Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

46

47

A B C D E F

10/28/2015

Amount invested $1,000

Amount received in one year $1,060

Dollar return (Profit) $60

Rate of return = Profit/Investment = 6%

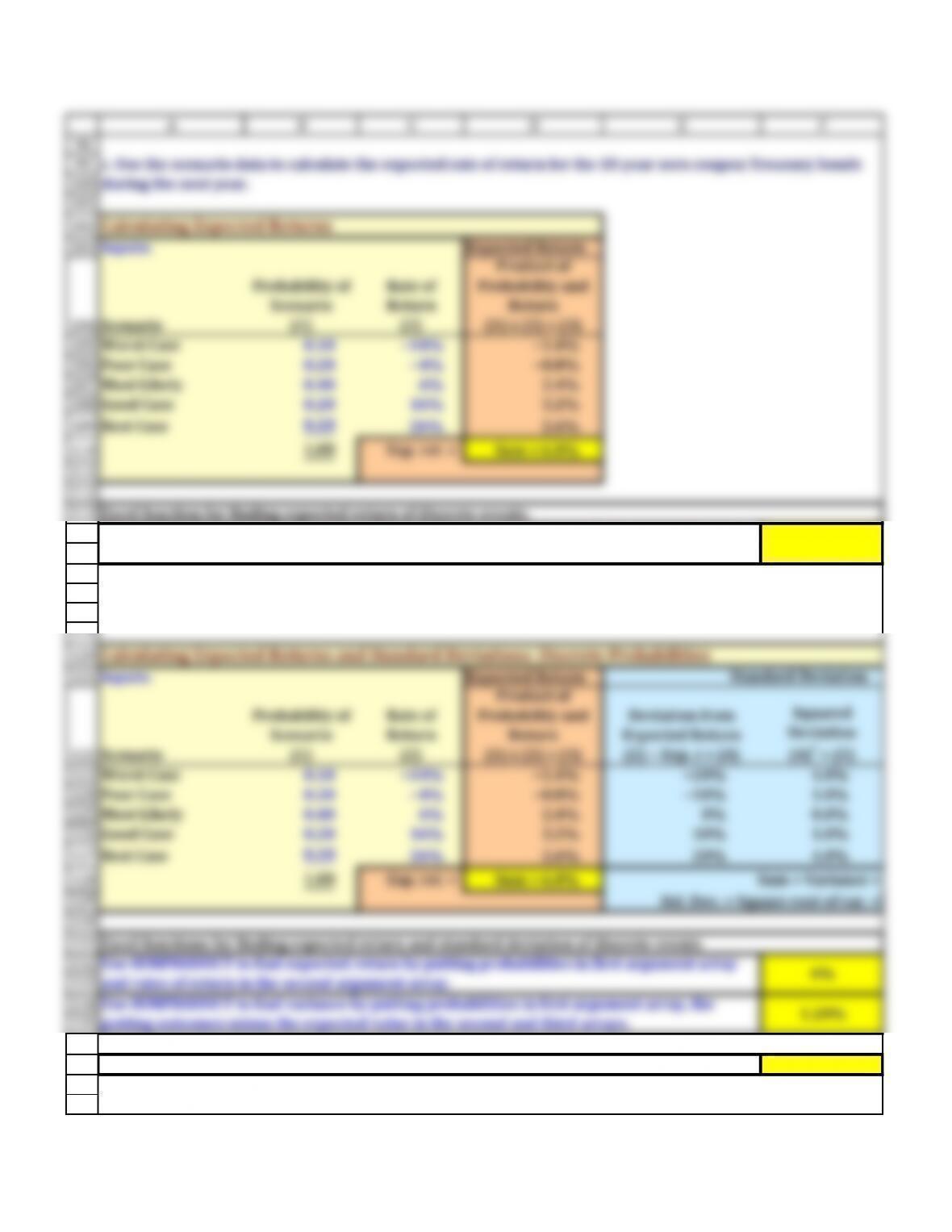

Worst Case 0.10 −%

Poor Case 0.20 −%

Good Case 0.20 16%

Best Case 0.10 26%

Return on a

10-Year Zero

Coupon

Treasury

Bond During

Next Year

Probability of

Scenario

CHAPTER 6 MINI CASE

a. What are investment returns? What is the return on an investment that costs $1,000 and is sold after 1 year

for $1,060?

