1

2

3

4

5

6

7

8

9

10

11

12

19

20

21

22

23

30

31

32

33

34

41

42

43

44

45

52

53

54

55

56

A B C D E F G H I

Features of Common Stock

1. Common Stock represents ownership. 2. Ownership implies control. 3. Stockholders elect directors. 4. Directors hire

10/28/2015

Situation

Classified Stock

Classified Stock carries special provisions. For example, shares could be classified as founders’ shares which come with

voting rights but dividend restrictions.

Chapter 7 Mini Case

Your employer, a mid-sized human resources management company, is considering expansion into related fields, including

the acquisition of Temp Force Company, an employment agency that supplies word processor operators and computer

programmers to businesses with temporary heavy workloads. Your employer is also considering the purchase of Biggerstaff &

McDonald (B&M), a privately held company owned by two friends, each with 5 million shares of stock. B&M currently has free

cash flow of $24 million, which is expected to grow at a constant rate of 5%. B&M’s financial statements report short-term

investments of $100 million, debt of $200 million, and preferred stock of $50 million. B&M’s weighted average cost of capital

management who attempt to maximize stock price.

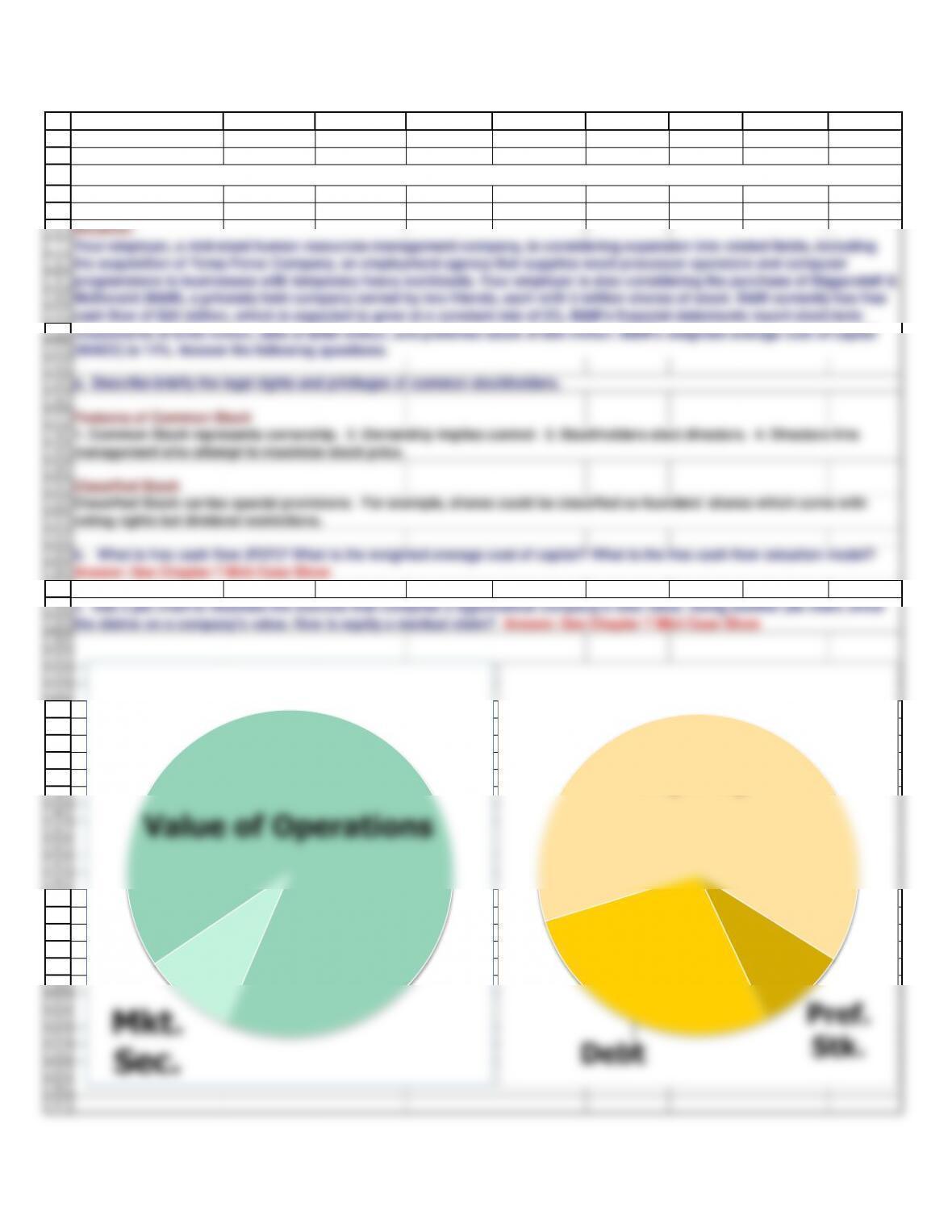

Mkt.

Sec.

Value of Operations

Pref.

Stk.

Debt

58

59

60

61

62

63

64

65

67

68

69

70

71

72

If constant growth begins at Time 0:

