.

gL = 6%

Constant long-run growth rate for all years after Year 3.

Growth rate 30% 25% 15% 6% 6%

+

0.06

value, which gives the current estimated stock price.

q. Now assume that the stock is currently selling at $30.29. What is its expected rate of return?

For many companies, it is unreasonable to assume that it grows at a constant growth rate. Hence, valuation for these

companies proves a little more complicated. The valuation process, in this case, requires us to estimate the short-run non-

constant growth rate and predict future dividends. Then, we must estimate a constant long-term growth rate at which the firm

is expected to grow. Generally, we assume that after a certain point of time, all firms begin to grow at a rather constant rate.

Of course, the difficulty in this framework is estimating the short-term growth rate, how long the short-term growth will hold,

=

=

613

614

615

616

617

618

619

620

629

630

631

632

633

634

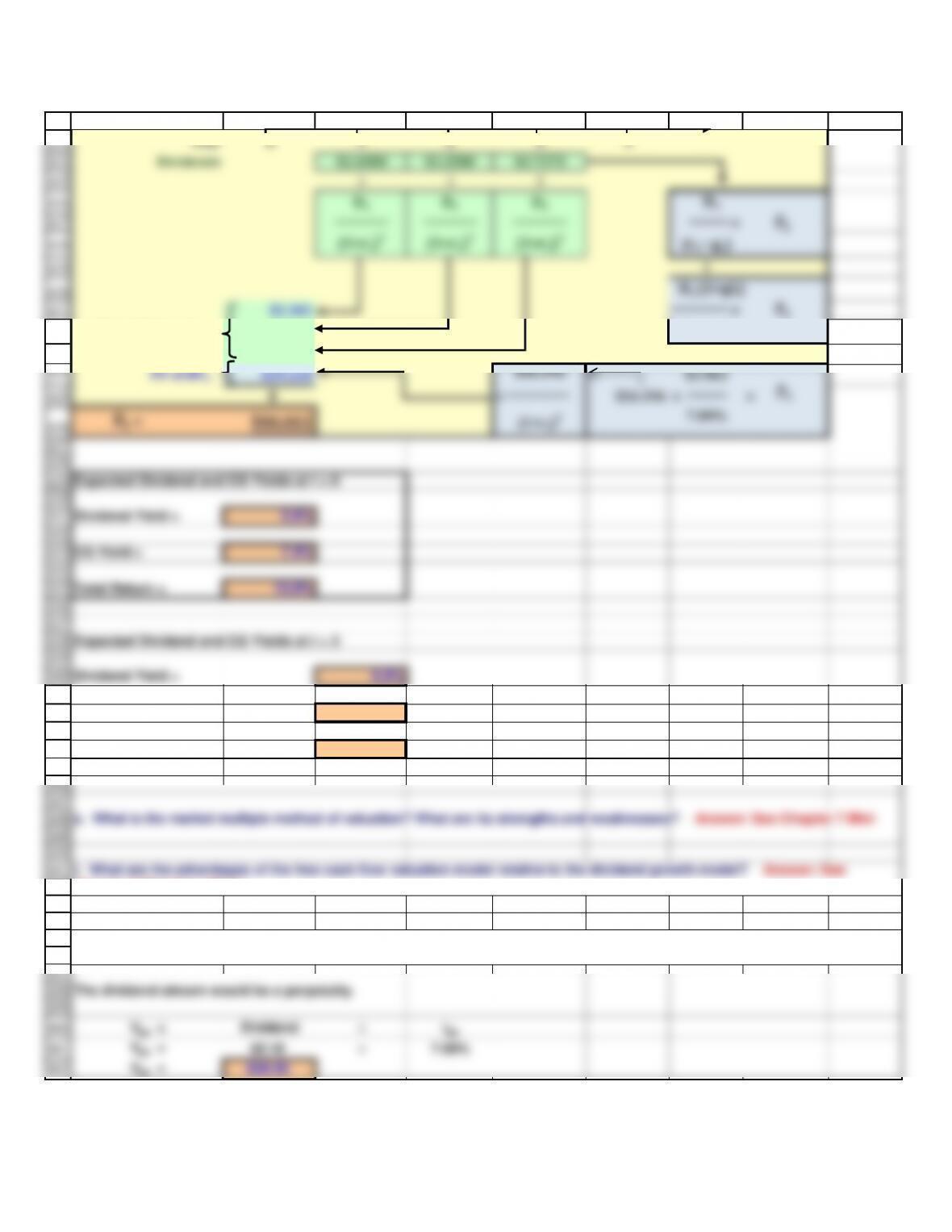

Total Return = 13.0%

Expected Dividend and CG Yields at t = 3

Dividend Yield = 0.0%

CG Yield = 13.0%

Total Return = 13.0%

The dividend stream would be a perpetuity.

A B C D E F G H I

Year 0 1 2 3 4

Dividends $2.6000 $3.2500 $3.7375

↓ ↓ ↓

D1D2D3 D4

────── ────── ──────

──── =

(1+rs)1(1+rs)2(1+rs)3(rs− gL)

↓

D3 (1+gL)

Expected Dividend and CG Yields at t = 0

Dividend Yield = 5.6%

CG Yield = 7.4%

�

1

2

3

4

5

6

7

8

9

10

11

18

19

20

21

22

29

30

31

32

33

40

41

42

43

44

51

52

53

54

55

J

58

59

60

61

62

63

64

65

66

72

73

74

75

76

77

82

83

84

85

86

87

88

94

95

96

97

98

104

105

106

107

108

109

110

J

112

113

114

115

116

117

118

119

120

126

127

128

129

137

138

139

140

141

148

149

150

151

152

153

159

160

161

162

163

164

J

165

166

167

168

169

170

171

172

173

180

181

182

183

184

185

191

192

193

194

195

196

202

203

204

205

206

212

213

214

215

216

217

218

J

219

220

221

222

223

224

225

233

234

235

236

243

244

245

246

247

248

254

255

256

257

258

259

265

266

267

J

268

269

270

271

272

273

274

276

277

278

279

280

281

284

285

286

287

288

289

290

291

292

293

294

295

299

300

301

302

303

310

311

312

313

314

321

322

J

323

324

325

326

327

328

329

330

331

332

333

334

335

341

342

343

344

345

346

352

353

354

355

356

357

363

364

365

366

367

368

374

375

376

377

378

J