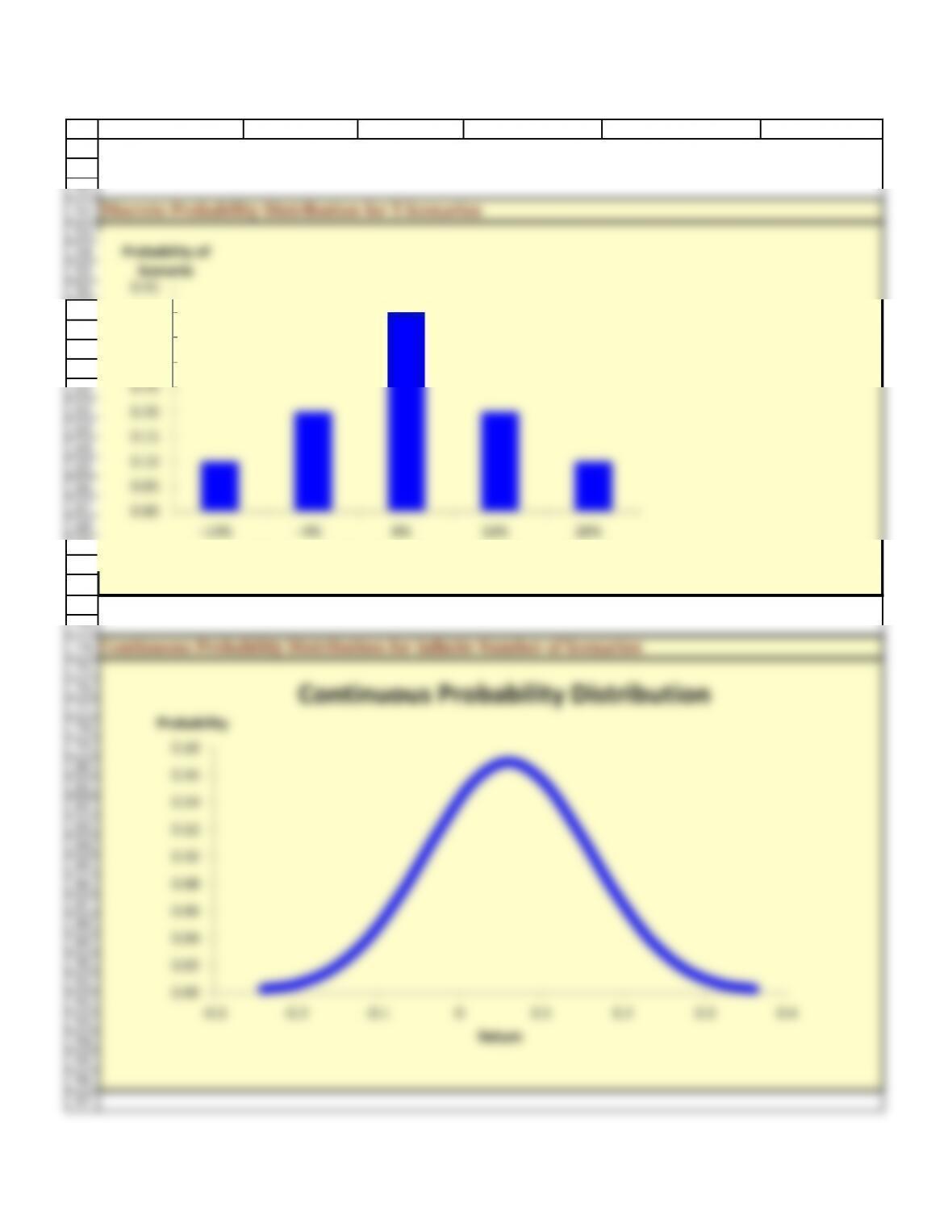

b. Graph the probability distribution for the 5 scenarios during the next year for the 10-year zero coupon

bonds. What might the graph of the probability distribution look like if there were an infinite number of

scenarios (i.e., if it were a continuous distribution and not a discrete distribution)?

You have also gathered historical returns for the past 10 years for Blandy, Gourmange Corporation (a

producer of gourmet specialty foods), and the stock market.

The risk-free rate is 4% and the market risk premium is 5%.

Assume that you recently graduated and landed a job as a financial planner with Cicero Services, an

investment advisory company. Your first client recently inherited some assets and has asked you to evaluate

them. The client presently owns a bond portfolio with $1 million invested in zero coupon Treasury bonds

that mature in 10 years. The client also has $2 million invested in the stock of Blandy, Inc., a company that

produces meat-and-potatoes frozen dinners. Blandy’s slogan is Solid food for shaky times.

Unfortunately, Congress and the President are engaged in an acrimonious dispute over the budget and the

debt ceiling. The outcome of the dispute, which will not be resolved until the end of the year, will have a big

impact on interest rates one year from now. Your first task is to determine the risk of the client’s bond

portfolio. After consulting with the economists at your firm, you have specified 5 possible scenarios for the

resolution of the dispute at the end of the year. For each scenario, you have estimated the probability of the

scenario occurring and the impact on interest rates and bond prices if the scenario occurs. Given this

information, you have calculated the rate of return on 10-year zero coupon Treasury bonds for each scenario.

The probabilities and returns are shown further below.

Scenario

49

50

51

52

53

A B C D E F

Discrete Probability Distribution for 5 Scenarios

98

99

100

101

102

103

104

106

107

108

109

A B C D E F

Calculating Expected Returns

Inputs: Expected Return

Scenario

Probability of

Scenario

(1)

Rate of

Return

(2)

Product of

Probability and

Return

(1) x (2) = (3)

Poor Case 0.20 −% −.%

Most Likely 0.40 6% 2.4%

Good Case 0.20 16% 3.2%

Best Case 0.10 26% 2.6%

c. Use the scenario data to calculate the expected rate of return for the 10-year zero coupon Treasury bonds

during the next year.