78

79

80

81

82

Free cash flow

WACC

Growth

88

89

90

91

92

93

94

95

96

97

98

100

101

102

103

104

105

106

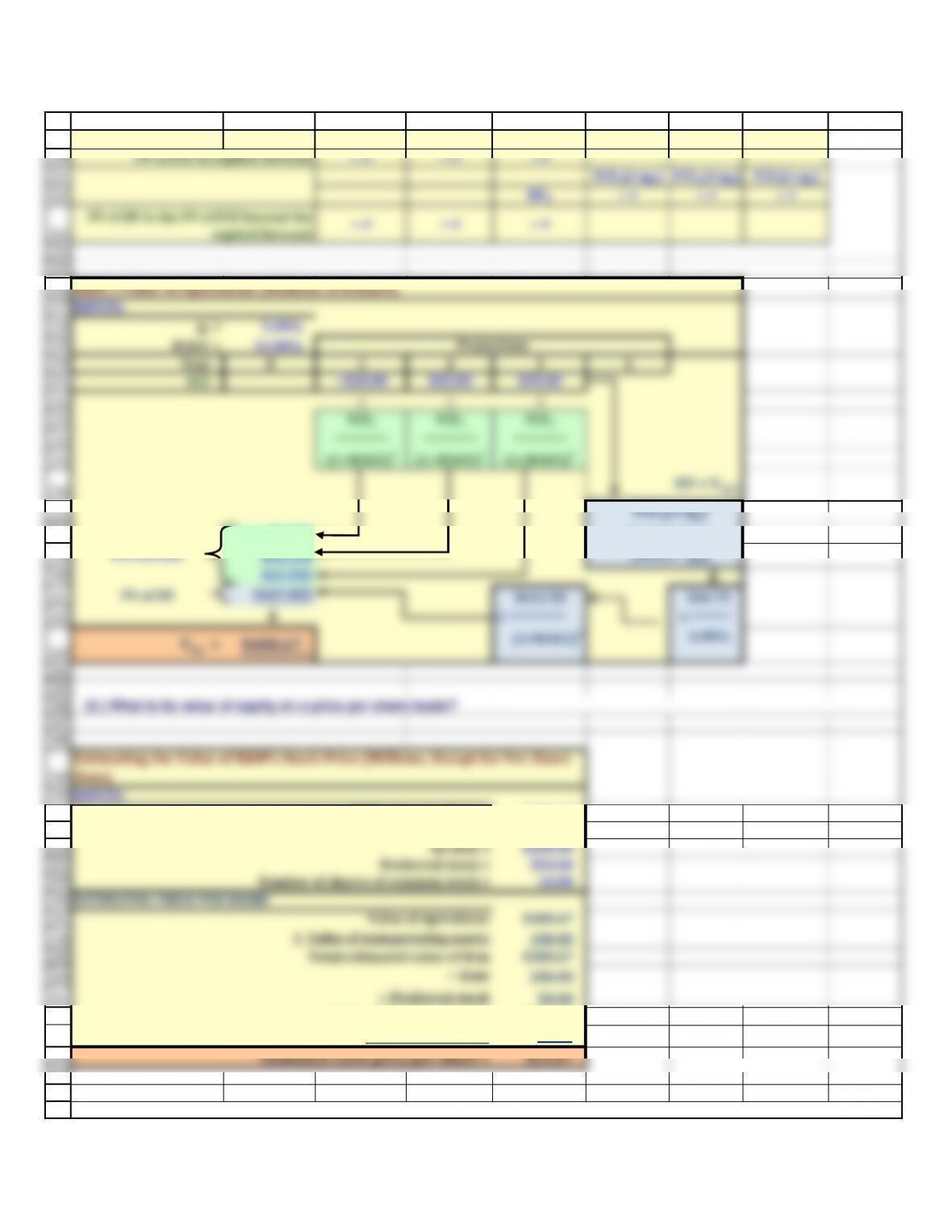

(3) What is its estimated intrinsic value of equity?

111

A B C D E F G H I

If constant growth begins at Time 1:

$100.0

$200.0

$50.0

Number of shares of stock 10.0

(1) What is its estimated value of operations?

FCF1 FCF0 (1+gL)

(WACC-gL) (WACC-gL)

Vop = $420.00

Value of Operation $420.0

Plus Value of Non-operating Assets $100.0

d. Suppose the free cash flow at Time 1 is expected to grow at a constant rate of gL forever. If gL < WACC, what is a formula for

the present value of expected free cash flows when discounted at the WACC? If the most recent free cash flow is expected to

grow at a constant rate of gL forever (and gL < WACC), what is a formula for the present value of expected free cash flows when

discounted at the WACC?

Short-term investments

Debt

e. Use B&M’s data and the free cash flow valuation model to answer the following questions.

Preferred stock

Debt holders have the first claim on corporate value. Preferred stockholders have the next claim and the remaining is left to

=

Vop =

(2) What is its estimated total corporate value?

L

1

0,op gWACC

FCF

V

112

113

114

115

116

117

118

119

120

121

127

128

129

130

138

139

140

141

142

149

150

151

152

153

154

FCF1FCF2FCF3

160

161

162

163

164

A B C D E F G H I

Intrinsic Value of Equity $270.0

Divided by number of shares 10.0