140

141

142

143

144

145

146

147

148

149

150

151

152

153

159

A B C D E F

Year Market Blandy Gourmange

130% 26% 47%

27% 15% -54%

318% -14% 15%

4 -22% -15% 7%

5 -14% 2% -28%

610% -18% 40%

Standard deviation of returns: 20.1% 25.2% 38.6%

e. Your client has decided that the risk of the bond portfolio is acceptable and wishes to leave it as it is. Now

your client has asked you to use historical returns to estimate the standard deviation of Blandy’s stock

returns. (Note: Many analysts use 4 to 5 years of monthly returns to estimate risk and many use 52 weeks of

weekly returns; some even use a year or less of daily returns. For the sake of simplicity, use Blandy’s

annual returns.)

Stock Returns

185

186

187

188

189

190

191

192

193

194

195

196

202

203

204

205

206

207

213

A B C D E F

10 28% 75% 39.8%

Average return: 6.4% 9.2% 7.1%

Standard deviation of returns: 25.2% 38.6% 22.2%

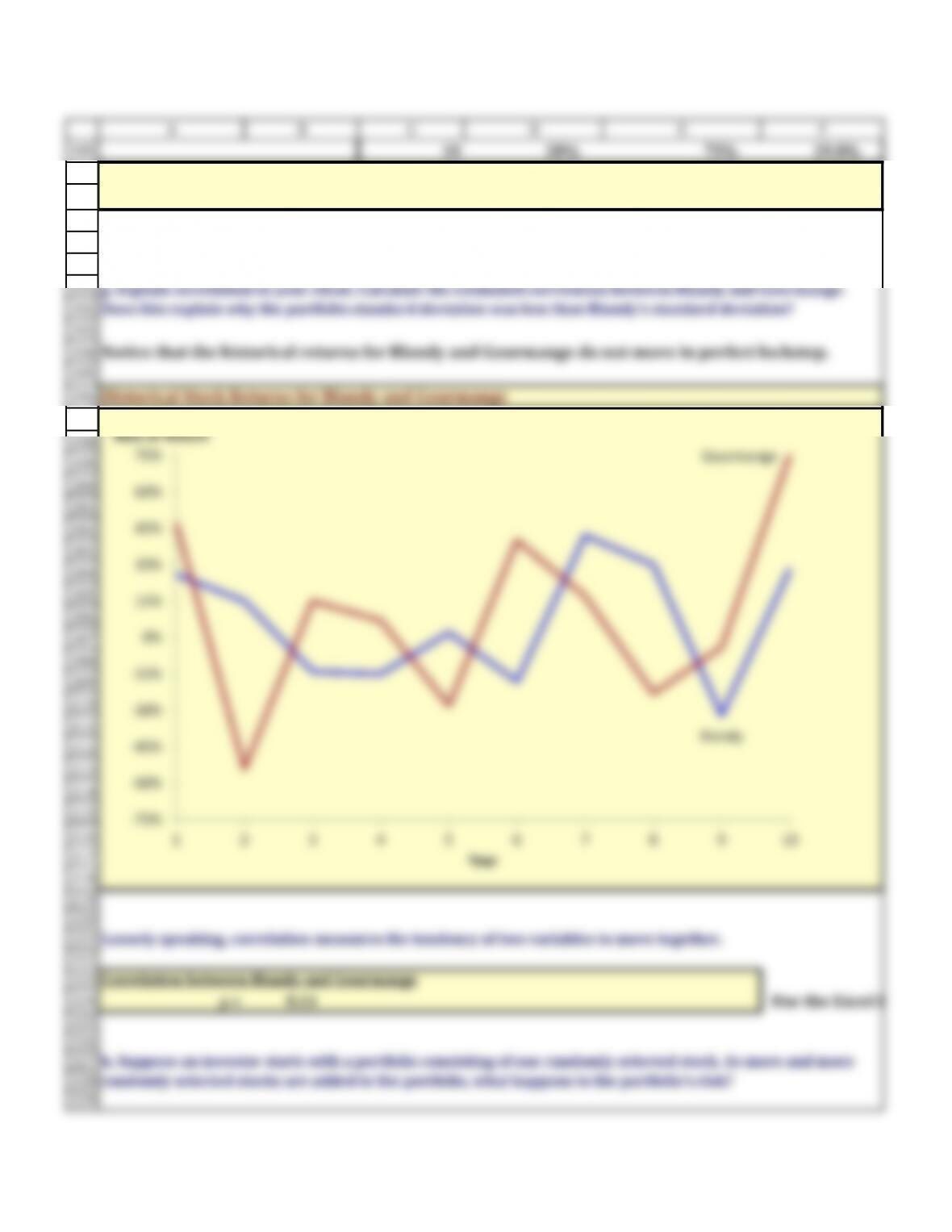

Notice that the historical returns for Blandy and Gourmange do not move in perfect lockstep.

g. Explain correlation to your client. Calculate the estimated correlation between Blandy and Gourmange.

Does this explain why the portfolio standard deviation was less than Blandy’s standard deviation?