Intrinsic price per share $27.00

Total Corporate Value $520.0

Minus Value of Debt $200.0

Minus Value of Preferred Stock $50.0

Intrinsic Value of Equity $270.0

INPUTS:

Value of operations = $420.00

Value of nonoperating assets = $100.00

− Debt 200.00

− Preferred stock 50.00

Estimated value of equity $270.00

÷ Number of shares 10.00

Estimated stock price per share = $27.00

Explicit forecast:

Year

0 1 2 3 4 5 … t

FCF

FCF1FCF2FCF3FCF3(1+gL) FCF4(1+gL) FCFt(1+gL)

(1.) What is its horizon value (i.e., its value of operations at year three)? What is its current value of operations (i.e., at time

zero)?

common stockholders.

(4) What is its estimated intrinsic stock price per share?

Explicit forecast ends at Year 3, so make the horizon date Year 3, too. (Note: it is possible to make the horizon date Year 2

Estimating the Value of R&R’s Stock Price (Millions, Except for Per Share

Data)

165

166

167

168

169

170

171

172

173

174

175

176

182

183

184

185

186

187

193

194

195

196

197

204

205

206

207

A B C D E F G H I

HV3 = Vop,3 = PV of FCF4 and beyond discounted back to Year 3

Year

0 1 2 3 4 5 … t

FCF

FCF3(1+gL) FCF4(1+gL) FCFt(1+gL)

HV3←↵←↵←↵

Year

0 1 2 3

FCF

−$. $20.00 $35.00

After Year 3, gL = 5%

$36.750

6%

Explicit forecast ends at Year 3, so make the horizon date Year 3, too. (Note: it is possible to make the horizon date Year 2

because FCF3 is known and grows at a constant rate, but it is easy to make mistakes if horizon year is not set equal to end of

explicit forecast.)

Because free cash flows are constant from Year 4 and beyond, we can apply the constant growth model at Year 3:

The general horizon value formula is:

HV3 = Vop,3 =

Lt

t,optgWACC

)g1(FCF

VHV

219

220

221

222

223

224

A B C D E F G H I

FCF

FCF1FCF2FCF3

PV of FCF in explicit forecast ←↵←↵←↵

FCF3(1+gL) FCF4(1+gL) FCFt(1+gL)

HV3←↵←↵←↵

←↵←↵←↵

PV of HV is the PV of FCF beyond the

explicit forecast

268

269

270

271

272

273

274

275

281

282

283

284

285

286

287

288

290

291

292

293

294

295

296

297

304

305

306

307

308

315

316

317

318

319

A B C D E F G H I

INPUTS:

Vop,0 = $480.67

HV3 = $612.50

PV of HV3

=

Vop,0

No Change Actual Forecast

Year 0 1 2 3 4

Inputs

WACC 9.0%

Sales $2,000

NOPAT $99 $107 $112 $117.879

OpCap $1,120 $1,232 $1,331 $1,397.088 #########

FCF −$3. $8.360 $45.738 $48.025

Growth in FCF -164% 447.1% 5.0%

ROIC 8.0% 8.0% 8.0% 8.0%

Percent of value

due to cash flows

beyond Year 3

Percent of value

h. Based on your answer to the previous question, what are two reasons why managers often emphasize short-term

earnings? Answer: See Chapter 7 Mini Case Show

First, calculate the present value of the horizon value. Then divide the Year 0 value of operations by the present value of

the horizon value. This will show what percent of value is due to cash flows occurring 4 or more years in the future.