Historical Stock Returns for Blandy and Gourmange

-60%

0%

15%

30%

45%

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267

268

269

270

271

272

273

274

275

276

277

278

A B C D E F

Beta for Stock i = bi = riM(si/sM)

rRF The risk-free rate. It varies over time, but is constant for all firms at a given time.

RPM

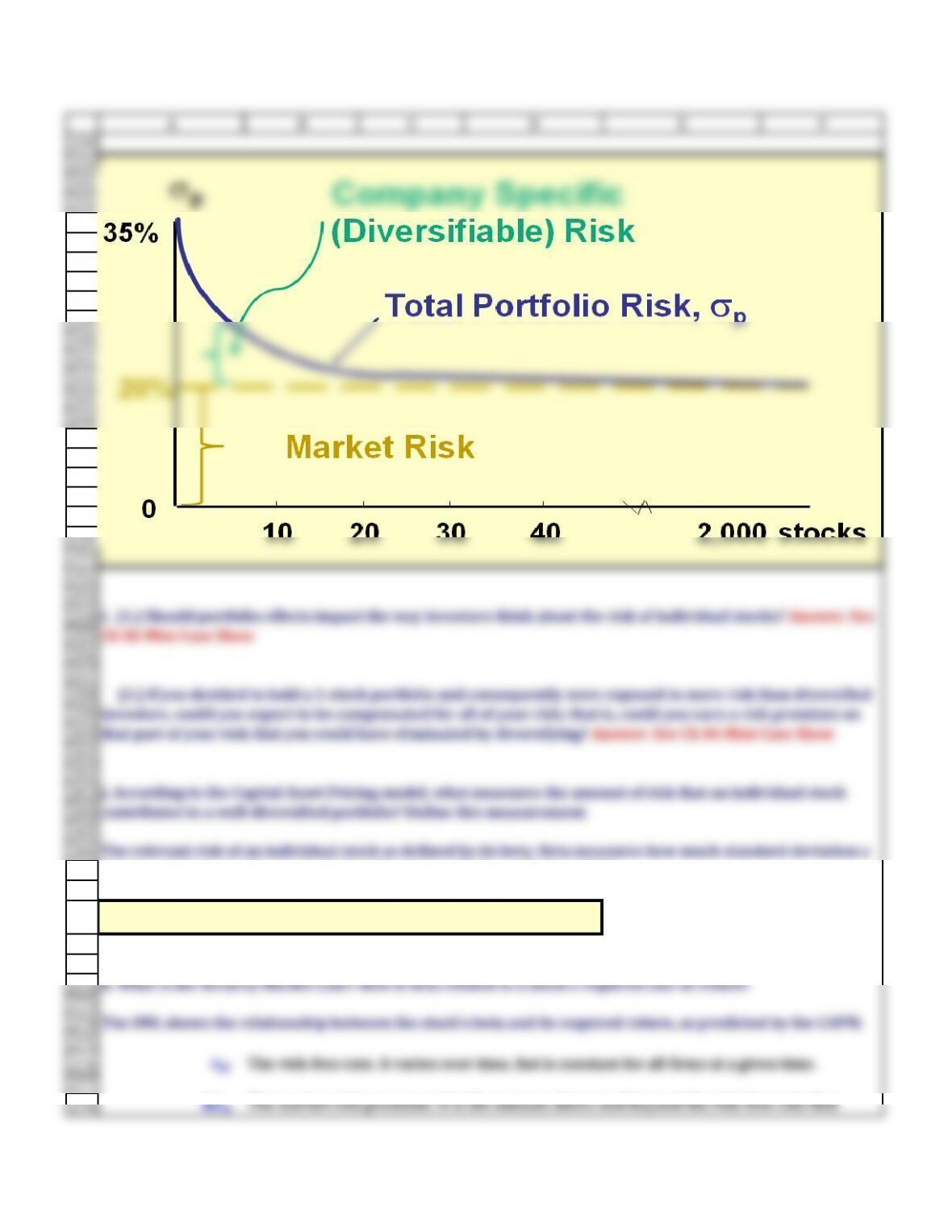

i. (1.) Should portfolio effects impact the way investors think about the risk of individual stocks? Answer: See

Ch 06 Mini Case Show

(2.) If you decided to hold a 1-stock portfolio and consequently were exposed to more risk than diversified

investors, could you expect to be compensated for all of your risk; that is, could you earn a risk premium on

that part of your risk that you could have eliminated by diversifying? Answer: See Ch 06 Mini Case Show

The relevant risk of an individual stock as defined by its beta. Beta measures how much standard deviation a

stock contributes to the standard deviation of a well-diversified portfolio.

k. What is the Security Market Line? (ow is beta related to a stock’s required rate of return?

The SML shows the relationship between the stock's beta and its required return, as predicted by the CAPM.

j. According to the Capital Asset Pricing model, what measures the amount of risk that an individual stock

contributes to a well-diversified portfolio? Define this measurement.