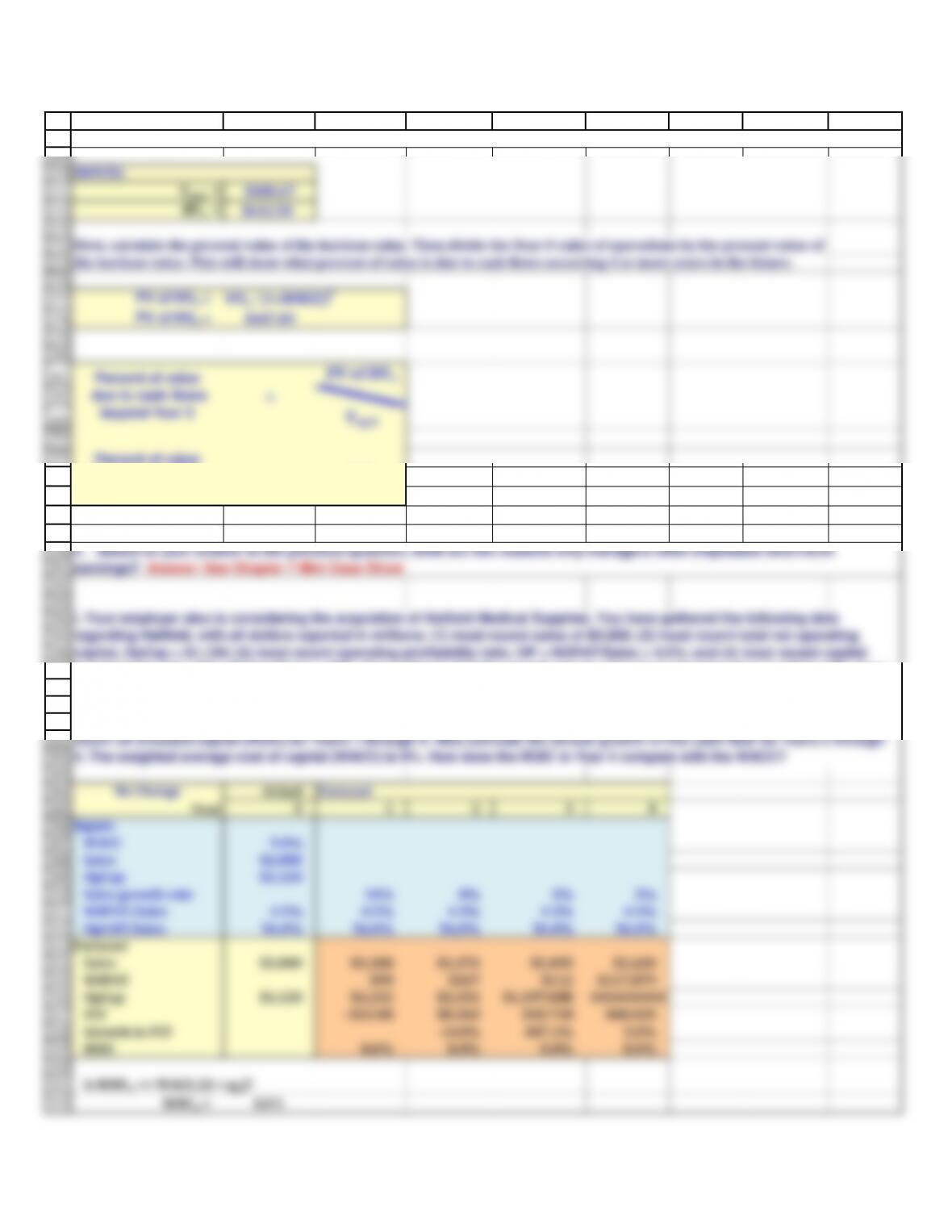

i. Your employer also is considering the acquistion of Hatfield Medical Supplies. You have gathered the following data

regarding Hatfield, with all dollars reported in millions: (1) most recent sales of $2,000; (2) most recent total net operating

capital, OpCap = $1,120; (3) most recent operating profitability ratio, OP = NOPAT/Sales = 4.5%; and (4) most recent capital

requirement ratio, CR = OpCap/Sales = 56%. You estimate that the growth rate in sales from Year 0 to Year 1 will be 10%, from

g. If B&M undertakes the expansion, what percent of B&M’s value of operations at Year 0 is due to cash flows from Years 4

and beyond? Hint: use the horizon value at t = 3 to help answer this question.