The market risk premium. It is the amount above and beyond the risk-free rate that

investor require to induce them to take on the risk of the stock market. It varies over

time, but is constant for all firms at a given time. Note: the market risk premium can be

279

280

281

282

283

284

285

286

287

288

289

290

291

292

293

295

296

297

298

299

300

301

302

303

311

312

313

314

316

317

319

320

321

322

323

324

325

A B C D E F

biThe beta of stock i. It varies over time, and varies from firm to firm.

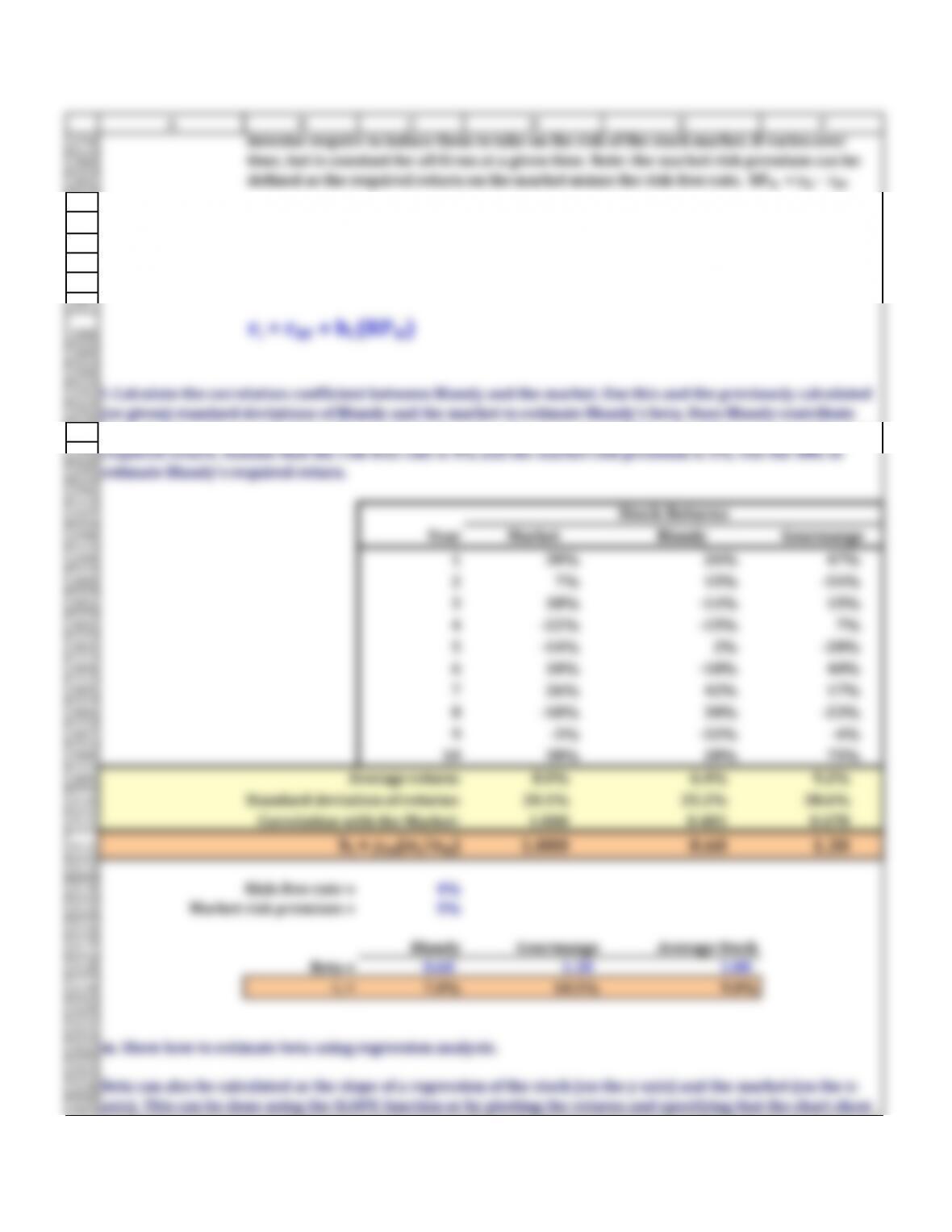

ri = rRF + bi (RPM)

Year Market Blandy Gourmange

130% 26% 47%

27% 15% -54%

318% -14% 15%

4 -22% -15% 7%

5 -14% 2% -28%

Correlation with the Market: 1.000 0.481 0.678

bi = riM(si/sM)1.000 0.60 1.30

Risk-free rate = 4%

Blandy Gourmange Average Stock

ri = 7.0% 10.5% 9.0%

Stock Returns

l. Calculate the correlation coefficient between Blandy and the market. Use this and the previously calculated

or given standard deviations of Blandy and the market to estimate Blandy’s beta. Does Blandy contribute

more or less risk to a well-diversified portfolio than does the average stock? Use the SML to estimate Blandy’s

estimate Blandy’s required return.

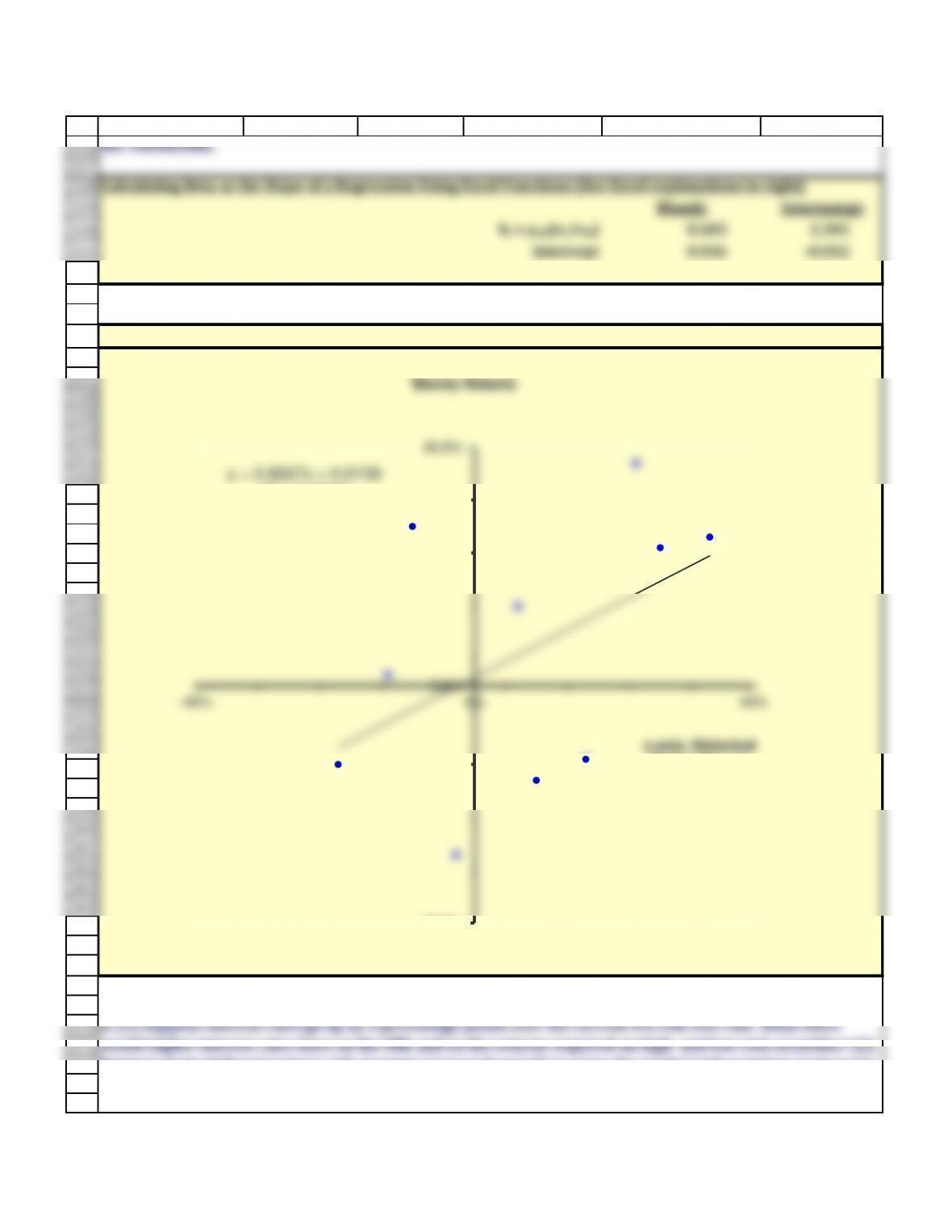

m. Show how to estimate beta using regression analysis.

The SML predicts stock i's required return to be:

Beta can also be calculated as the slope of a regression of the stock (on the y-axis) and the market (on the x-

axis). This can be done using the SLOPE function or by plotting the returns and specifying that the chart show

the TRENDLINE.

The market risk premium. It is the amount above and beyond the risk-free rate that

investor require to induce them to take on the risk of the stock market. It varies over

time, but is constant for all firms at a given time. Note: the market risk premium can be

defined as the required return on the market minus the risk-free rate, RPM = rM - rRF