323

324

325

326

327

328

329

331

332

333

334

335

336

342

343

344

345

346

347

353

354

355

356

357

358

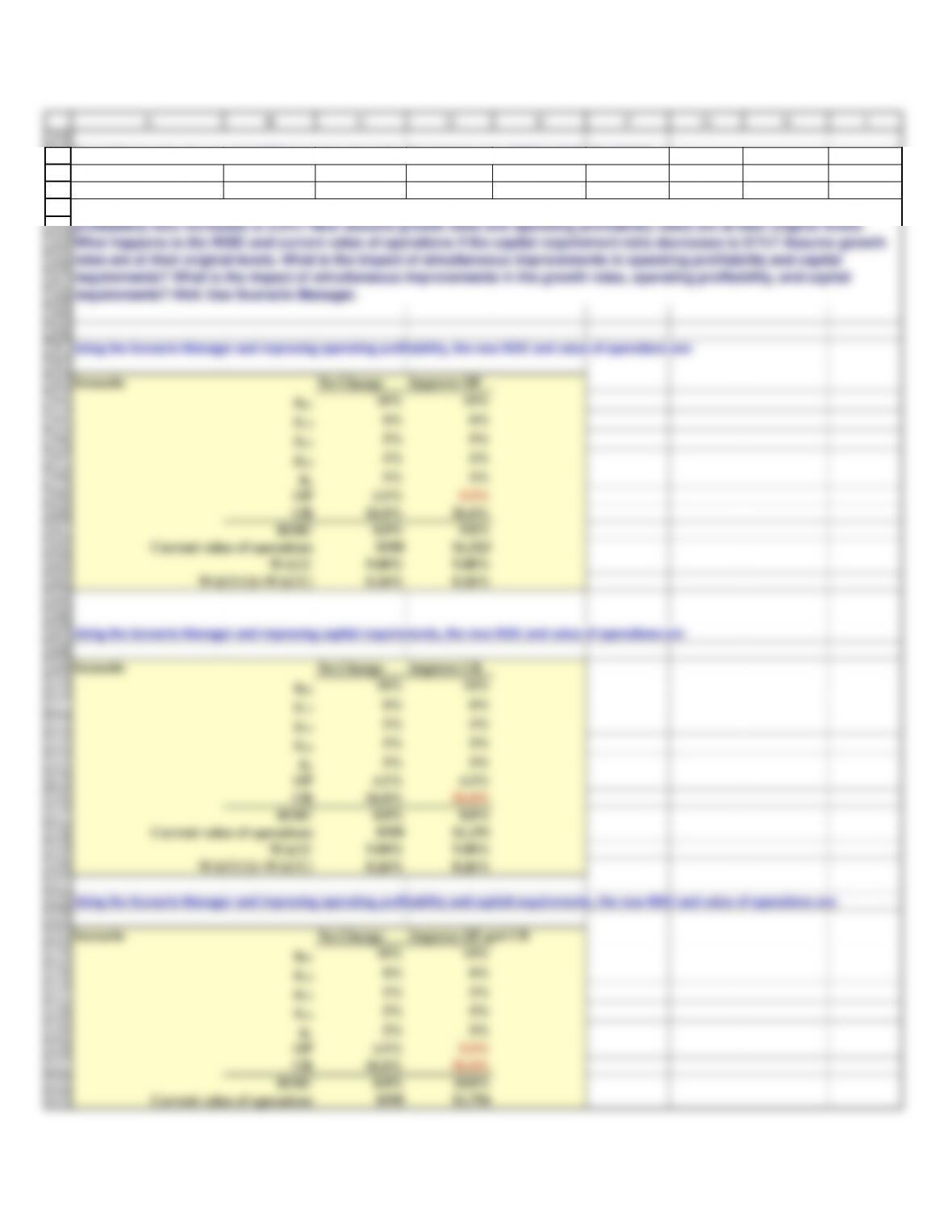

percentage point relative to the original growth rates (including the long-term growth rate)? What can explain this? Hint: Use

364

365

366

367

368

369

g2,3 5% 6%

g3,4 5% 6%

375

376

377

378

A B C D E F G H I

with the current total net operating capital?

WACC/(1+gL)= 8.6%

Horizon Value:

= $1,260.65

Value of Operations:

Current value of operations ≈ $958 < $1,120 = OpCap at horizon

Using the Scenario Manager, the new ROIC and value of operations are:

Scenario No Change Improve Growth

g0,1 10% 11%

g1,2 8% 9%

ROIC

8.0% 8.0%

Current value of operations

$958 $933

WACC

9.00% 9.00%

WACC/(1+WACC)

8.26% 8.26%

Yes, ROIC4 =< WACC/(1 + gL). Therefore, we expect that the value of operations at Year 4 (HV4) should be less than the total net

operating capital at Year 4 (OpCap4).

expected because ROIC4 < WACC/(1+gL).

k. What are value drivers? What happens to the ROIC and current value of operations if expected growth increases by 1

j. What is the horizon value at Year 4? What is the value of operations at Year 0? How does the value of operations compare

The value of operations at Year 0 is less than the total net operating capital at Year 0 because the ROIC is too low when

compared to the WACC. ROIC must be greater than WACC/(1+gL) before the horizon value exceeds the total net operating

�=���+��

��� − ��

379

380

381

382

383

384

385

387

388

389

390

391

g0,1 10% 10%

g1,2 8% 8%

g2,3 5% 5%

g3,4 5% 5%

398

399

400

401

402

9.00% 9.00%

8.26% 8.26%

Using the Scenario Manager and improving capital requirements, the new ROIC and value of operations are:

409

410

g1,2 8% 8%

412

413

gL5% 5%

8.0% 8.8%

$958 $1,191

9.00% 9.00%

420

421

422

423

g0,1 10% 10%

g1,2 8% 8%

g2,3 5% 5%

g3,4 5% 5%

gL5% 5%

430

431

432

433

A B C D E F G H I

Growth hurts value because the ROIC is too low. Growth will only help value if ROIC>WACC/(1+WACC).