326

327

328

329

330

331

332

333

334

337

338

339

340

341

342

343

344

345

346

347

348

349

350

351

352

353

354

355

356

357

358

359

360

361

362

363

364

365

370

371

372

373

374

A B C D E F

Blandy Gourmange

bi = riM(si/sM)0.603 1.301

Intercept 0.016 -0.012

R squared 0.232 0.460

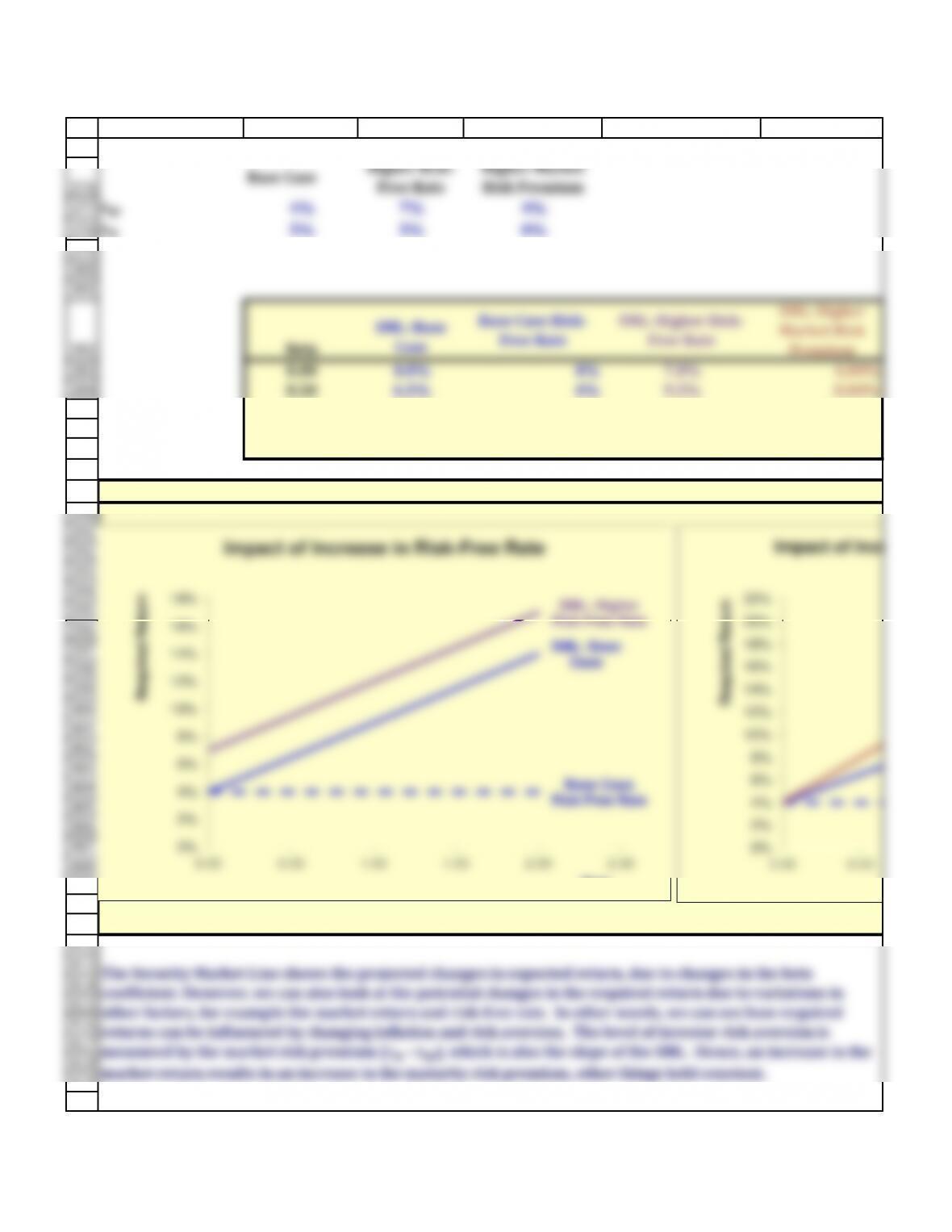

n. (1) Suppose interest rates go up by 3 percentage points over the current 4% risk-free rate. What effect

would higher interest rates have on the SML and on the returns required on high- and low-risk securities? (2)

Suppose instead that investors’ risk aversion increased enough to cause the market risk premium to increase

by 3 percentage points. (Assume the risk-free rate remains constant.) What effect would this have on the SML

and on returns of high- and low-risk securities?

Calculating Beta as the Slope of a Regression Using Excel Functions (See Excel explanations to right)

axis). This can be done using the SLOPE function or by plotting the returns and specifying that the chart show

the TRENDLINE.

y = 0.6027x + 0.0158

R² = 0.2316

-45.0%

0.0%

45.0%

-45% 0% 45%

Blandy Returns

x-axis: Historical

Market Returns

375

376

377

378

379

380

381

382

383

384

385

386

387

389

390

391

392

393

394

395

396

397

398

399

400

401

402

403

404

405

406

407

408

409

410

411

412

A B C D E F

Base Case

Higher Risk-

Free Rate

Higher Market

Risk Premium

rRF 4% 7% 4%

rM5% 5% 8%

Beta

SML: Base

Case

Base Case Risk-

Free Rate

SML: Higher Risk-

Free Rate

SML: Higher

Market Risk

Premium

0.00 4.0% 4% 7.0% 4.00%

0.50 6.5% 4% 9.5% 8.00%

1.00 9.0% 4% 12.0% 12.00%

1.50 11.5% 4% 14.5% 16.00%

2.00 14.0% 4% 17.0% 20.00%

Changes to Inputs for the Security Market Line

SML: Base

Case

Base Case

Risk-Free Rate

SML: Higher

Risk-Free Rate

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0.00 0.50 1.00 1.50 2.00 2.50

Required Return

Beta

Impact of Increase in Risk-Free Rate

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

0.00 0.50

Required Return

Impact of Increase

421

422

423

424

425

426

427

428

429

430

431

433

435

436

437

438

439

442

443

444

445

447

448

449

450

451

452

453

455

457

458

459

460

461

462

463

464

465

A B C D E F

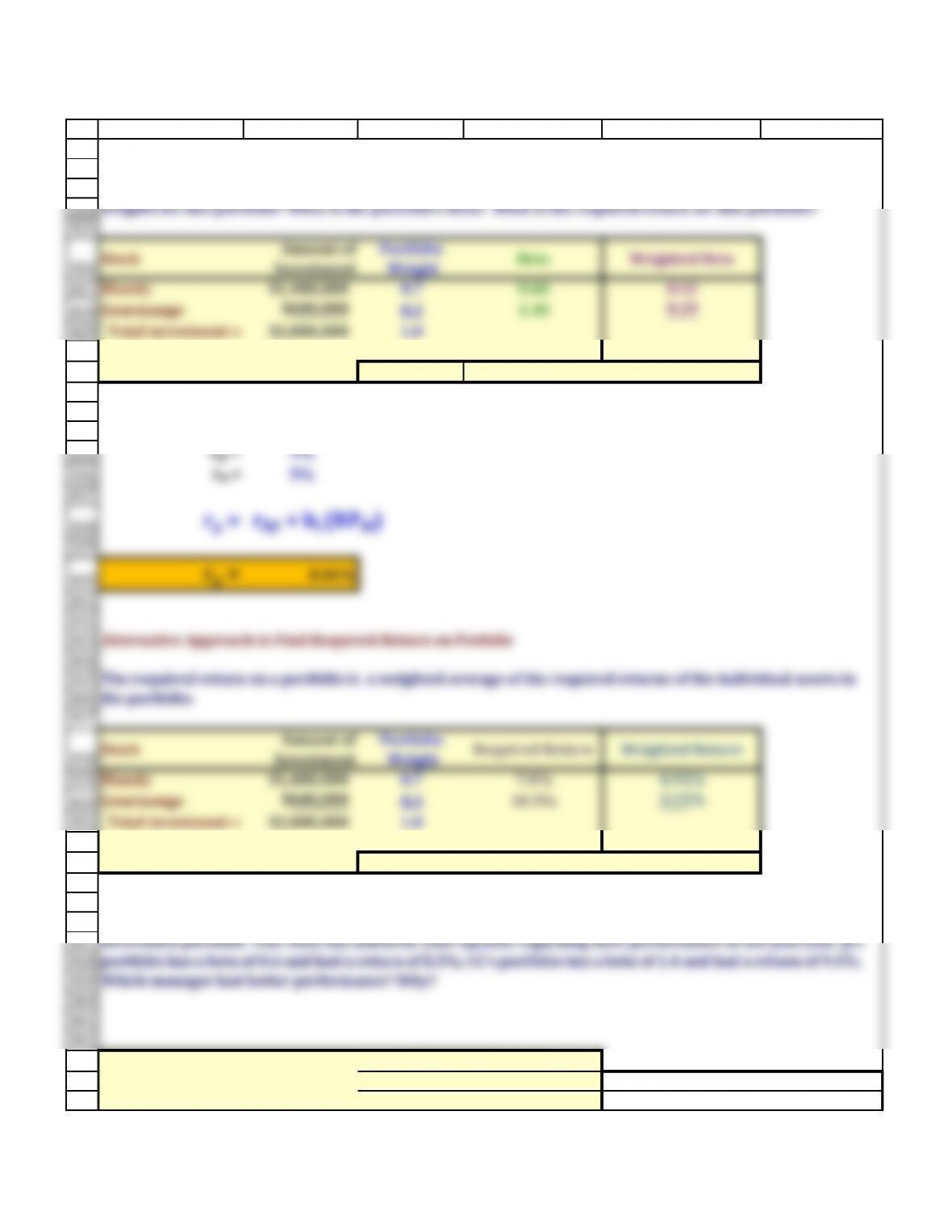

Stock

Amount of

Investment

Portfolio

Weight

Beta Weighted Beta

Blandy $1,400,000 0.7 0.60 0.42

Gourmange $600,000 0.3 1.30 0.39

Total investment = $2,000,000 1.0

Portfolio's Beta = 0.81

rRF = 4%

rM = 5%

rp = rRF + bi (RPM)

Alternative Approach to Find Required Return on Porfolio

Stock

Amount of

Investment

Portfolio

Weight

Required Return Weighted Return

Blandy $1,400,000 0.7 7.0% 4.91%

Gourmange $600,000 0.3 10.5% 3.15%

Total investment = $2,000,000 1.0

Portfolio's Return = 8.06%

JJ CC

Portfolio beta = 0.7 1.4 0 2

o. Your client decides to invest $1.4 million in Blandy stock and $0.6 million in Gourmange stock. What are the

weights for this portfolio? What is the portfolio’s beta? What is the required return for this portfolio?

The required return on a portfolio is a weighted average of the required returns of the individual assets in

Portfolio Manager

Additonal data for graph

diversified portfolio. Your boss has asked for your opinion regarding their performance in the past year. JJ’s

portfolio has a beta of . and had a return of .%; CC’s portfolio has a beta of . and had a return of .%.

Which manager had better performance? Why?