Using the Scenario Manager and improving operating profitability, the new ROIC and value of operations are:

gL5% 5%

OP 4.5% 5.5%

CR 56.0% 56.0%

ROIC

8.0% 9.8%

Current value of operations

$958 $1,523

Scenario No Change Improve CR

g0,1 10% 10%

g2,3 5% 5%

g3,4 5% 5%

WACC/(1+WACC)

8.26% 8.26%

Using the Scenario Manager and improving operating profitability and capital requirements, the new ROIC and value of operations are:

OP 4.5% 5.5%

CR 56.0% 51.0%

ROIC

8.0% 10.8%

Current value of operations

$958 $1,756

l. Assume growth rates are at their original levels. What happens to the ROIC and current value of operations if the operating

profitability ratio increases to 5.5%? Now assume growth rates and operating profitability ratios are at their original levels.

What happens to the ROIC and current value of operations if the capital requirement ratio decreases to 51%? Assume growth

requirements? What is the impact of simultaneous improvements in the growth rates, operating profitability, and capital

requirements? Hint: Use Scenario Manager.

434

435

436

437

438

439

440

442

443

444

445

446

9.00% 9.00%

8.26% 8.26%

453

454

455

464

465

466

467

468

475

476

477

478

479

486

487

488

489

A B C D E F G H I

g0,1 10% 11%

WACC

9.00% 9.00%

WACC/(1+WACC)

8.26% 8.26%

Using the Scenario Manager and improving growth rates, operating profitability, and capital requirements, the new ROIC and value of operations are

Scenario No Change Improve All

g1,2 8% 9%

g2,3 5% 6%

g3,4 5% 6%

gL5% 6%

OP 4.5% 5.5%

D1D2DN

( 1 + rs ) ( 1 + rs ) 2 ( 1 + rs ) N

+

+

. . . .

m. What insight does the free cash flow valuation model give provide us about possible reasons for market volatility? Hint:

Look at the value of operations for the combinations of ROIC and gL in the previous questions.

n. (1.) Write out a formula that can be used to value any dividend-paying stock, regardless of its dividend pattern.

Naturally, trying to estimate an infinite series of dividends and interest rates forever would be a tremendously difficult task.

Now, we are charged with the purpose of finding a valuation model that is easier to predict and construct. That simplification

comes in the form of valuing stocks on the premise that they have a constant growth rate.

Here is the basic dividend valuation equation:

�=

490

491

492

493

494

495

496

497

498

499

500

501

502

503

504

505

A B C D E F G H I

D1

( rs – gL )

In this equation, the long-run growth rate (g) can be approximated by multiplying the firm’s return on assets by the retention

ratio. Generally speaking, the long-run growth rate of a firm is likely to fall between 5% and 8% a year.

In this stock valuation model, we first assume that the dividend and stock will grow forever at a constant growth rate.

Naturally, assuming a constant growth rate for the rest of eternity is a rather bold statement. However, considering the

implications of imperfect information, information asymmetry, and general uncertainty, perhaps our assumption of constant

growth is reasonable. It is reasonable to guess that a given firm will experience ups and downs throughout its life. By

assuming constant growth, we are trying to find the average of the good times and the bad times, and we assume that we will

see both scenarios over the firm’s life. In addition to assuming a constant growth rate, we will be estimating a long-term

required return for the stock. By assuming these variables are constant, our price equation for common stock simplifies to the

n. (2.) What is a constant growth stock? How are constant growth stocks valued?

�=